First Brands Group debt targeted by Apollo Global Management - report

Introduction & Market Context

Chewy Inc. (NYSE:CHWY) released its Q2 2025 financial results on September 10, 2025, showcasing solid growth across key metrics, though shares fell sharply in premarket trading. The online pet retailer reported an 8.6% year-over-year increase in net sales to $3.104 billion, while maintaining strong profitability with an adjusted EBITDA margin of 5.9%.

Despite the positive results, Chewy’s stock dropped 7.39% to $38.99 in premarket trading, continuing a pattern seen after its Q1 results when shares declined despite exceeding analyst expectations. The company’s stock has traded within a 52-week range of $26.28 to $48.62.

Quarterly Performance Highlights

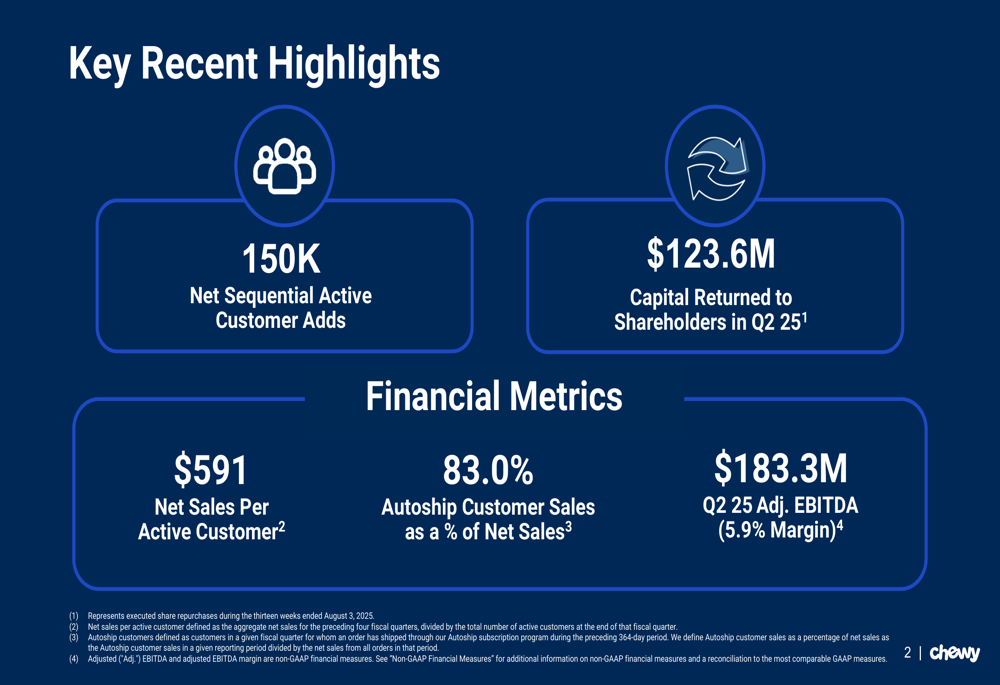

Chewy’s Q2 2025 presentation highlighted several positive developments, including the addition of 150,000 net new active customers during the quarter, bringing its total active customer base to 20.9 million, up from 20.0 million in Q2 2024.

As shown in the following key metrics summary:

The company’s Autoship program, which provides automatic reordering of pet supplies, continues to be a significant growth driver, representing 83.0% of total net sales in Q2 2025. Net sales per active customer (NSPAC) reached $591, reflecting the company’s success in increasing customer spending over time.

Chewy also returned $123.6 million to shareholders during the quarter, demonstrating its commitment to delivering shareholder value while maintaining strong operational performance.

Detailed Financial Analysis

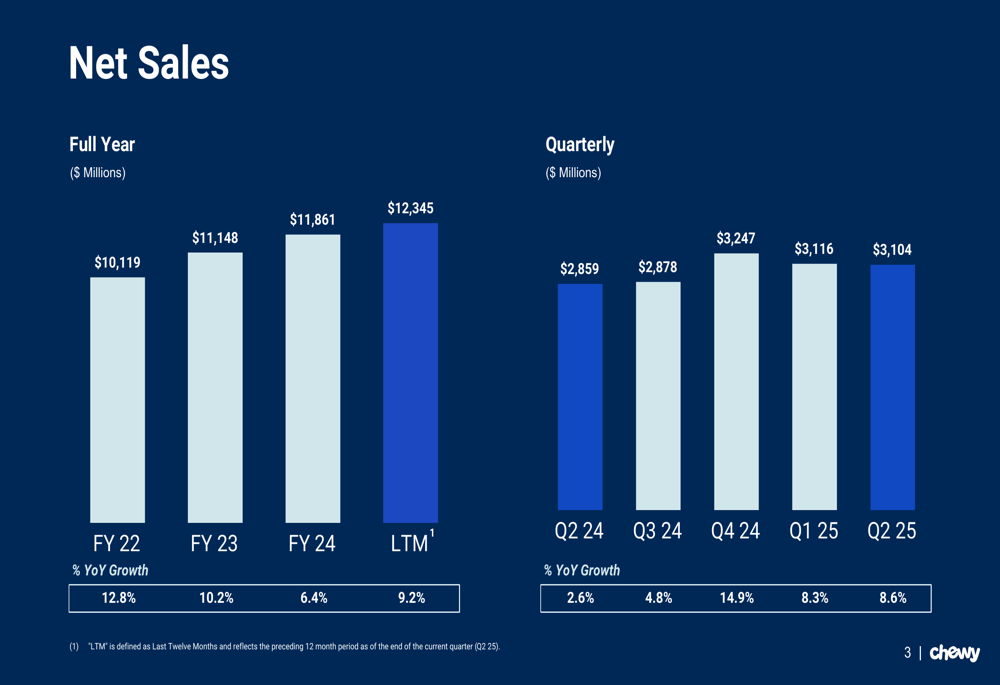

Chewy’s net sales have shown consistent growth over recent years, with the latest quarter continuing this positive trend:

The company’s Q2 2025 net sales of $3.104 billion represent an 8.6% increase year-over-year, outpacing the 2.6% growth seen in Q2 2024. On a trailing twelve-month basis, Chewy has generated $12.345 billion in net sales, reflecting 9.2% year-over-year growth.

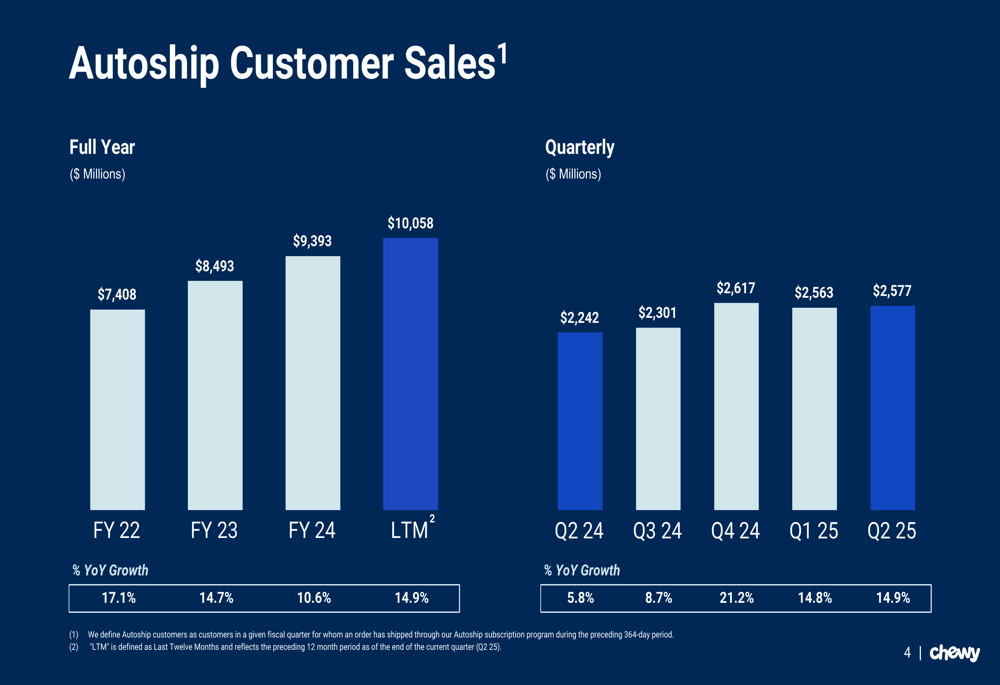

Particularly impressive is the performance of Chewy’s Autoship program, which continues to gain traction:

Autoship customer sales reached $2.577 billion in Q2 2025, representing 14.9% year-over-year growth, significantly outpacing the overall sales growth rate. This subscription-like service has become increasingly important to Chewy’s business model, now accounting for 83.0% of total net sales.

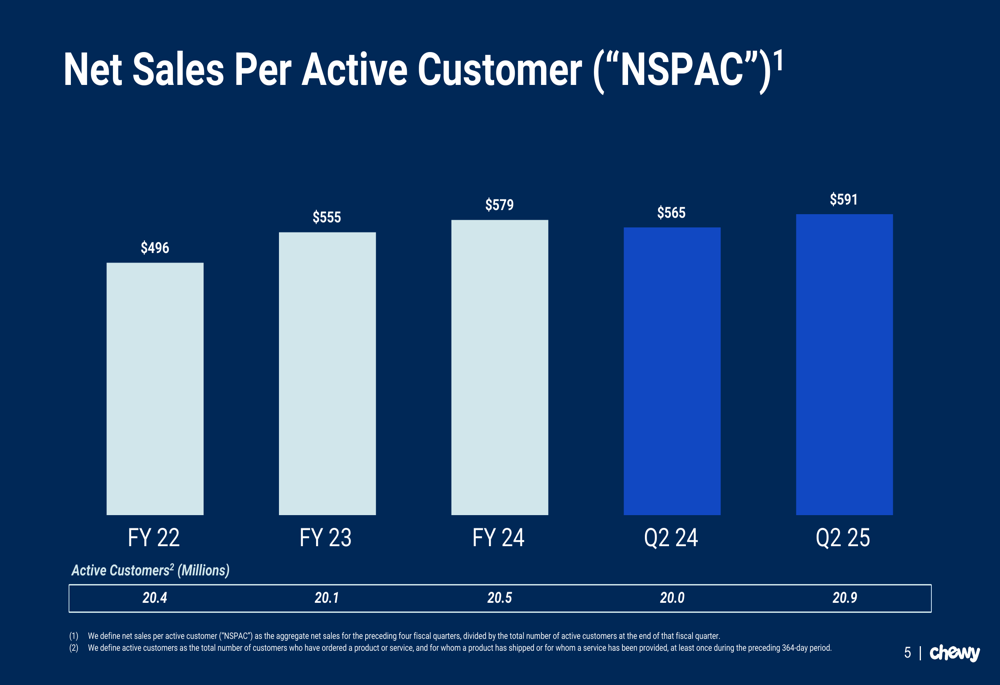

The company has also successfully increased customer value over time:

Net sales per active customer (NSPAC) reached $591 in Q2 2025, up from $565 in Q2 2024 and continuing a multi-year upward trend from $496 in FY 2022. This metric demonstrates Chewy’s ability to extract more value from its customer base through effective cross-selling and retention strategies.

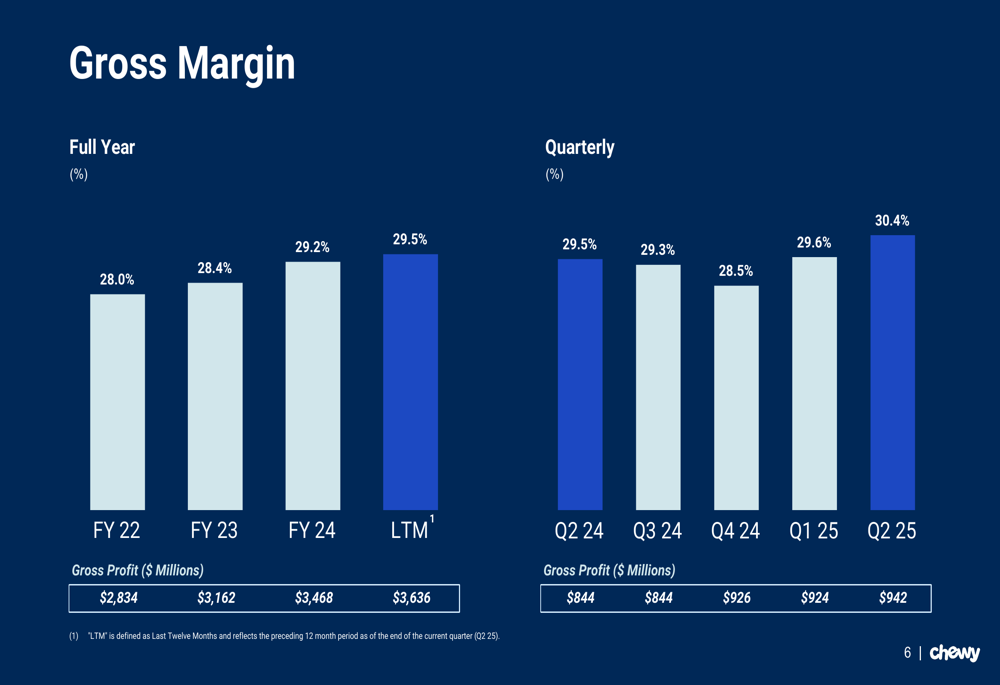

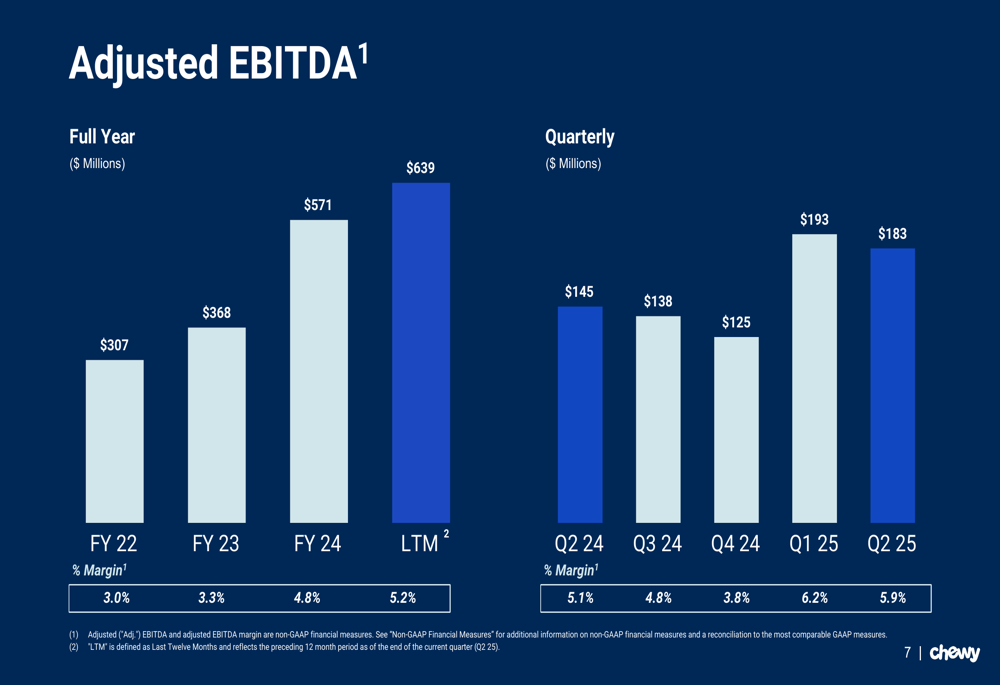

Profitability metrics have also shown improvement:

Adjusted EBITDA for Q2 2025 was $183.3 million, representing a 5.9% margin. While this is slightly lower than the 6.2% margin achieved in Q1 2025, it remains significantly higher than the 3.0% margin reported in FY 2022, demonstrating the company’s progress in improving operational efficiency.

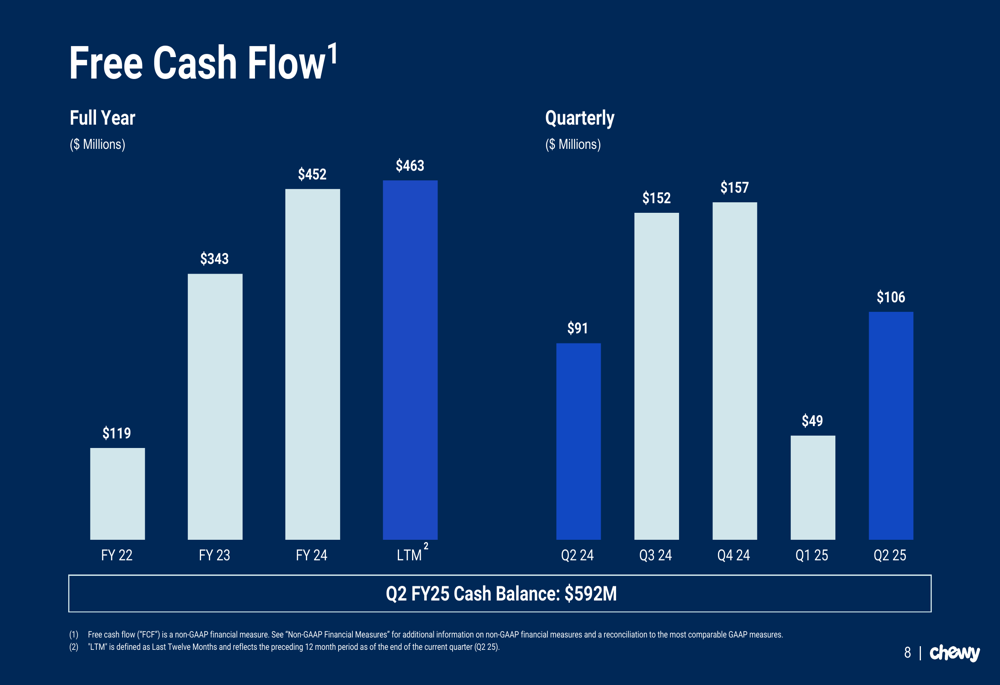

Chewy’s cash generation capabilities remain strong:

The company reported free cash flow of $106 million for Q2 2025, up from $91 million in Q2 2024. On a trailing twelve-month basis, free cash flow reached $463 million, compared to $452 million for FY 2024. Chewy ended the quarter with a cash balance of $592 million, providing financial flexibility for future investments and shareholder returns.

Forward-Looking Statements

Looking ahead, Chewy provided guidance for both Q3 2025 and the full fiscal year:

For Q3 2025, the company expects net sales between $3.07 billion and $3.10 billion, representing approximately 7-8% year-over-year growth. Adjusted diluted EPS is projected to be between $0.28 and $0.33.

For the full fiscal year 2025, Chewy anticipates net sales of $12.5 billion to $12.6 billion, with an adjusted EBITDA margin of 5.4% to 5.7%, showing continued confidence in its ability to maintain profitability while growing revenue.

Market Reaction & Conclusion

The sharp decline in Chewy’s stock price following the release of its Q2 2025 results appears somewhat disconnected from the company’s operational performance. With consistent growth across key metrics, improving profitability, and strong cash generation, the fundamentals remain solid.

This disconnect may reflect broader market concerns about consumer discretionary spending in the current economic environment rather than company-specific issues. It’s worth noting that Chewy experienced a similar stock decline following its Q1 2025 results despite exceeding analyst expectations at that time.

Investors will likely be watching closely to see if Chewy can deliver on its Q3 and full-year guidance, particularly regarding its ability to maintain margin expansion while continuing to grow its active customer base and average customer spending. The company’s consistent execution on its Autoship program and its ability to return capital to shareholders while investing in growth initiatives will remain key factors in its long-term success.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.