Fubotv earnings beat by $0.10, revenue topped estimates

Introduction & Market Context

Chord Energy (NASDAQ:CHRD) presented its corporate strategy on August 6, 2025, highlighting its position as a premier Williston Basin operator focused on enhancing free cash flow generation. The presentation comes after the company reported Q1 2025 results that showed mixed performance, with earnings per share of $4.04 exceeding analyst expectations while revenue of $1.1 billion fell short of forecasts.

Following the presentation, Chord Energy’s stock saw a modest increase of 1% in aftermarket trading to $107.50, building on its regular session closing price of $106.44. The stock has traded between $79.83 and $157.85 over the past 52 weeks, reflecting the volatility in the energy sector.

Executive Summary

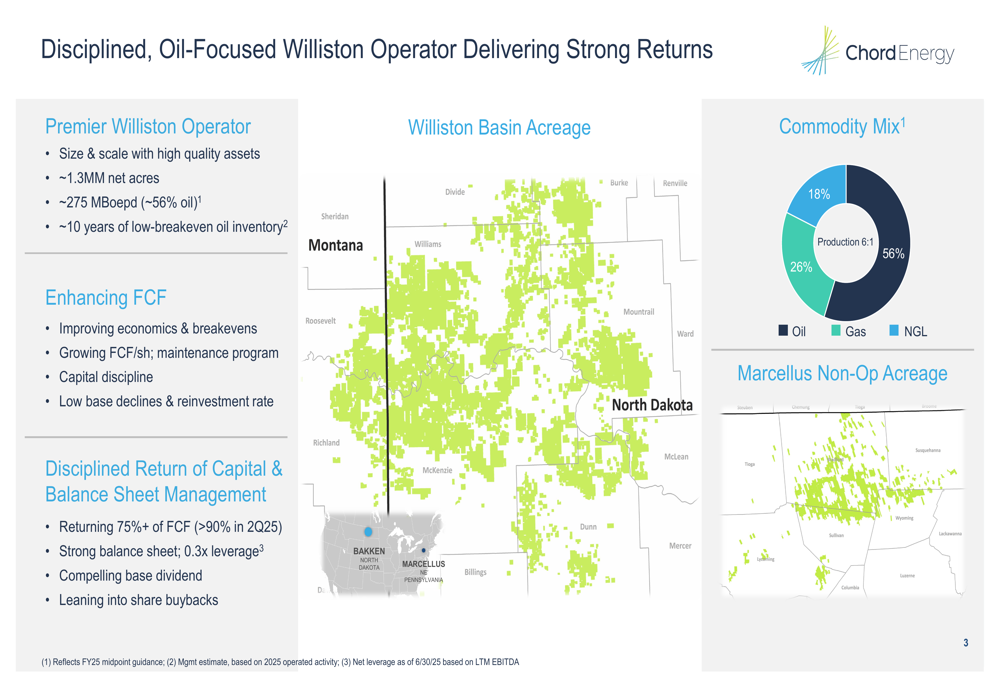

Chord Energy’s presentation emphasized its disciplined approach to capital allocation and operational efficiency, which has enabled the company to enhance free cash flow generation despite challenging oil price conditions. With approximately 1.3 million net acres in the Williston Basin and production of around 275,000 barrels of oil equivalent per day (56% oil), Chord has established itself as a significant player in the region.

The company highlighted its 20% increase in free cash flow compared to original 2025 guidance, driven by higher oil production, lower capital expenditures, and reduced operating expenses. Additionally, Chord has maintained a strong balance sheet with a leverage ratio of just 0.3x, significantly below the peer average of 1.1x.

As shown in the following overview of Chord’s Williston Basin position and commodity mix:

Operational Improvements Driving FCF Growth

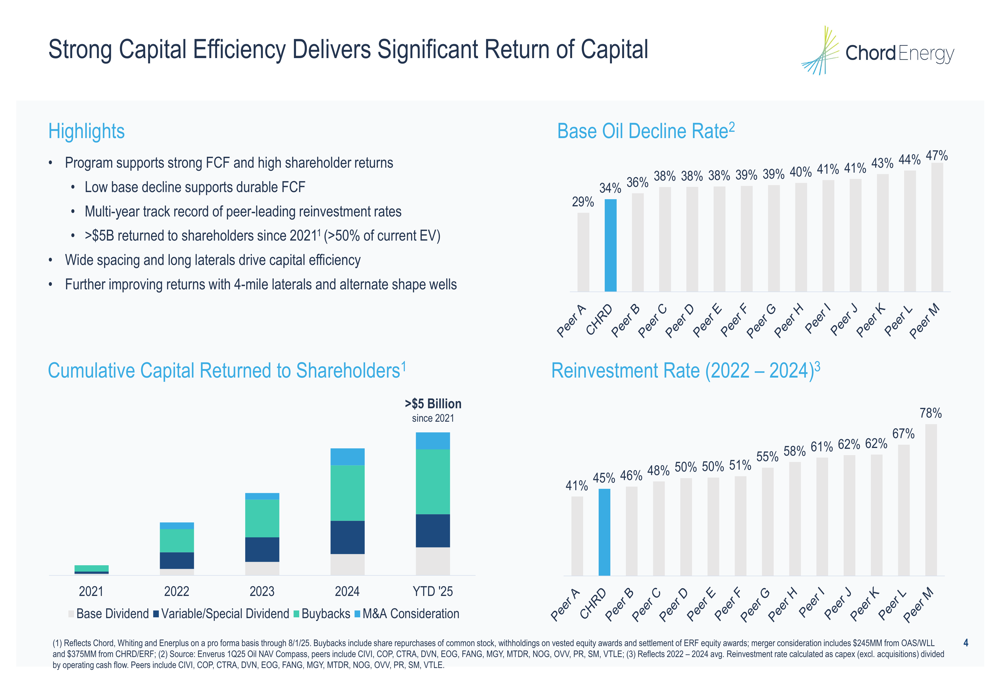

A key focus of Chord’s presentation was its operational efficiency, particularly its industry-leading low base decline rate of 29% compared to peers ranging from 34% to 47%. This low decline rate, coupled with a reinvestment rate of just 41% (versus peer average of 45-78%), has enabled the company to generate substantial free cash flow.

The following chart illustrates Chord’s advantageous position relative to peers:

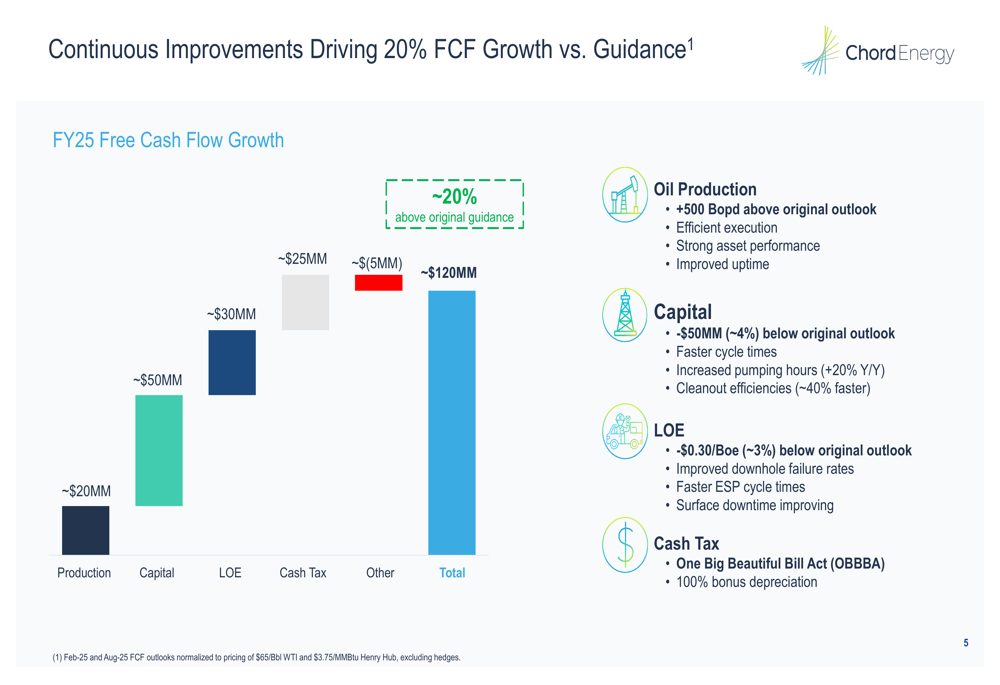

Chord identified several drivers behind its 20% free cash flow growth compared to original guidance, including increased oil production (+500 barrels per day), reduced capital expenditures ($50 million below original outlook), lower lease operating expenses ($0.30/Boe below original outlook), and favorable tax treatment under the One Big Beautiful Bill Act.

This waterfall chart demonstrates the cumulative impact of these improvements:

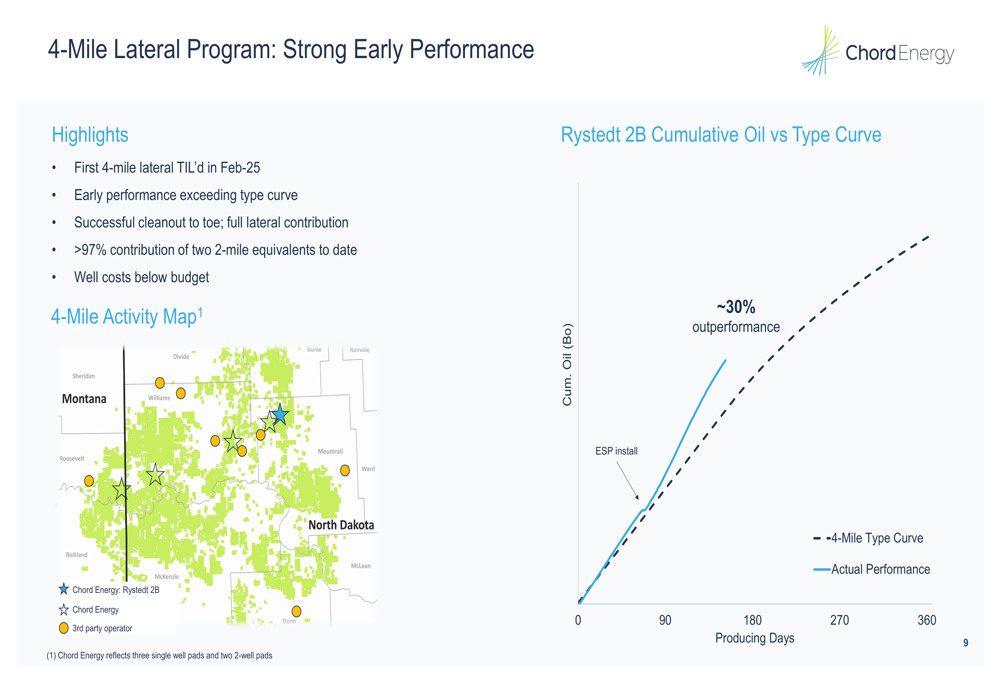

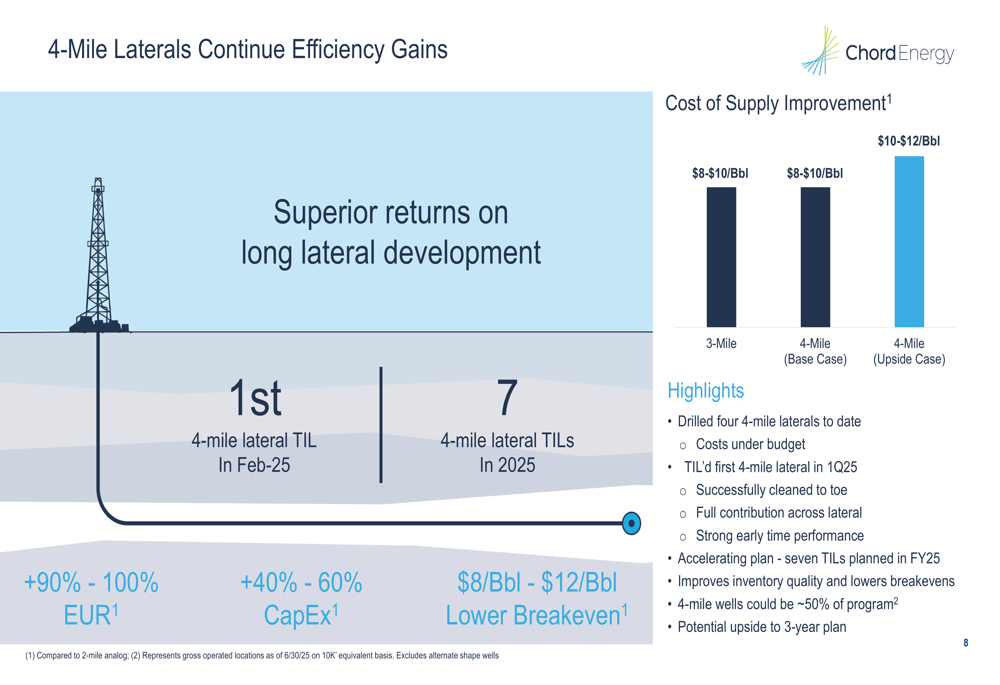

The company’s most significant operational innovation has been the implementation of 4-mile lateral wells, which are showing promising early results. Chord reported that its first 4-mile lateral well, which began producing in February 2025, is outperforming type curve expectations by approximately 30%. The company plans to continue expanding this program, with seven 4-mile lateral wells expected to be turned in line (TIL) in 2025.

The following chart shows the performance of Chord’s 4-mile lateral program:

These longer laterals provide substantial economic benefits, with 4-mile laterals delivering $8-12 per barrel lower breakeven costs compared to traditional well designs. The company expects that 4-mile wells could eventually comprise approximately 50% of its development program.

Capital Allocation and Shareholder Returns

Chord Energy has maintained a disciplined approach to capital allocation, with a strong focus on returning capital to shareholders. Since 2021, the company has returned over $5 billion to shareholders, representing more than 50% of its current enterprise value.

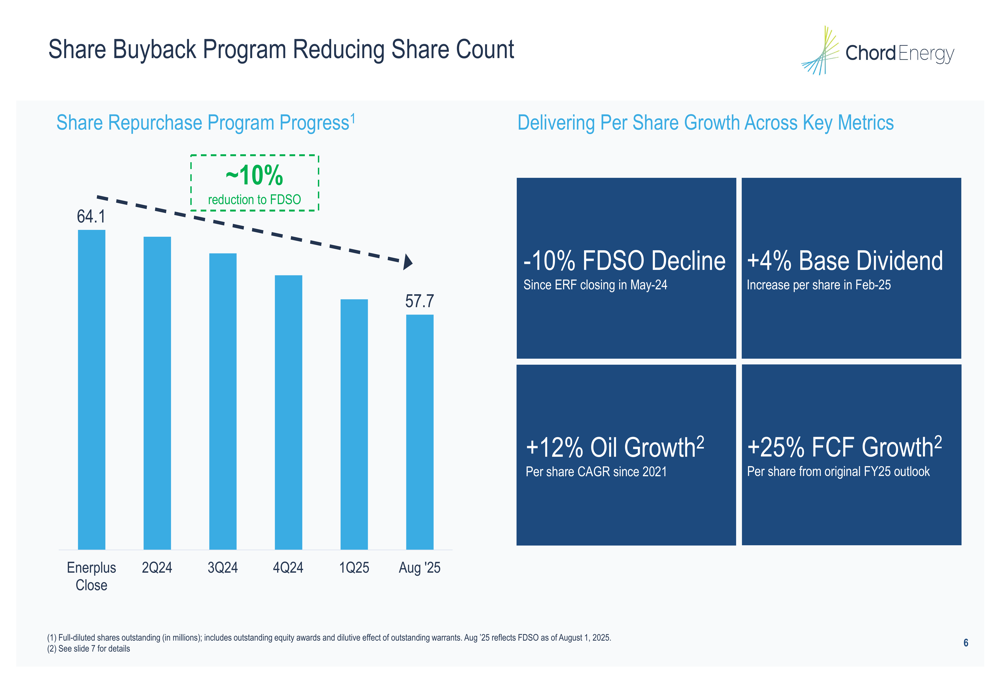

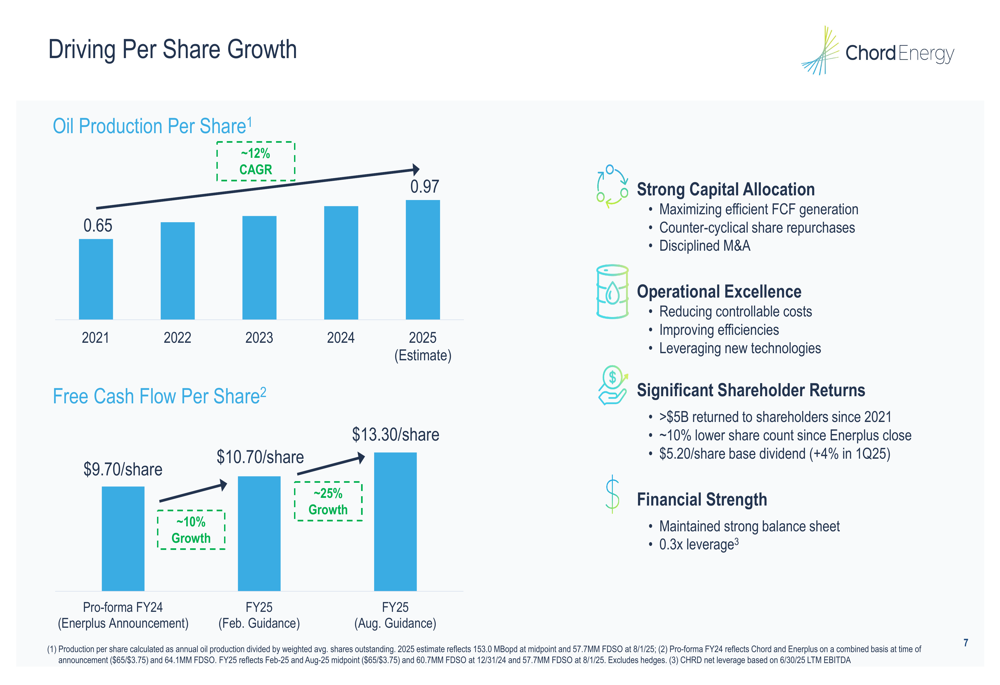

The company’s share repurchase program has reduced fully diluted shares outstanding by approximately 10% since the closing of its Enerplus (NYSE:ERF) acquisition in May 2024. This reduction, combined with operational improvements, has driven significant per-share growth metrics.

The following chart illustrates the impact of Chord’s share repurchase program:

This focus on per-share metrics has resulted in impressive growth, with oil production per share increasing at a compound annual growth rate of approximately 12% since 2021. Similarly, free cash flow per share has grown from $10.70 in the February 2025 guidance to $13.30 in the August update.

For Q2 2025, Chord reported adjusted free cash flow of $141 million, with $75 million allocated to base dividends and $55 million to share repurchases, consistent with its commitment to return at least 75% of free cash flow to shareholders.

Financial Position and 2025 Outlook

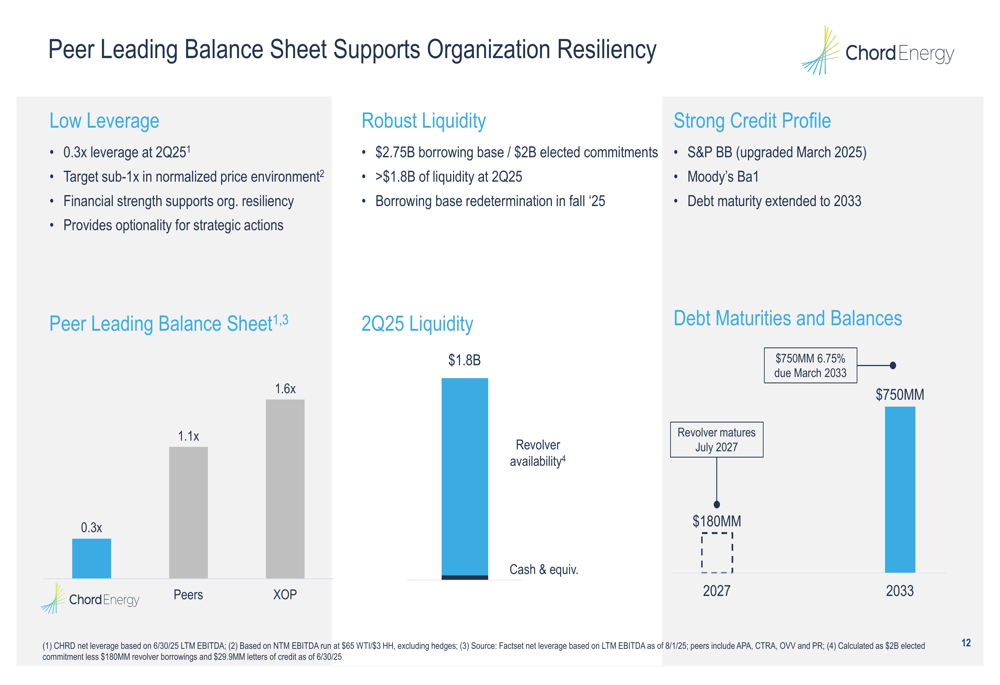

Chord Energy maintains a strong financial position with industry-leading low leverage of 0.3x compared to the peer average of 1.1x. This conservative balance sheet provides significant financial flexibility and resilience in a volatile commodity price environment.

The following chart illustrates Chord’s balance sheet strength relative to peers:

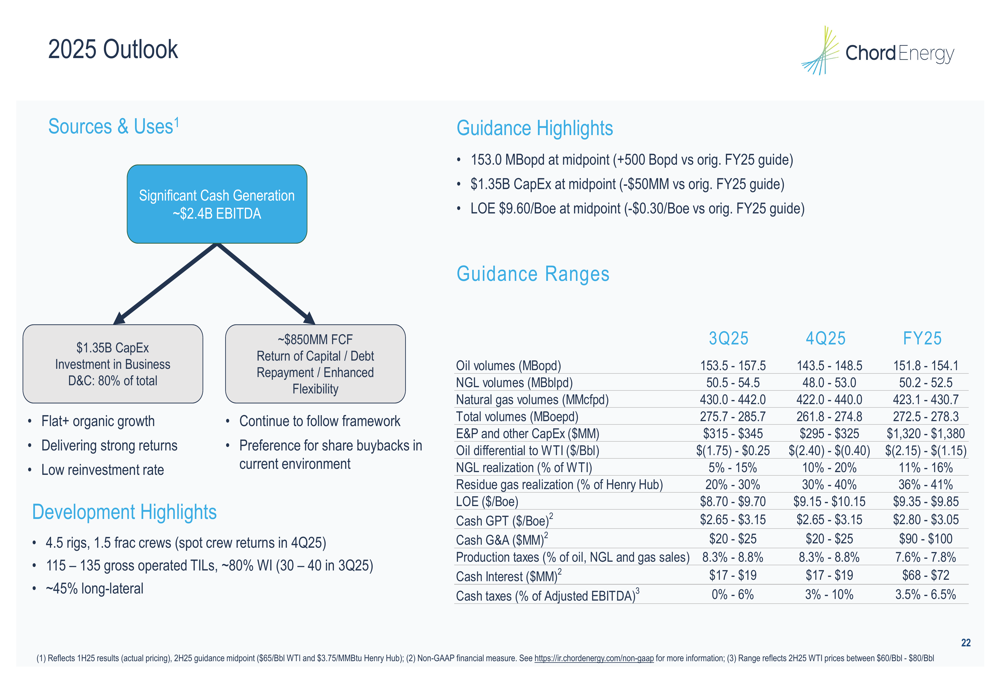

For 2025, Chord provided detailed guidance, projecting EBITDA of approximately $2.4 billion and free cash flow of around $850 million. The company plans to operate approximately 4.5 rigs and complete 115-135 gross operated wells, with approximately 45% being long laterals.

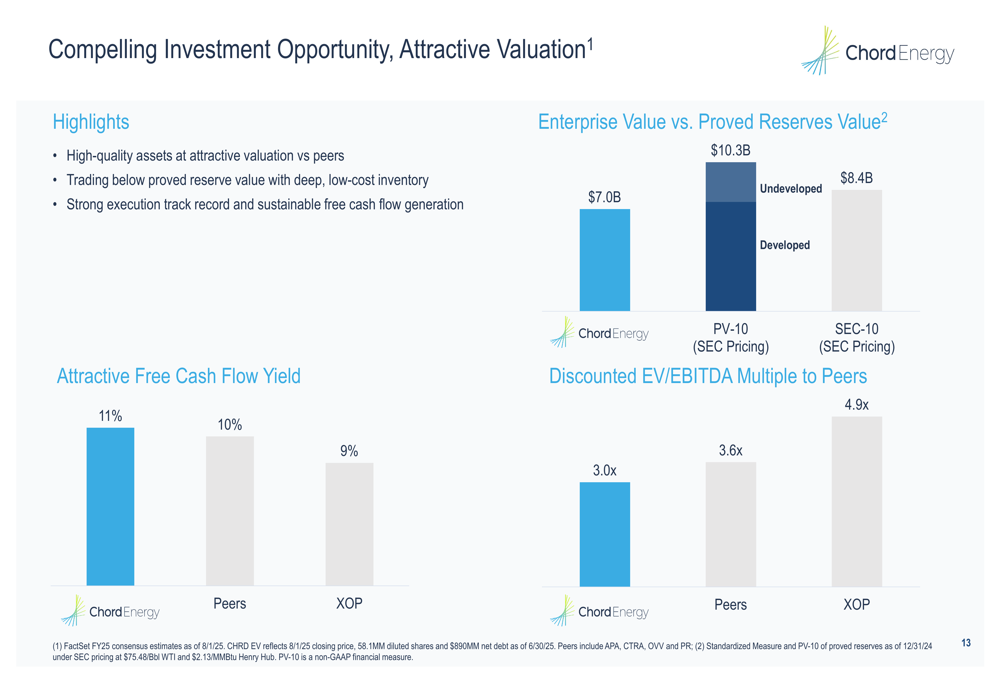

The company also highlighted its attractive valuation relative to peers, noting that it is trading below its proved reserve value and at a discounted EV/EBITDA multiple compared to peers.

Forward-Looking Statements

Looking ahead, Chord Energy aims to maintain its disciplined approach to capital allocation while continuing to enhance operational efficiency. The company’s 2025-2027 outlook focuses on holding oil volumes flat at 152-153 thousand barrels per day while transitioning more of its development to long-lateral wells.

This strategy aligns with comments made during the Q1 2025 earnings call, where CEO Danny Brown emphasized the company’s "substantial, yet low decline and high oil cut production base" and noted that Chord is "in a really nice place just naturally through our program that we’ve reduced activity in this environment."

While the presentation highlighted numerous strengths and opportunities, investors should note that Chord faces challenges from volatile oil prices, which contributed to the revenue miss in Q1 2025. The company’s conservative hedging strategy, covering approximately 40% of production in the prompt quarter, aims to mitigate some of this price risk.

Overall, Chord Energy’s presentation reinforced its position as a disciplined operator focused on capital efficiency, free cash flow generation, and shareholder returns, with significant operational improvements driving enhanced financial performance despite challenging market conditions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.