Bubble Wrap maker Sealed Air surges on report of buyout talks

Introduction & Market Context

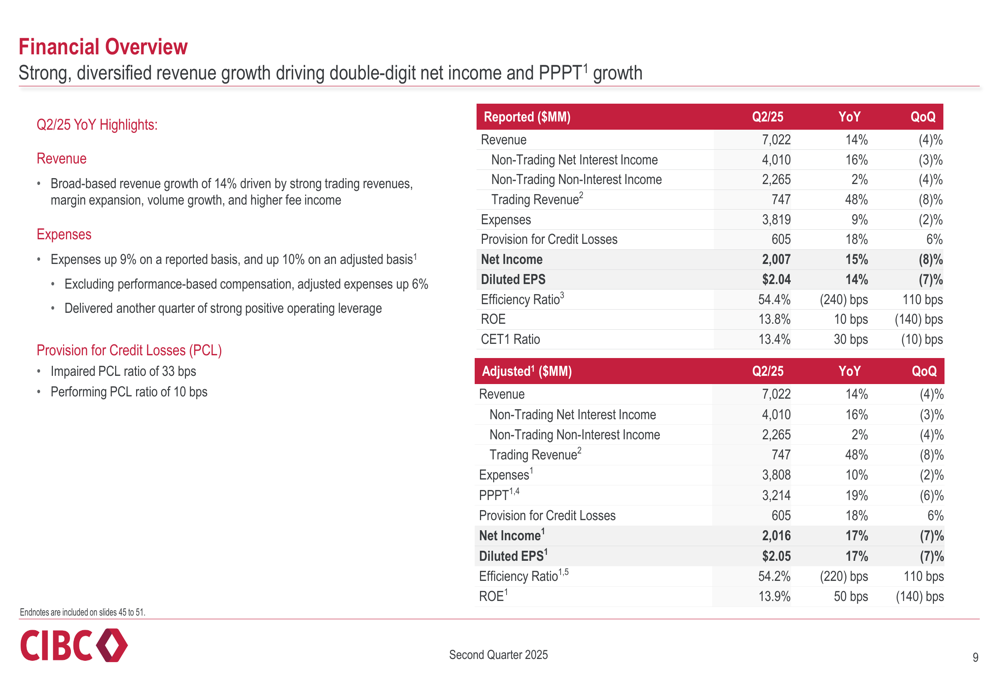

Canadian Imperial Bank of Commerce (TSX:CM) released its second quarter 2025 financial results on May 29, 2025, showcasing strong performance across all business segments. The bank reported adjusted earnings per share of $2.05, representing a 17% year-over-year increase, while revenue grew 14% to $7.0 billion.

CIBC ’s stock closed at $67.91 on May 28, 2025, down 0.73% ahead of the earnings release. The stock has been trading near its 52-week high of $68.85, reflecting investor confidence in the bank’s performance despite economic uncertainties.

Quarterly Performance Highlights

CIBC delivered impressive financial results in the second quarter of 2025, with broad-based revenue growth and strong profitability metrics. The bank’s adjusted return on equity reached 13.9%, up 50 basis points year-over-year, while maintaining a solid capital position with a CET1 ratio of 13.4%.

As shown in the following comprehensive financial performance overview, CIBC achieved double-digit growth across key metrics, including a 17% increase in adjusted net income to $2.0 billion:

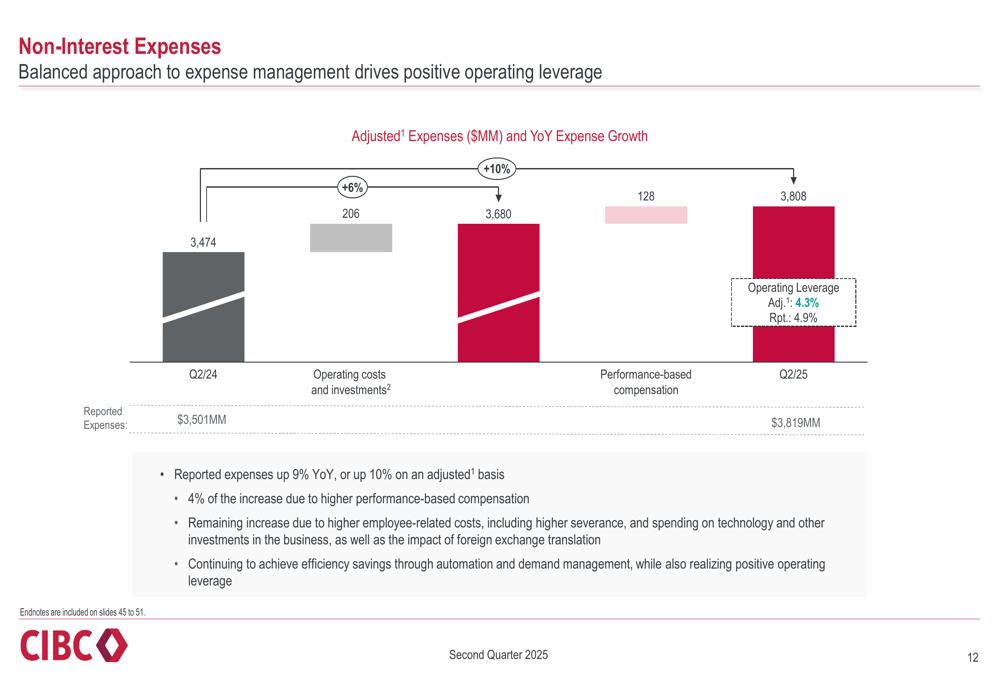

The bank demonstrated positive operating leverage, with revenue growth of 4.3% outpacing expense growth of 1.9%. This disciplined approach to expense management, combined with strong revenue generation, contributed to the significant improvement in profitability.

Detailed Financial Analysis

CIBC’s revenue growth was driven by multiple factors, including strong trading revenues, margin expansion, volume growth, and higher fee income. Net interest income (excluding trading) grew 16% year-over-year, benefiting from both volume growth and spread expansion.

The bank’s total net interest margin (excluding trading) expanded to 1.88% in Q2 2025, up from 1.72% in the same period last year, as illustrated in the following chart:

Non-interest income increased by 12% year-over-year, with trading non-interest income up 45%. Market-related fees excluding trading rose 8%, reflecting broad-based growth across fee categories.

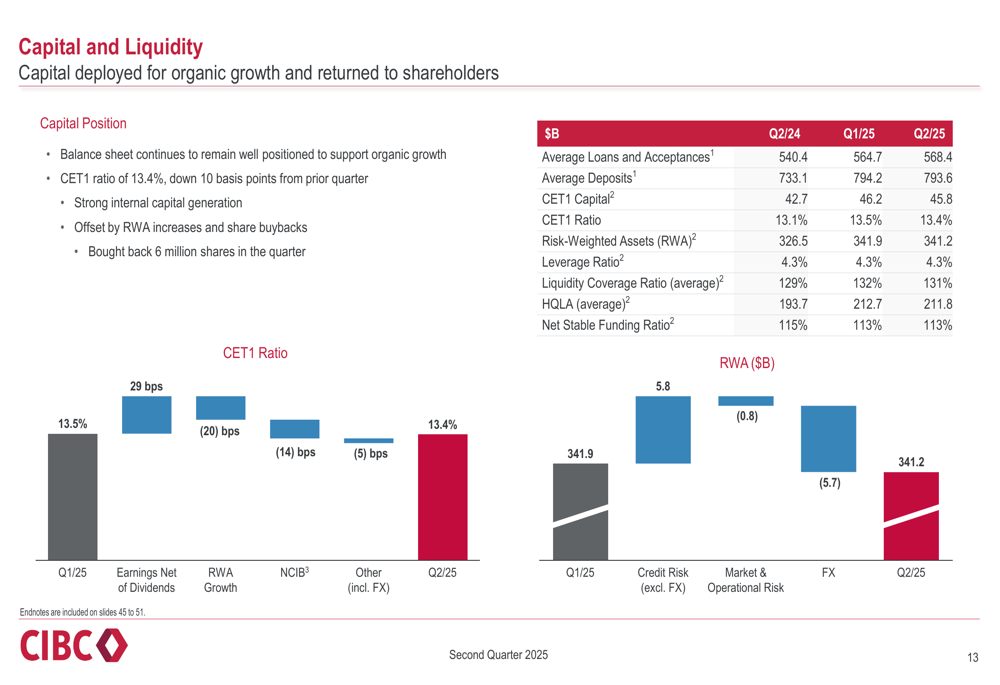

CIBC maintained a strong capital position, with a CET1 ratio of 13.4%, down 10 basis points from the previous quarter but up 30 basis points year-over-year. The bank continued to return capital to shareholders, buying back 6 million shares during the quarter.

Business Segment Performance

All of CIBC’s business segments delivered strong results in the second quarter of 2025.

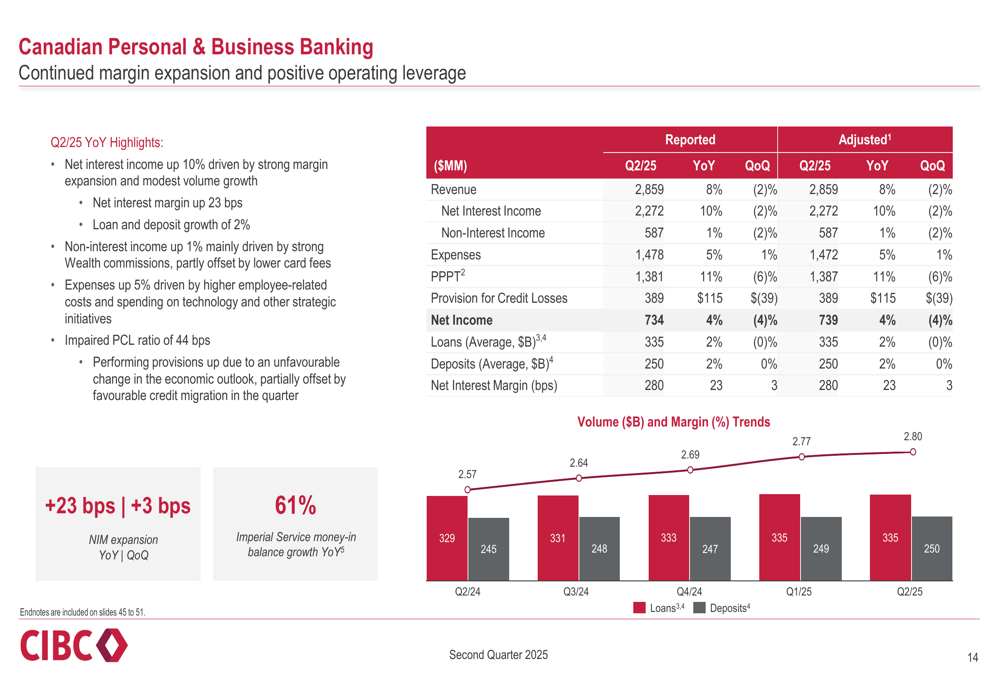

Canadian Personal and Business Banking reported a 10% increase in net interest income, driven by strong margin expansion of 23 basis points and modest volume growth of 2%. The segment benefited from broad-based revenue growth, particularly from higher yields.

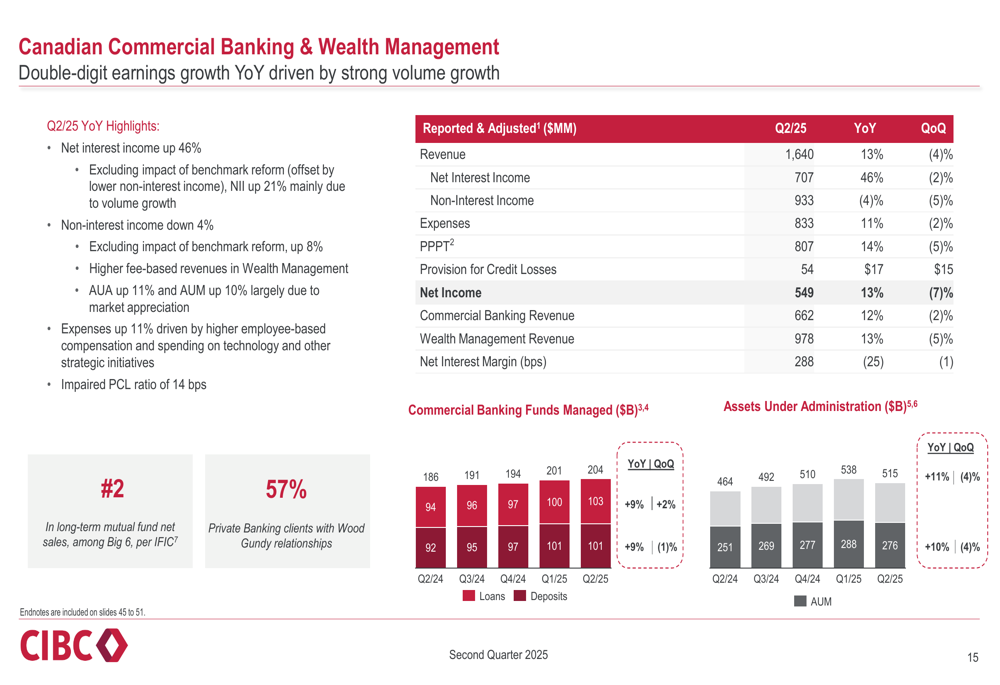

Canadian Commercial Banking and Wealth Management achieved double-digit earnings growth, with net interest income surging 46% year-over-year. This impressive performance was supported by strong volume growth in both commercial banking and wealth management.

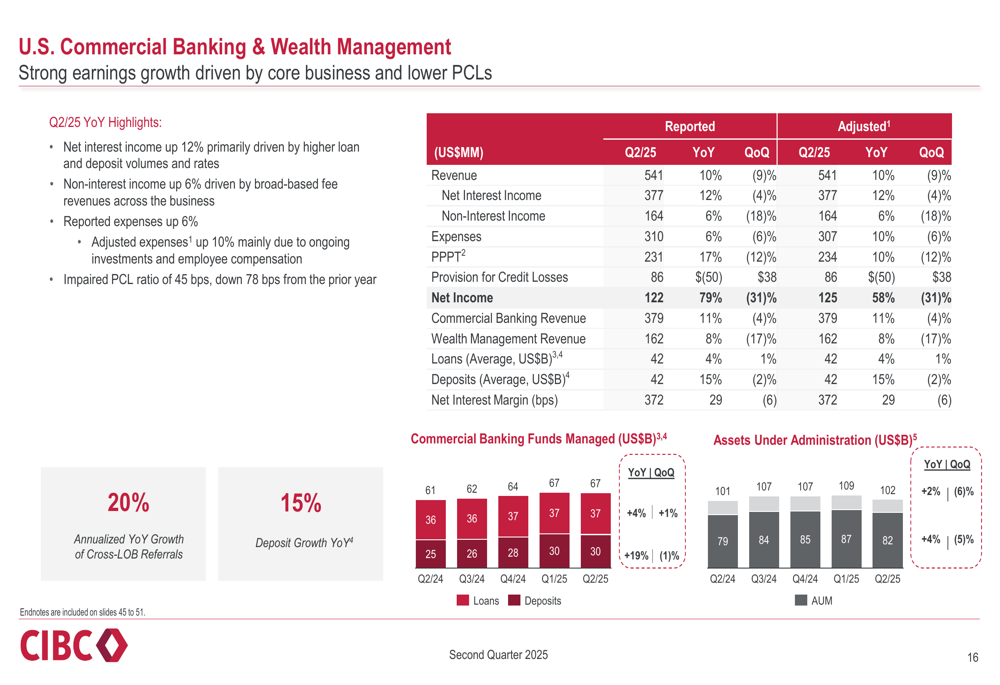

U.S. Commercial Banking and Wealth Management also delivered strong earnings growth, with net interest income up 12% primarily due to higher loan and deposit volumes and rates. This segment continues to be an important contributor to CIBC’s overall performance, accounting for 20% of total earnings.

Capital Markets was a standout performer, with adjusted revenue up 32% year-over-year. The segment benefited from strong trading activity, record corporate banking and investment banking revenues, and positive operating leverage.

Credit Quality and Risk Management

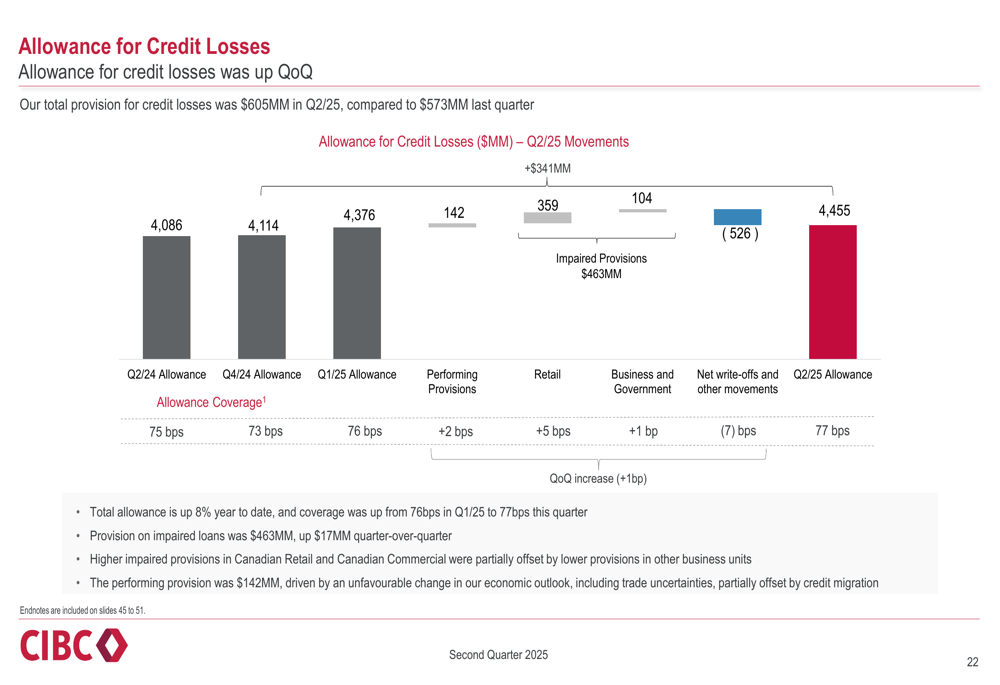

CIBC maintained strong credit quality in the second quarter of 2025, with total provision for credit losses (PCL) of $605 million, compared to $573 million in the previous quarter. The total PCL ratio was 44 basis points, with an impaired PCL ratio of 33 basis points.

The bank’s allowance for credit losses remained robust, as illustrated in the following chart:

PCL on impaired loans varied across business segments, with Canadian Personal and Business Banking showing stability, while U.S. Commercial Banking and Wealth Management saw some increases:

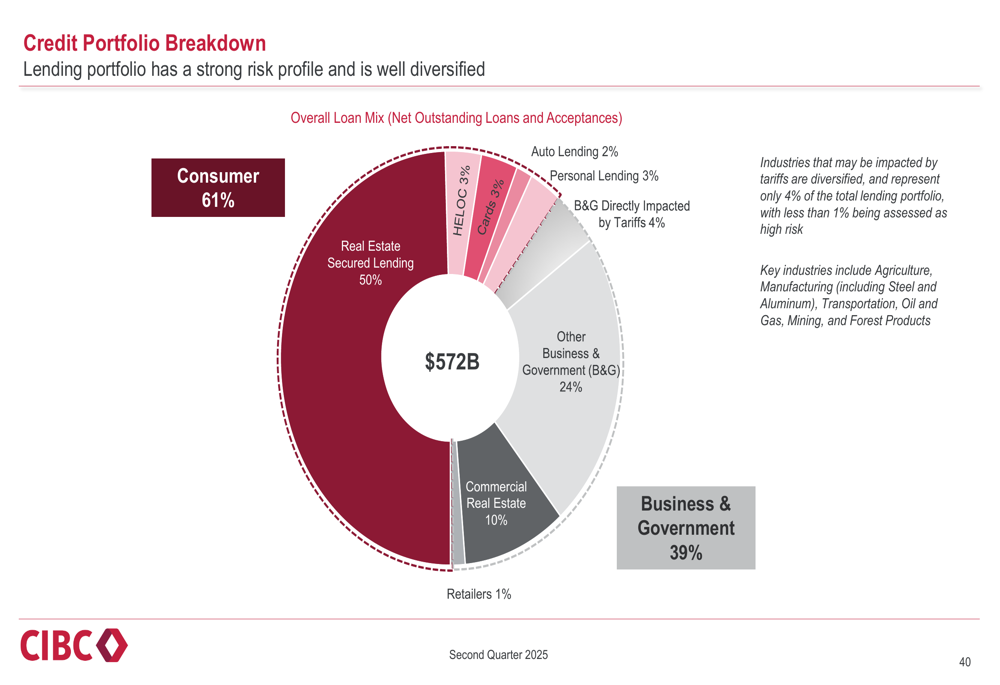

CIBC’s credit portfolio remains well-diversified across various sectors, with a balanced exposure to different industries and geographies:

The bank’s commercial real estate exposure is also well-diversified, with a focus on high-quality properties and strong borrowers:

Strategic Initiatives and Outlook

CIBC continues to make progress on its strategic priorities, focusing on client experience, operational efficiency, and digital transformation. The bank achieved its highest-ever Imperial Service Net Promoter Score of 74.7 and was recognized as the first major Canadian bank to be an AI Code of Conduct Signatory.

The bank’s digital initiatives have yielded significant operational efficiencies, with 200,000 hours saved since the launch of CIBC’s AI platform. Digital adoption rates continue to increase, with more clients engaging through digital channels.

Looking ahead, CIBC’s management expressed confidence in the bank’s ability to deliver consistent, profitable growth despite economic uncertainties. The bank is well-positioned to execute on its strategy and deliver relative outperformance through the economic cycle.

In closing, CIBC’s Q2 2025 results demonstrate continued momentum and consistency in a period of elevated uncertainty. The bank’s proactive management approach, strong capital position, and client-focused strategy provide a solid foundation for future growth and shareholder returns.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.