Tonix Pharmaceuticals stock halted ahead of FDA approval news

Introduction & Market Context

Cineplex Inc . (TSX:CGX) recently presented its second quarter 2025 investor presentation, highlighting the company’s ongoing recovery from pandemic disruptions and its diversification strategy. Despite showing progress in several key areas, the presentation comes against the backdrop of mixed Q2 results, where the company missed earnings expectations but exceeded revenue forecasts.

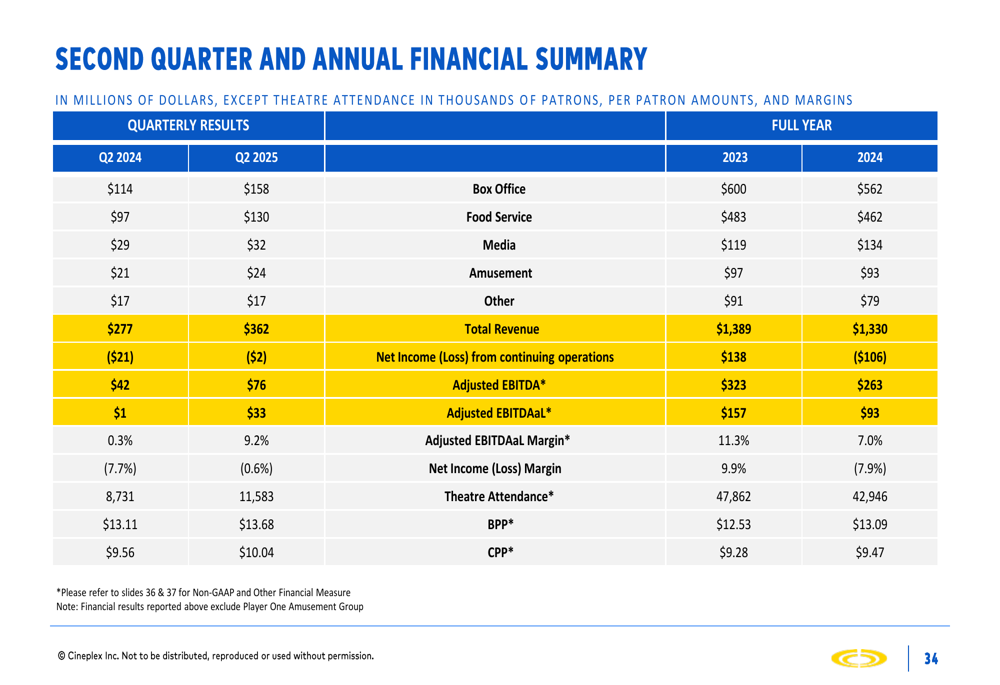

The Canadian entertainment giant reported Q2 revenue of $361.8 million, slightly above analyst expectations of $360.18 million, representing a 30.5% year-over-year increase. However, the company posted an earnings per share (EPS) of -$0.03, falling short of the forecasted $0.10. Despite this earnings miss, Cineplex shares showed resilience, trading up 3.87% to $10.73 as of the most recent market close.

Quarterly Performance Highlights

Cineplex’s Q2 2025 results showed significant improvement over the same period last year, with adjusted EBITDA surging to $33.4 million from just $900,000 in Q2 2024. Box office attendance grew by 32.7% year-over-year, driving much of the revenue increase. The company also strengthened its cash position, which stood at $42.1 million at quarter-end, an increase of $24.1 million from Q1 2025.

As shown in the following comprehensive financial summary, Cineplex has been tracking its performance across multiple metrics and business segments:

CEO Ellis Jacob expressed confidence in the company’s direction during the earnings call, stating, "The success we’ve seen in Q2 combined with our strategic initiatives to win with our guests gives us confidence in our ability to deliver results." However, the company also announced a restructuring program aimed at achieving $10 million in annual savings, suggesting management is focused on improving operational efficiency amid ongoing recovery efforts.

Business Segment Analysis

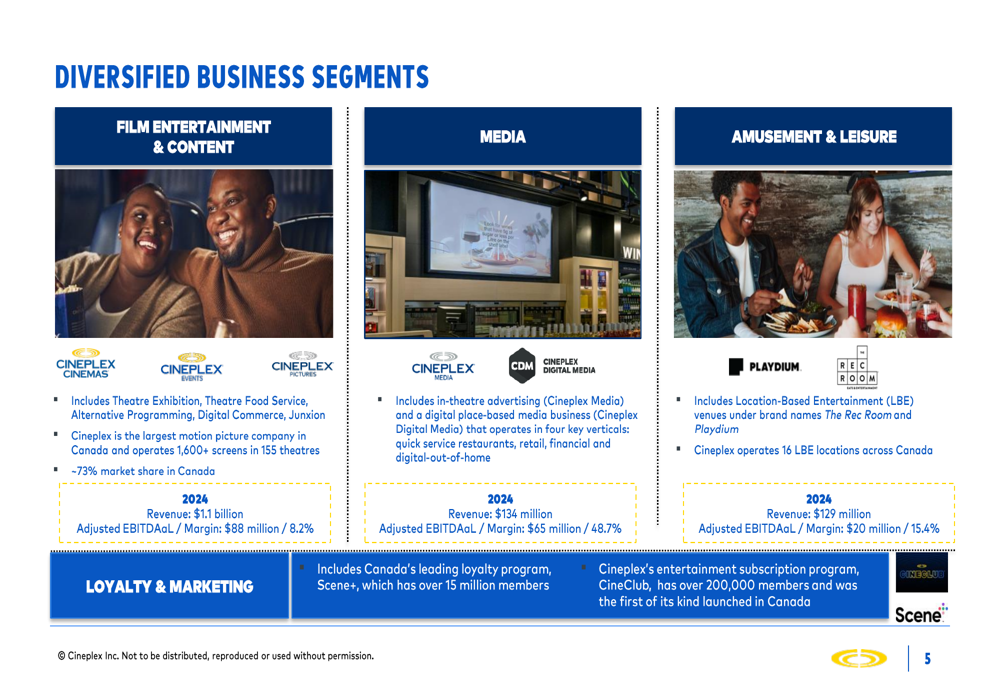

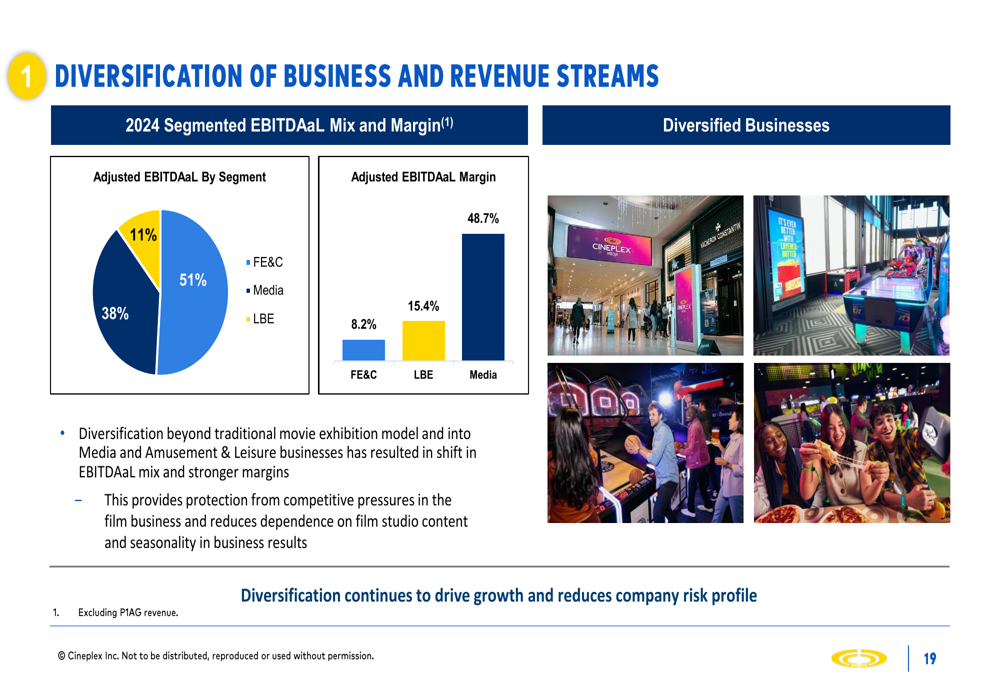

Cineplex operates as a diversified entertainment and media company with three main business segments: Film Entertainment and Content (51% of revenue), Media (38%), and Amusement and Leisure (11%). Each segment contributes differently to the company’s profitability, with Media delivering the highest margins.

The following breakdown illustrates the company’s diversified business model and the performance of each segment:

In the Film Entertainment segment, Cineplex maintains a dominant 73% market share in the Canadian box office. Box office revenue has been steadily recovering from pandemic lows, reaching $562 million in 2024 compared to $236 million in 2021, though still below the pre-pandemic level of $706 million in 2019. Similarly, box office revenue per patron has increased from $10.63 in 2019 to $13.09 in 2024, indicating successful premium pricing strategies.

The Media segment, which includes cinema advertising and digital place-based media, has shown strong recovery with revenues reaching $79 million in 2024, up from the pandemic low of $24 million in 2020, though still below the 2019 level of $115 million. This segment boasts the highest adjusted EBITDAaL margin at 48.7%.

Strategic Initiatives

Cineplex’s investor presentation emphasized several strategic initiatives aimed at driving long-term growth and profitability. A key focus is the expansion of premium offerings, with premium theatre formats accounting for 41.6% of box office revenues in 2024.

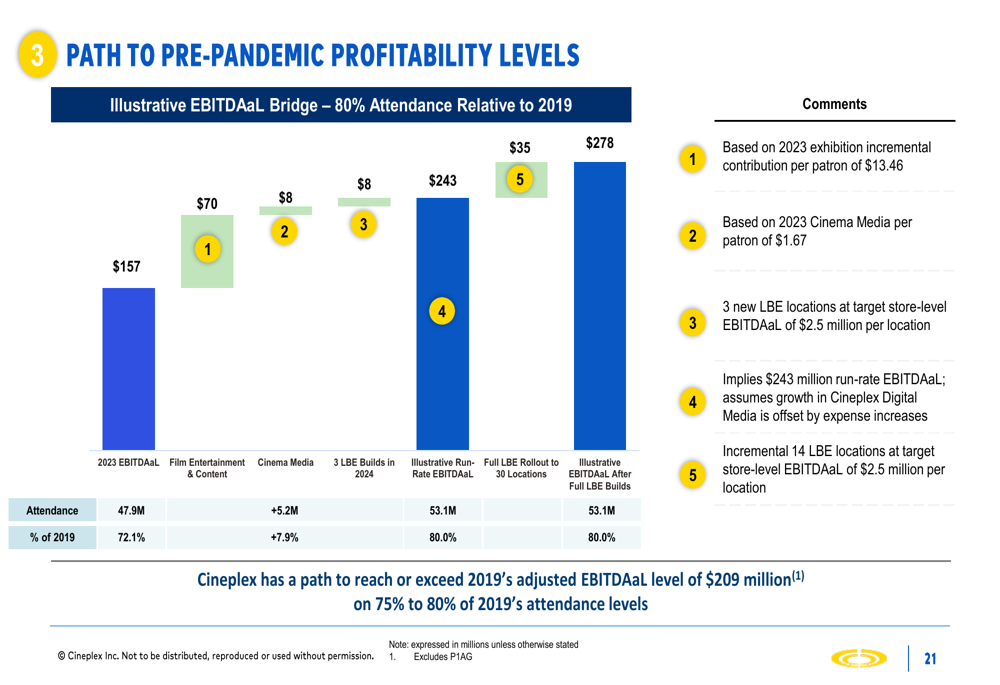

As illustrated in the company’s path to pre-pandemic profitability levels, Cineplex is targeting increased attendance and higher per-patron spending to drive EBITDA growth:

The Location-Based Entertainment (LBE) segment represents a significant growth opportunity for Cineplex. The company operates 16 LBE locations across Canada under brands like The Rec Room and Playdium. LBE revenues have grown from $79 million in 2019 to $129 million in 2024, with adjusted store-level EBITDAaL margins improving from 20.9% to 23.3% over the same period.

Cineplex sees potential to double LBE revenues from $132 million to $300 million and increase adjusted store-level EBITDAaL from $38 million to $75 million through additional locations and concepts. However, this optimistic outlook contrasts with near-term guidance provided during the earnings call, which anticipates a 3-5% decline in same-store LBE revenue for 2025.

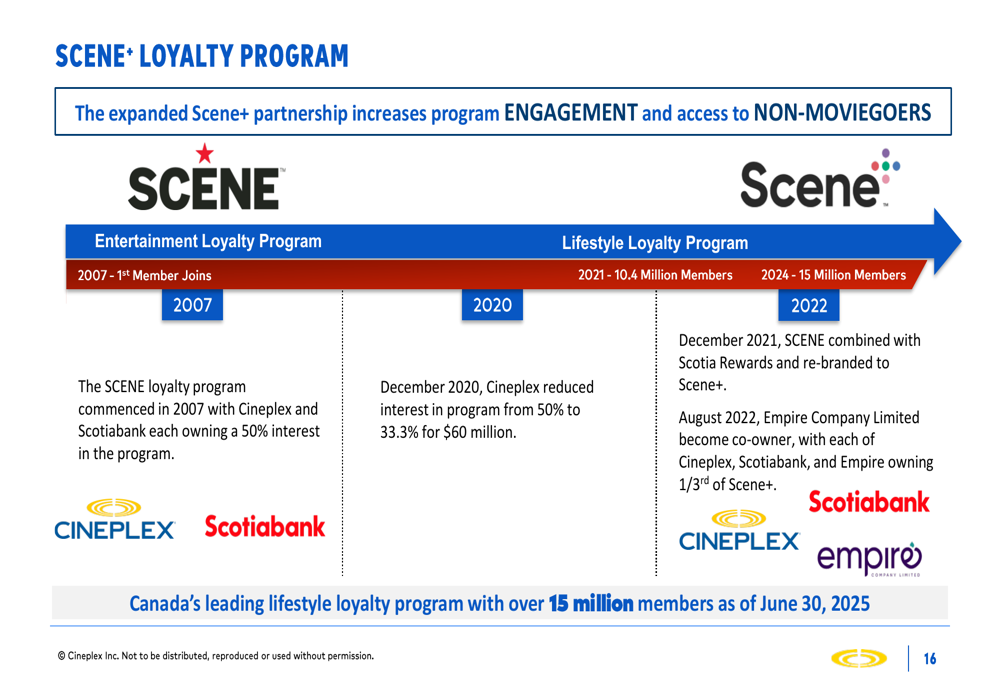

The company’s loyalty program, Scene+, represents another strategic asset with over 15 million members. In 2022, Empire Company Limited joined Cineplex and Scotiabank (TSX:BNS) as co-owners of the program, expanding its reach beyond moviegoers.

Forward-Looking Statements

Looking ahead, Cineplex’s presentation highlighted a strong slate of upcoming films for 2025 and 2026, which the company believes will drive attendance and revenue growth:

Despite the optimistic film slate, Cineplex faces several challenges. The company anticipates a decline of 3-5% in same-store revenue for its location-based entertainment segment in 2025. Capital expenditures are projected between $40 million and $50 million for the full year, reflecting disciplined spending.

The company is also preparing for a leadership transition, with CEO Ellis Jacob planning to retire in 2026 after a long tenure with the company. During the earnings call, analysts inquired about the search for a new CEO and the potential renewal of the normal course issuer bid (NCIB).

Competitive Industry Position

Cineplex positions itself as a defensive business that has historically been resilient during recessionary periods. The presentation emphasized the company’s diversification strategy as a key factor in reducing risk and driving growth.

The following chart illustrates the diversification of Cineplex’s business and revenue streams:

This diversification strategy appears to be yielding results, with the company’s adjusted EBITDA margin improving to 9.2% in Q2 2025, up from just 0.3% in the same period last year. However, with a P/E ratio of 100 according to InvestingPro data, the stock may be considered overvalued by some metrics.

Detailed Financial Analysis

Cineplex’s financial position has strengthened, with the company extending debt maturities and targeting a leverage ratio of 2.5x-3.0x. The presentation outlined a path to free cash flows in excess of pre-pandemic levels, with a projected free cash flow yield of 20.7%.

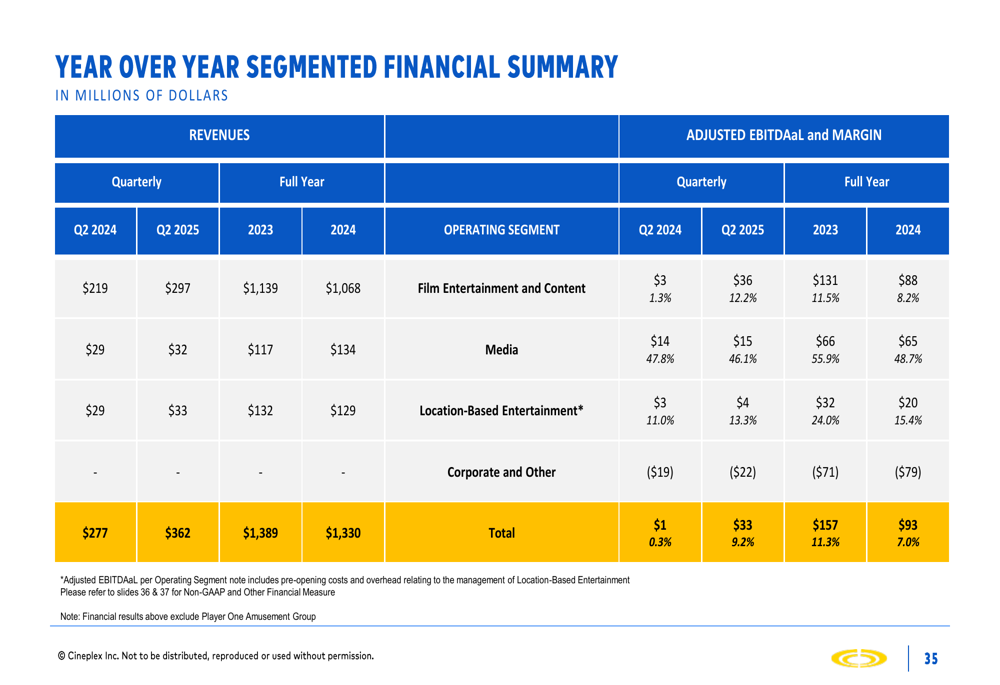

The year-over-year segmented financial summary provides a detailed look at the company’s performance across business segments:

While the company has made progress in its recovery, it’s worth noting that Cineplex’s stock has experienced a YTD return of -10.11% according to the earnings report, suggesting investors remain cautious about the pace and sustainability of the recovery.

In conclusion, Cineplex’s Q2 2025 investor presentation paints a picture of a company in recovery mode, with diversification strategies helping to mitigate risks and drive growth. However, the mixed Q2 results and near-term challenges in the LBE segment suggest the recovery path may not be entirely smooth. Investors will be watching closely to see if the company’s strategic initiatives translate into consistent financial performance in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.