Intel stock extends gains after report of possible U.S. government stake

Introduction & Market Context

Citigroup Inc (NYSE:C) released its second quarter 2025 earnings presentation on July 15, revealing strong financial performance across its core business segments. The banking giant’s shares were trading at $88 in premarket, up 0.57% following the announcement, building on the previous day’s close of $87.50.

The Q2 results demonstrate continued momentum from the company’s first quarter performance, with significant revenue growth and improved efficiency as Citigroup advances its strategic transformation initiatives.

Quarterly Performance Highlights

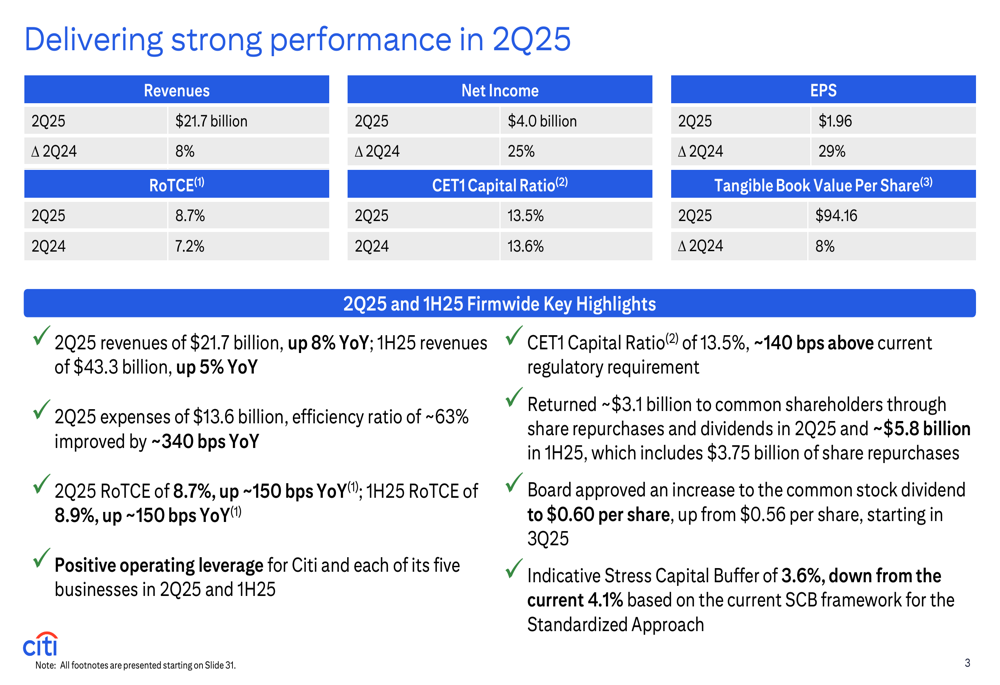

Citigroup reported Q2 2025 revenues of $21.7 billion, an 8% increase year-over-year, driven by strong performance across its five interconnected businesses. Net income rose 25% to $4.0 billion, while earnings per share grew 29% to $1.96.

As shown in the following financial highlights:

The bank’s Return on Tangible Common Equity (ROTCE) reached 8.7%, a 150 basis point improvement from the previous year. Citigroup maintained a robust capital position with a CET1 Capital Ratio of 13.5%, approximately 140 basis points above current regulatory requirements. The efficiency ratio improved by 340 basis points year-over-year, reflecting the company’s focus on expense management.

Citigroup returned $3.1 billion to shareholders during the quarter and approved a dividend increase to $0.60 per share starting in Q3. The bank’s Indicative Stress Capital Buffer decreased to 3.6% from 4.1%, providing additional flexibility for capital deployment.

Segment Performance Analysis

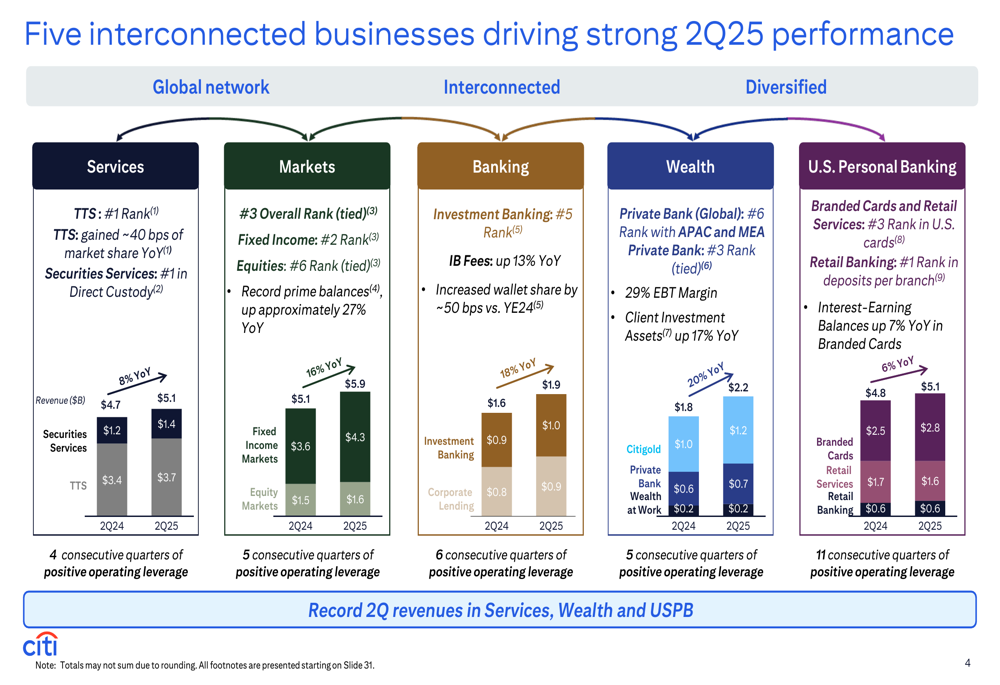

All five of Citigroup’s core business segments delivered positive operating leverage, with most reporting double-digit revenue growth. The presentation highlighted the interconnected nature of these businesses and their competitive positioning:

Services, which includes Treasury and Trade Solutions (TTS) and Securities Services, generated $5.1 billion in revenue, up 8% year-over-year. Both TTS and Securities Services maintained their #1 market rankings, marking four consecutive quarters of positive operating leverage.

Markets revenue also reached $5.1 billion, representing a 16% increase year-over-year. The division maintained its #3 overall ranking, with Fixed Income at #2 and Equities at #6, achieving five consecutive quarters of positive operating leverage.

Banking revenue grew 18% year-over-year to $1.6 billion, driven by a 13% increase in investment banking fees. The segment holds the #5 rank in Investment Banking and has delivered six consecutive quarters of positive operating leverage.

Wealth Management showed the strongest growth among all segments with a 20% year-over-year revenue increase to $2.2 billion. The Private Bank maintained its #6 ranking with an impressive 29% EBT margin and five consecutive quarters of positive operating leverage.

U.S. Personal Banking revenue rose 6% year-over-year to $5.1 billion. The segment holds the #3 rank in Branded Cards and Retail Services and the #1 position in Retail Banking, with eleven consecutive quarters of positive operating leverage.

Strategic Initiatives and Transformation

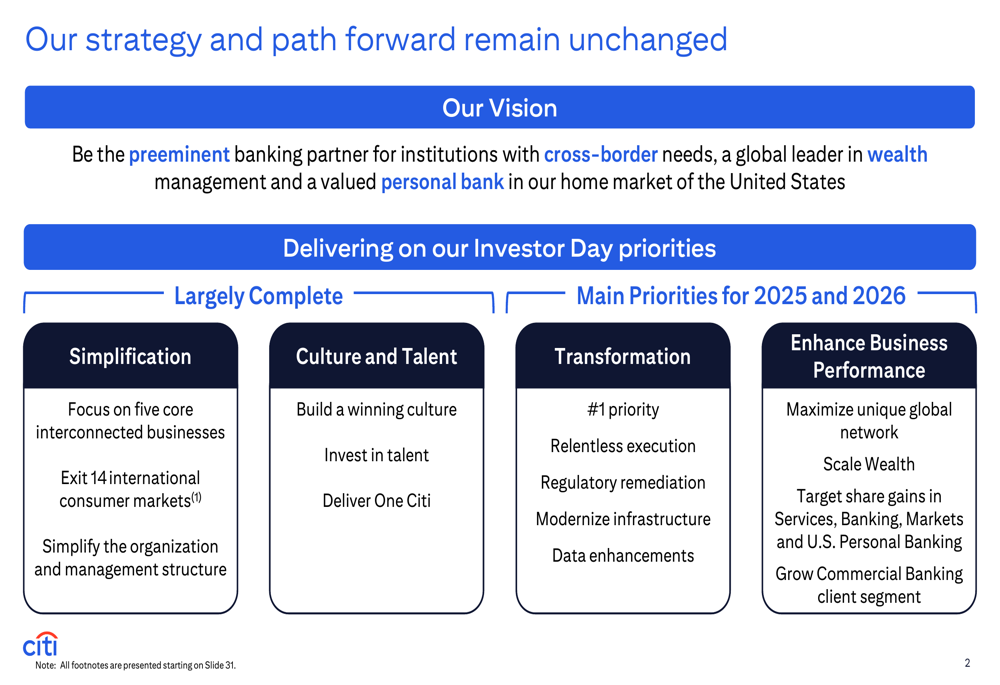

Citigroup’s presentation emphasized that its simplification strategy is largely complete, having focused the organization on five core businesses and exited 14 international consumer markets. The bank continues to make progress on its transformation initiatives, which remain a top priority:

Key achievements in Q2 included the expansion of Citi Token Services to four major markets, record trading volumes in Markets, continued market share gains in Banking, and the closure of the iCapital transaction for Wealth’s Alternative Investments. The bank also announced the sale of its Consumer business in Poland.

Technological advancement remains central to Citigroup’s transformation, with ongoing investments in end-to-end risk management, payment controls, and artificial intelligence. The presentation highlighted the expanded adoption of generative AI tools and the implementation of "Agentic AI" in production environments.

Forward Guidance and Capital Return

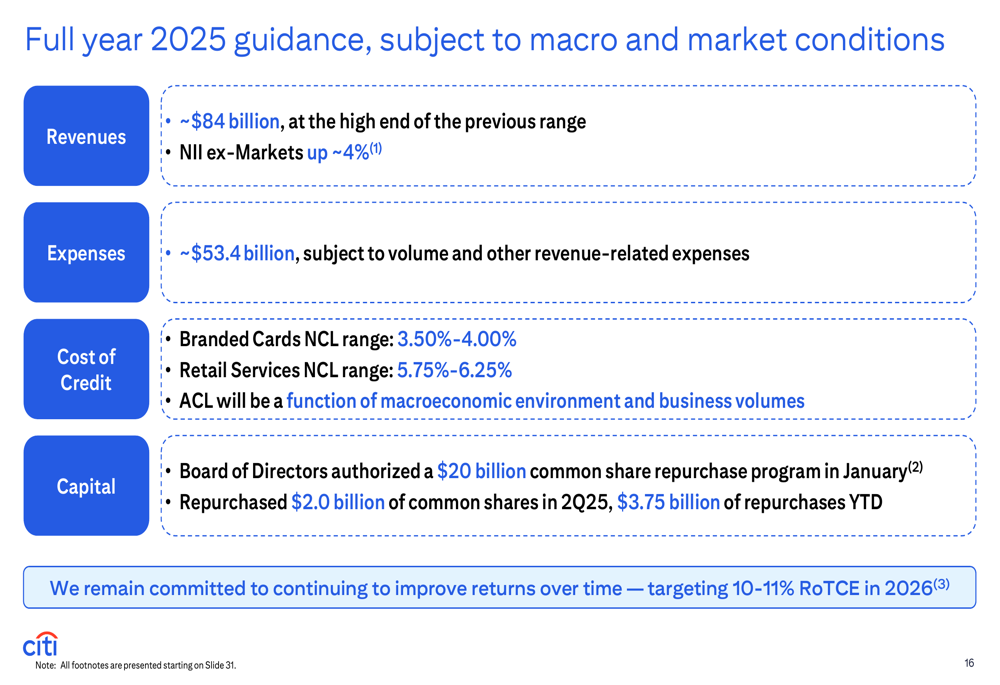

Citigroup raised its full-year 2025 revenue guidance to approximately $84 billion, at the high end of its previous range. Net Interest Income excluding Markets is expected to grow by approximately 4%, while expenses are projected to be around $53.4 billion.

The forward-looking guidance includes:

In a significant move for shareholders, the board authorized a $20 billion share repurchase program, underscoring confidence in the bank’s financial position and future prospects. Management reaffirmed its commitment to achieving a 10-11% Return on Tangible Common Equity by 2026.

Credit quality guidance indicates expected Branded Cards Net Credit Loss (NCL) rates of 3.50%-4.00% and Retail Services NCL rates of 5.75%-6.25% for the full year.

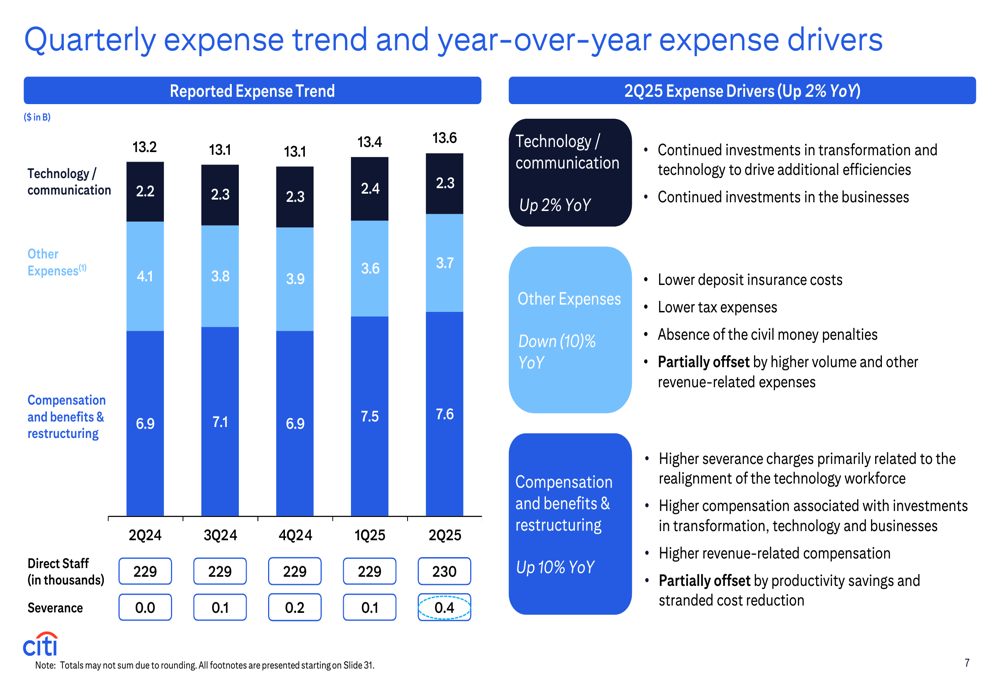

Expense Management

Citigroup’s expense management remains a key focus area, with the presentation detailing quarterly trends and year-over-year drivers:

While total expenses increased by 2% year-over-year to $13.6 billion, the bank improved its efficiency ratio by 340 basis points. The increase was primarily driven by higher compensation and benefits, partially offset by productivity savings and lower risk and controls costs. Technology investments continue to be prioritized as part of the bank’s transformation strategy.

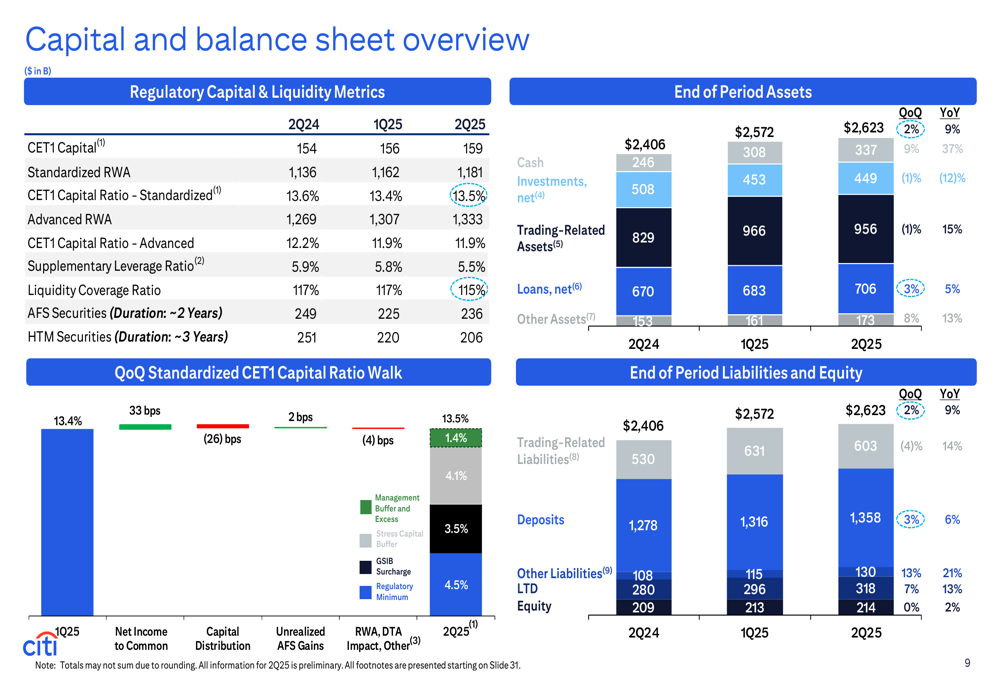

Capital Position and Balance Sheet

The presentation highlighted Citigroup’s strong capital and liquidity position, with detailed metrics on regulatory capital ratios and balance sheet composition:

The CET1 Capital Ratio improved by 33 basis points quarter-over-quarter, reflecting strong earnings generation and effective capital management. Total (EPA:TTEF) assets increased by 2% quarter-over-quarter, with balanced growth across cash investments and trading-related assets.

Citigroup’s disciplined approach to capital management, combined with its improved efficiency and strong revenue growth, positions the bank well for continued progress toward its medium-term financial targets while navigating evolving macroeconomic conditions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.