Powell’s speech, Nvidia’s chips, Meta deal - what’s moving markets

Introduction & Market Context

Citizens Financial Group (NYSE:CFG) released its second quarter 2025 earnings presentation on July 17, revealing strong financial performance across key metrics despite a challenging economic environment. The bank reported diluted earnings per share of $0.92, representing a 19% increase quarter-over-quarter and 18% year-over-year, continuing its momentum from Q1 when it beat analyst expectations.

However, the market’s initial reaction was negative, with CFG shares down 2.9% in premarket trading to $45.61, suggesting investors may be focusing on broader economic concerns rather than the company’s solid results.

Quarterly Performance Highlights

Citizens reported total revenue of $2.037 billion for Q2 2025, up 5% from the previous quarter and 4% year-over-year, driven by growth in both net interest income and noninterest income.

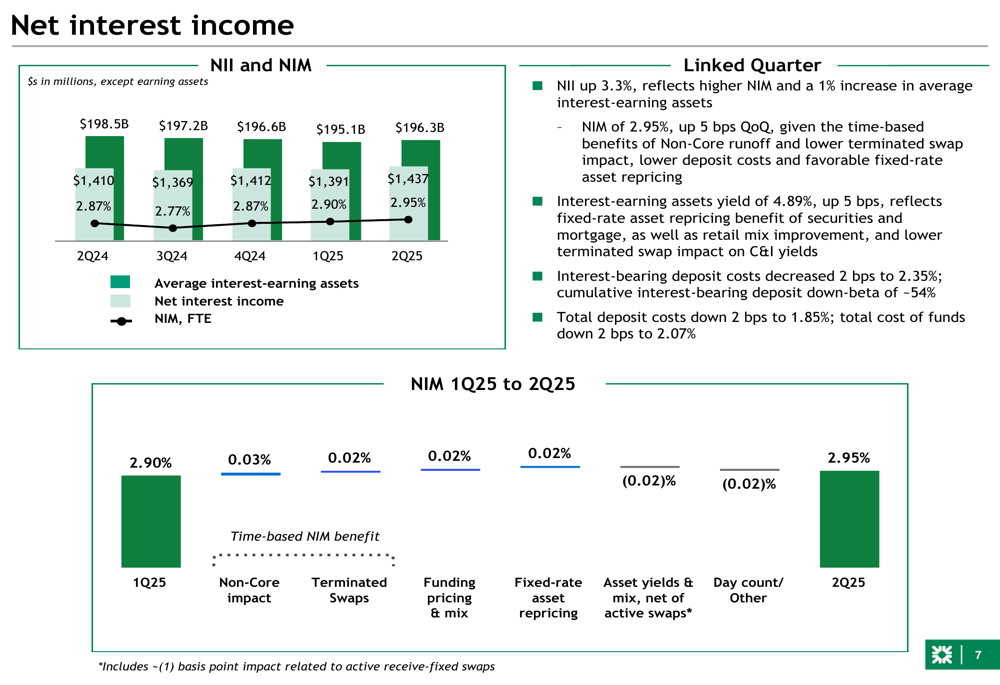

Net interest income reached $1.437 billion, increasing 3% quarter-over-quarter and 2% year-over-year, while the net interest margin expanded to 2.94%, up 5 basis points from Q1 and 8 basis points year-over-year.

As shown in the following chart of net interest income and margin trends:

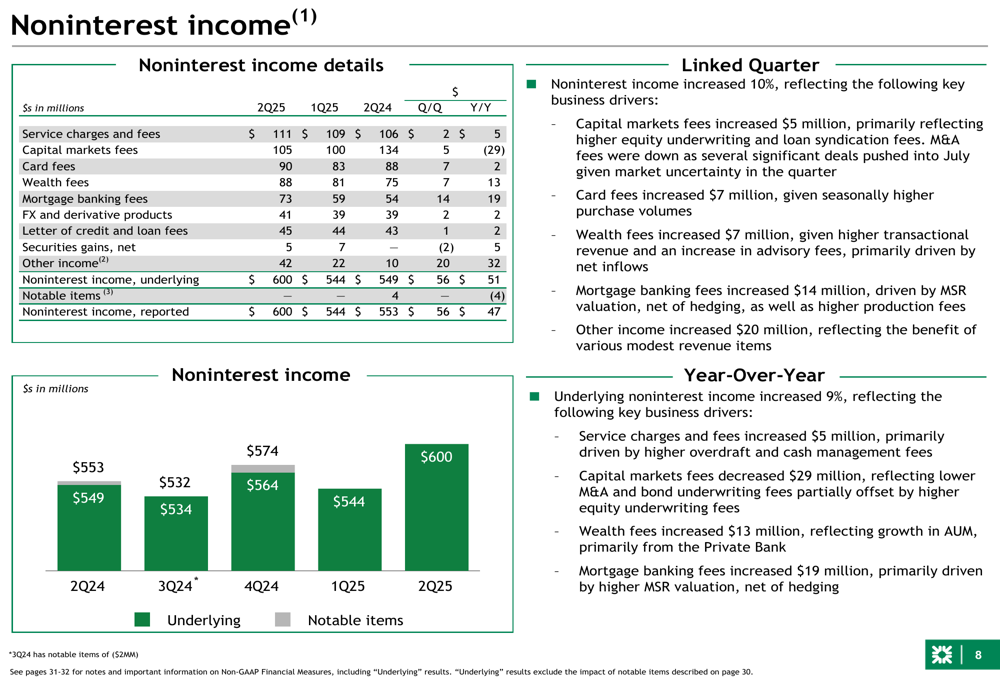

Noninterest income showed particularly strong growth at $600 million, up 10% quarter-over-quarter and 8% year-over-year. This growth was primarily driven by higher capital markets fees, increased card fees from seasonally higher purchase volumes, growth in wealth management fees, and improved mortgage banking revenue.

The following chart illustrates the noninterest income components and trends:

Net income rose to $436 million, representing a 17% increase from the previous quarter and 11% from the same period last year. The company’s return on tangible common equity (ROTCE) improved significantly to 11.0%, up 141 basis points quarter-over-quarter and 44 basis points year-over-year.

Strategic Initiatives

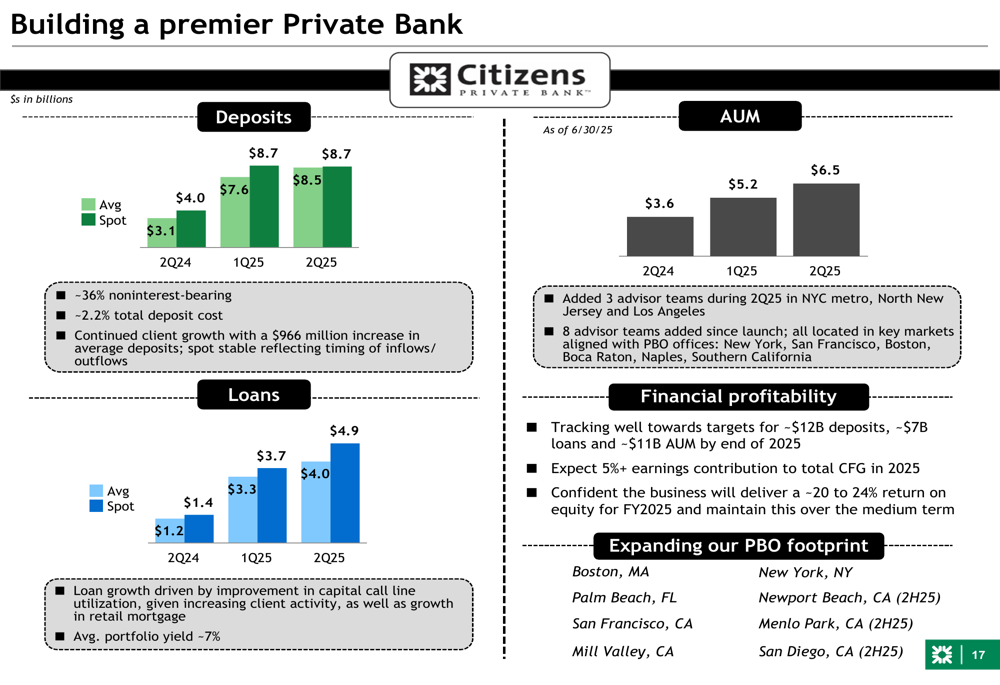

Citizens continues to make progress on its strategic initiatives, with particular emphasis on its Private Bank build-out. The company reported that the Private Bank is on track to deliver approximately 20-24% return on equity for fiscal year 2025.

The Private Bank has shown consistent growth across key metrics, with assets under management reaching $6.5 billion, deposits growing to $8.7 billion, and loans increasing to $4.9 billion in Q2 2025. The business is expected to contribute approximately 5% to Citizens’ total earnings in 2025.

The following chart shows the Private Bank’s growth trajectory:

The company is also advancing its TOP 10 efficiency program, which is progressing toward a target of approximately $100 million in pre-tax run-rate benefits by year-end 2025. Additionally, Citizens has commenced work on a "Reimagining the Bank" initiative, described as a multi-year transformational program.

Credit Quality & Capital Management

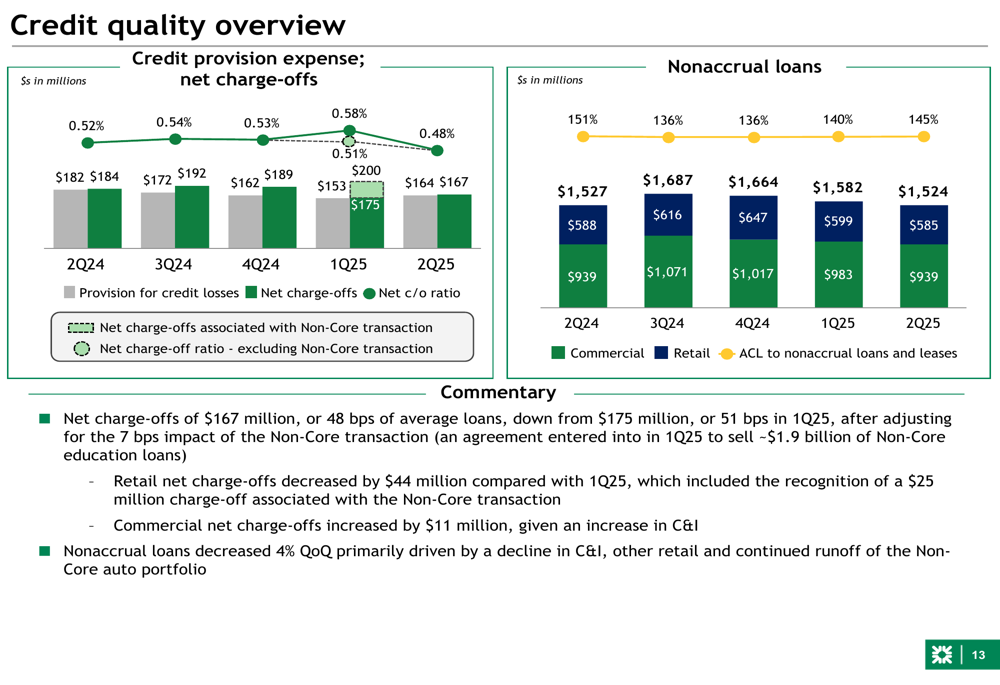

Citizens’ credit quality metrics showed improvement in Q2 2025, with net charge-offs of $167 million, or 48 basis points of average loans, down from 51 basis points in Q1. Nonaccrual loans decreased 4% quarter-over-quarter, primarily driven by a decline in commercial and industrial loans.

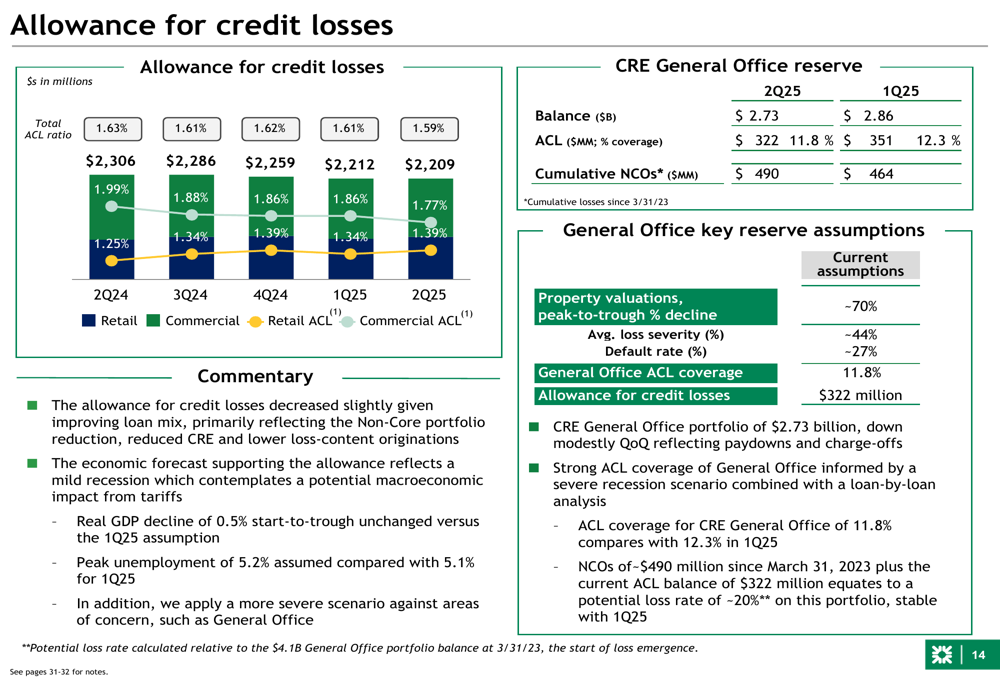

The following chart provides an overview of credit quality trends:

The company’s allowance for credit losses decreased slightly, driven by improvements in loan mix. The coverage for Commercial Real Estate (CRE) General Office loans remains strong at 11.8%, compared to 12.3% in Q1 2025.

Citizens maintained a robust capital position with a Common Equity Tier 1 (CET1) ratio of 10.6%. During the quarter, the company returned significant capital to shareholders, paying $185 million in common dividends and repurchasing $200 million of common stock. Notably, the Board of Directors increased the capacity of the company’s common share repurchase program to $1.5 billion on June 12, 2025.

Forward Guidance

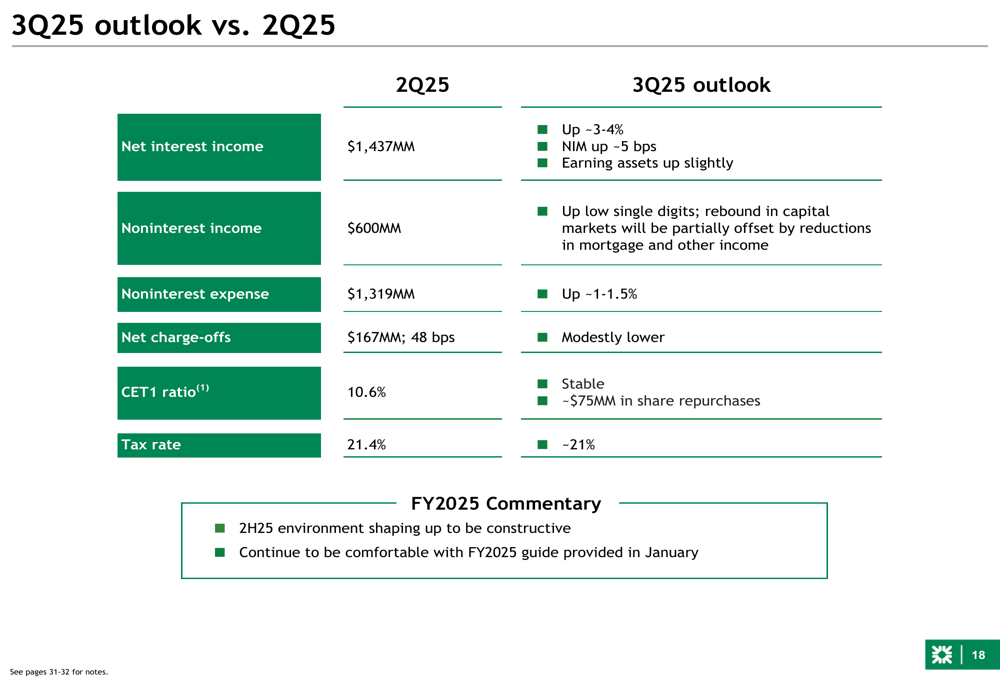

Looking ahead to Q3 2025, Citizens provided a positive outlook compared to Q2 results. The company expects net interest income to increase approximately 3-4%, with the net interest margin expanding by about 5 basis points and earning assets growing slightly.

Noninterest income is projected to increase by low single digits, while noninterest expense is expected to rise by approximately 1-1.5%. Net charge-offs are anticipated to be modestly lower, and the CET1 ratio is expected to remain stable with approximately $75 million in share repurchases planned.

The following table outlines the company’s Q3 2025 outlook:

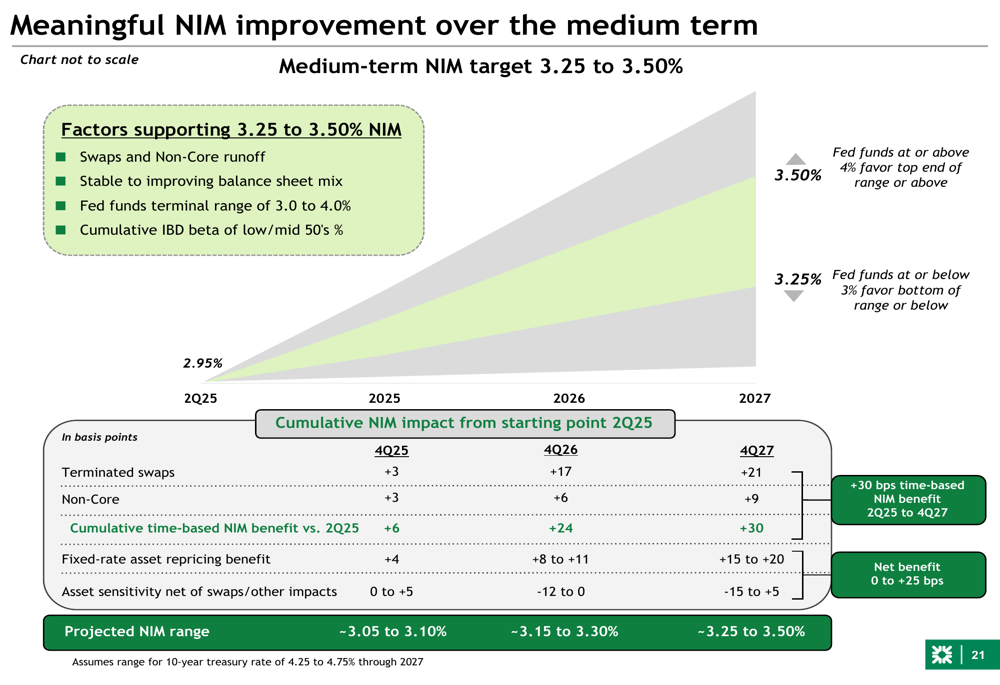

For the longer term, Citizens is targeting a net interest margin of 3.25-3.50%, supported by the runoff of non-core assets, terminated swaps, and fixed-rate asset repricing. The company expects to deliver a return on tangible common equity of approximately 16-18% over the medium term.

"We delivered solid Q2 2025 results with strong revenue and positive operating leverage," noted the company in its presentation overview. "Our net interest margin continues to expand, tracking well to 3.05-3.10% in Q4 2025 and 3.15-3.30% in Q4 2026."

Citizens emphasized that it is well-positioned for the medium term, with its Private Bank build-out tracking well and strong execution of strategic initiatives continuing across Private Banking, NYC Metro expansion, Private Capital, Payments, and Business Services Optimization.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.