Oklo stock tumbles as Financial Times scrutinizes valuation

Citizens Financial Group (NYSE:CFG) reported strong third-quarter 2025 results on October 15, with significant year-over-year growth across key financial metrics and continued expansion of its net interest margin. The bank’s shares rose 1.83% in premarket trading to $52.75, reflecting positive investor sentiment toward the results.

Quarterly Performance Highlights

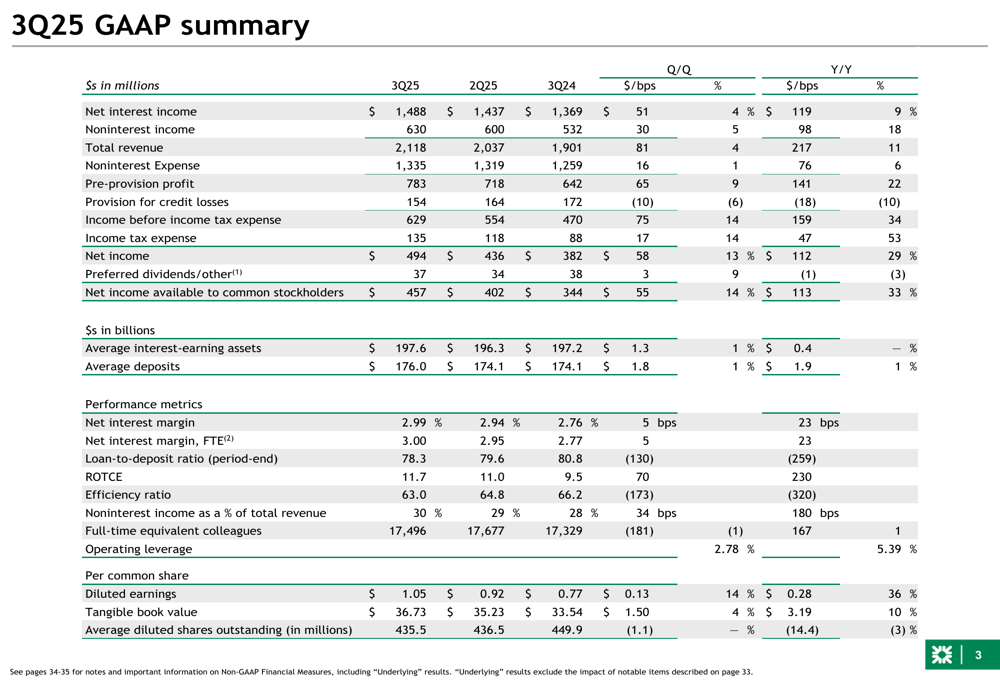

Citizens reported diluted earnings per share of $1.05 for Q3 2025, representing a 36% increase year-over-year and a 14% improvement from the $0.92 reported in the previous quarter. The strong performance was driven by revenue growth and improved operating leverage.

Total revenue reached $2.12 billion, up 11% compared to the same period last year, with net interest income of $1.49 billion (up 9% year-over-year) and noninterest income of $630 million (up 18% year-over-year). The bank’s net interest margin expanded to 2.99%, a 23 basis point improvement year-over-year and 5 basis points higher than the previous quarter.

As shown in the following comprehensive financial summary:

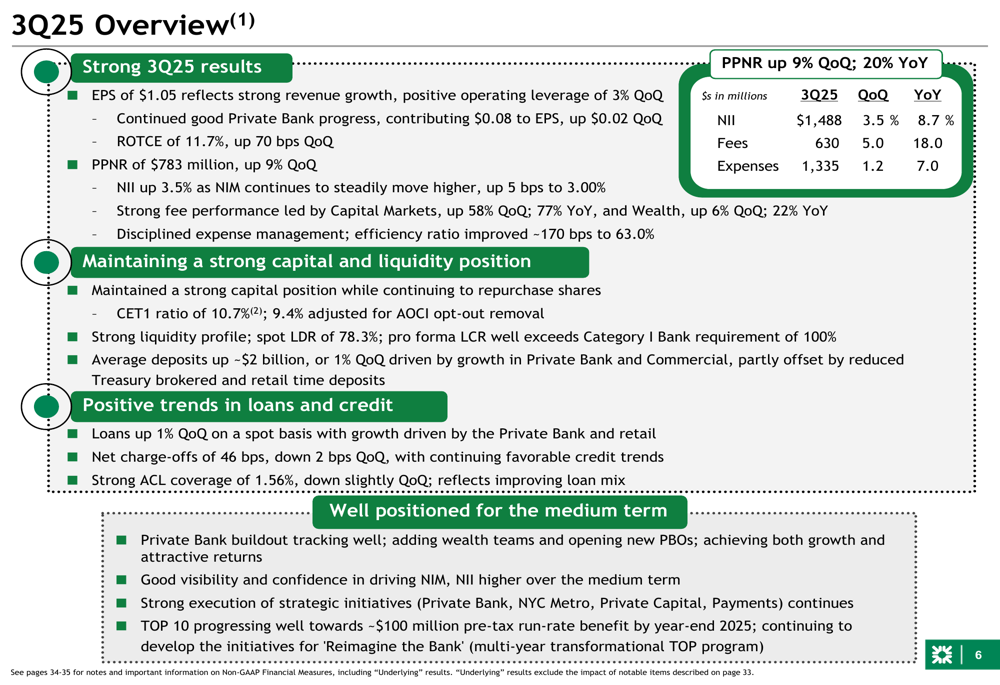

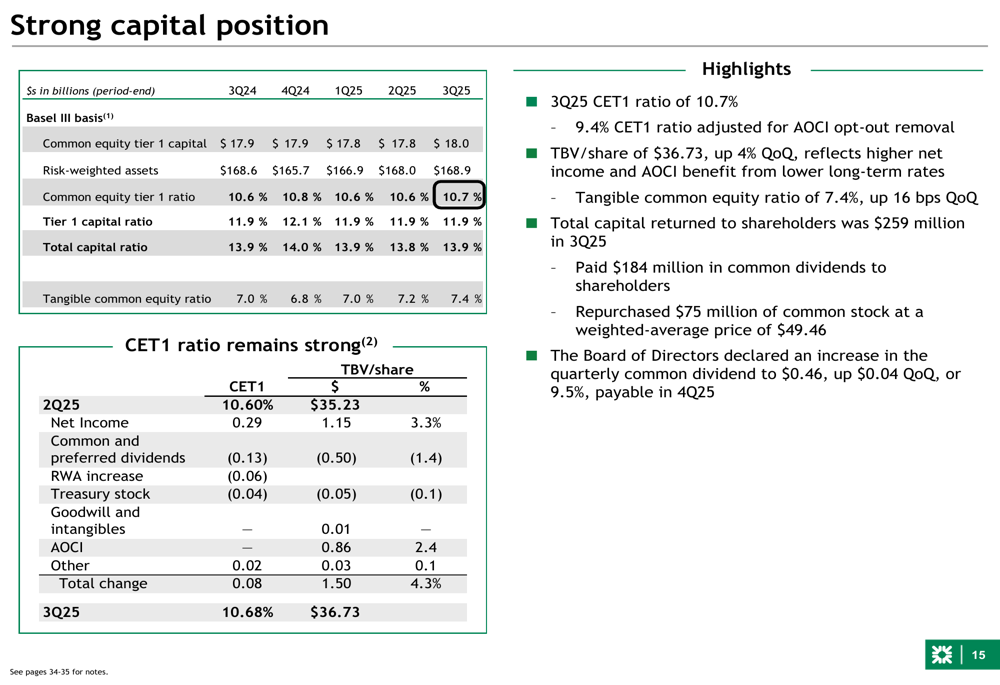

Return on tangible common equity (ROTCE) improved to 11.7%, up 70 basis points quarter-over-quarter, while the efficiency ratio showed positive trends. The bank maintained a strong capital position with a CET1 ratio of 10.7% and increased its tangible book value per share by 4% quarter-over-quarter to $36.73.

The key highlights of the quarter are summarized in this overview:

Detailed Financial Analysis

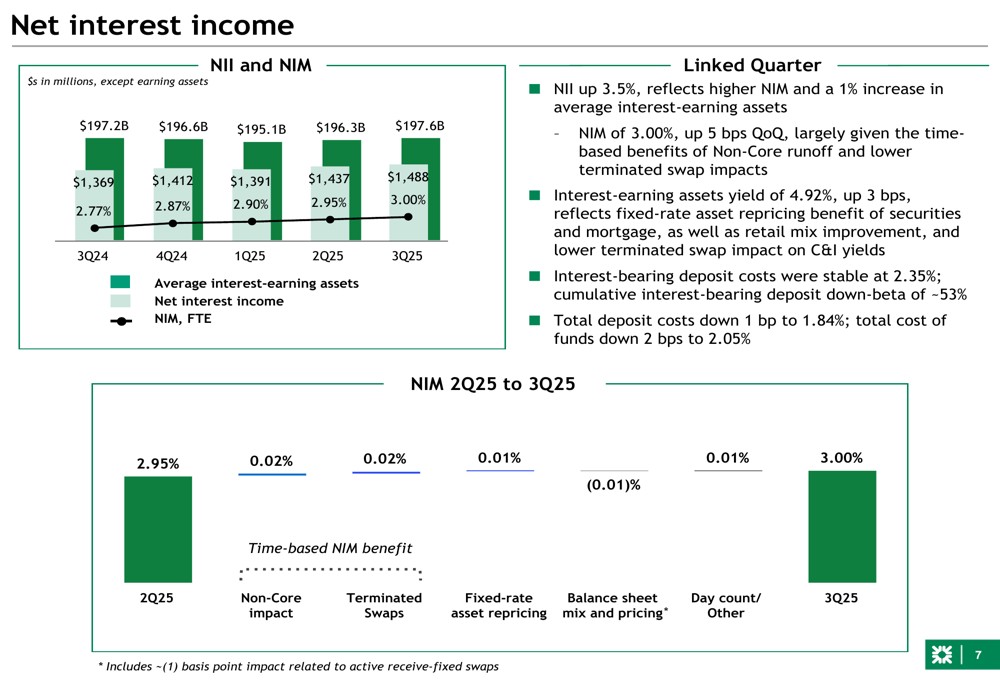

Net interest income showed steady improvement, driven by time-based benefits from non-core runoff and lower terminated swap impacts. The bank’s net interest margin continued its upward trajectory, with further expansion expected in coming quarters.

The following chart illustrates the net interest income trends and margin expansion:

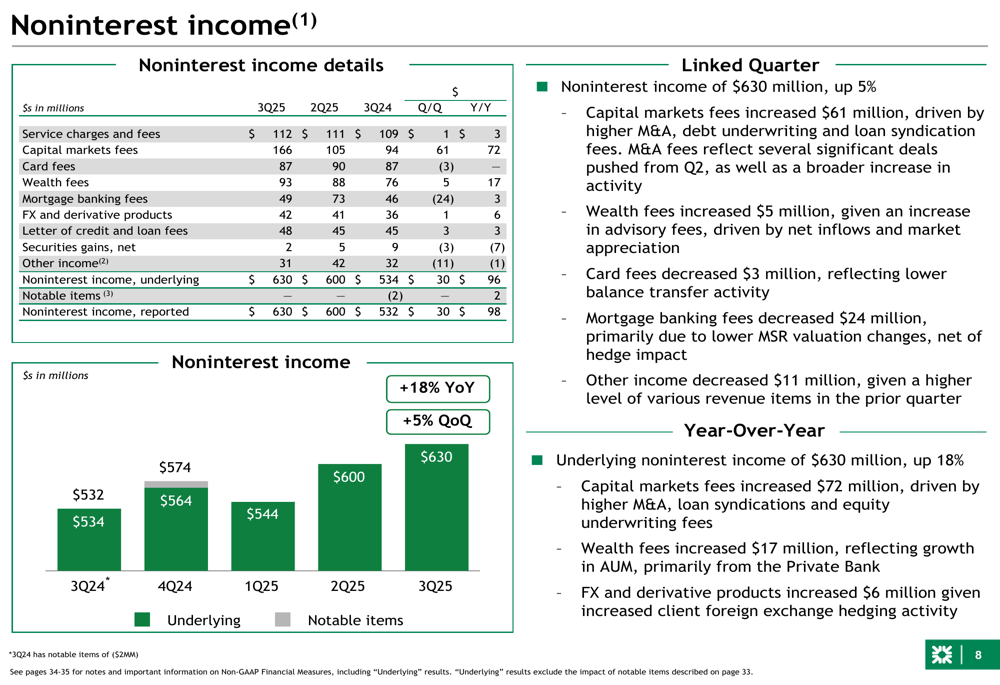

Noninterest income growth was particularly strong, with capital markets fees increasing by $61 million quarter-over-quarter and $72 million year-over-year. Wealth fees also showed positive momentum, increasing by $5 million quarter-over-quarter and $17 million year-over-year.

This breakdown shows the components driving noninterest income growth:

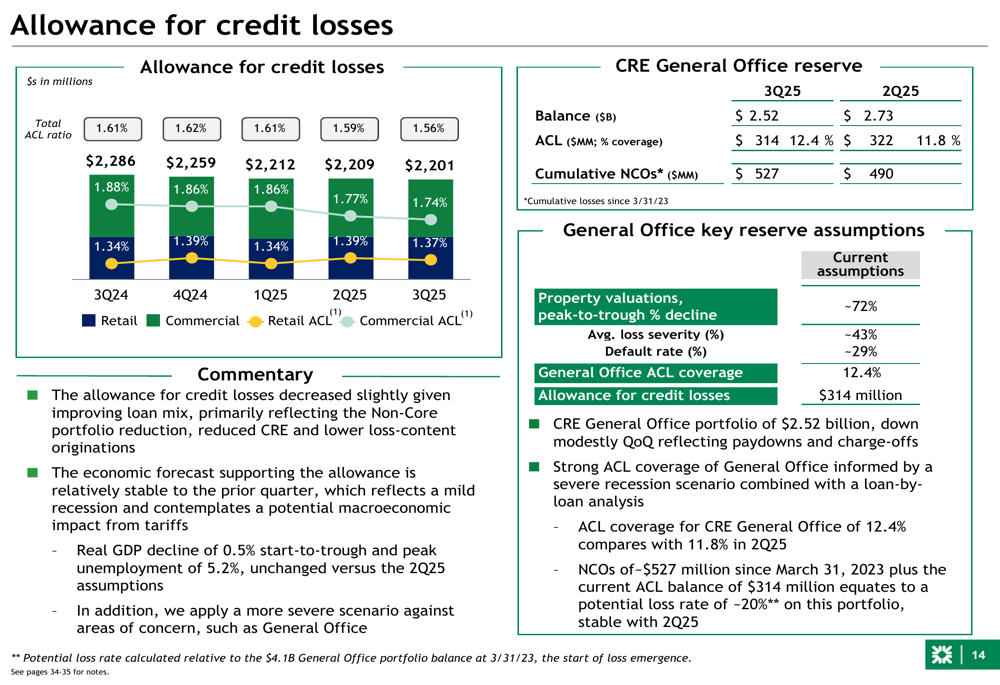

On the credit quality front, Citizens maintained strong reserves while seeing improvements in key metrics. The bank’s allowance for credit losses stands at 1.56% of loans, with particularly robust coverage for the general office commercial real estate portfolio at 12.4%.

The following slide details the bank’s approach to credit loss reserves:

Citizens returned $259 million to shareholders during the quarter, including $75 million in common stock repurchases at an average price of $49.46 per share. The bank also increased its quarterly dividend to $0.46 per share.

As shown in this capital position summary:

Strategic Initiatives

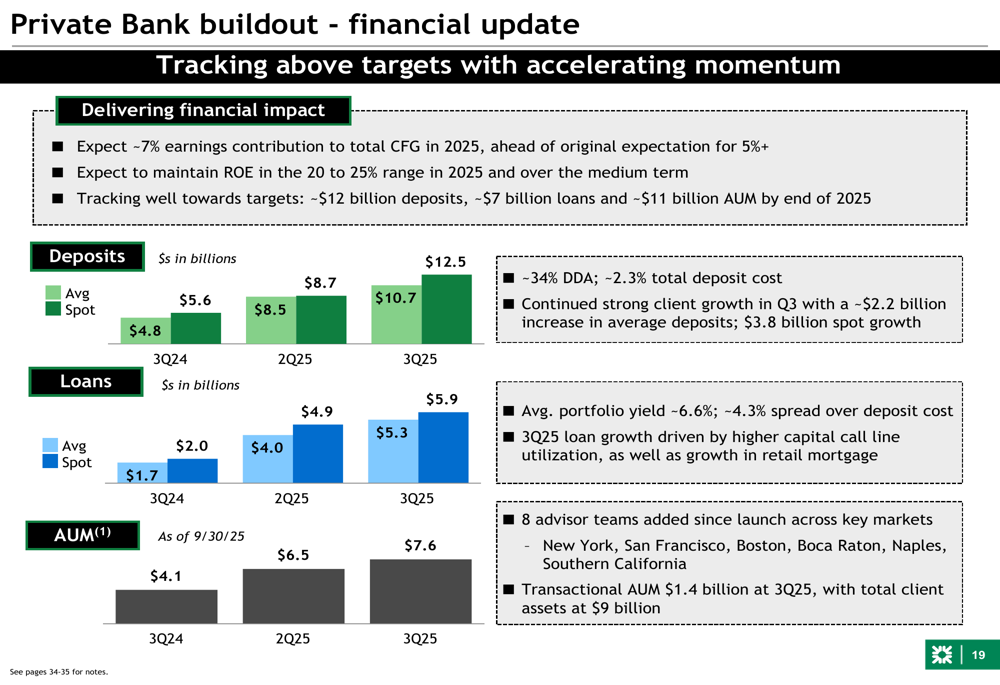

A key focus for Citizens has been the expansion of its Private Bank, which contributed $0.08 to EPS in the third quarter. The bank continues to open new Private Banking Offices (PBOs) in strategic locations including Newport Beach, San Diego, Menlo Park, West Palm Beach, and Los Angeles.

The Private Bank now has $12.5 billion in deposits, $5.9 billion in loans, and $7.6 billion in assets under management. The business is expected to contribute approximately 7% to earnings in 2025 while maintaining a return on equity in the 20-25% range.

The following financial update highlights the Private Bank’s performance:

In the Consumer Banking segment, Citizens has focused on transforming its retail deposit franchise, with approximately 56% of households in the mass affluent and above categories. The bank has achieved approximately 19% growth in average low-cost deposit balances per household and a 10% CAGR in home equity loans.

The Commercial Bank has positioned itself strongly in the middle market, mid-corporate, and sponsor client segments, with total Commercial Banking fees up 9% versus last year. The bank ranks #4 for sponsor and #8 overall in bookrunning.

Forward-Looking Statements

For the fourth quarter of 2025, Citizens expects net interest income to increase by 2.5-3% and net interest margin to expand by approximately 5 basis points. Noninterest income and noninterest expense are projected to remain stable, while credit charge-offs are expected to continue favorably in the low 40 basis points range.

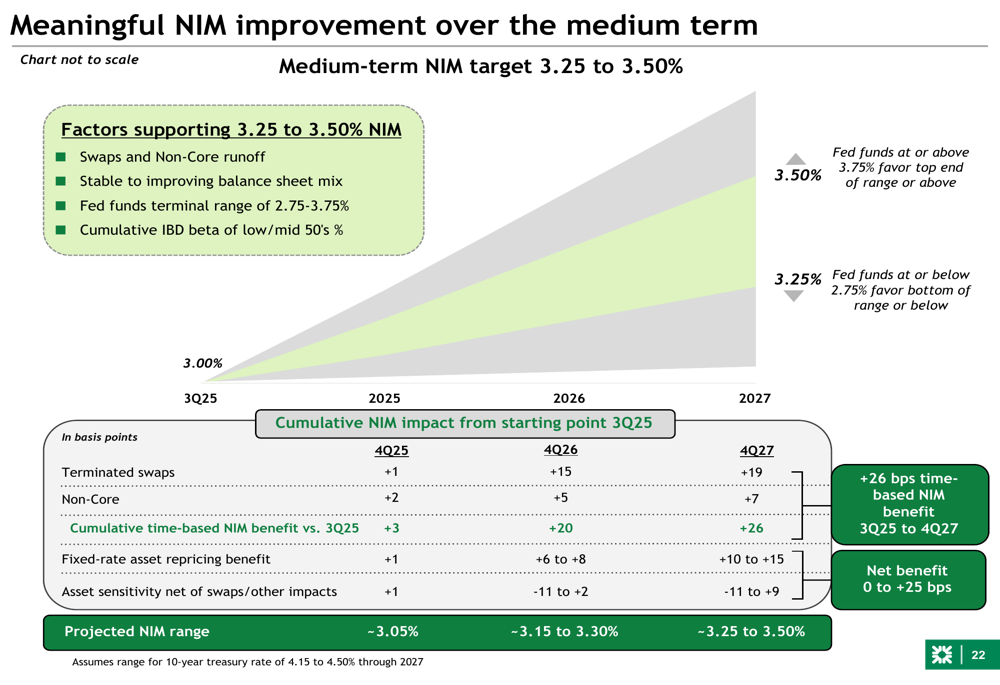

Looking further ahead, the bank has set a medium-term target for net interest margin in the 3.25-3.50% range, supported by swap impacts, non-core runoff, balance sheet mix improvements, and expectations for the Federal funds rate.

The projected NIM improvement is illustrated in this forward-looking chart:

Citizens is also implementing a "Reimagine the Bank" initiative focused on technology modernization, simplification, and cost reduction. The project aims to deliver run-rate benefits exceeding $400 million, with plans to exit data centers by year-end 2025 and standardize operational processes.

Investment Thesis

Citizens positions itself as an attractive investment opportunity based on its transformed Consumer Bank, well-positioned Commercial Bank, and growing Private Bank/Wealth franchise. The bank expects to achieve a 16-18% ROTCE over time, supported by NIM improvement and significant tailwinds from non-core operations.

As summarized in this investment thesis slide:

The strong Q3 results continue the positive momentum seen in Q2 2025, when the bank reported an EPS of $0.92 against a forecast of $0.88. With consistent execution of its strategic initiatives and ongoing margin expansion, Citizens appears well-positioned to deliver on its medium-term financial targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.