Fubotv earnings beat by $0.10, revenue topped estimates

Civitas Resources Inc (NYSE:CIVI) delivered strong second-quarter 2025 results that exceeded expectations across key operational metrics, according to the company’s latest investor presentation. The oil and gas producer is implementing strategic initiatives to optimize costs, divest non-core assets, and enhance shareholder returns while maintaining a focus on debt reduction.

Quarterly Performance Highlights

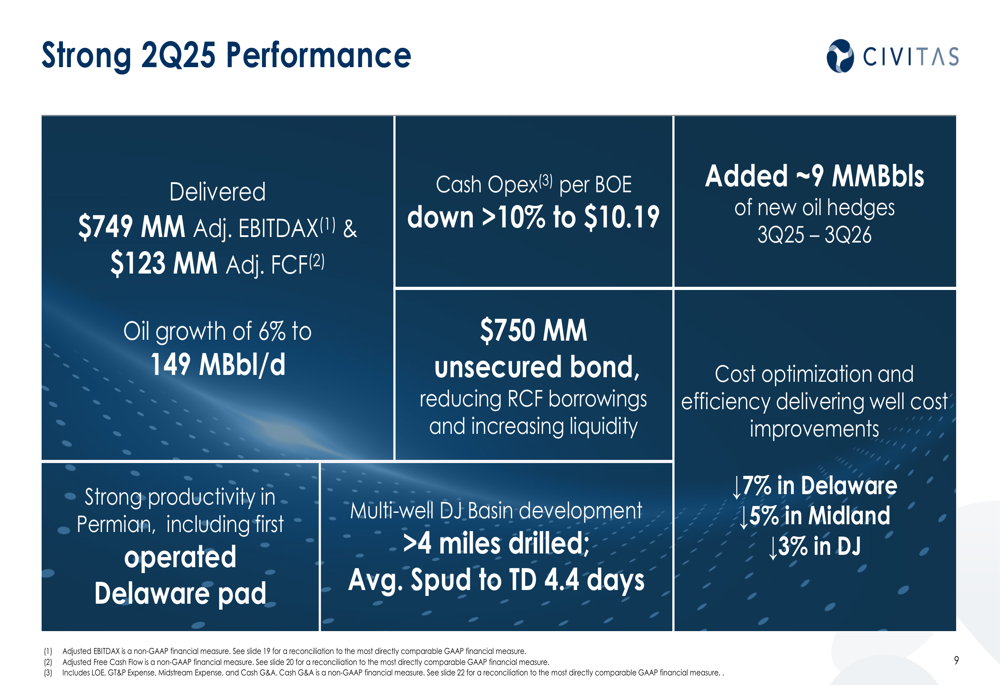

Civitas reported robust financial results for Q2 2025, generating $749 million in adjusted EBITDAX and $123 million in adjusted free cash flow. The company achieved 6% oil production growth to 149 MBbl/d while simultaneously reducing cash operating expenses per BOE by more than 10% to $10.19.

"Operating results outperformed expectations in Q2, with the company beating on oil volumes, capital expenditures, and operating costs," the presentation highlighted, demonstrating Civitas’s operational execution capabilities.

As shown in the following summary of Q2 2025 performance:

The company’s strong operational performance comes despite recent stock price pressure. Civitas shares have declined significantly over the past year, with the stock trading at $27.85 as of August 6, 2025, down 2.38% for the day and well below its 52-week high of $63.82.

Strategic Initiatives

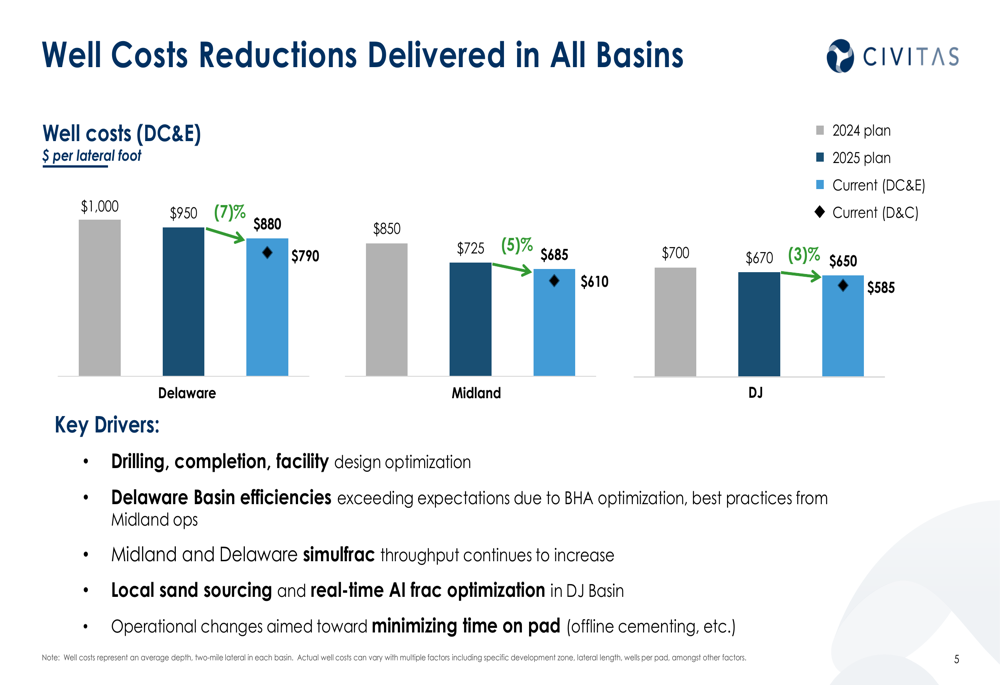

Civitas has implemented several strategic initiatives to strengthen its financial position and enhance operational efficiency. The company’s cost optimization and capital efficiency initiative is on track, with expected savings of $40 million in 2025 and a 2026 run-rate of $100 million.

A key component of this strategy has been the successful reduction of well costs across all operating basins:

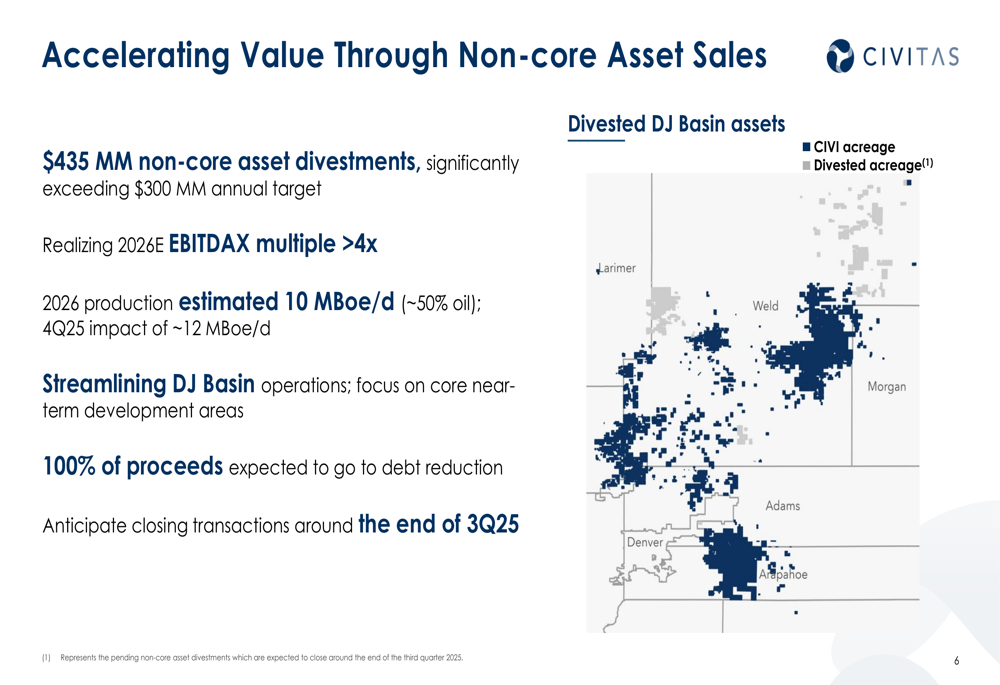

The company has also made significant progress in its asset optimization strategy, announcing $435 million in non-core DJ Basin asset sales, which substantially exceeded its year-to-date divestment goal. These transactions are expected to close around the end of Q3 2025 and will streamline operations while accelerating value from non-core assets.

"We’re accelerating value through non-core asset sales at attractive multiples exceeding 4x 2026E EBITDAX," the presentation noted. The divested assets represent approximately 10 MBoe/d of production (approximately 50% oil).

In the Permian Basin, Civitas reported impressive operational improvements, with Delaware drilling efficiency improving by approximately 20% and completions throughput increasing by approximately 50%. The company’s first operated New Mexico pad came online in late Q2, with early results in line with expectations.

Forward-Looking Guidance

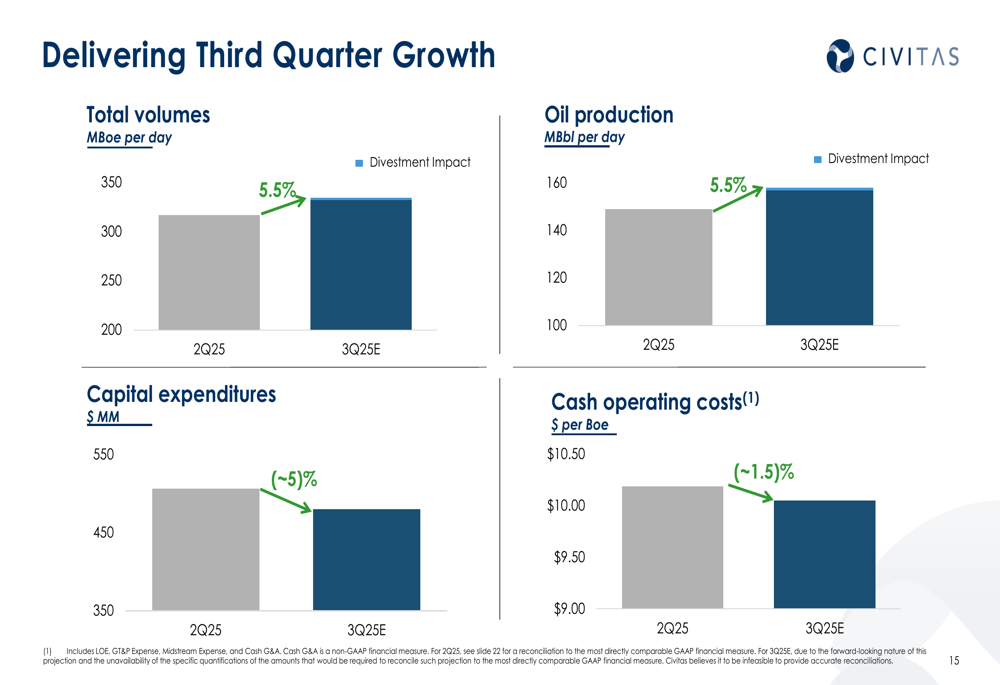

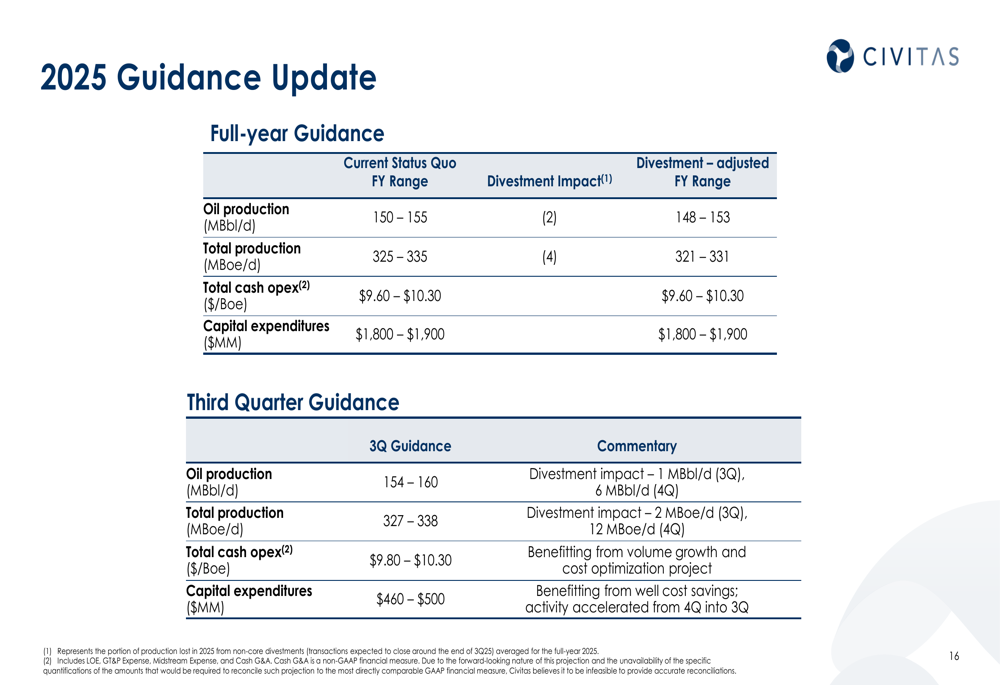

Looking ahead to Q3 2025, Civitas expects continued growth in both total volumes and oil production, while further reducing capital expenditures and operating costs:

The company has updated its full-year 2025 guidance to account for the impact of asset divestments, slightly reducing its oil production forecast to 148-153 MBbl/d from the previous 150-155 MBbl/d. Total (EPA:TTEF) production guidance has been adjusted to 321-331 MBoe/d from 325-335 MBoe/d previously.

Civitas has also enhanced its financial protection through hedging, adding approximately 9 million barrels of new oil hedges for the period from Q3 2025 through Q3 2026. The company is currently hedged at approximately 60% through the end of 2025 with an average floor of approximately $67 per barrel WTI.

Capital Allocation Strategy

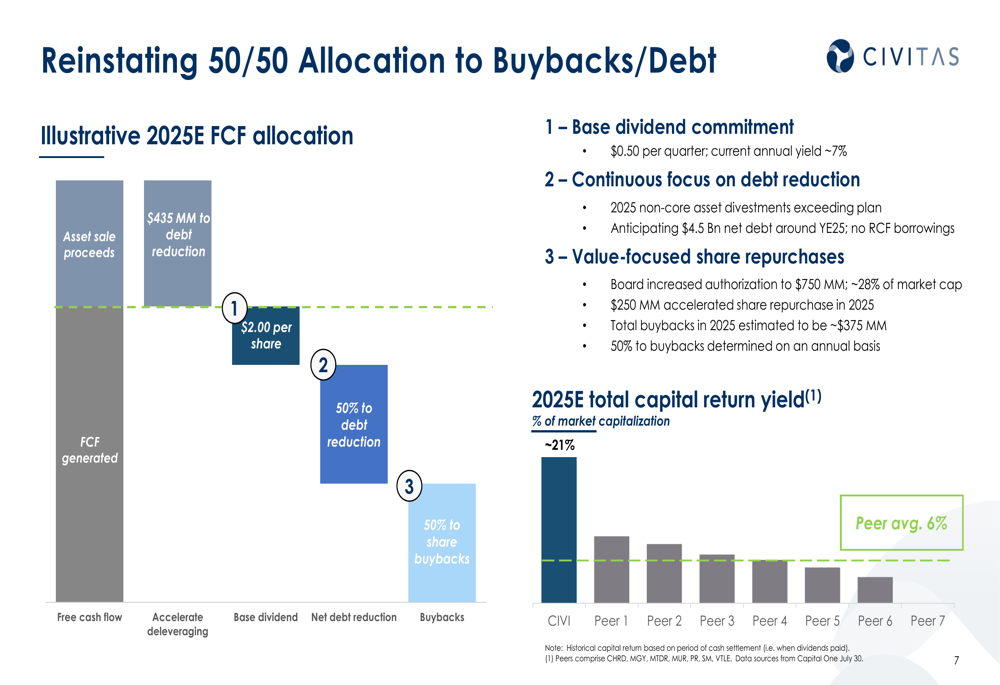

Civitas is reinstating its balanced approach to capital allocation, with a 50/50 split between share repurchases and debt reduction. The company’s board has increased its buyback authorization to $750 million, representing approximately 28% of its market capitalization, and plans to execute a $250 million accelerated share repurchase program in 2025.

The presentation highlighted Civitas’s attractive capital return yield compared to peers:

The company remains committed to its quarterly base dividend of $0.50 per share, which currently represents an annual yield of approximately 7%. Combined with the share repurchase program, Civitas estimates its 2025 total capital return yield at approximately 21%, significantly higher than the peer average of 6%.

Debt reduction continues to be a priority, with the company targeting a net debt level of approximately $4.5 billion by year-end 2025. This aligns with statements made during the Q1 2025 earnings call, where CEO Chris Doyle emphasized, "Our top priority is debt and to hit that absolute debt target by the end of the year."

Civitas has made progress in strengthening its balance sheet by issuing a $750 million unsecured bond, which reduced revolving credit facility borrowings and increased liquidity. However, net debt increased from $4,949 million at the end of December 2024 to $5,381 million as of June 30, 2025, underscoring the importance of the company’s debt reduction initiatives.

The combination of operational outperformance, strategic asset sales, and disciplined capital allocation positions Civitas to deliver enhanced shareholder returns while maintaining financial flexibility in a volatile commodity price environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.