NVIDIA launches Jetson Thor robotics computers for physical AI systems

Executive Summary

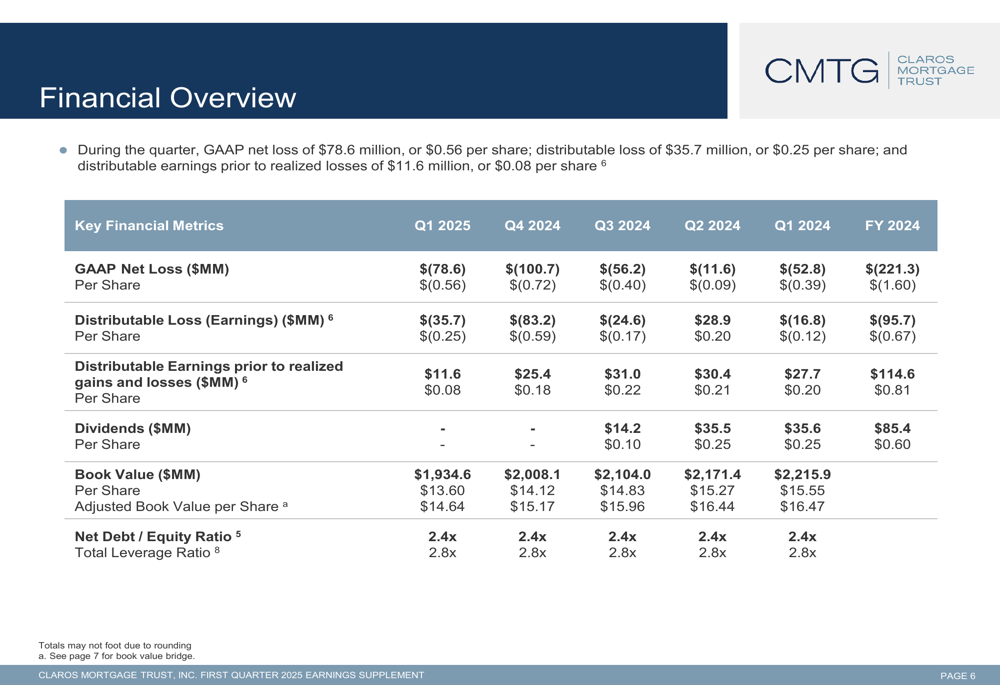

Claros Mortgage Trust , Inc. (NYSE:CMTG) reported a GAAP net loss of $78.6 million, or $0.56 per share, for the first quarter of 2025, according to the company’s earnings presentation released on May 7, 2025. The commercial real estate finance company continues to face significant headwinds, posting a distributable loss of $35.7 million ($0.25 per share), while maintaining its focus on deleveraging and resolving troubled loans.

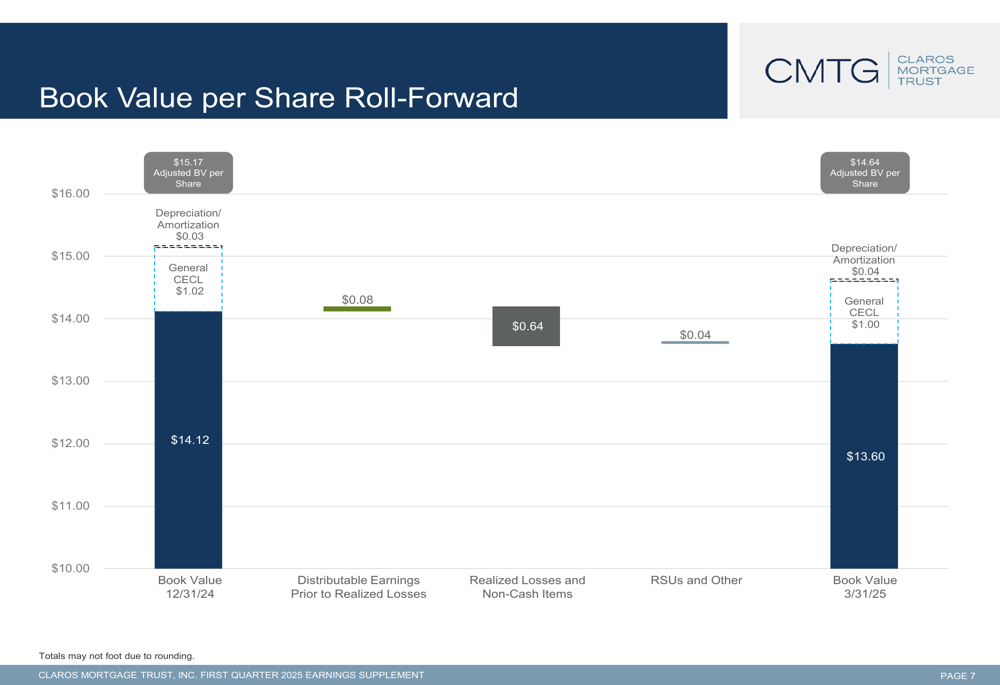

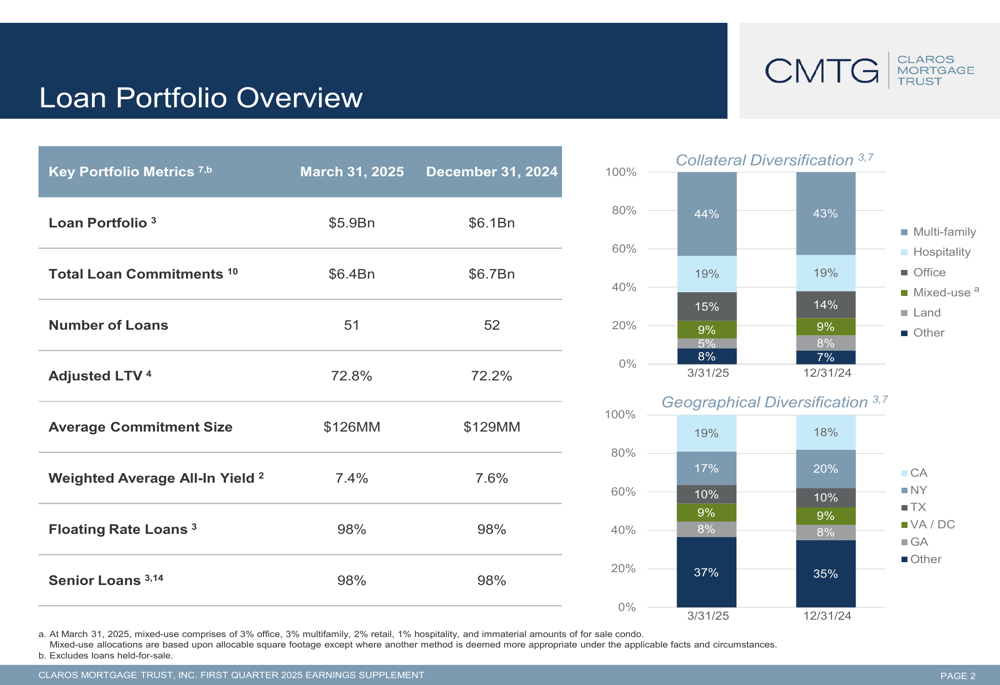

The company’s book value declined to $13.60 per share from $14.12 at the end of 2024, while its $5.9 billion loan portfolio remains heavily weighted toward multifamily properties (44%). CMTG reported total liquidity of $136 million as of March 31, including $128 million in cash, as it continues to manage through a challenging commercial real estate environment.

Quarterly Performance Highlights

Claros Mortgage Trust’s first quarter results reflect ongoing challenges in the commercial real estate sector. While the company reported distributable earnings prior to realized losses of $11.6 million ($0.08 per share), this was offset by significant provisions and valuation adjustments.

As shown in the following financial overview, CMTG has posted consistent losses over the past five quarters, with Q1 2025 showing a slight improvement over Q4 2024’s $0.72 per share loss:

The company recorded a provision for CECL (Current Expected Credit Loss) reserves of $41.1 million ($0.29 per share) during the quarter, bringing total CECL reserves to $260.8 million ($1.83 per share). Additionally, CMTG took a valuation adjustment of $42.6 million ($0.30 per share) for loan receivables held-for-sale.

The following chart illustrates the changes in book value per share during the quarter:

Loan Portfolio Analysis

CMTG’s $5.9 billion loan portfolio remains predominantly composed of floating-rate (98%) senior loans (98%). The portfolio is diversified across property types, with multifamily representing the largest segment at 44%, followed by hospitality (19%) and office (15%).

The following chart provides a detailed breakdown of the portfolio composition and geographical distribution:

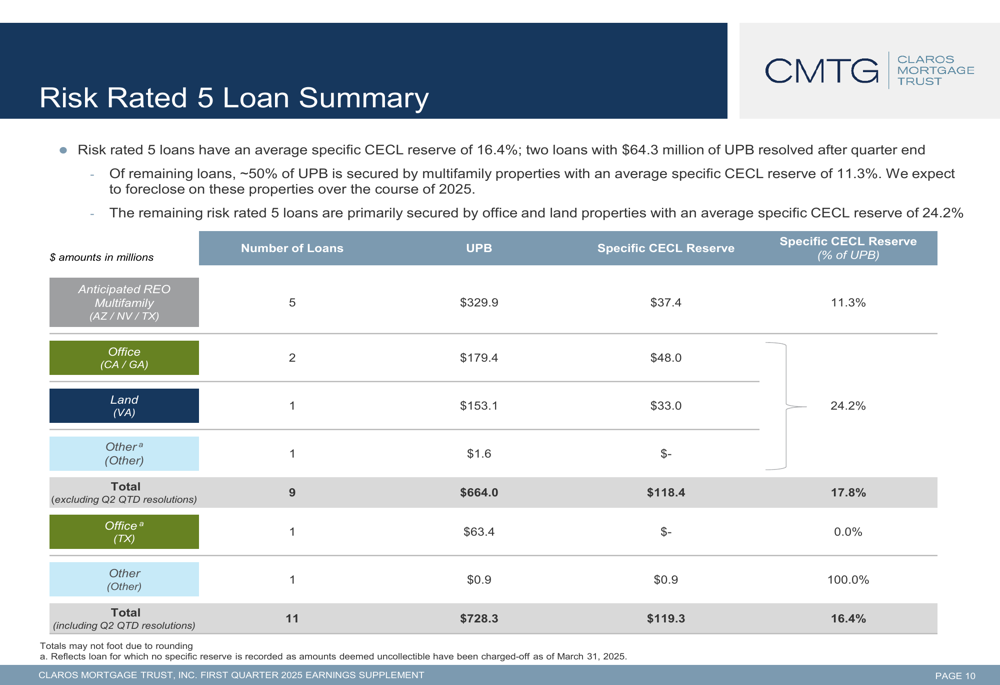

A concerning trend is the continued high proportion of troubled loans, with 46% of the portfolio risk-rated 4 or higher as of March 31, 2025, compared to 45% at the end of 2024. Risk-rated 5 loans (the most troubled category) have an average specific CECL reserve of 16.4%.

The company provided this detailed breakdown of its risk-rated 5 loans:

Liquidity and Deleveraging Progress

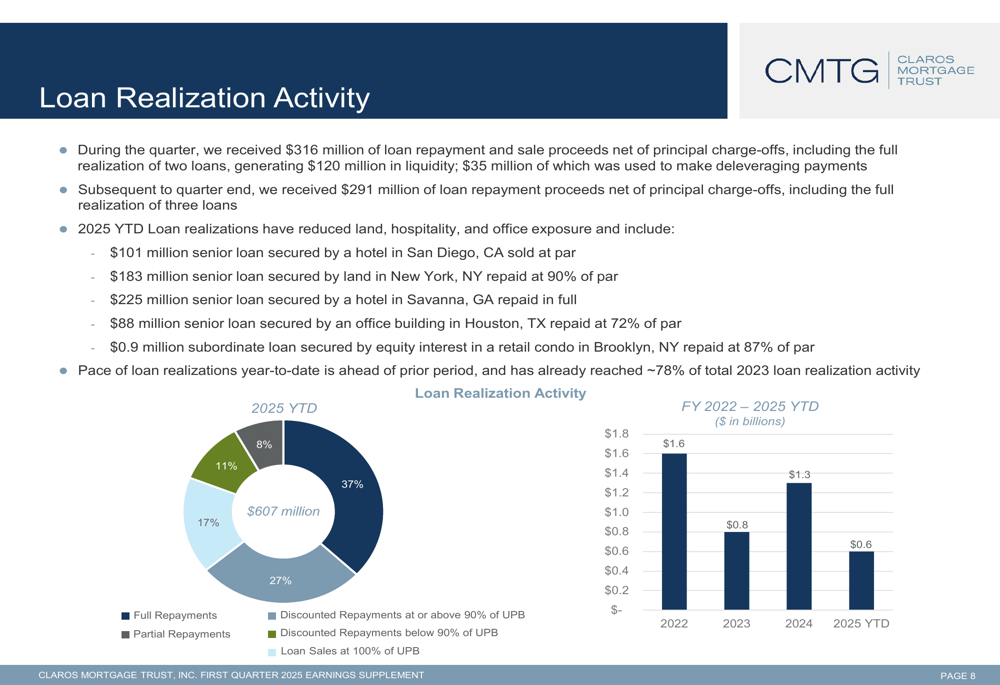

Despite the challenging environment, CMTG has made progress on its deleveraging initiatives. The company received $316 million in loan repayment and sale proceeds during Q1 2025, including the full realization of two loans generating $120 million in liquidity. An additional $291 million in loan repayment proceeds was received after the quarter ended.

As illustrated in the following chart, loan realization activity in 2025 year-to-date has already reached approximately 78% of total 2023 activity:

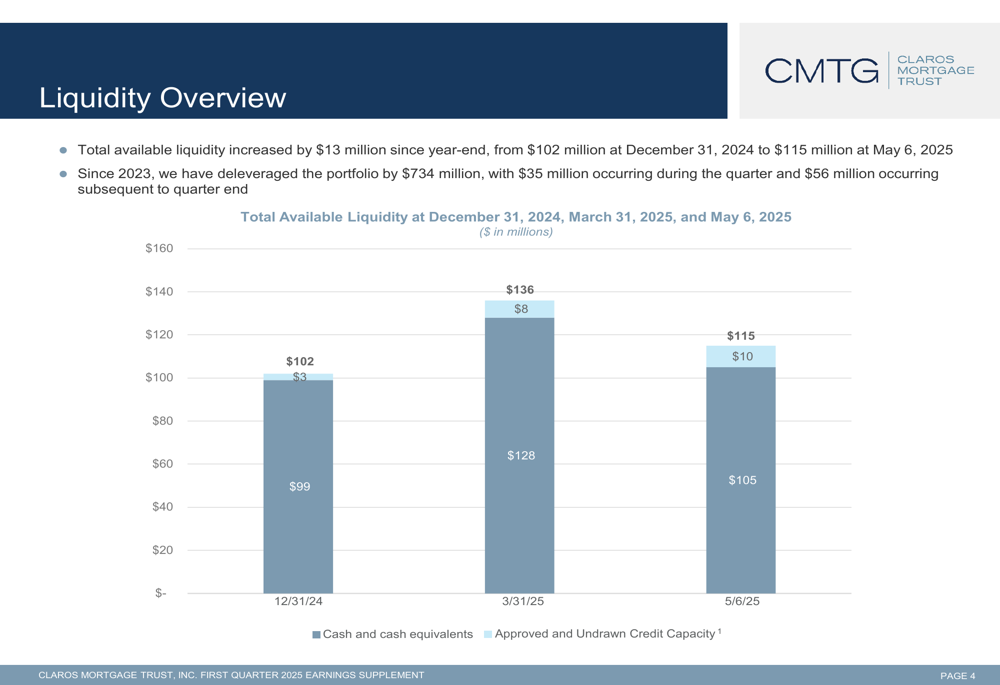

The company’s liquidity position has improved slightly since year-end, with total available liquidity increasing from $102 million at December 31, 2024, to $136 million at March 31, 2025:

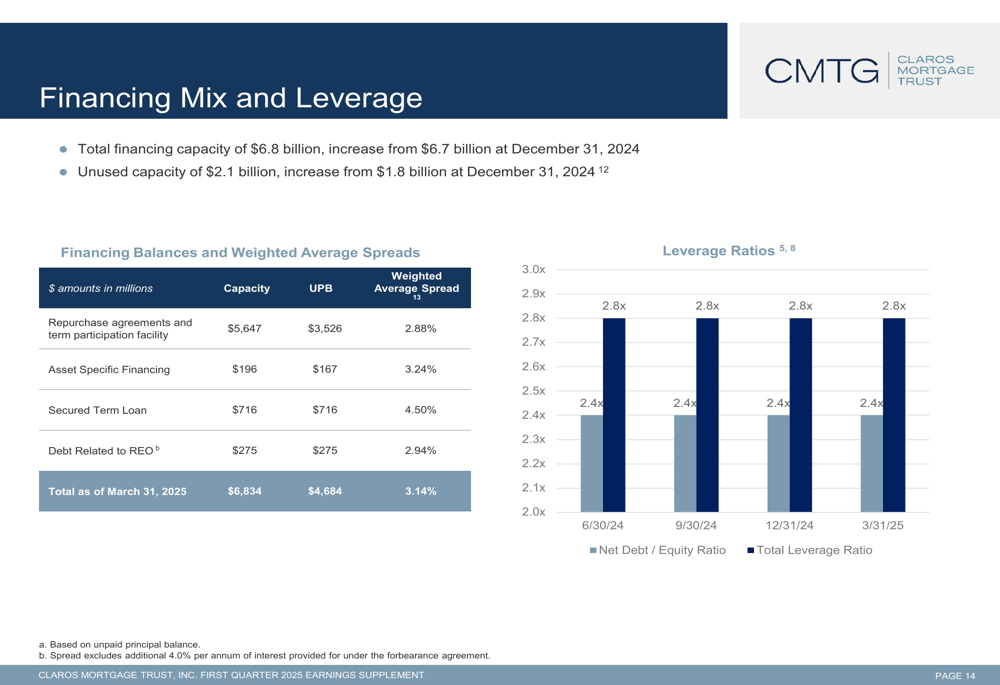

CMTG has maintained stable leverage ratios, with a net debt-to-equity ratio of 2.4x and a total leverage ratio of 2.8x, unchanged from the previous quarter. The company’s financing mix includes $5.6 billion in repurchase agreements and term participation facilities, of which $3.5 billion was outstanding at quarter-end:

Strategic Initiatives

Claros Mortgage Trust continues to focus on managing through its troubled loan portfolio while preserving liquidity. The company has significantly reduced its unfunded loan commitments, which declined from $1.9 billion at the end of 2022 to $457 million as of March 31, 2025, representing a reduction of approximately 76%.

During the quarter, CMTG closed a new financing facility with $214 million of capacity, with $205 million of financing proceeds advanced and used to repay $208 million of previously outstanding financings. Since 2023, the company has deleveraged its portfolio by $734 million.

The company is also working to resolve its real estate owned (REO) properties, including a portfolio of seven limited-service hotels in New York that is classified as held-for-sale and expected to generate approximately $50 million in liquidity. Additionally, CMTG has executed a binding agreement to sell 77,000 square feet of office and retail space in a mixed-use property in New York for $28.8 million.

Forward-Looking Statements

While the Q1 2025 presentation did not include explicit forward guidance, the company’s focus on deleveraging, resolving troubled loans, and maintaining liquidity suggests a continued defensive posture in the face of ongoing commercial real estate market challenges.

This approach aligns with statements made during the company’s Q3 2024 earnings call, where management anticipated increased transaction volumes in 2025, particularly in the multifamily sector, and expressed optimism about market stabilization. However, the continued high proportion of risk-rated loans and ongoing losses indicate that significant challenges remain.

The pace of loan realizations in 2025 is ahead of the prior period, which could provide additional liquidity for the company as it works through its troubled assets. However, investors should note that CMTG did not declare a dividend for Q1 2025, continuing the pattern from Q4 2024, after reducing its dividend from $0.25 to $0.10 per share in Q3 2024.

As of May 7, 2025, Claros Mortgage Trust’s stock price was $2.67, up 5.12% for the day, but well below its 52-week high of $9.81 and near its 52-week low of $2.13, reflecting investor concerns about the company’s ongoing challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.