Street Calls of the Week

Introduction & Market Context

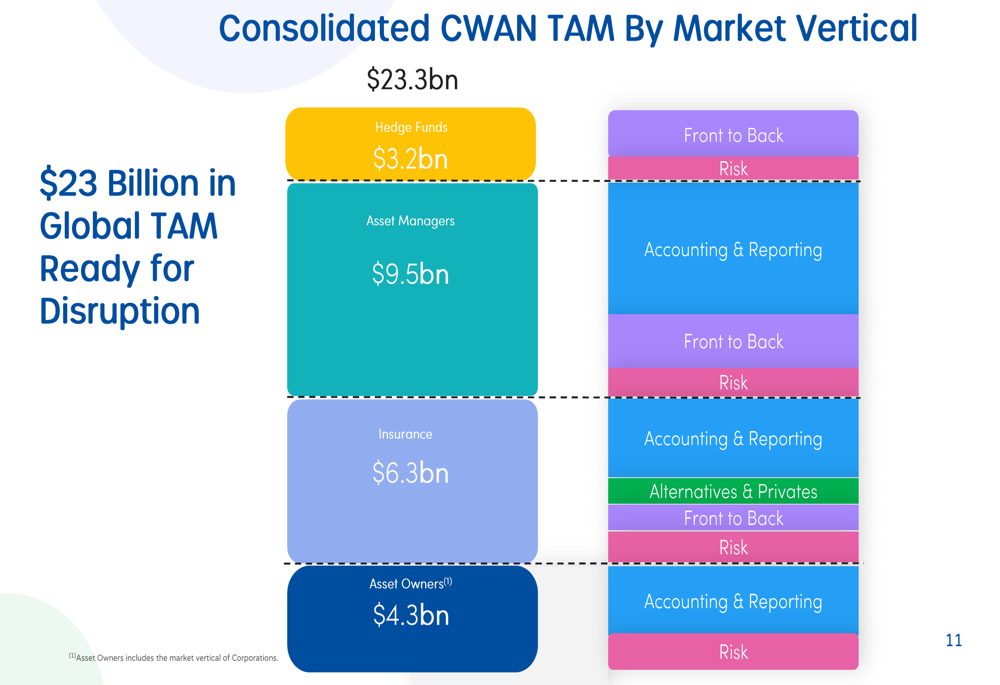

Clearwater Analytics Holdings Inc (NYSE:CWAN) presented its Q2 2025 investor presentation on August 6, highlighting significant growth driven by strategic acquisitions and organic expansion. The company, which provides a comprehensive investment management technology platform, has positioned itself to address a $23.3 billion total addressable market across insurance, asset management, hedge funds, and asset owner verticals.

The presentation comes as Clearwater’s stock trades near its 52-week low of $17.98, despite strong operational performance. Following the earnings announcement, the stock saw modest movement, with premarket trading showing a 0.36% increase to $19.44 as of August 15.

Quarterly Performance Highlights

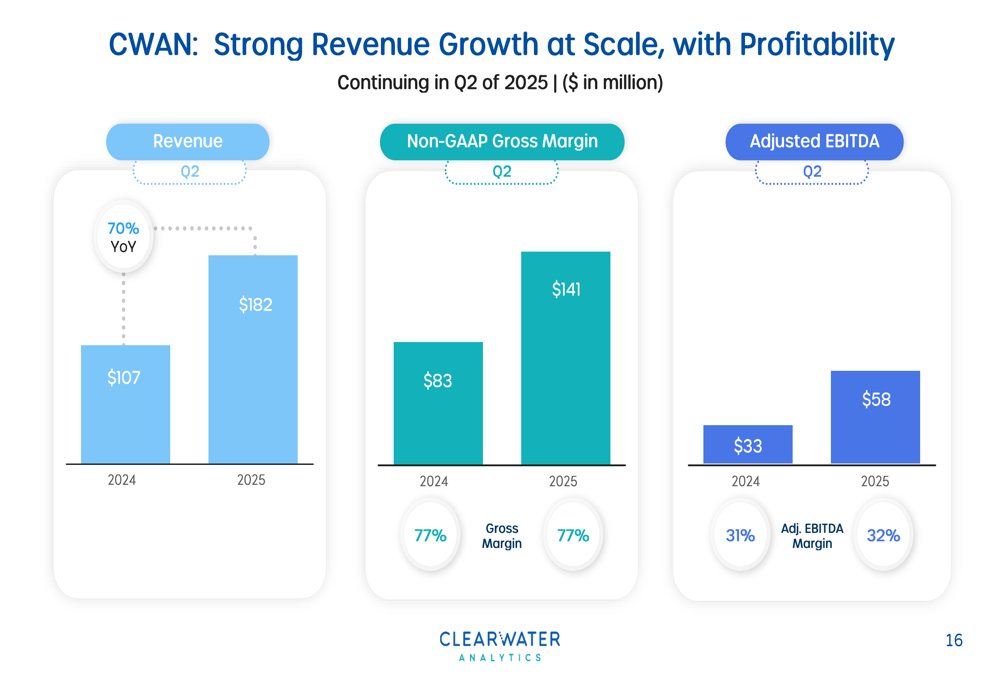

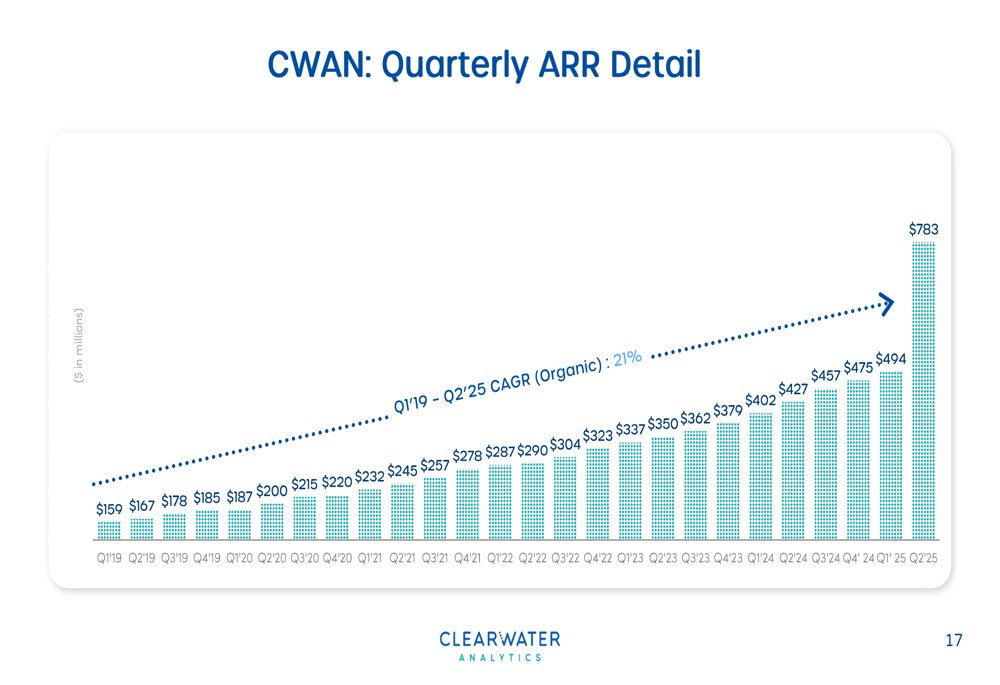

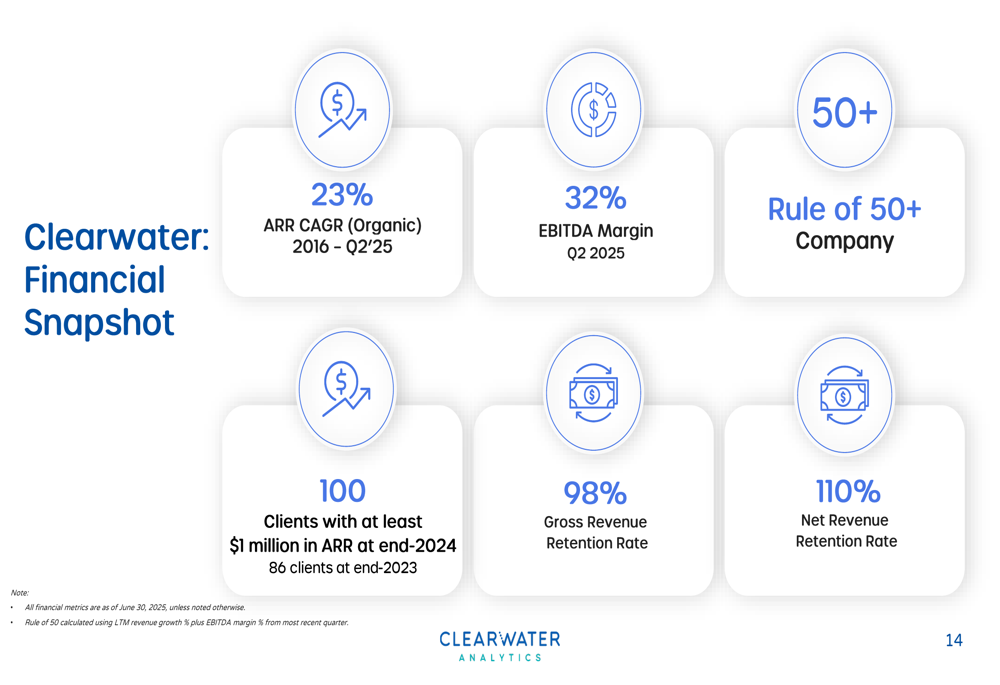

Clearwater reported impressive Q2 2025 results, with revenue reaching $182 million, representing a 70% year-over-year increase from $107 million in Q2 2024. The company’s Annual Recurring Revenue (ARR) reached $783 million, maintaining a 23% organic compound annual growth rate (CAGR) from 2016 to Q2 2025.

As shown in the following chart of quarterly revenue and profitability metrics:

The company maintained its gross margin at 77% while improving its Adjusted EBITDA margin to 32% in Q2 2025, up from 31% in the same period last year. This performance exceeded analyst expectations, with earnings per share of $0.12 surpassing the forecast of $0.11.

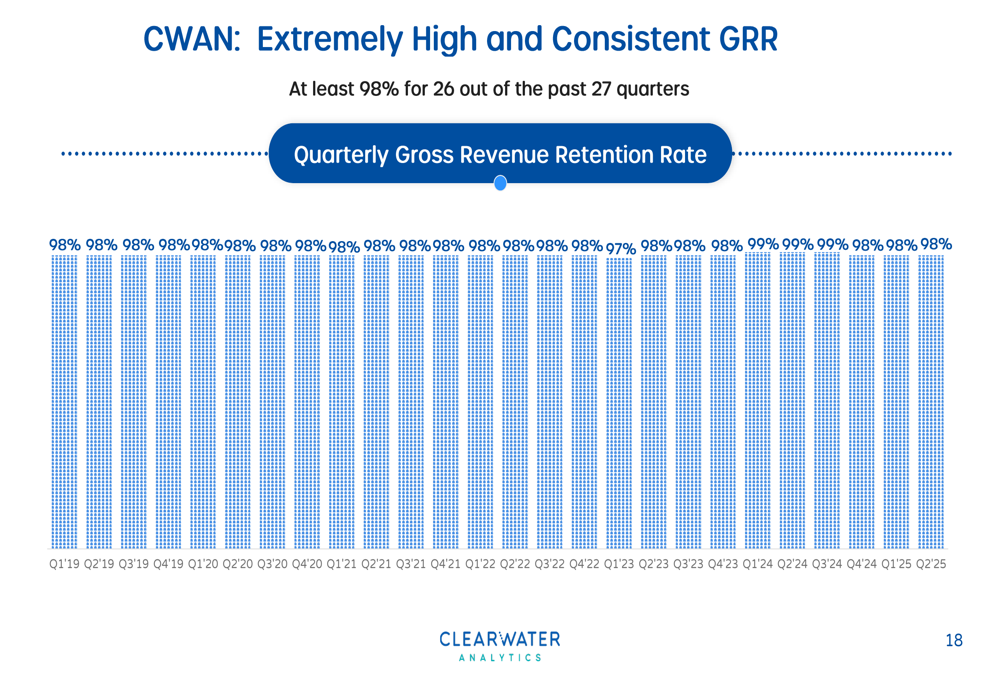

Clearwater’s client retention metrics remain exceptionally strong, with a 98% Gross Revenue Retention Rate and 110% Net Revenue Retention Rate, indicating both strong client loyalty and successful upselling efforts. The company’s quarterly ARR growth has been consistent since 2019, as illustrated in this chart:

The company’s high retention rates have been remarkably consistent over time:

Strategic Initiatives and Growth Opportunities

Clearwater’s presentation outlined several strategic growth initiatives, including deepening relationships with existing clients, gaining market share within asset managers and insurers, accelerating growth in hedge funds, and expanding globally. The company noted that it maintains an approximately 80% win rate in North America insurance and asset management sectors.

The company’s consolidated total addressable market of $23.3 billion is broken down across various verticals:

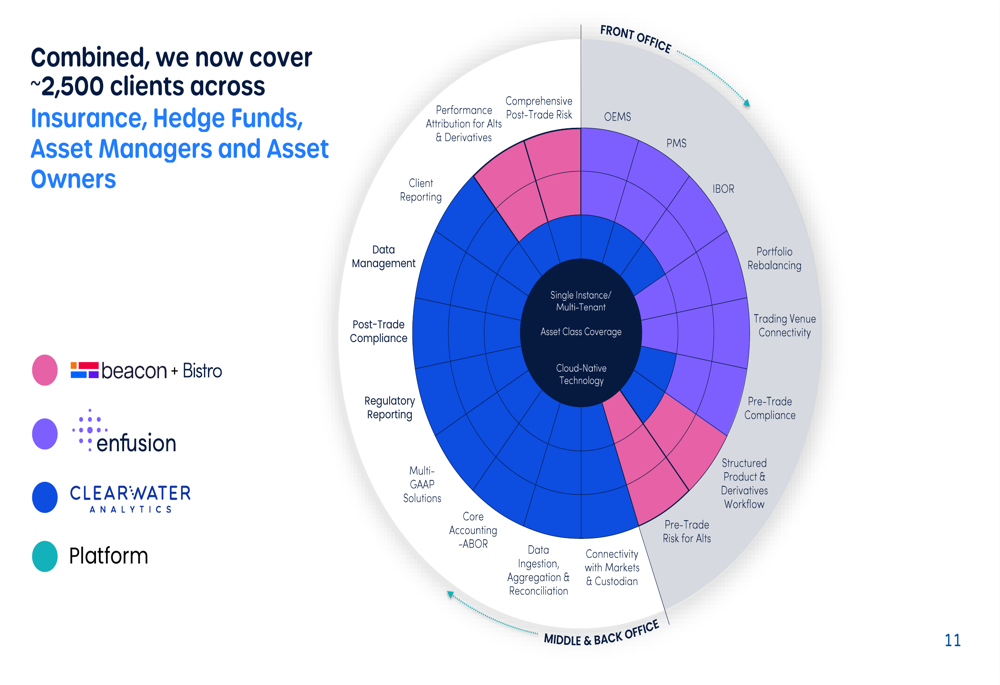

Recent acquisitions, including Enfusion, Beacon, and Bistro, have expanded Clearwater’s capabilities across front, middle, and back office functions. These acquisitions have contributed to the company’s ability to serve approximately 2,500 clients across various sectors, as visualized in the following capability matrix:

CEO Sandeep Sahai emphasized the transformative potential of generative AI during the earnings call, stating, "We think generative AI will change everything about our business and our clients’ business." He also articulated the company’s vision to "build the nervous system of the future investment management industry."

Detailed Financial Analysis

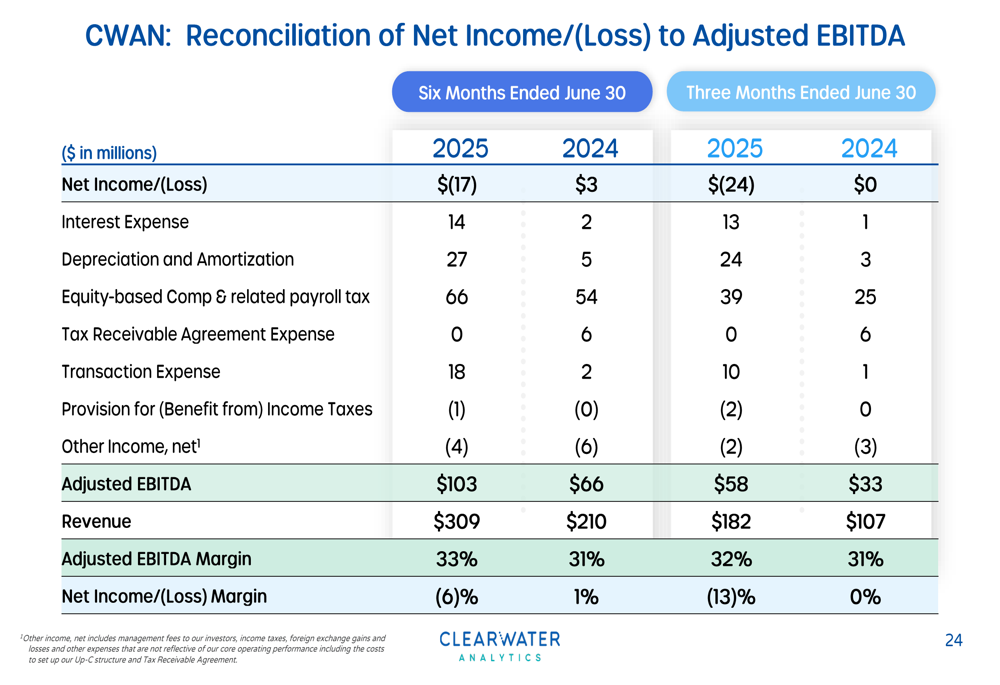

While Clearwater’s top-line growth has been impressive, the company reported a net loss of $24 million for Q2 2025, compared to breakeven results in Q2 2024. This loss occurred despite the strong revenue growth and can be attributed to several factors, including increased interest expenses, higher depreciation and amortization, and significant transaction expenses related to recent acquisitions.

The reconciliation from net loss to Adjusted EBITDA reveals these underlying factors:

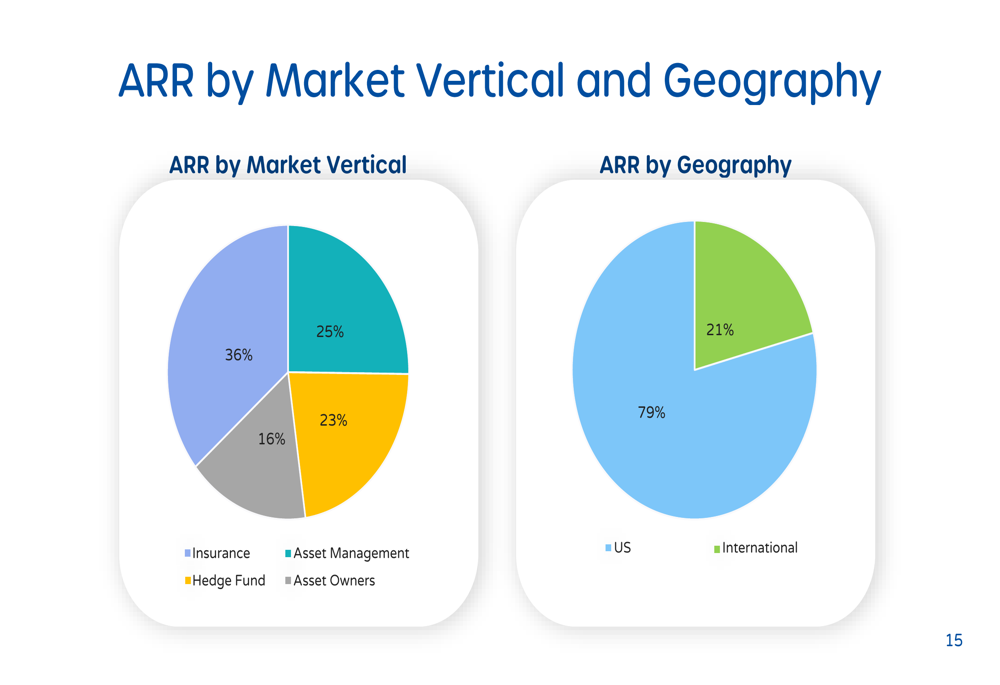

The company’s ARR is diversified across market verticals and geographies, providing some resilience against sector-specific downturns:

Clearwater’s financial snapshot highlights its strong business fundamentals:

Forward-Looking Statements

Looking ahead, Clearwater Analytics has provided full-year 2025 revenue guidance between $726 million and $732 million, representing 61-62% year-over-year growth. The company also anticipates adjusted EBITDA to range from $232 million to $237 million.

Management has identified several enhanced opportunities for growth:

However, investors should be aware of potential risks, including integration challenges from recent acquisitions, increasing competition in the investment management technology sector, and macroeconomic pressures that could affect client investment decisions. The significant increase in interest expenses and transaction costs also bears watching in future quarters.

The company’s global team of over 2,900 employees across the United States, EMEA, and APAC regions positions it well to pursue international growth opportunities, with management noting that half of the world’s wealth exists outside North America.

Despite the net loss in Q2, Clearwater’s strong recurring revenue model, high client retention rates, and expanding market presence suggest the company remains well-positioned for long-term growth as it integrates its recent acquisitions and continues to expand its platform capabilities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.