Hyperscale Data reduces debt by $30 million for AI, bitcoin expansion

Introduction & Market Context

Cleveland-Cliffs Inc. (NYSE:CLF) presented its second-quarter 2025 earnings on July 21, showing signs of recovery with a return to positive EBITDA after a challenging first quarter. The company’s stock responded positively, trading up 3.27% in premarket at $9.79, following the presentation that highlighted record steel shipments and strategic initiatives to improve profitability.

The steel producer’s Q2 results come against the backdrop of strengthened trade policies, with steel tariffs raised to 50% for major importing countries, creating a more favorable environment for domestic producers. This marks a significant improvement from Q1 2025, when the company reported a larger-than-expected loss with an EPS of -$0.92 and negative adjusted EBITDA of -$174 million.

Quarterly Performance Highlights

Cleveland-Cliffs reported Q2 2025 revenues of $4.9 billion, supported by record steel shipments of 4.3 million net tons. The company achieved an adjusted EBITDA of $97 million, a substantial improvement from the -$174 million reported in the previous quarter. Liquidity remained strong at $2.7 billion.

As shown in the following chart of key financial metrics for Q2 2025:

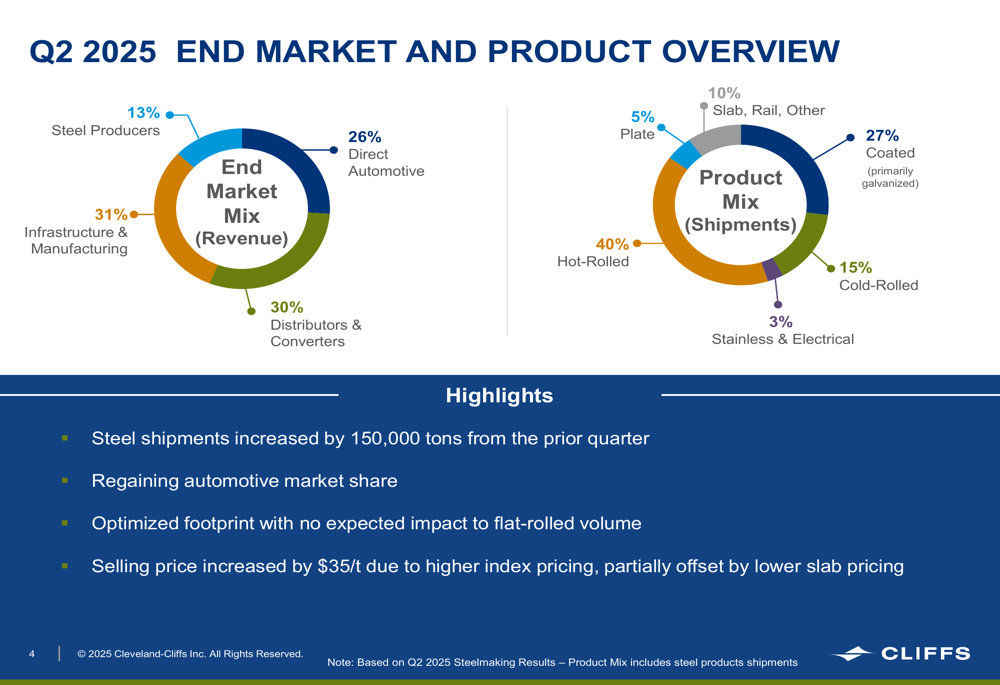

Steel shipments increased by 150,000 tons from the prior quarter, with the company noting it was regaining automotive market share. The average selling price increased by $35 per ton due to higher index pricing, though this was partially offset by lower slab pricing.

The company’s end market mix shows a diversified customer base, with Infrastructure & Manufacturing accounting for 31% of revenue, Direct Automotive representing 26%, and Distributors & Converters making up 30%. In terms of product mix, Hot-Rolled steel remains the dominant product at 40% of shipments, followed by Coated products at 27%.

As illustrated in this breakdown of end markets and product mix:

The record quarterly steel shipments represent a culmination of a gradual recovery trend, as shown in the following historical chart:

Strategic Initiatives

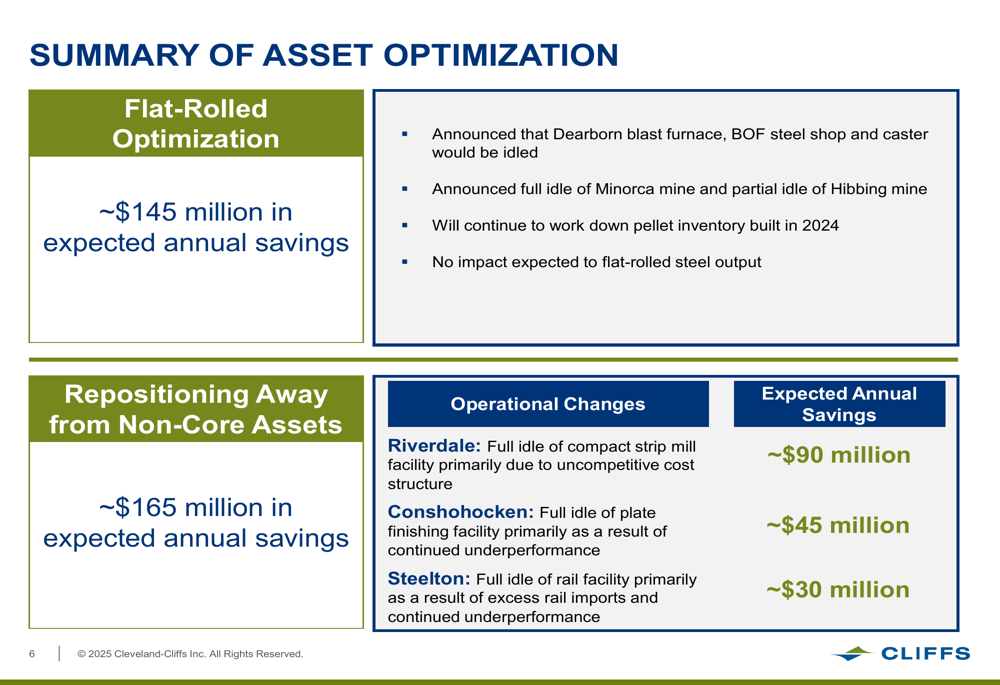

Cleveland-Cliffs outlined several strategic initiatives aimed at optimizing operations and reducing costs. The company expects to achieve $145 million in annual savings from flat-rolled optimization, which includes idling the Dearborn blast furnace, BOF steel shop and caster, as well as the full idle of Minorca mine and partial idle of Hibbing mine.

Additionally, the company is repositioning away from non-core assets, targeting $165 million in expected annual savings. This includes the full idle of facilities at Riverdale, Conshohocken, and Steelton due to uncompetitive cost structures and underperformance.

The comprehensive asset optimization strategy is detailed in the following summary:

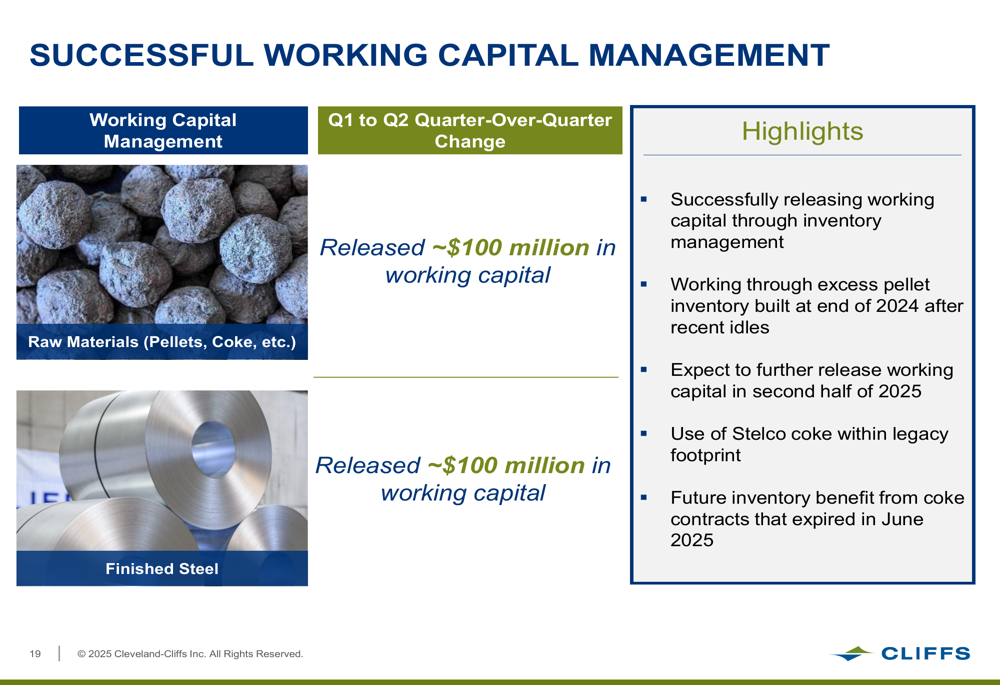

The company is also making progress on working capital management, releasing approximately $200 million in inventory working capital during Q2, with plans to further release working capital in the second half of 2025.

As shown in this working capital management overview:

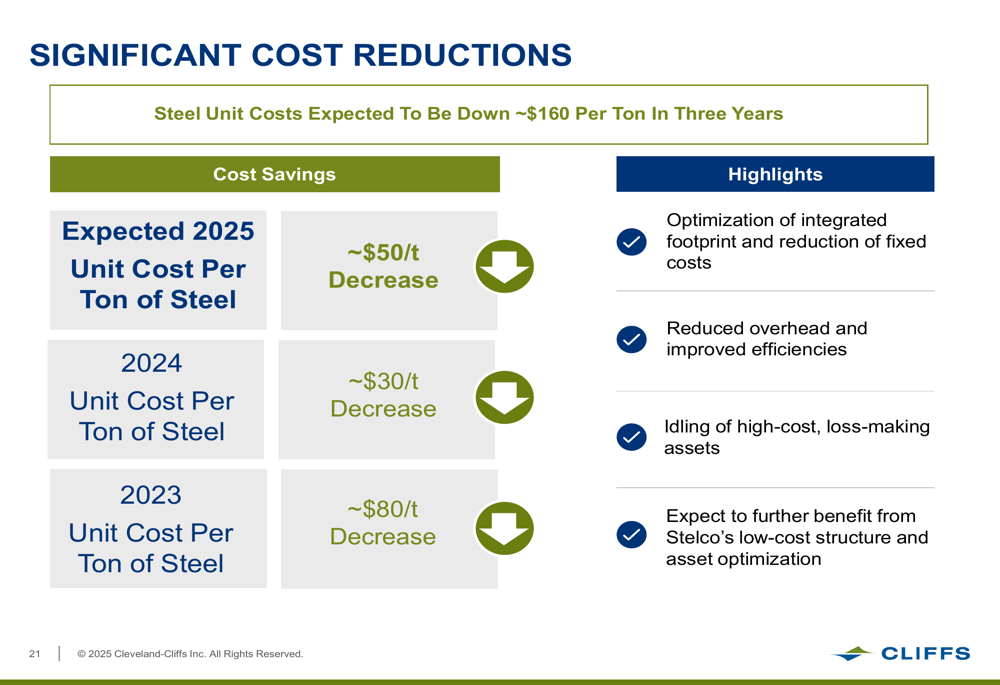

Cleveland-Cliffs expects significant cost reductions, with steel unit costs projected to decrease by approximately $160 per ton over three years. For 2025 specifically, the company anticipates a reduction of about $50 per ton.

The cost reduction trajectory is illustrated in this chart:

Competitive Industry Position

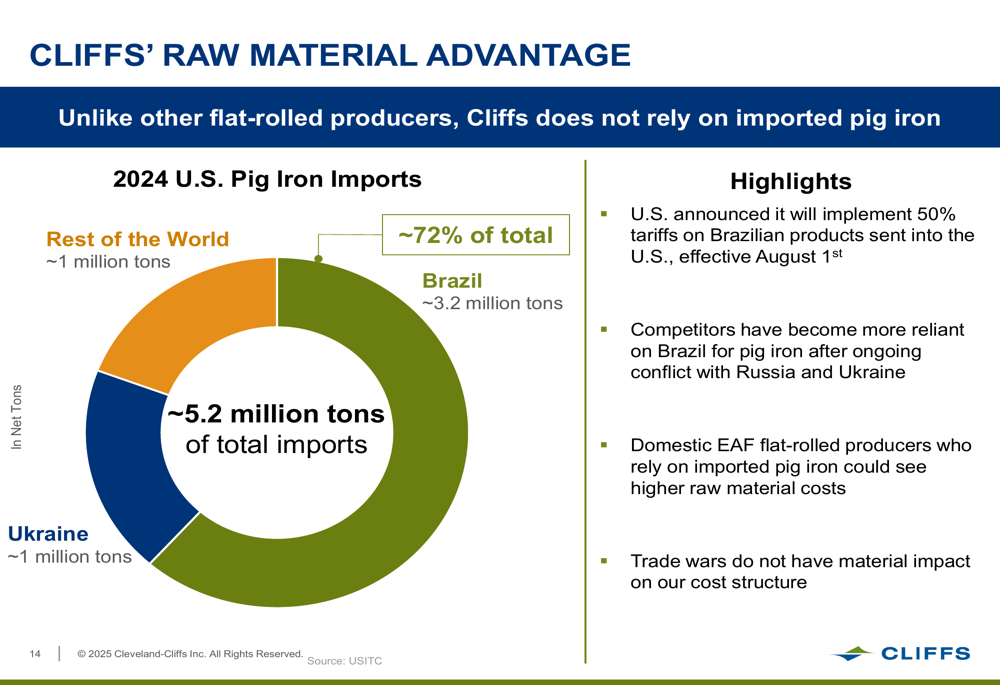

Cleveland-Cliffs highlighted its competitive advantage in raw materials, noting that unlike other flat-rolled producers, it does not rely on imported pig iron. This positions the company favorably as the U.S. implements 50% tariffs on Brazilian products effective August 1, which could increase raw material costs for competitors who depend on imported pig iron.

The company’s raw material advantage is depicted in the following chart:

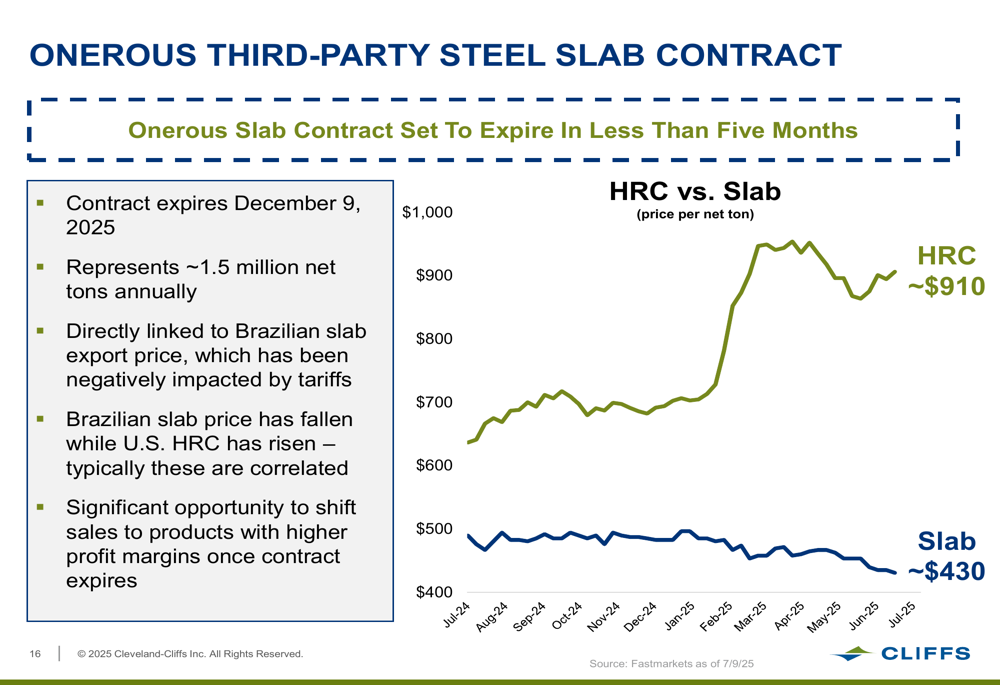

Another significant opportunity lies in the expiration of an "onerous" third-party steel slab contract on December 9, 2025. This contract represents approximately 1.5 million net tons annually and is directly linked to Brazilian slab export prices, which have been negatively impacted by tariffs. The company sees this as an opportunity to shift sales to products with higher profit margins once the contract expires.

As illustrated in this chart showing the divergence between HRC and slab prices:

Forward-Looking Statements

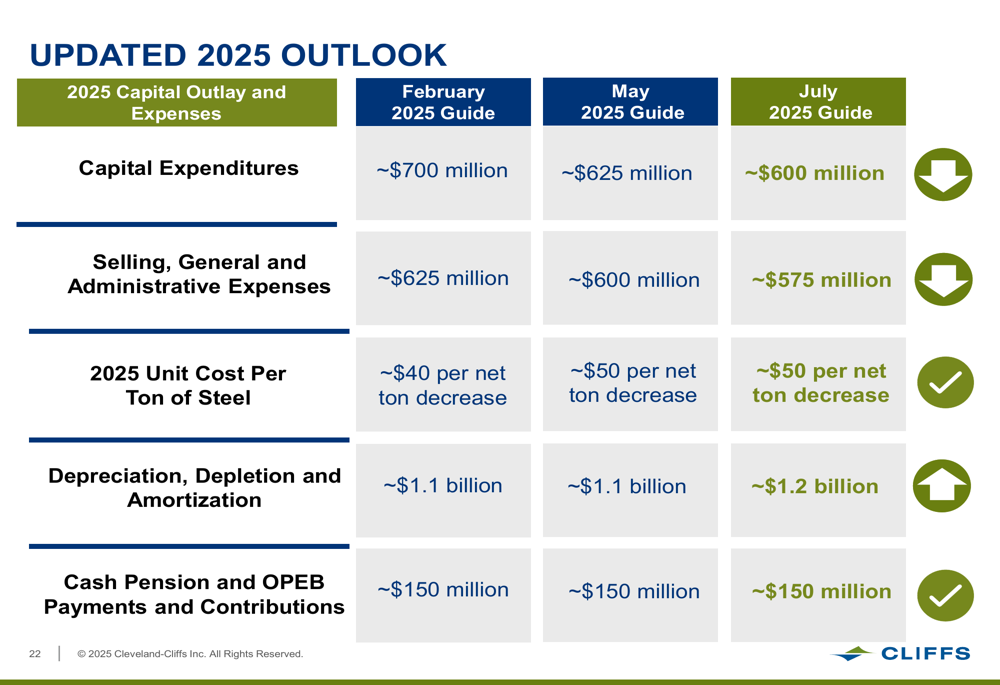

Cleveland-Cliffs provided an updated outlook for 2025, reducing its capital expenditure guidance to approximately $600 million from the previous $700 million forecast in February. Similarly, selling, general and administrative expenses are now expected to be around $575 million, down from the earlier estimate of $625 million.

The company maintained its guidance for a decrease in unit cost per ton of steel of approximately $50 for 2025, while slightly increasing its depreciation, depletion and amortization forecast to $1.2 billion.

The updated 2025 guidance is summarized in the following table:

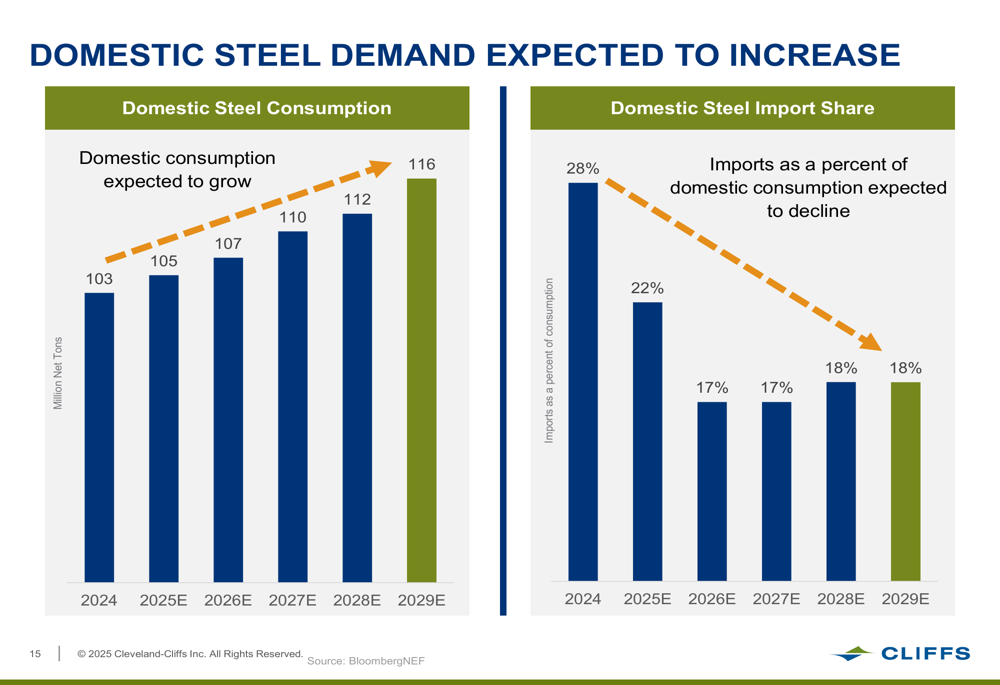

Looking ahead, Cleveland-Cliffs expects domestic steel demand to increase, with consumption projected to rise from 103 million net tons in 2024 to 105 million net tons in 2025, and continuing upward to 116 million net tons by 2029. Simultaneously, imports as a percentage of consumption are expected to decline from 28% in 2024 to 22% in 2025 and stabilize around 18% in later years.

The domestic steel demand forecast is presented in this chart:

Management expressed confidence in continued improvement in adjusted EBITDA from Q2 to Q3, supported by higher pricing that began in late Q1 and ongoing cost reduction initiatives. This represents a significant turnaround from the company’s challenging first quarter, when CEO Lorenzo Gonsalves acknowledged that results were "unacceptable."

The company remains committed to utilizing 100% of its cash flow toward debt repayment, with a leverage target (Net debt / TTM Adj. EBITDA) of 2.5x, reinforcing its focus on strengthening the balance sheet while navigating the recovery path.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.