Street Calls of the Week

Introduction & Market Context

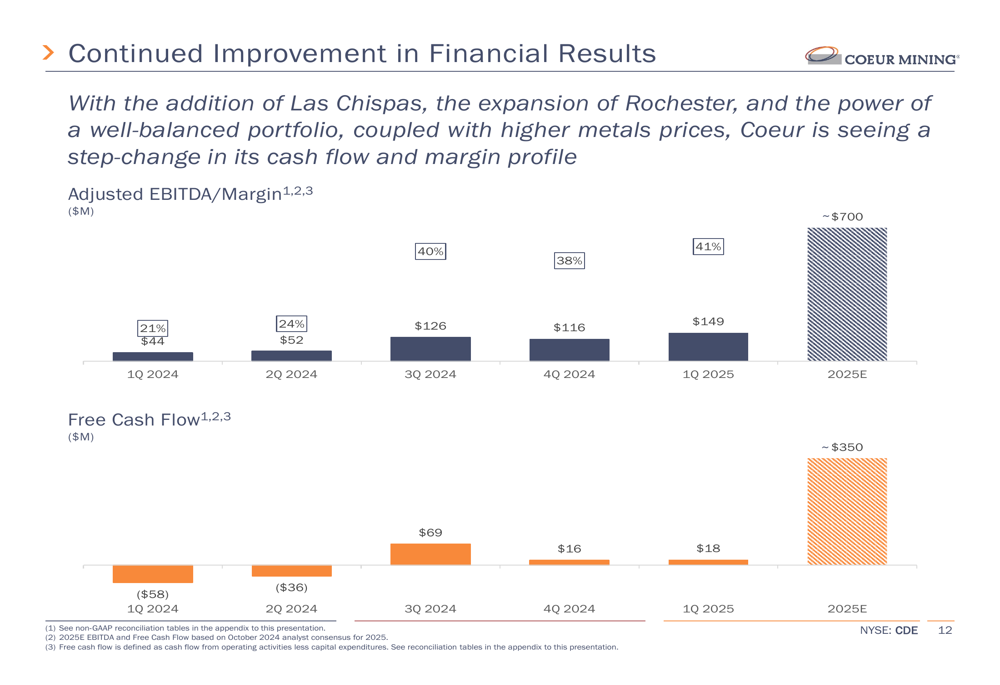

Coeur Mining, Inc. (NYSE:CDE) reported strong first quarter 2025 results on May 8, highlighting significant improvements in financial performance driven by its transformed portfolio. The company’s strategic focus on the Rochester expansion and Las Chispas integration has positioned it for record performance in 2025, with substantial increases in revenue, margins, and free cash flow generation.

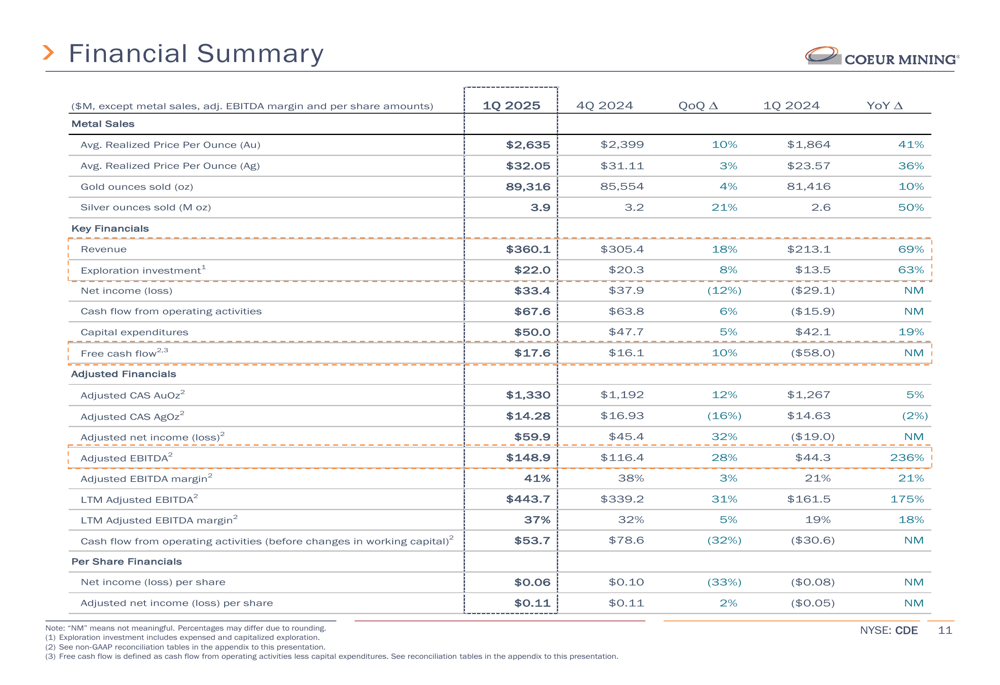

The precious metals producer benefited from robust metal prices during the quarter, with gold prices averaging $2,635 per ounce (up 41% year-over-year) and silver prices averaging $32.05 per ounce (up 36% year-over-year). This pricing environment, combined with operational improvements, helped drive a 69% year-over-year increase in revenue to $360.1 million.

Quarterly Performance Highlights

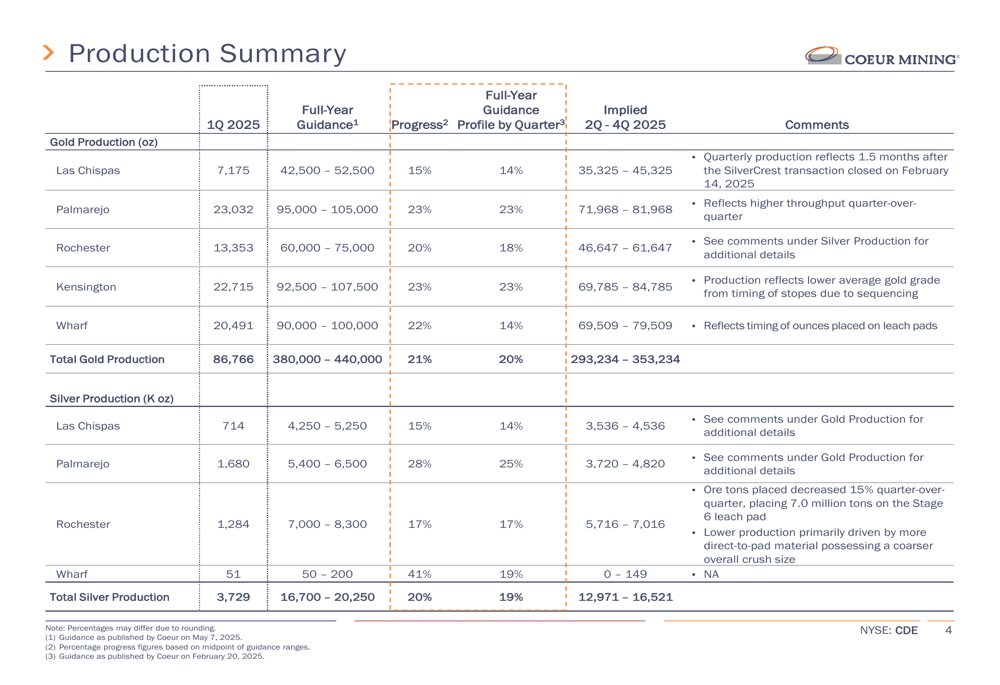

Coeur’s first quarter 2025 showed solid production across its operations, with 86,766 ounces of gold and 3.73 million ounces of silver produced. The company is on track to meet its full-year guidance ranges across all operations.

As shown in the following comprehensive production summary, the company is making steady progress toward its 2025 targets:

Financial results demonstrated significant improvement, with adjusted EBITDA of $148.9 million representing a 28% increase quarter-over-quarter and a remarkable 236% increase year-over-year. The adjusted EBITDA margin expanded to 41%, up from 38% in the previous quarter and 21% in the first quarter of 2024.

The following financial summary highlights the company’s strong performance across key metrics:

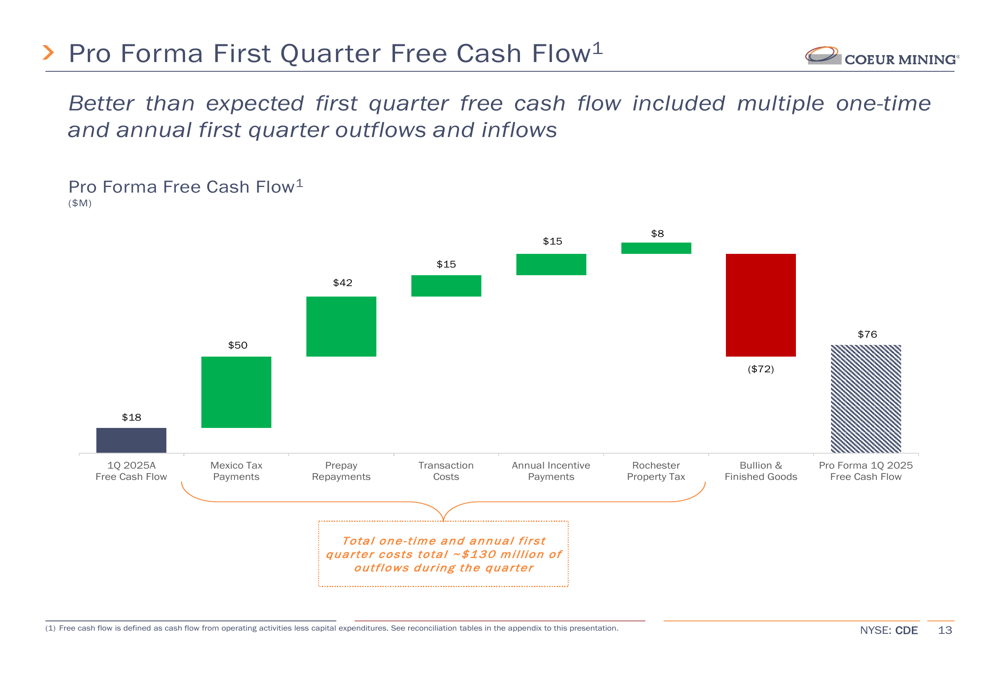

Free cash flow generation continued to improve, reaching $17.6 million for the quarter. However, this figure was impacted by several one-time and seasonal factors. On a pro forma basis, adjusting for these items, free cash flow would have been approximately $76 million.

The following chart illustrates the bridge between reported and pro forma free cash flow:

Portfolio Transformation

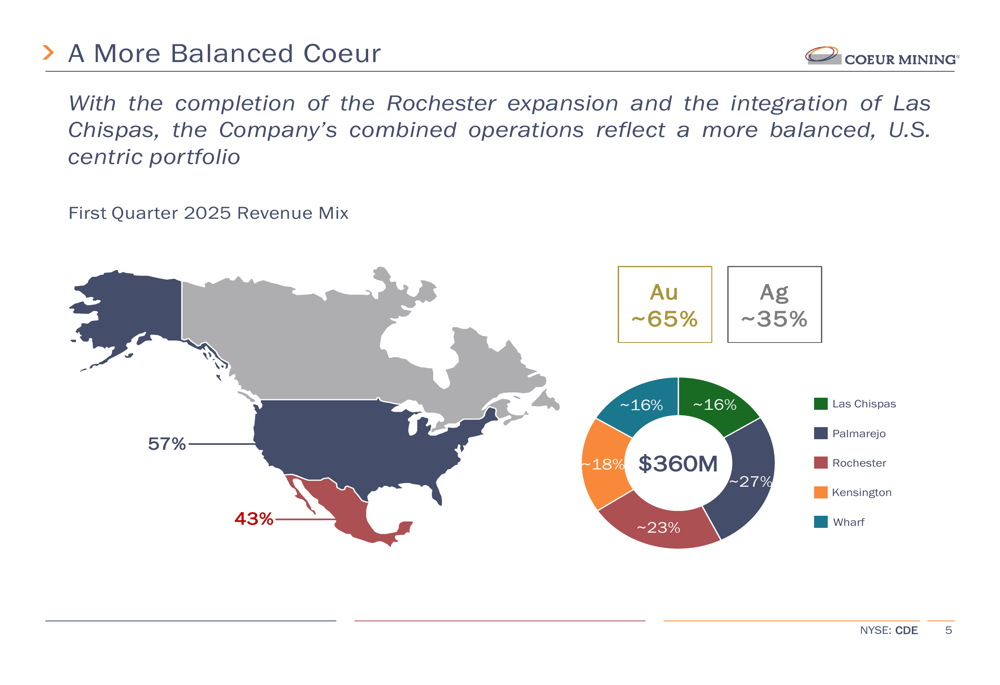

Coeur’s portfolio has undergone a significant transformation, creating a more balanced operation with improved geographic diversification and margin profile. The company now derives approximately 65% of its revenue from gold and 35% from silver, with 57% of revenue generated from U.S. operations.

The following map and revenue breakdown illustrate this balanced portfolio:

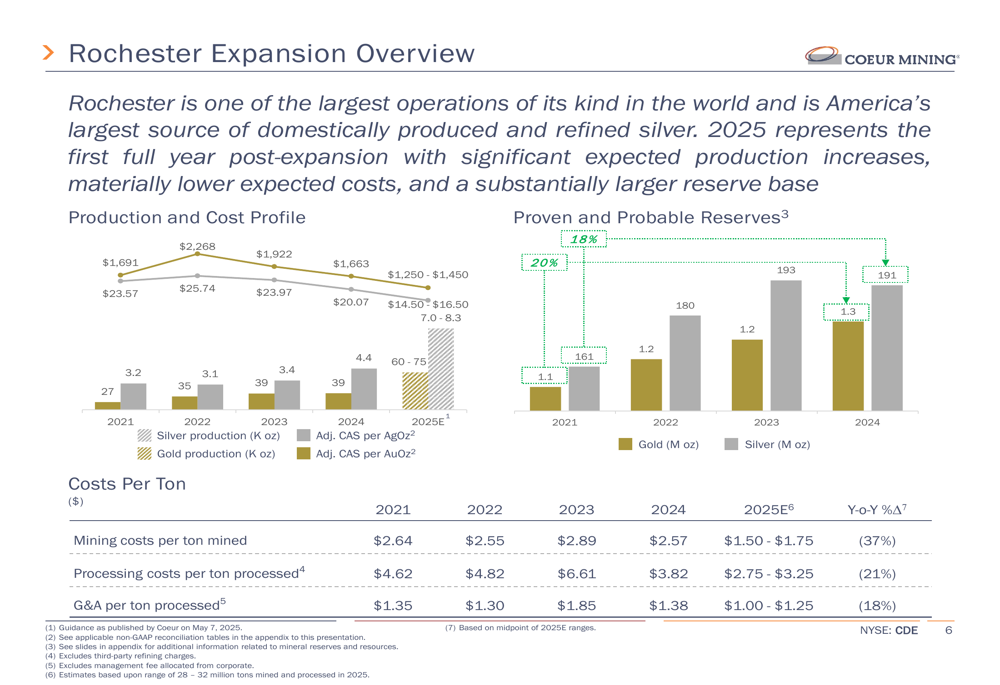

The Rochester expansion in Nevada represents a cornerstone of Coeur’s transformation. As one of the largest operations of its kind and America’s largest source of domestically produced and refined silver, Rochester is expected to deliver significantly higher production at materially lower costs in 2025, its first full year post-expansion.

The following chart details Rochester’s production and cost profile improvements:

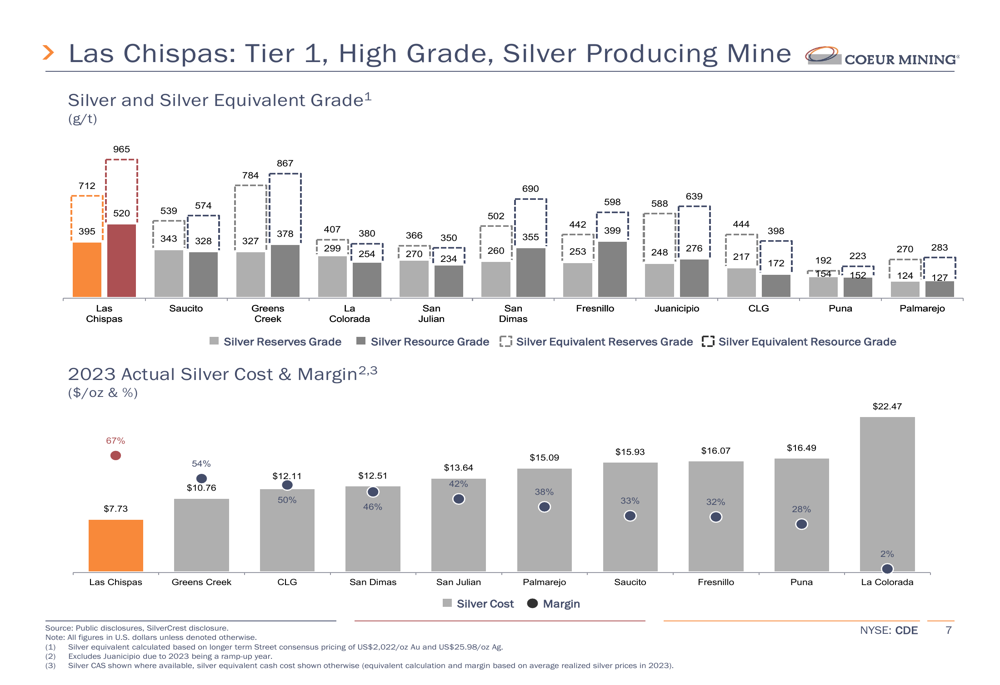

The integration of Las Chispas, acquired through the SilverCrest transaction that closed on February 14, 2025, is proceeding smoothly. This high-grade silver-gold operation in Mexico is positioned as a Tier 1 asset with industry-leading grades and margins.

As shown in the following comparison, Las Chispas boasts the highest silver equivalent grade among peers at 965 g/t and the lowest silver cost at $7.73 per ounce, resulting in a leading margin of 67%:

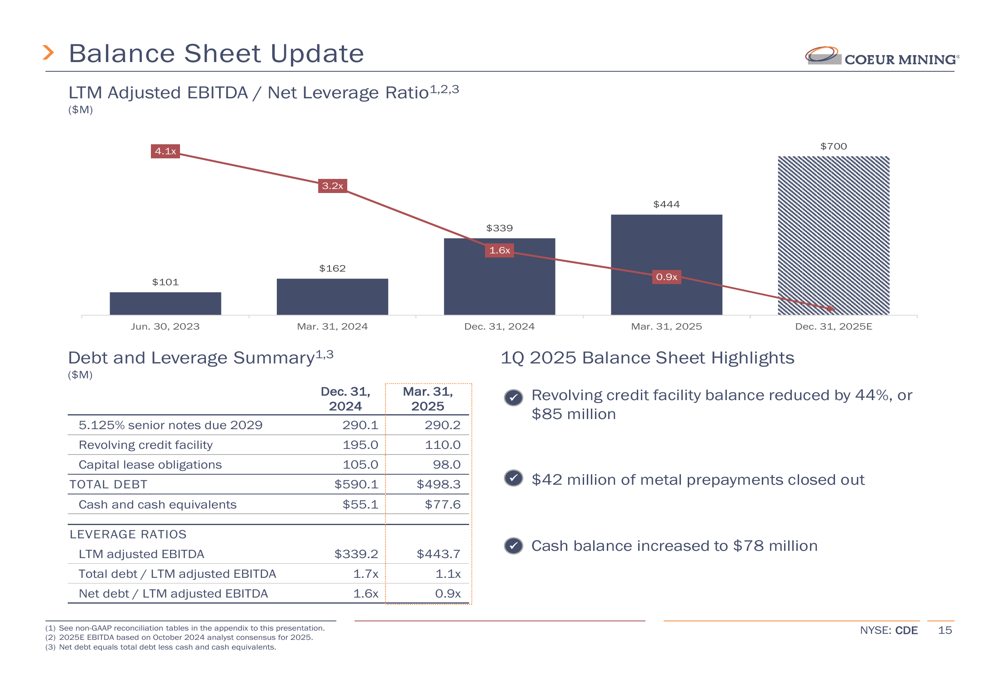

Balance Sheet Improvement

Coeur has made substantial progress in strengthening its balance sheet, reducing its revolving credit facility balance by $85 million (44%) during the quarter. The company’s net debt to LTM adjusted EBITDA ratio improved to 0.9x as of March 31, 2025, down from 1.6x at the end of 2024 and 4.1x in June 2023.

The following chart illustrates this deleveraging trend:

The company’s financial position continues to benefit from improving operational performance and higher metals prices, with LTM adjusted EBITDA reaching $443.7 million, a 31% increase from the end of 2024 and a 175% increase year-over-year.

This trend of improvement is expected to continue throughout 2025:

Strategic Initiatives

Coeur is investing in organic growth opportunities across its portfolio, with capital expenditures of $50 million in the first quarter and full-year guidance of $187-225 million. These investments are primarily focused on underground development, crusher optimization, and infrastructure improvements to support extended mine lives.

The company is also maintaining a higher level of exploration investment, with a total budget of $77-93 million for 2025, focused on resource conversion and expansion at Las Chispas, Palmarejo, and other operations.

At Las Chispas, exploration efforts have already identified a new discovery called Augusta, which is part of the Gap zone. The company’s 2025 drill plan aims to replace depletion through conversion of existing inferred resources and expansion drilling around current veins.

Forward-Looking Statements

Coeur has reaffirmed its 2025 guidance, projecting consolidated production of 380,000-440,000 ounces of gold and 16.7-20.25 million ounces of silver. The company expects adjusted EBITDA of approximately $700 million and free cash flow of approximately $350 million for the full year.

Key deliverables for 2025 include:

- Delivering strong post-expansion results at Rochester

- Successfully integrating Las Chispas

- Continuing to deleverage the balance sheet

- Investing in high-return exploration opportunities

- Accelerating investment at Silvertip

- Communicating an approach to returning capital to shareholders

Inflationary cost pressures appear to be subsiding, with decreases in diesel, materials, labor, and power costs compared to previous quarters, which should support margin expansion going forward.

The company’s transformation into a more balanced, higher-margin producer with a strengthened balance sheet positions it well to deliver on its 2025 objectives and potentially begin returning capital to shareholders as its deleveraging goals are achieved.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.