Street Calls of the Week

Introduction & Market Context

Coeur Mining (NYSE:CDE) presented its second quarter 2025 earnings results on August 7, 2025, showcasing record financial performance across multiple metrics. The precious metals producer, with operations spanning the United States and Mexico, has benefited from higher gold and silver prices, successful integration of the Las Chispas acquisition, and improved operational efficiency at its expanded Rochester mine.

The company’s stock has responded positively to these developments, with premarket trading showing a 2.73% increase to $10.16, building on yesterday’s close of $9.89. This continues the strong momentum seen after Q1 results, when the stock jumped 22.77% following better-than-expected performance.

Quarterly Performance Highlights

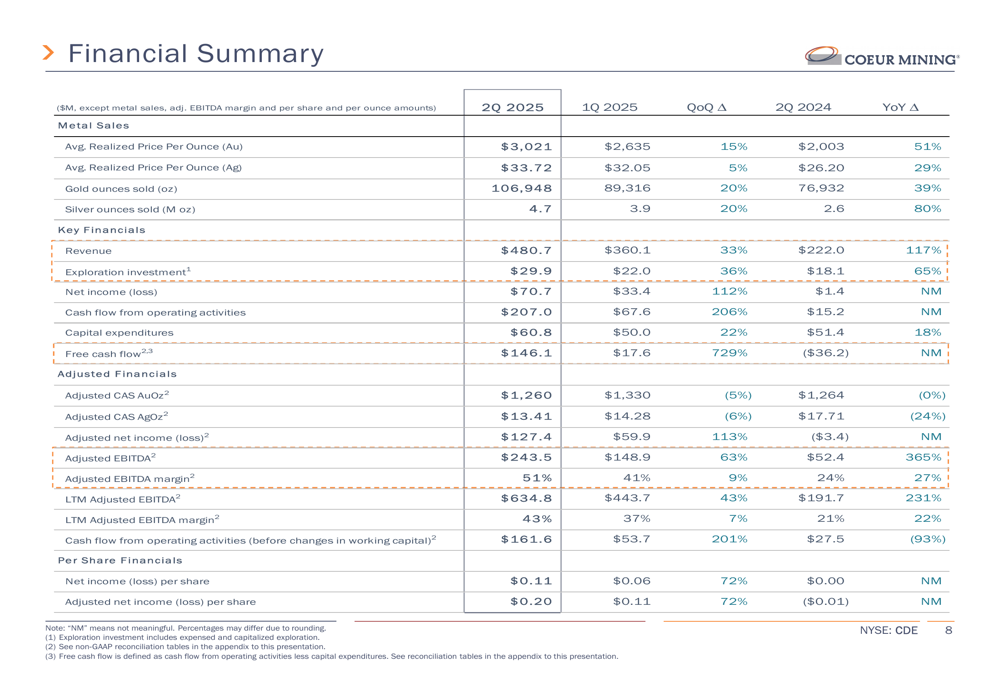

Coeur reported exceptional financial results for Q2 2025, achieving record figures for net income, free cash flow, and adjusted EBITDA. Revenue reached $480.7 million, representing a 33% increase from Q1 2025 and a remarkable 117% jump year-over-year. Net income rose to $70.7 million, more than doubling from the previous quarter’s $33.4 million and significantly higher than the $1.4 million reported in Q2 2024.

The company’s performance was driven by both higher metal prices and increased production volumes. Average realized gold prices rose to $3,021 per ounce (up 15% quarter-over-quarter and 51% year-over-year), while silver prices reached $33.72 per ounce (up 5% quarter-over-quarter and 29% year-over-year). Gold sales volume increased by 20% to 106,948 ounces, and silver sales grew by 20% to 4.7 million ounces compared to the previous quarter.

As shown in the following comprehensive financial summary, Coeur’s performance improved substantially across all key metrics:

Detailed Financial Analysis

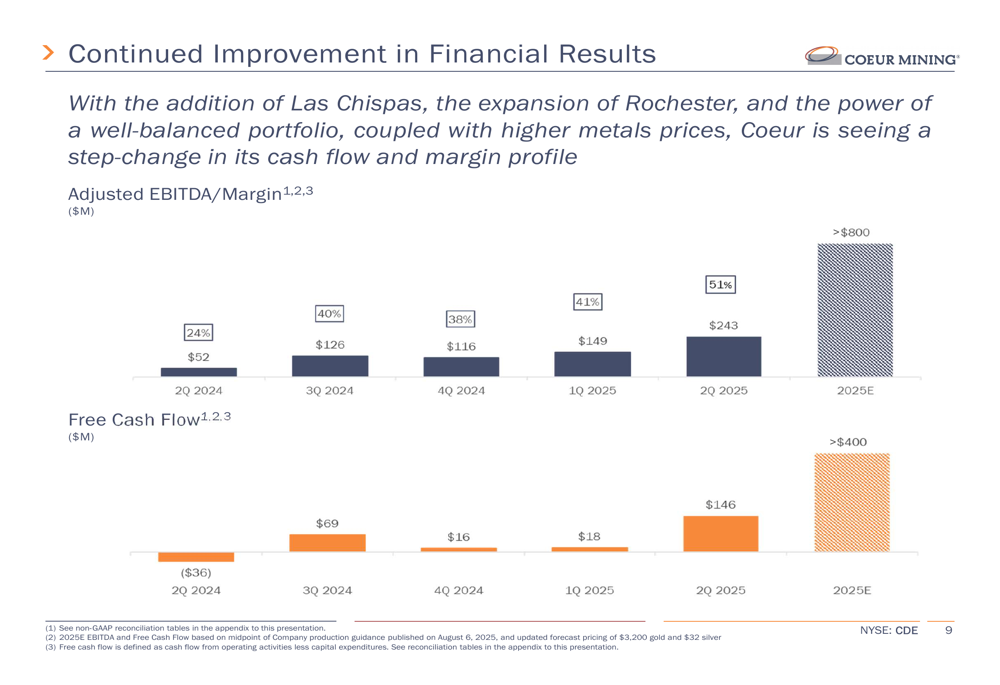

The second quarter saw Coeur’s adjusted EBITDA reach $243.5 million, a 63% increase from Q1 2025 and a 365% jump from Q2 2024. The adjusted EBITDA margin expanded to 51%, up from 41% in the previous quarter and 24% in the same period last year. This margin expansion reflects both higher metal prices and operational improvements, particularly at the Rochester mine where crushed ore tons increased 24% versus the prior quarter.

Free cash flow showed the most dramatic improvement, surging to $146.1 million—a 729% increase from Q1 2025 and a remarkable turnaround from negative $36.2 million in Q2 2024. This strong cash generation has enabled the company to strengthen its balance sheet and initiate share repurchases.

The following chart illustrates the company’s consistent financial improvement over recent quarters and its upgraded full-year outlook:

Coeur now projects full-year 2025 adjusted EBITDA to exceed $800 million and free cash flow to surpass $400 million, representing upgrades from the previous guidance of over $700 million and $300 million respectively, provided during the Q1 earnings call.

Balance Sheet Strengthening

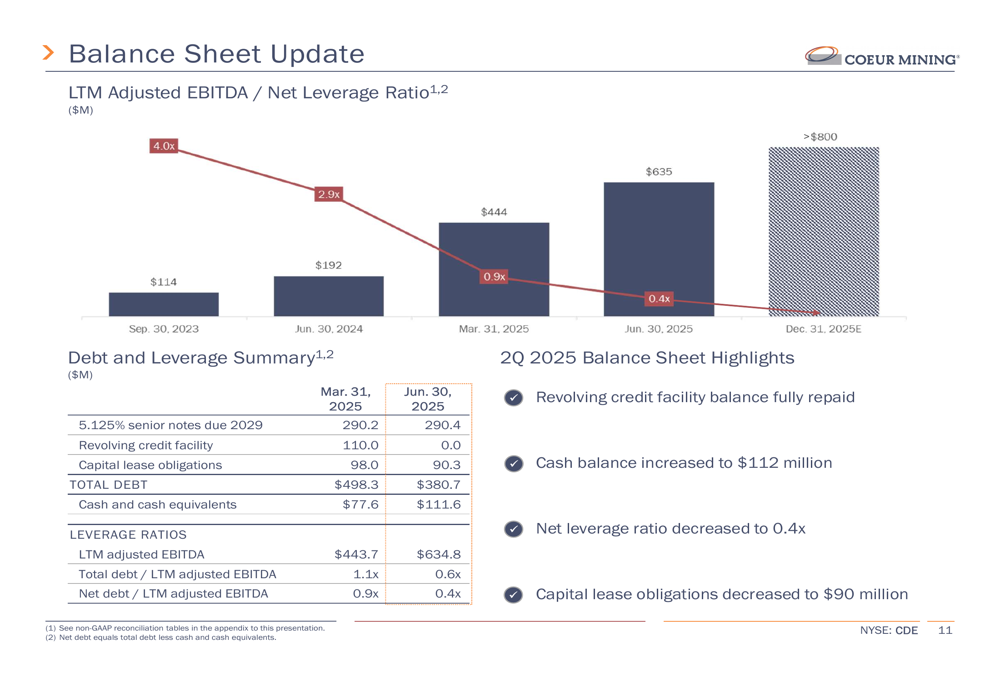

A key highlight of the quarter was Coeur’s significant deleveraging, with the company fully repaying its revolving credit facility balance. The net leverage ratio decreased to 0.4x, down from 0.9x at the end of Q1 2025 and dramatically lower than the 4.0x reported in September 2023. Cash balance increased to $111.6 million, up from $77.6 million at the end of the previous quarter.

The company’s debt reduction progress and leverage trends are illustrated in the following chart:

This strengthened financial position has allowed Coeur to initiate share repurchases under its previously announced $75 million program, signaling management’s confidence in the company’s future prospects.

Operational Improvements

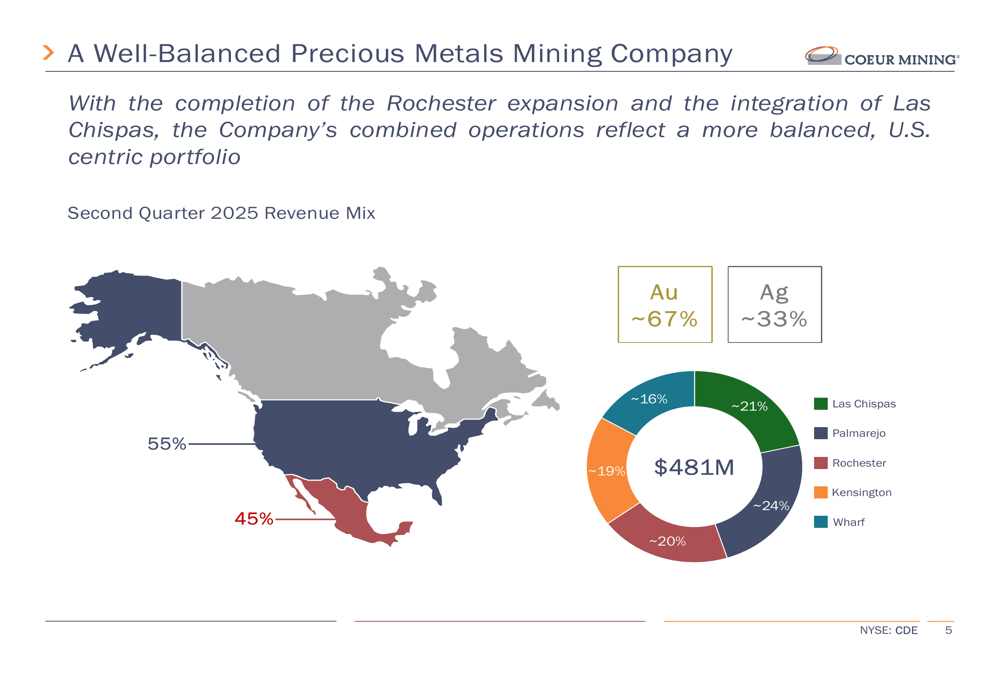

Coeur’s operational portfolio has become more balanced following the Las Chispas acquisition (completed on February 14, 2025) and the Rochester expansion. No single operation now accounts for more than 25% of total revenue, with Rochester contributing 24%, Palmarejo 21%, Kensington 20%, Wharf 19%, and Las Chispas 16%. The revenue mix is approximately 67% gold and 33% silver, with operations split between the USA (55%) and Mexico (45%).

The following map and chart illustrate this well-balanced portfolio:

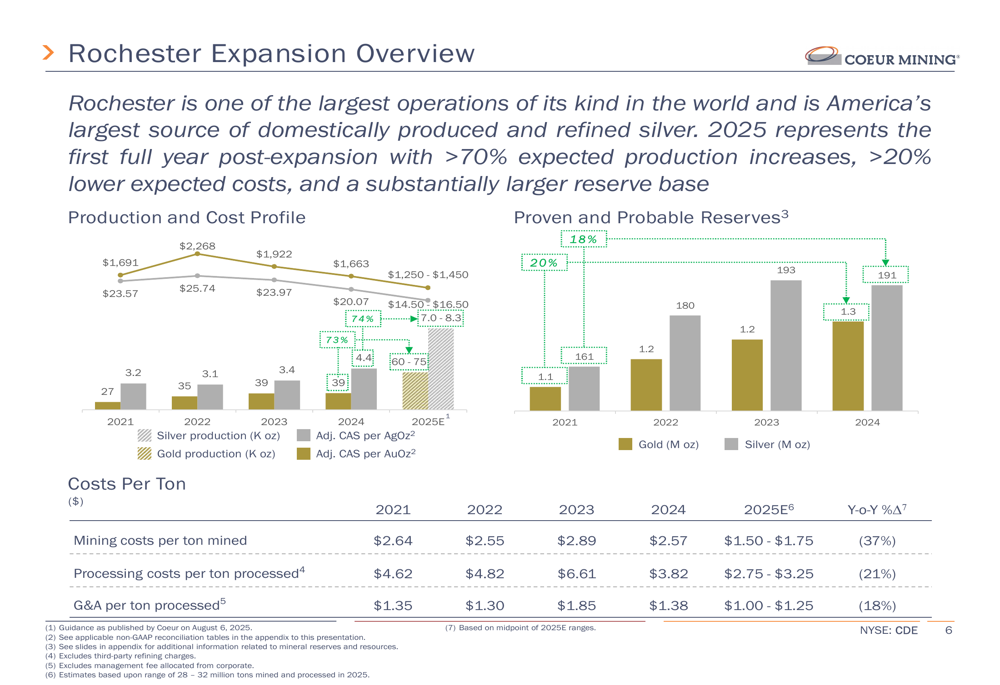

The Rochester expansion, highlighted as America’s largest source of domestically produced and refined silver, is showing promising results with expectations for over 70% production increases and more than 20% lower costs. The following chart shows the production and cost profile improvements:

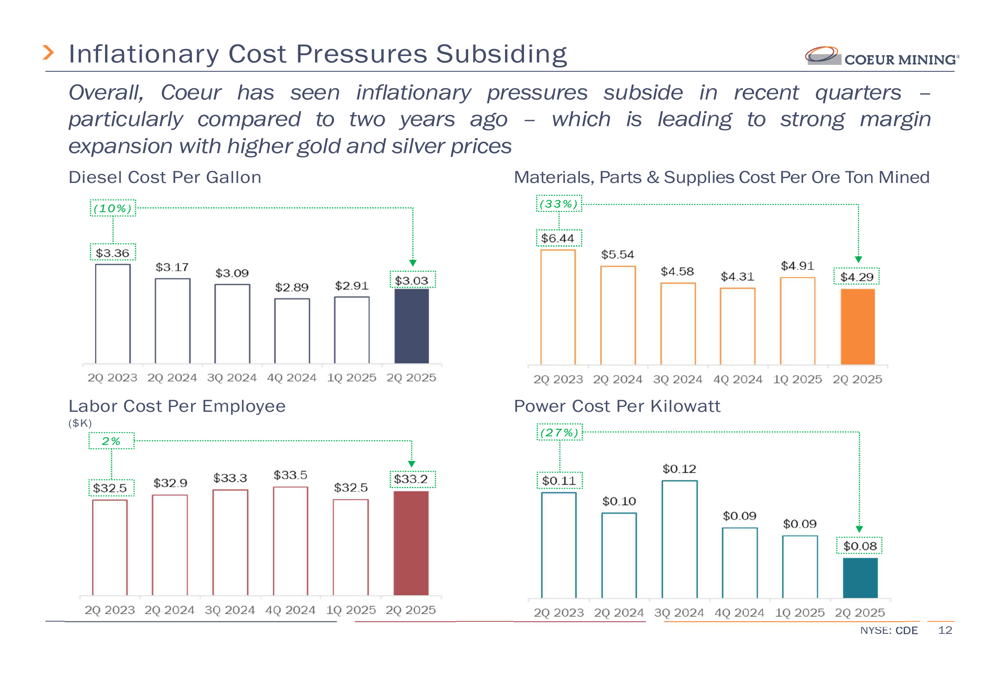

Another positive development is the subsiding of inflationary cost pressures across various operational inputs. As shown in the following charts, costs for diesel, materials, and power have all decreased compared to 2023 levels:

Forward-Looking Statements

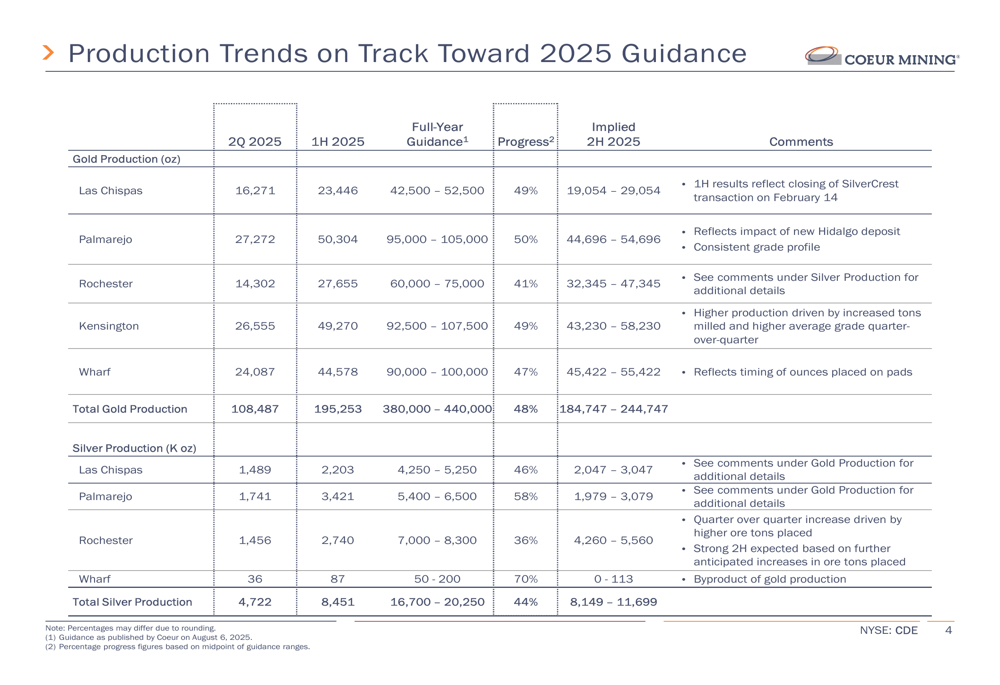

Coeur has reaffirmed its full-year production and cost guidance, maintaining confidence in its operational outlook despite the strong first-half performance. The company’s production is on track toward 2025 targets, with first-half gold production at 195,253 ounces (48% of full-year guidance) and silver production at 8.45 million ounces (44% of full-year guidance).

The detailed production trends and guidance are shown in the following table:

For the second half of 2025, Coeur outlined several key deliverables, including continuing to increase crushing rates at Rochester, maintaining strong performance at Las Chispas, further strengthening the balance sheet, delivering results from exploration investments, advancing the Silvertip exploration program, and continuing share repurchases.

The company is also sustaining a higher level of exploration investment, with $100 million allocated for 2025 compared to $84 million in 2024. This investment is focused on high-return opportunities at Palmarejo, Las Chispas, and Silvertip, aimed at extending mine life and discovering new resources.

With its strengthened balance sheet, well-balanced portfolio, and operational improvements, Coeur appears well-positioned to capitalize on favorable precious metals prices and deliver strong results through the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.