Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

Cogent Communications Holdings Inc (NASDAQ:CCOI) recently presented its Q1 2025 investor slides, revealing a company in transition following its significant Sprint Wireline acquisition. The global network provider, which carries approximately 25% of all internet traffic, reported mixed results that led to a notable stock decline of 7.35% on May 8, with shares closing at $49.30.

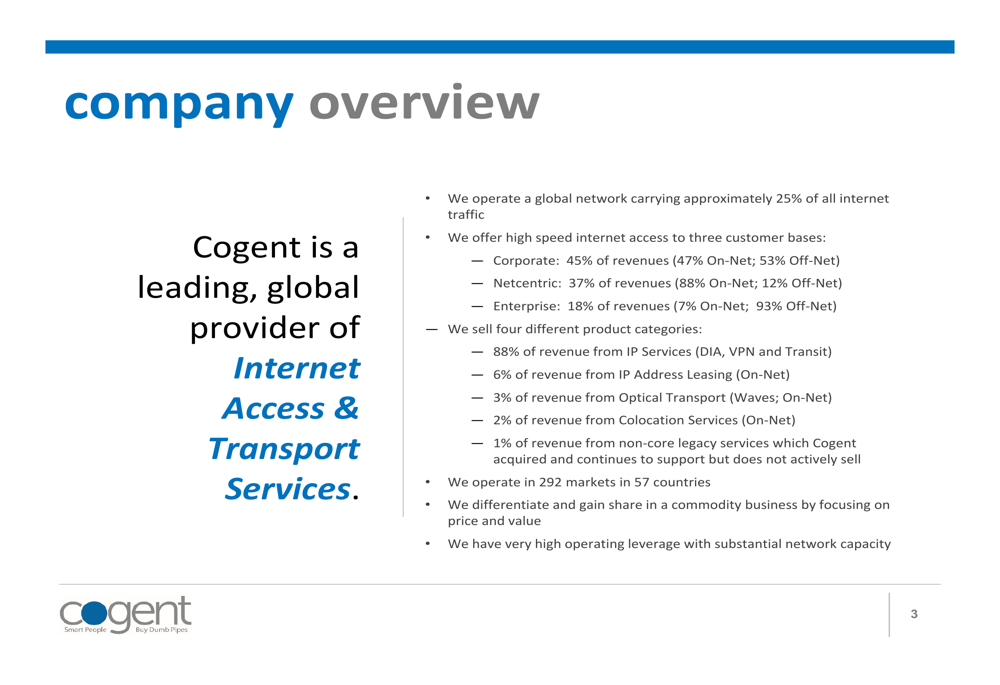

The company operates across 292 markets in 57 countries, positioning itself as a low-cost provider of internet access and transport services. Cogent’s business spans three customer segments: Corporate (45% of revenue), Netcentric (37%), and Enterprise (18%), with a product mix heavily weighted toward IP Services (88%).

As shown in the following company overview slide, Cogent differentiates itself through price and value, leveraging high operating leverage from its substantial network capacity:

Quarterly Performance Highlights

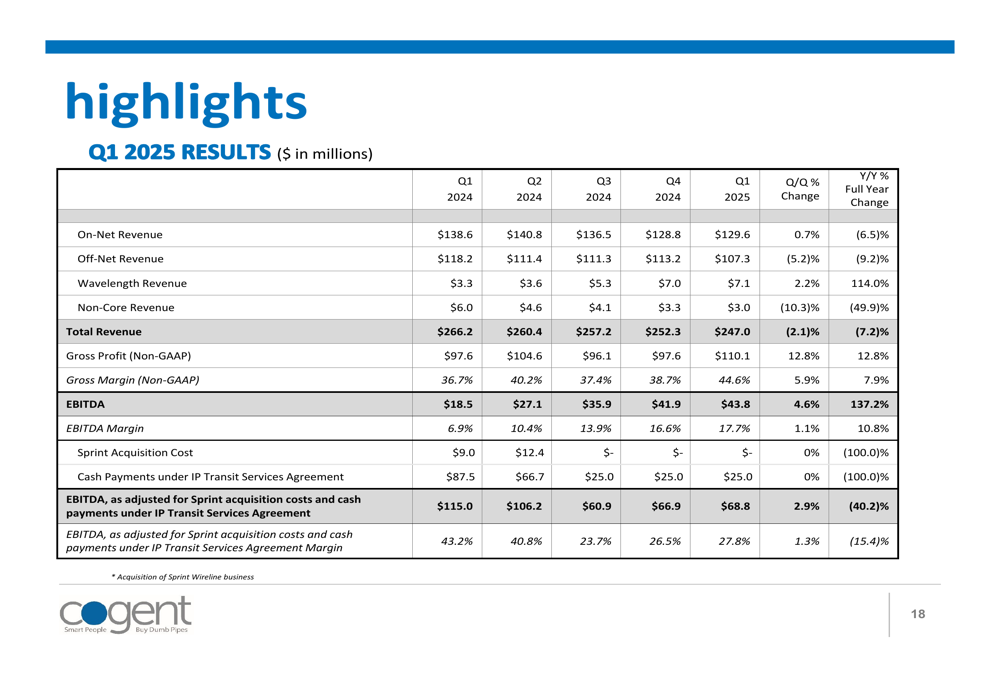

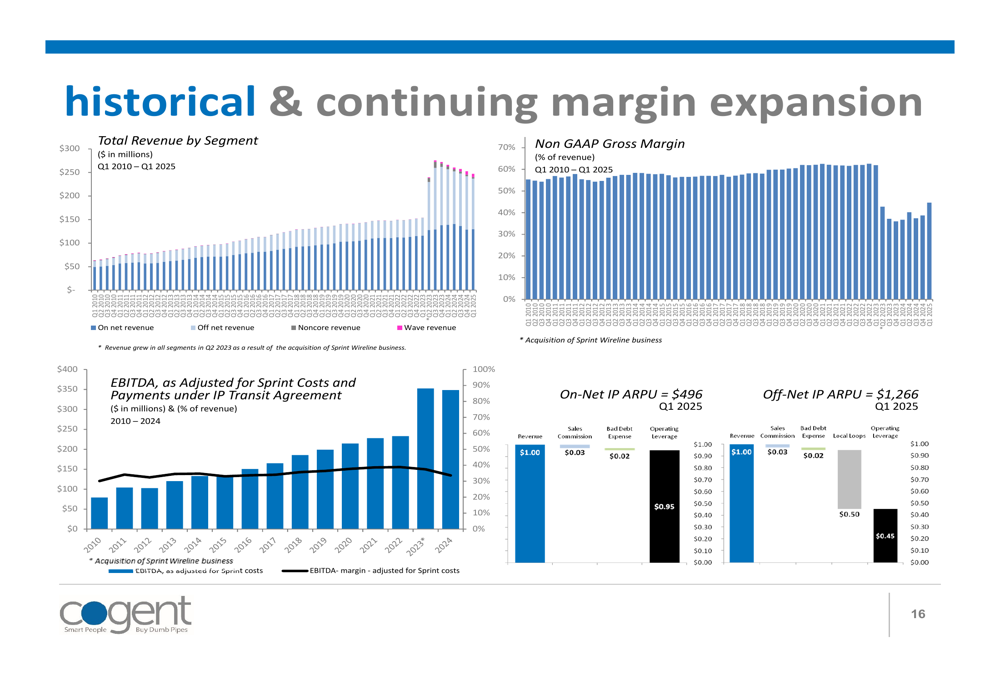

Cogent’s Q1 2025 results fell short of analyst expectations, with total revenue of $247.0 million representing a 7.2% year-over-year decline. Despite this revenue drop, the company showed significant improvement in profitability metrics, with non-GAAP gross profit increasing 12.8% year-over-year to $110.1 million and gross margin expanding to 44.6%.

EBITDA showed dramatic improvement, rising 137.2% year-over-year to $43.8 million, though EBITDA adjusted for Sprint acquisition costs and payments under the IP Transit Services Agreement declined 40.2% to $68.8 million.

The following slide summarizes these key financial metrics:

CEO Dave Schaeffer expressed optimism about future growth during the earnings call, stating, "We expect to return to total top line revenue growth by mid-Q3 2025." This projection aligns with the company’s long-term annual revenue growth target of 6-8% and its aim for EBITDA margin expansion of 50 basis points annually.

Detailed Financial Analysis

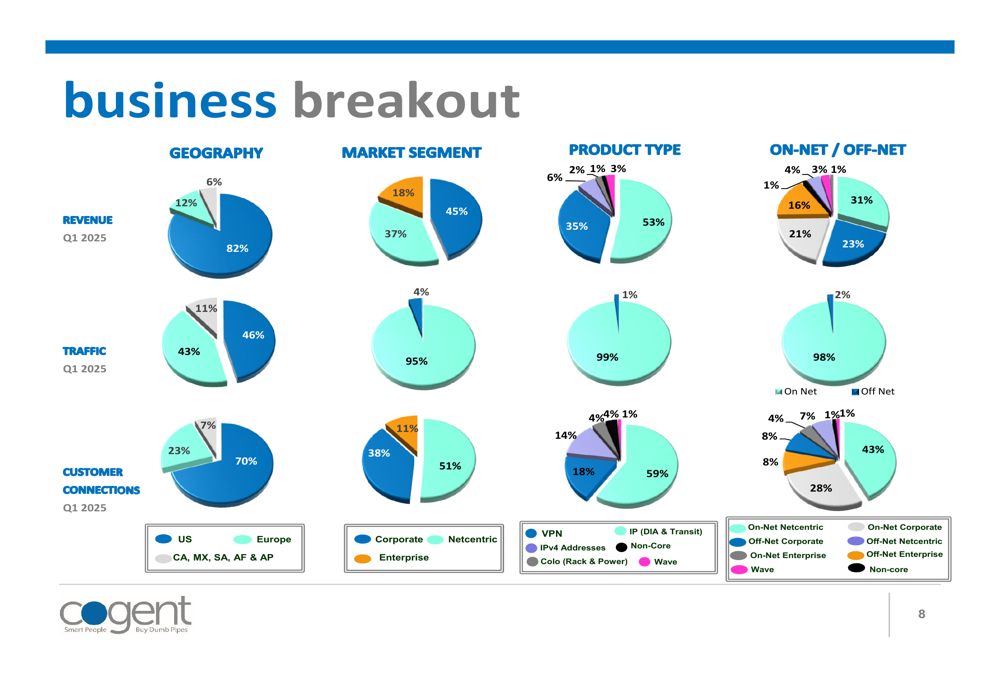

Cogent’s revenue streams are diversified across geographies and service types. The company generates 82% of its revenue from the US, with the remaining 18% coming from international markets. From a product perspective, IP services dominate the mix at 88%, followed by IP address leasing (6%), optical transport (3%), and colocation services (2%).

The following business breakout slide illustrates this diversification:

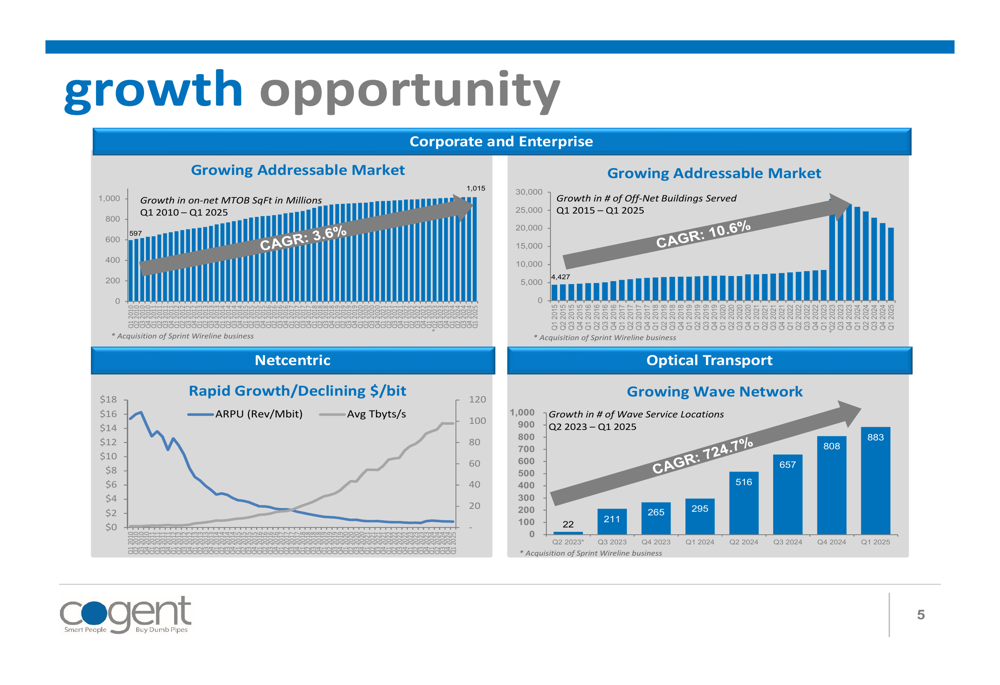

A bright spot in Cogent’s portfolio is its wavelength services, which saw 14% year-over-year revenue growth according to the earnings call. The company’s presentation highlights the rapid expansion of this network, with growth in wave service locations projected to increase from 22 in Q2 2023 to 883 in Q1 2025, representing a remarkable 724.7% CAGR.

The growth opportunity across Cogent’s business segments is illustrated in the following slide:

Margin expansion remains a key focus for Cogent despite revenue challenges. The company has demonstrated a consistent pattern of improving margins over time, as shown in the historical margin expansion slide:

Strategic Initiatives

Cogent’s acquisition of Sprint’s wireline business in May 2023 represents a transformative move for the company. The $20.5 billion original investment (based on asset value) brought significant technical infrastructure to Cogent, including 1.9 million square feet of technical space, 482 buildings, approximately 9.9 million IPv4 addresses, and over 20,000 owned route miles of fiber. The company recorded a bargain purchase gain of $1.4 billion, or $29.69 per share, from this acquisition.

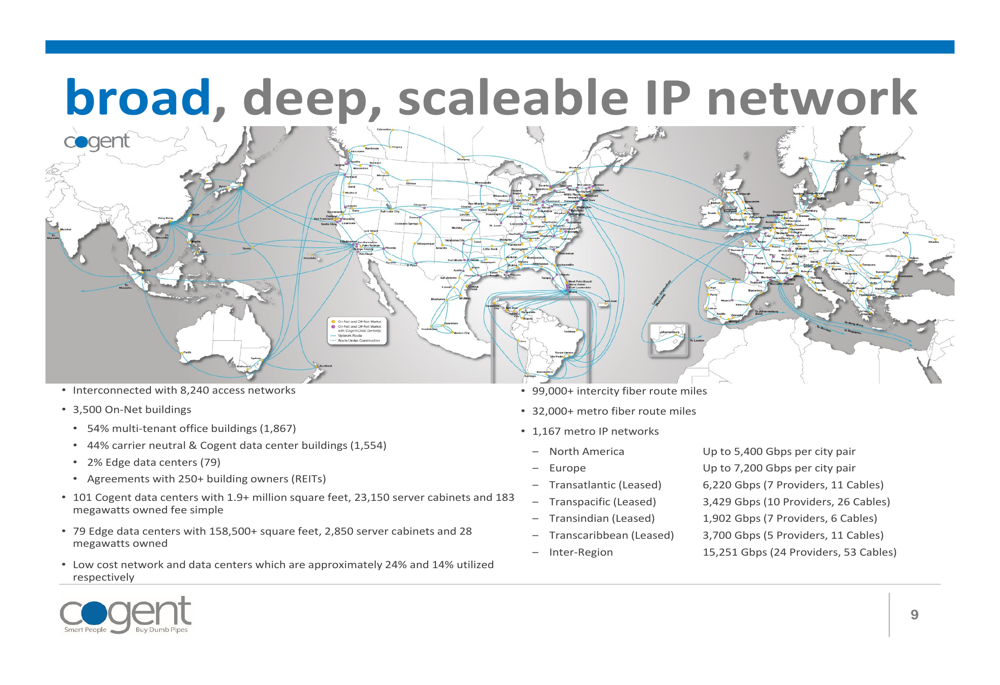

The company’s global network infrastructure provides a competitive advantage, as illustrated in this network map:

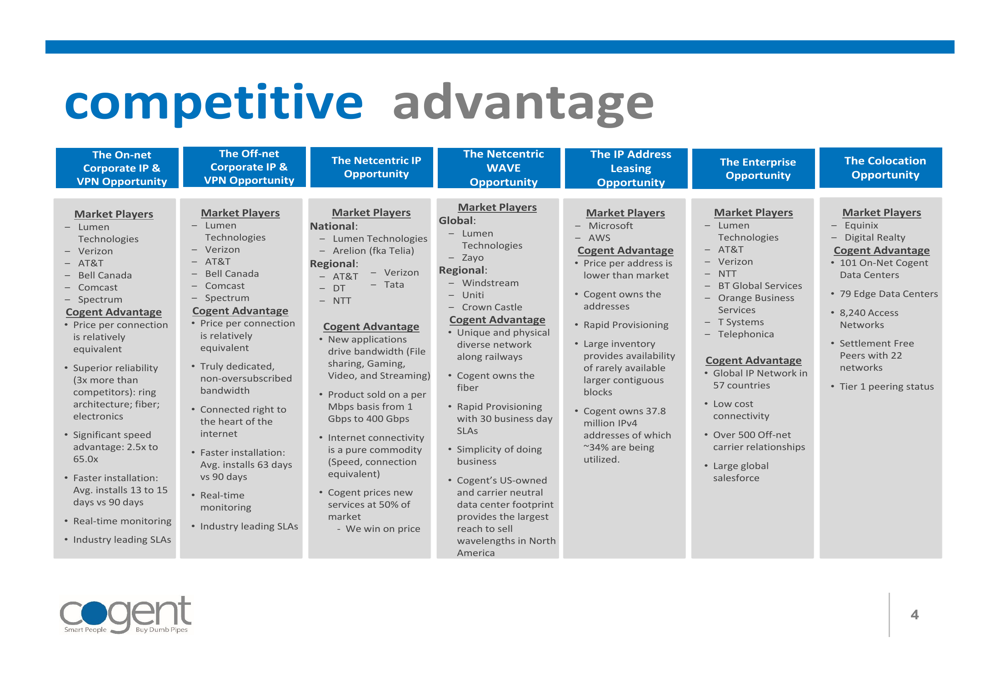

Cogent’s competitive positioning is built on several key advantages across different market segments, including price competitiveness, superior reliability, speed advantages (2.5x to 65.0x faster than competitors), and faster installation times (13-15 days versus 90 days for competitors). The company’s wavelength services network is particularly strategic, offering unique routes, ubiquitous locations, fast provisioning, and low cost.

The following slide details these competitive advantages:

Another key strategic asset is Cogent’s expanded inventory of 37.9 million IPv4 addresses, which provides a valuable revenue stream through IP address leasing as these addresses become increasingly scarce.

Forward-Looking Statements

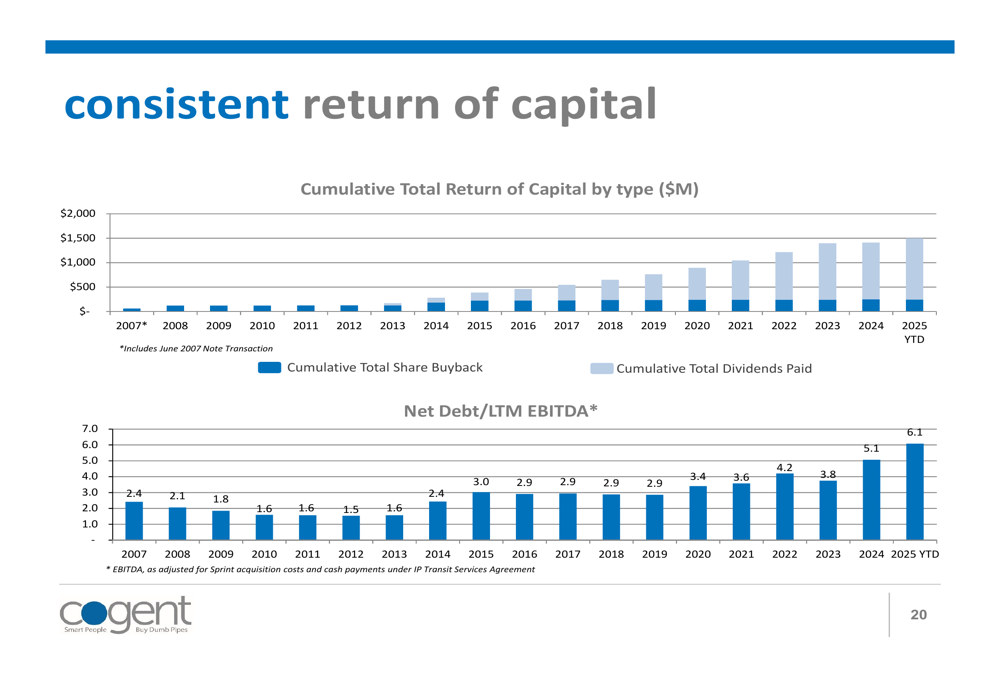

Despite current revenue challenges, Cogent maintains a consistent focus on returning capital to shareholders. The company has increased its dividend for 51 consecutive quarters and has returned a total of $1.6 billion to shareholders since its 2005 public offering.

The following slide illustrates this consistent return of capital:

Looking ahead, Cogent expects its corporate revenues to grow by 4-5% and its NetCentric segment to see over 10% growth. The company anticipates returning to total revenue growth by mid-Q3 2025, driven by continued expansion of its wavelength services and stabilization of its core IP business.

Potential risks to this outlook include slowing internet traffic growth (now at 8%), the historical trend of declining pricing by 22-23% annually, and seasonal increases in SG&A expenses. Additionally, the company mentioned during its earnings call that it is negotiating potential data center sales, which could impact future revenue streams.

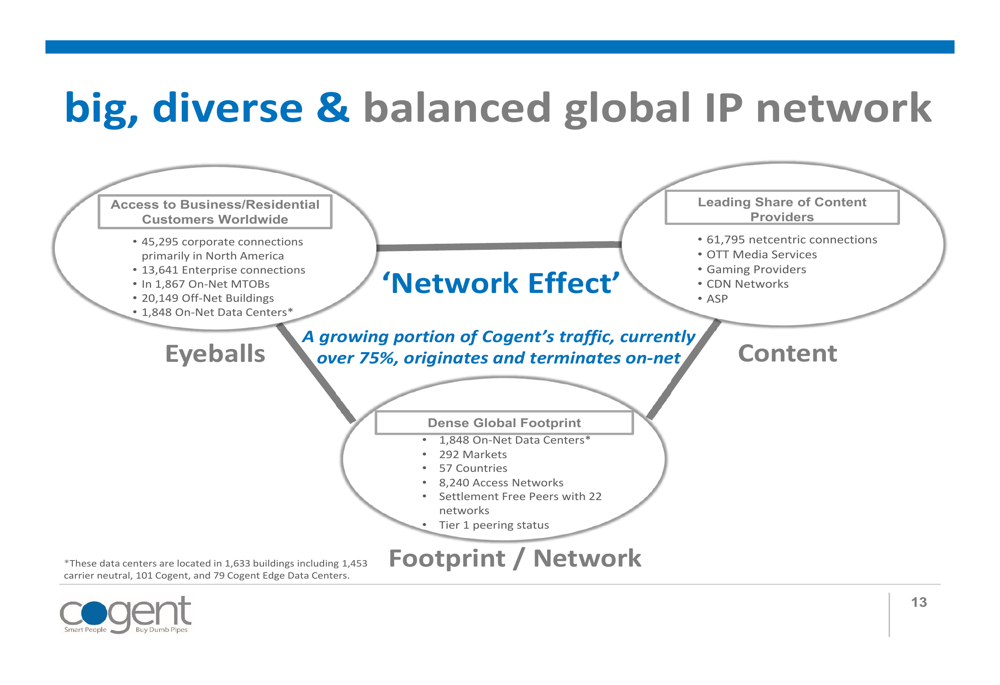

Cogent’s balanced global IP network provides a foundation for future growth, as illustrated in this comprehensive network overview:

With its disciplined capital allocation strategy, extensive network infrastructure, and focus on high-growth segments like wavelength services, Cogent is positioning itself to overcome current revenue challenges and return to growth in the coming quarters, while maintaining its commitment to shareholder returns through consistent dividend increases.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.