S&P 500 slips, but losses kept in check as Nvidia climbs ahead of results

Colabor Group Inc . (TSX:GCL) shares tumbled 13.68% following its Q2 2025 earnings presentation on July 25, as investors reacted to a significant profit decline despite revenue growth. The Quebec-based foodservice distributor reported mixed results, with acquisition-driven sales increases overshadowed by margin compression and rising debt levels.

Quarterly Performance Highlights

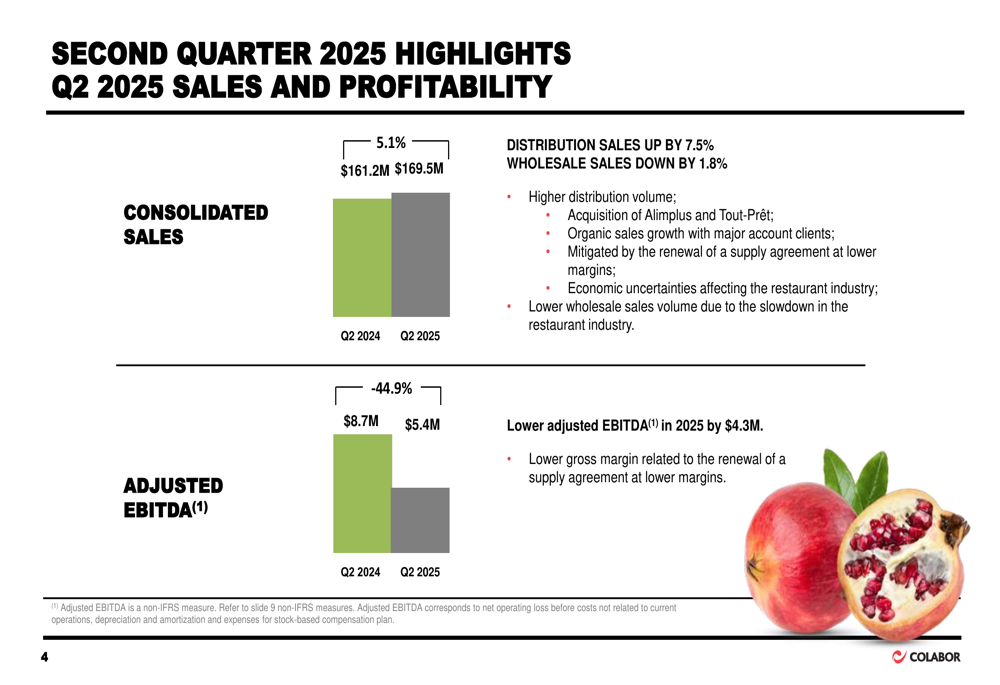

Colabor reported consolidated sales of $169.5 million for Q2 2025, representing a 5.1% increase from $161.2 million in the same quarter last year. This growth was primarily driven by a 7.5% increase in distribution sales, attributed to the company’s recent acquisitions of Alimplus and Tout-Prêt, along with organic growth from major account clients.

However, the company’s wholesale segment saw a 1.8% decline in sales, which management attributed to a broader slowdown in the restaurant industry amid economic uncertainties.

As shown in the following chart of quarterly sales and profitability metrics:

Despite the revenue growth, Colabor’s profitability metrics deteriorated significantly. Adjusted EBITDA fell 44.9% to $5.4 million from $8.7 million in Q2 2024, while adjusted EBITDA margin contracted to 3.2% from 6.0% a year earlier. The company cited lower gross margins related to the renewal of a supply agreement at reduced rates as a key factor in the profit decline.

Detailed Financial Analysis

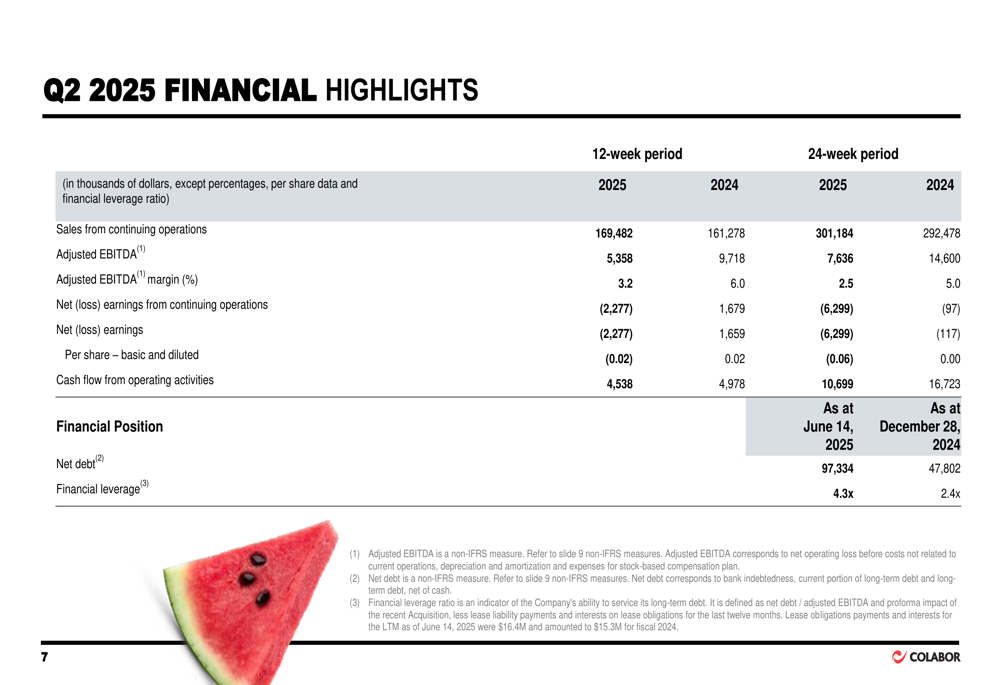

The company reported a net loss of $2.3 million (-$0.02 per share) for Q2 2025, compared to net earnings of $1.7 million ($0.02 per share) in the prior-year quarter. This decline was attributed to decreased adjusted EBITDA, increased amortization expenses, and higher costs not related to current operations, partially offset by income tax recovery.

Cash flow from operations decreased to $4.5 million from $5.0 million in Q2 2024, reflecting the lower adjusted EBITDA, though this was partially offset by more efficient working capital management.

The comprehensive financial summary table below highlights the company’s performance across key metrics:

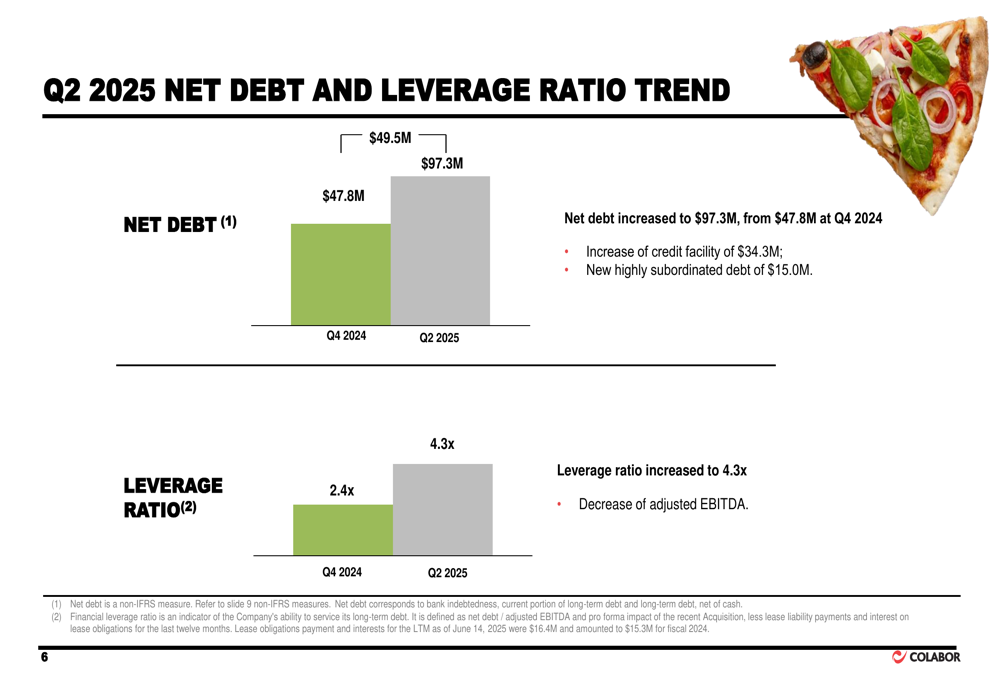

Of particular concern to investors is Colabor’s significantly increased debt load. Net debt more than doubled from $47.8 million at the end of Q4 2024 to $97.3 million, driven by a $34.3 million increase in credit facility usage and $15.0 million in new highly subordinated debt. Consequently, the company’s leverage ratio jumped from 2.4x to 4.3x adjusted EBITDA.

The following chart illustrates this concerning trend in debt and leverage:

Strategic Initiatives

Colabor’s most significant strategic move during the quarter was the completion of the Alimplus acquisition for $49.75 million. Management described this as a transformative transaction that accelerates the company’s growth strategy and strengthens its position in the Quebec foodservice distribution market.

"The closing of the Alimplus acquisition represents a strategic milestone in accelerating our growth and solidifying our position in the Quebec foodservice market," stated Louis Frenette, President and CEO, in the presentation materials.

The company also announced the appointment of Yanick Blanchard as interim SVP and CFO during the quarter, and disclosed a cybersecurity incident that occurred after the quarter’s end, though details on potential impacts were not provided.

Market Context and Forward Outlook

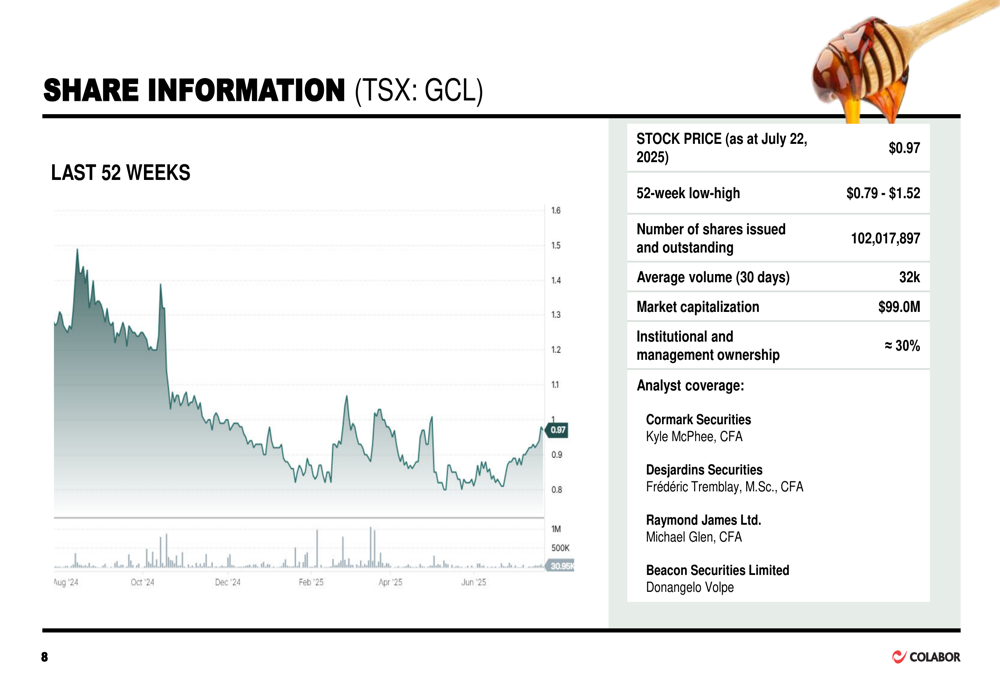

Colabor’s Q2 results continue a concerning trend that began in Q1 2025, when the company reported an EPS miss of -$0.04 versus expectations of -$0.01, along with revenue that fell short of forecasts. The consecutive quarterly disappointments have put significant pressure on the stock, which has declined substantially from its 52-week high of $1.52.

As of the presentation date (July 22, 2025), Colabor’s stock was trading at $0.97, with a market capitalization of approximately $99 million. Following the earnings release, the stock dropped further to $0.82, reflecting investor concerns about the company’s profitability and increased leverage.

The stock information chart below shows the trading range and key metrics:

Looking ahead, Colabor faces several challenges, including margin pressure from contract repricing, economic headwinds affecting the restaurant industry, and the need to successfully integrate the Alimplus acquisition while managing its substantially higher debt load. The company’s ability to reverse the negative profitability trend while maintaining revenue growth will be crucial for restoring investor confidence in the coming quarters.

While management continues to emphasize growth and market share gains, the financial results suggest that these achievements are coming at a significant cost to profitability and balance sheet strength, raising questions about the sustainability of the company’s current strategy.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.