Bullish indicating open at $55-$60, IPO prices at $37

Introduction & Market Context

Collegium Pharmaceutical Inc (NASDAQ:COLL) reported strong first-quarter results on May 8, 2025, with product revenues reaching $177.8 million, a 23% increase year-over-year. The company’s stock closed at $27.05 and remained flat in aftermarket trading, as investors digested the company’s performance and reaffirmed guidance for the year.

The biopharmaceutical company, which focuses on responsible pain management and ADHD treatment, has been recognized as a top workplace by multiple organizations, including Forbes and USA Today, strengthening its corporate reputation as it pursues its mission of "Healthier people. Stronger communities."

As shown in the following slide highlighting the company’s mission and recognitions:

Quarterly Performance Highlights

Collegium’s Q1 2025 results demonstrated solid growth across its portfolio, with particularly strong performance from its ADHD medication Jornay PM. The company achieved record product revenues while generating substantial cash flow from operations.

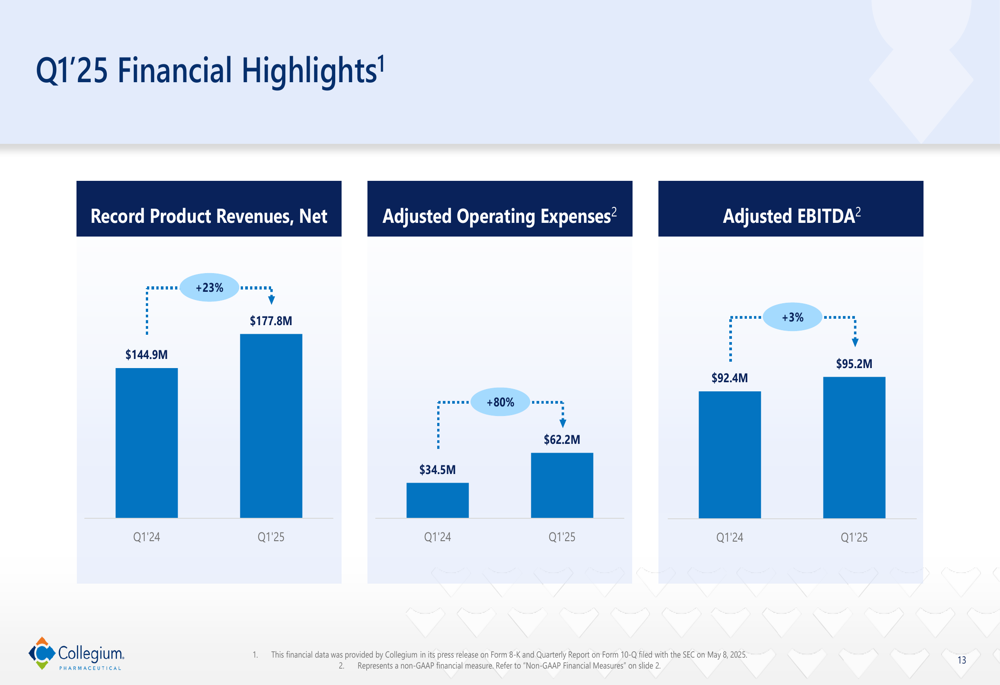

Key highlights from the quarter include product revenues of $177.8 million, up 23% from $144.9 million in Q1 2024. The company generated $55.4 million in cash from operations and ended the quarter with $197.8 million in cash, cash equivalents, and marketable securities, representing a $35 million increase from December 2024.

The following slide summarizes the company’s recent business highlights:

Adjusted EBITDA increased 3% year-over-year to $95.2 million, while adjusted operating expenses rose significantly to $62.2 million, an 80% increase from Q1 2024, reflecting investments in the company’s sales force and marketing initiatives.

The financial performance is illustrated in the following chart:

Jornay PM Growth Strategy

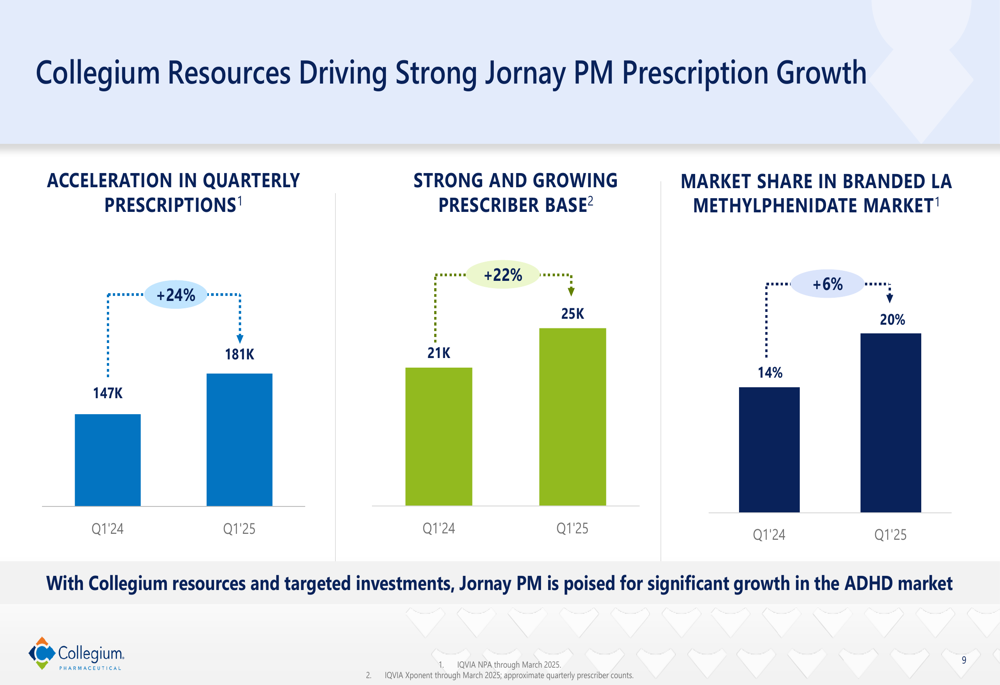

Jornay PM, Collegium’s ADHD medication, has emerged as a key growth driver for the company. Prescriptions for Jornay PM reached 181,000 in Q1 2025, representing a 24% increase from the same period last year. The prescriber base also expanded significantly, growing 22% year-over-year to approximately 25,000 prescribers.

The medication has gained market share in the branded long-acting methylphenidate market, reaching 20% in Q1 2025, up from 14% in Q1 2024. This growth is illustrated in the following charts:

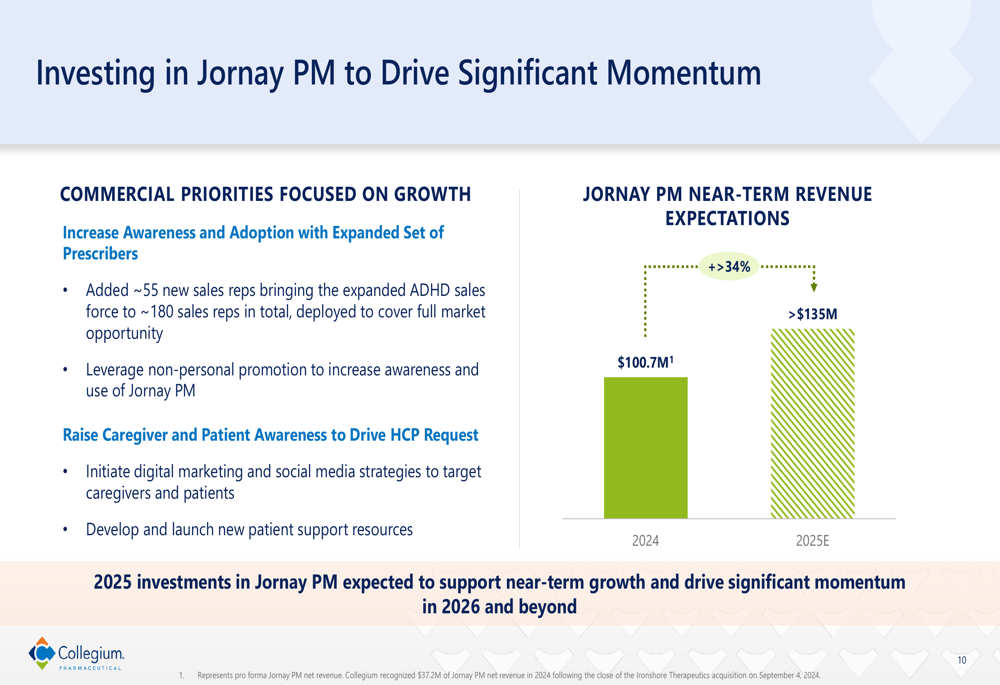

Collegium is making substantial investments to accelerate Jornay PM’s growth trajectory. The company has expanded its ADHD sales force by adding approximately 55 new sales representatives, bringing the total to around 180 representatives. Management expects Jornay PM to generate more than $135 million in revenue in 2025, representing over 34% growth from $100.7 million in 2024.

The company’s investment strategy and revenue projections for Jornay PM are outlined in the following slide:

Healthcare professionals recognize Jornay PM as the #1 branded ADHD medication for achieving all-day symptom control with one dose and for controlling after-school/work and evening symptoms, positioning the product well for continued growth.

Pain Portfolio Performance

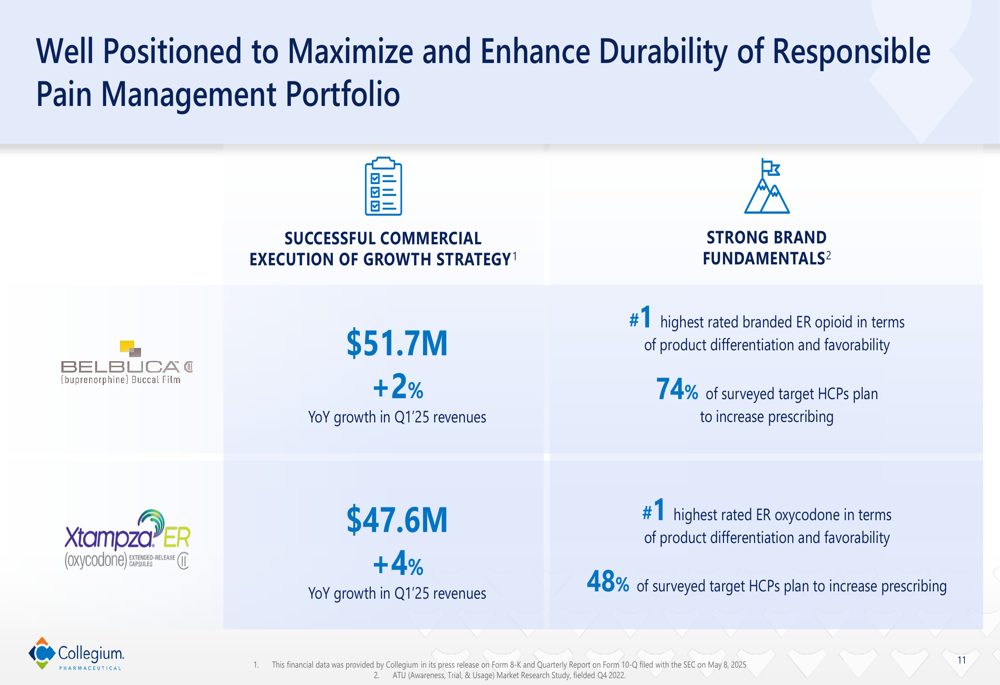

While Jornay PM has been the growth catalyst, Collegium’s pain management portfolio continues to deliver steady results. Belbuca sales reached $51.7 million in Q1 2025, a 2% year-over-year increase, while Xtampza ER sales grew 4% to $47.6 million.

Both products maintain strong brand fundamentals, with Belbuca rated as the #1 branded ER opioid in terms of product differentiation and favorability, and Xtampza ER rated as the #1 ER oxycodone in the same categories.

The following slide highlights the performance and positioning of the pain management portfolio:

Financial Analysis & Guidance

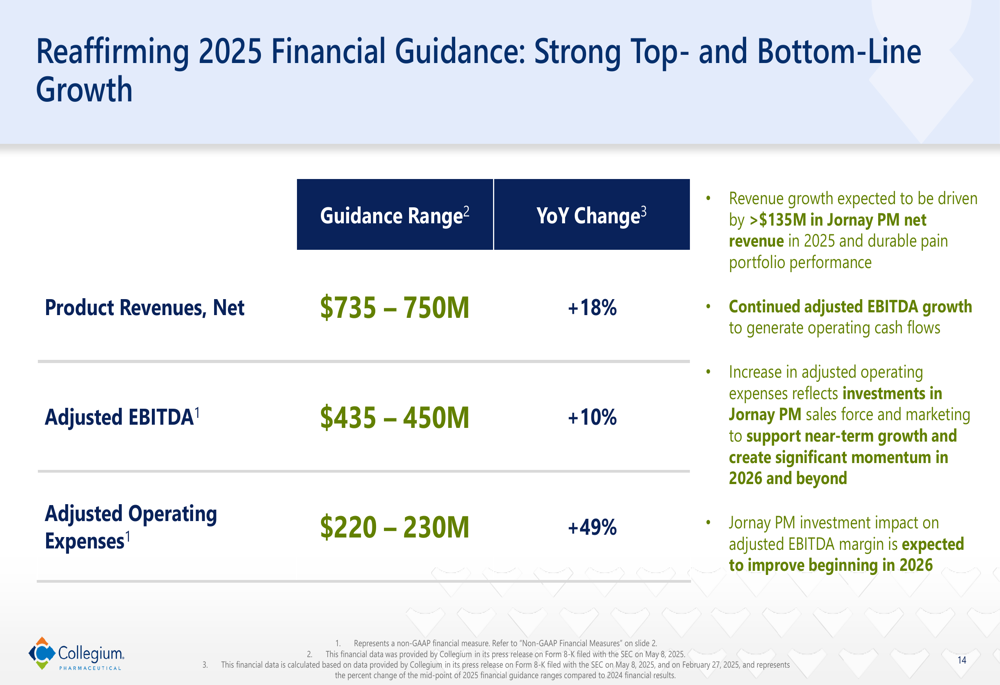

Collegium reaffirmed its 2025 financial guidance, projecting product revenues of $735-750 million, representing 18% year-over-year growth. The company expects adjusted EBITDA to reach $435-450 million, a 10% increase from 2024.

Adjusted operating expenses are projected to be $220-230 million, a 49% increase from the previous year, reflecting investments in the Jornay PM sales force and marketing. Management noted that the impact of these investments on adjusted EBITDA margin is expected to improve beginning in 2026.

The company’s financial guidance is summarized in the following slide:

Capital Deployment & Future Outlook

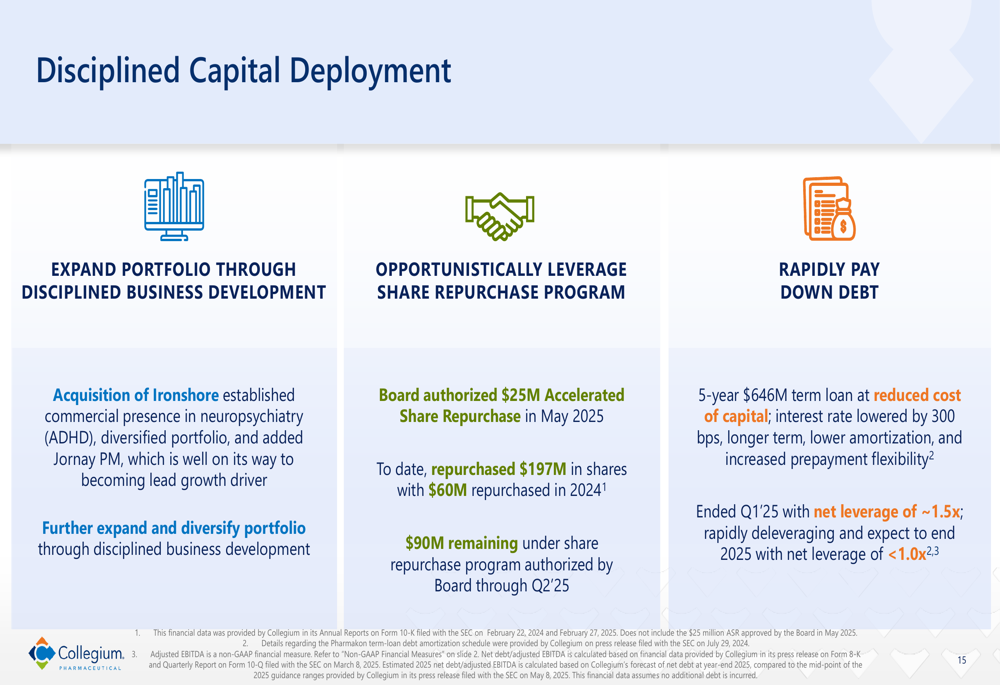

Collegium is pursuing a disciplined approach to capital deployment, focusing on three key areas: portfolio expansion through business development, share repurchases, and debt reduction.

The company’s Board authorized a $25 million Accelerated Share Repurchase in May 2025. To date, Collegium has repurchased $197 million in shares, with $60 million repurchased in 2024. The company has $90 million remaining under its share repurchase program authorized through Q2 2025.

Debt reduction remains a priority, with the company ending Q1 2025 with a net leverage ratio of approximately 1.5x. Management expects to reduce this to less than 1.0x by the end of 2025.

The capital deployment strategy is illustrated in the following slide:

Looking ahead, Collegium is focused on driving significant growth for Jornay PM, maximizing its pain portfolio, and strategically deploying capital. The company aims to create shareholder value through growing revenue, increasing profitability, generating strong cash flows, and pursuing disciplined business development opportunities.

As the company enters its next phase of growth, it is well-positioned to build on its successful strategy of portfolio diversification and operational excellence in both the pain management and ADHD markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.