Stock market today: Stocks fall as investors rotate out of tech into Jackson Hole

Introduction & Market Context

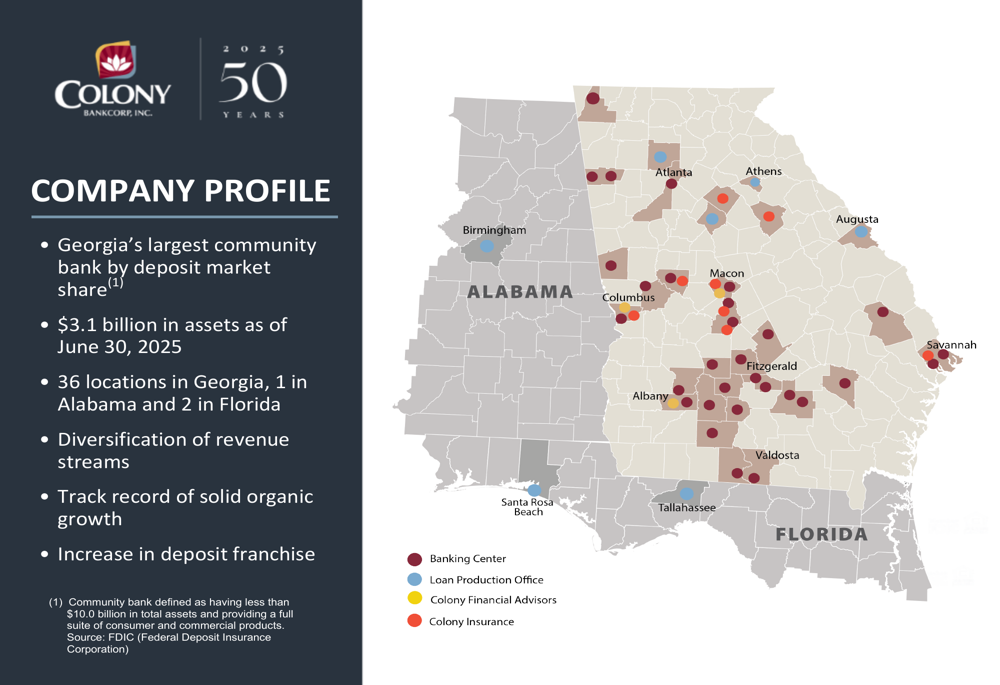

Colony Bankcorp, Inc. (NASDAQ:CBAN) released its second quarter 2025 investor presentation highlighting the company’s performance and strategic initiatives as it celebrates its 50th anniversary. The Georgia-based financial institution, which positions itself as the state’s largest community bank by deposit market share among banks with less than $10 billion in assets, reported total assets of $3.1 billion as of June 30, 2025.

The presentation comes as Colony’s stock has shown positive momentum, trading at $17.73 as of July 23, 2025, up 0.39% and significantly closer to its 52-week high of $18.49 than its low of $13.00. This represents a substantial improvement from the $15.46 closing price reported after Q1 2025 earnings.

Executive Summary

Colony Bankcorp operates 36 locations in Georgia, one in Alabama, and two in Florida, with a strategic focus on both organic growth and potential acquisitions. The bank has established short-term objectives to achieve a 1.00% return on assets while maintaining disciplined noninterest expense management. Long-term, Colony aims to develop five complementary lines of business each generating over $1 million in net income annually.

As shown in the following company profile and geographic footprint, Colony has strategically positioned itself across key markets in the Southeast:

Quarterly Performance Highlights

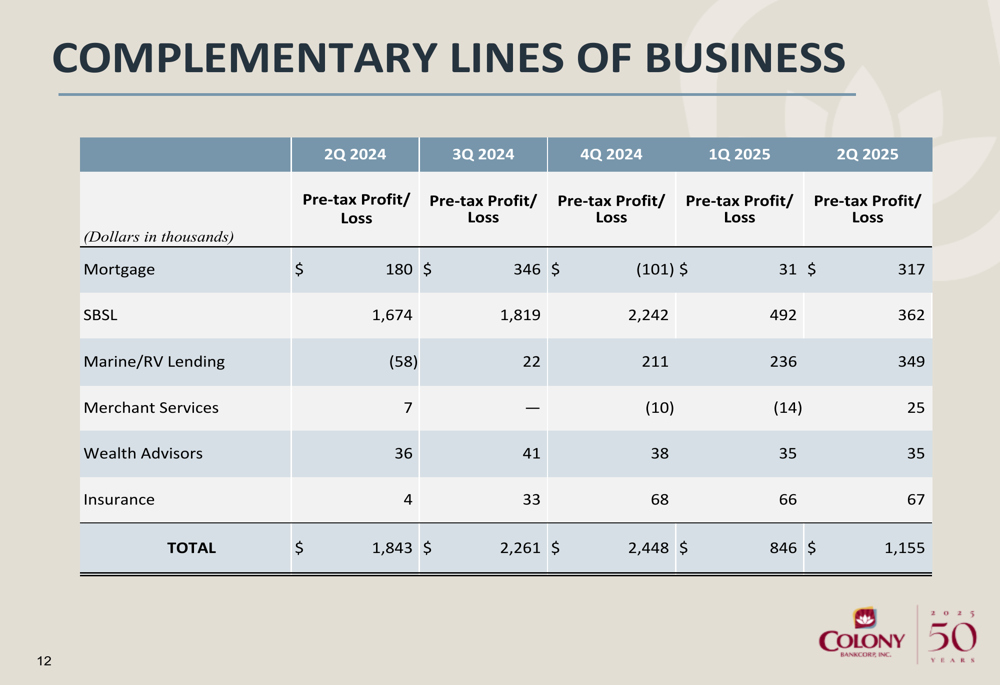

The bank’s complementary lines of business showed mixed performance in Q2 2025, with total pre-tax profit of $1.155 million, representing a recovery from $846,000 in Q1 2025 but still below the $2.448 million achieved in Q4 2024. Notably, the Mortgage division showed significant improvement, generating $317,000 in pre-tax profit in Q2 2025 compared to just $31,000 in Q1 2025.

The following table details the performance of Colony’s complementary business lines over the past five quarters:

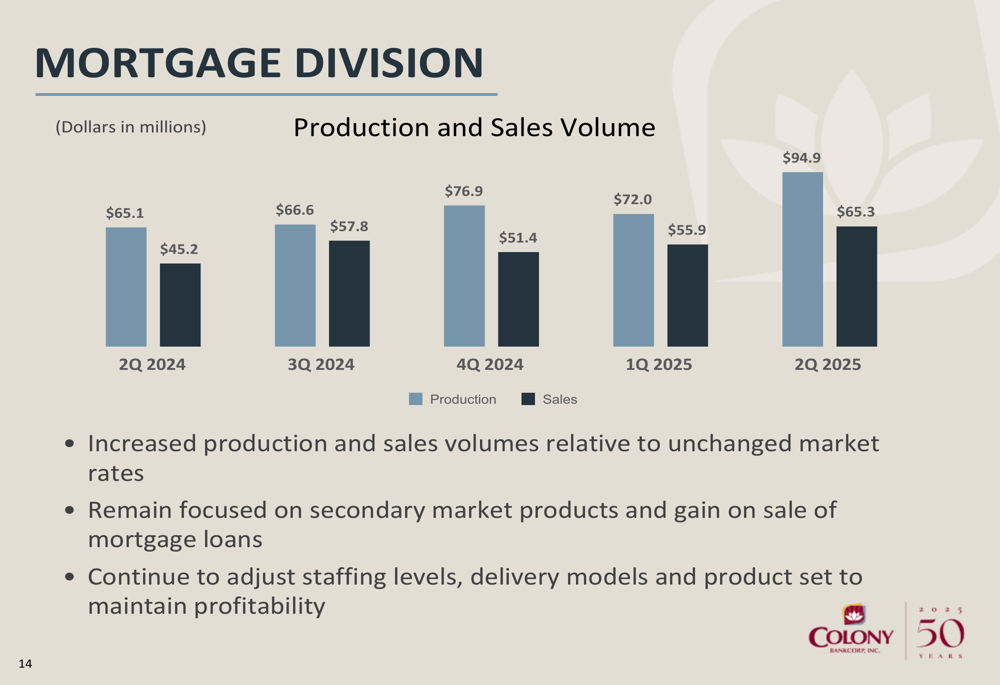

The Mortgage Division demonstrated particularly strong growth in Q2 2025, with production volume reaching $94.9 million and sales volume of $65.3 million, representing significant increases from the previous quarter despite unchanged market rates. Management noted they remain focused on secondary market products and gain on sale of mortgage loans.

As illustrated in the following chart of mortgage production and sales volumes:

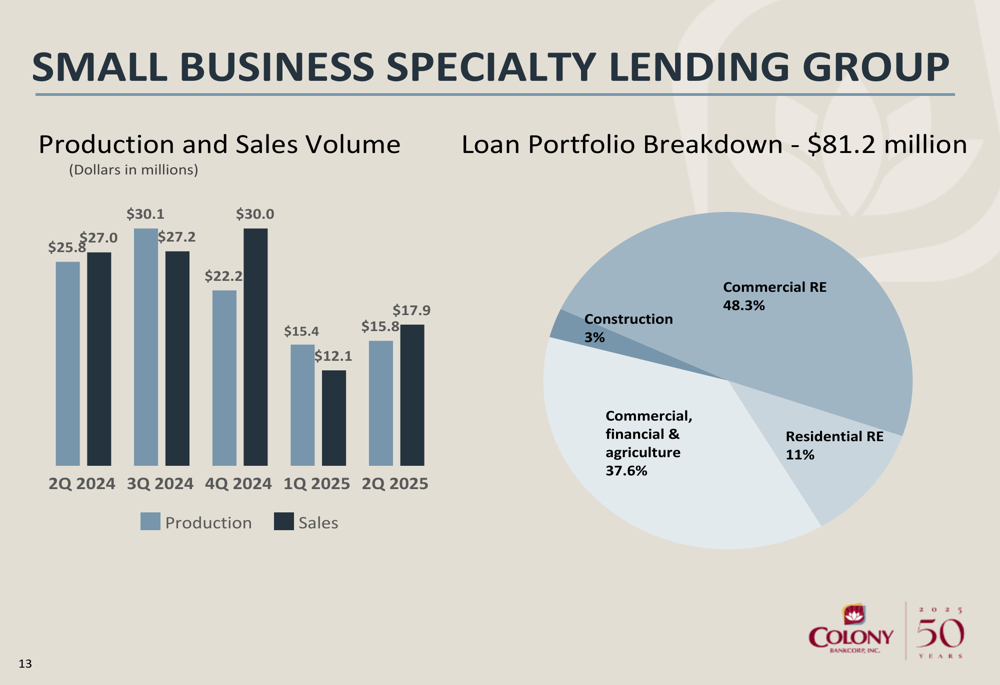

Similarly, the Small Business Specialty Lending (SBSL) Group showed signs of recovery in Q2 2025 with production of $15.8 million and sales of $17.9 million, though these figures remain below the levels seen in 2024. The SBSL loan portfolio of $81.2 million is diversified across commercial real estate (48.3%), commercial/financial/agriculture (37.6%), residential real estate (11%), and construction (3%).

Financial Position and Capital Management

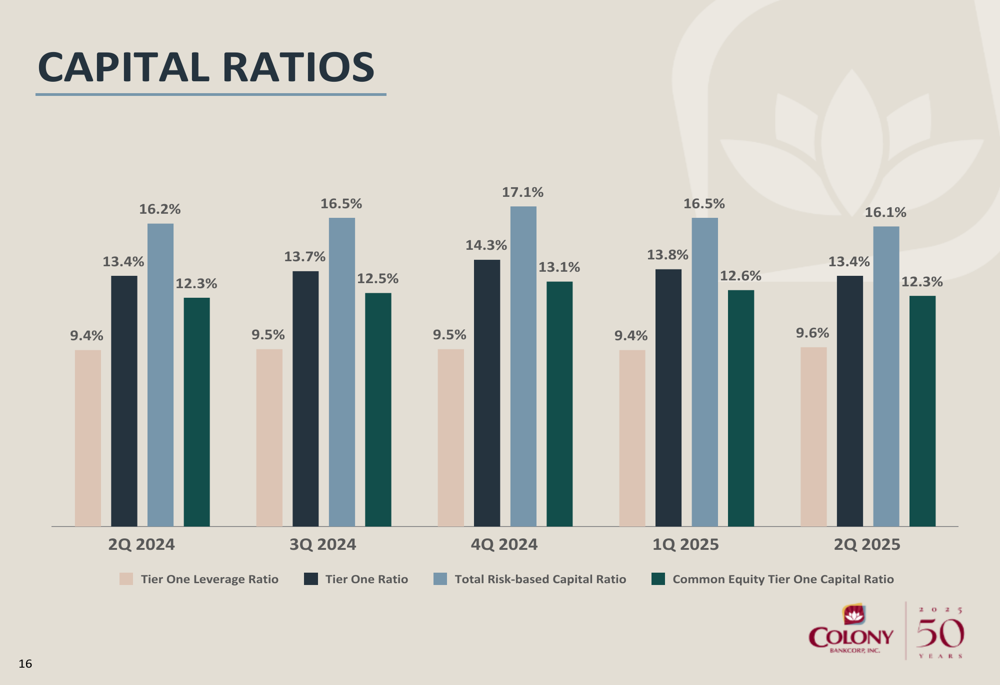

Colony maintained strong capital ratios in Q2 2025, with a Tier One Leverage Ratio of 9.6%, Tier One Ratio of 13.4%, Total (EPA:TTEF) Risk-based Capital Ratio of 16.1%, and Common Equity Tier One Capital Ratio of 12.3%. These ratios have remained relatively stable over the past five quarters, demonstrating the bank’s consistent capital management.

The following chart illustrates Colony’s capital position over time:

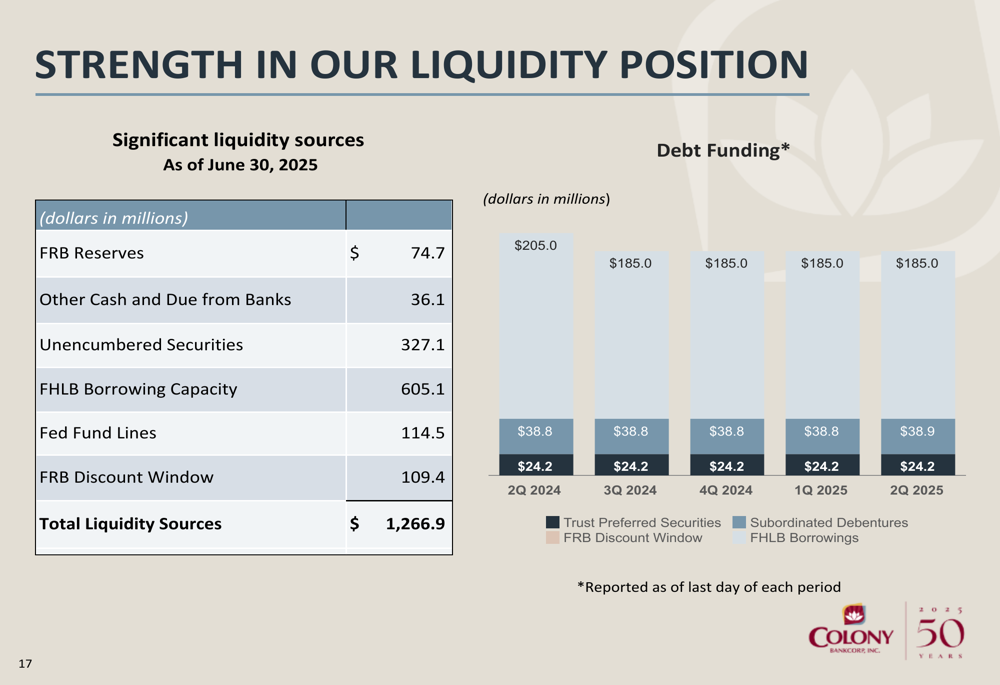

The bank’s liquidity position remains robust, with total liquidity sources of $1,266.9 million as of June 30, 2025. This includes $74.7 million in Federal Reserve reserves, $327.1 million in unencumbered securities, and $605.1 million in FHLB borrowing capacity, providing substantial flexibility for future growth initiatives.

As shown in the following breakdown of liquidity sources and debt funding:

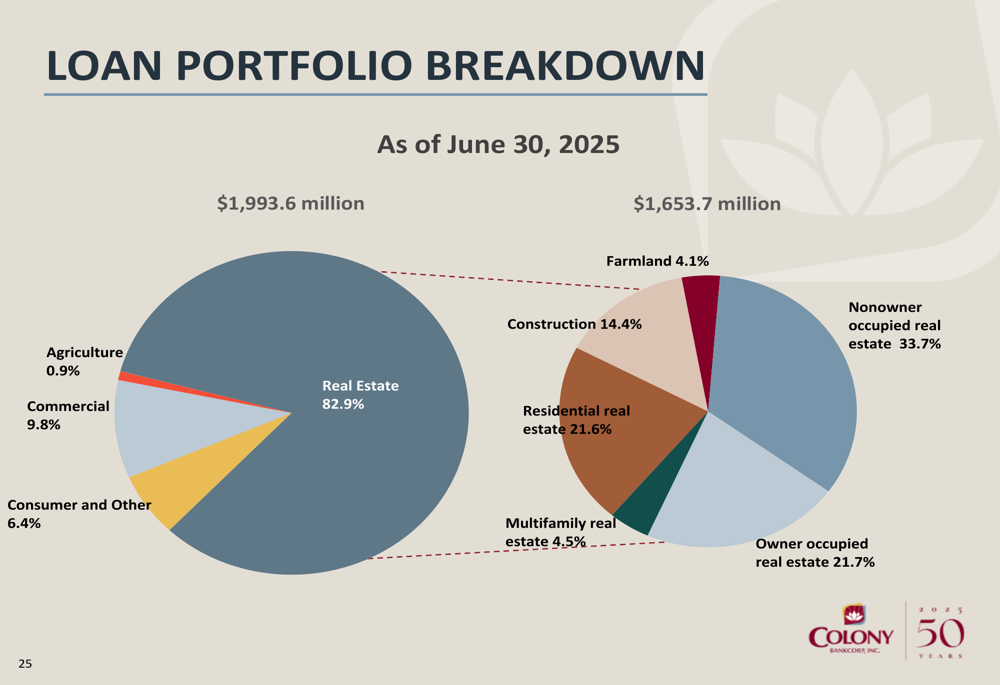

Colony’s loan portfolio totaled $1,993.6 million as of June 30, 2025, with real estate loans comprising 82.9% of the total. Within the real estate category, nonowner occupied real estate represents the largest segment at 33.7%, followed by owner-occupied real estate at 21.7% and residential real estate at 21.6%.

The following charts illustrate the composition of Colony’s loan portfolio:

Strategic Initiatives

As Colony celebrates its 50th anniversary, the bank has outlined several strategic initiatives to drive future growth. These include:

1. Organic growth in dynamic markets such as Atlanta, Augusta, Birmingham, North Florida, and Savannah, with a target of returning to 8-12% organic growth by the end of 2025.

2. Mergers and acquisitions, with a focus on becoming "the acquirer of choice" in Georgia and contiguous states. The bank has identified 319 potential acquisition targets with assets under $600 million and 87 banks with assets between $600 million and $1.2 billion.

3. Efficiency improvements through process optimization, including the hiring of a Director of Optimization and implementation of Robotic Process Automation (RPA) to enhance customer experience.

4. Innovation and data strategy, including the implementation of a Salesforce-based CRM system, nCino for loan processing, and middleware for Fintech partnerships.

Shareholder Returns and Outlook

Colony has maintained a shareholder-focused dividend policy, with a quarterly dividend of $0.1150 per share declared for Q2 2025, representing an annual rate of $0.46 per share and a yield of 2.6% based on the July 21, 2025 closing price. This continues a pattern of steady dividend increases from $0.1025 in 2021.

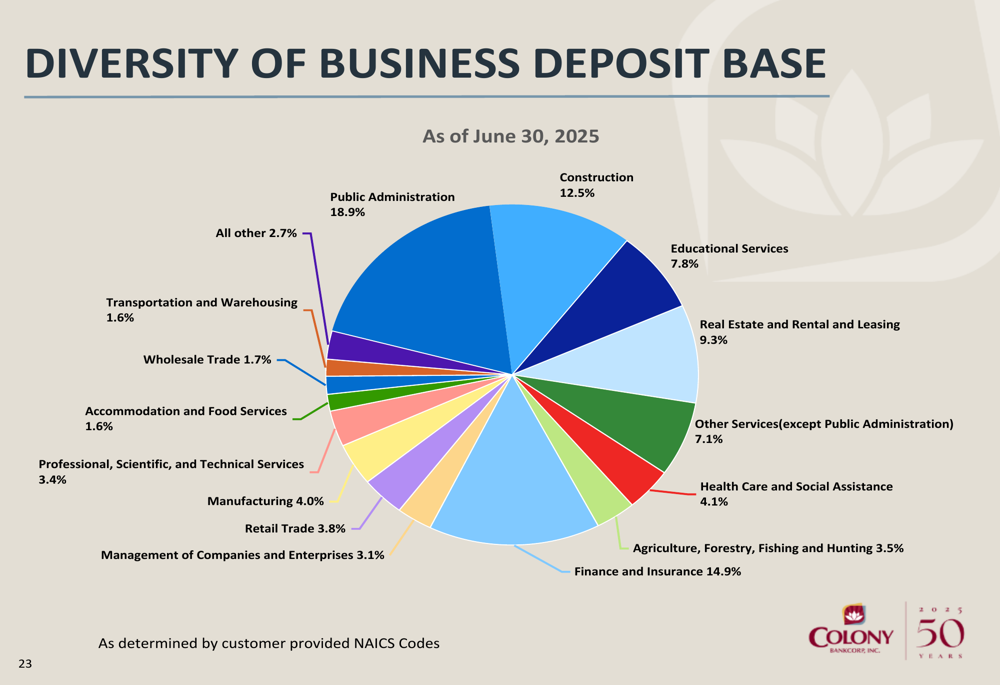

The bank’s deposit base remains well-diversified across sectors, with public administration (18.9%), finance and insurance (14.9%), and construction (12.5%) representing the largest segments. This diversification helps mitigate concentration risk and provides stability to the deposit base.

The following chart illustrates the diversity of Colony’s business deposit base:

Looking ahead, Colony aims to maintain its noninterest expense discipline while growing core deposits and customer relationships. The bank expects to benefit from industry consolidation and is targeting growth in its customer base of 8-12% per year over the long term, aligning with the outlook provided in its Q1 2025 earnings report.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.