Nvidia and TSMC to unveil first domestic wafer for Blackwell chips, Axios reports

Introduction & Market Context

Comerica Inc. (NYSE:CMA) presented its second quarter 2025 financial results on July 18, 2025, showcasing solid performance with notable improvements in profitability metrics. The bank’s stock has performed strongly, with a 51.6% return over the past six months according to recent market data, and currently trades near $77.37, representing a 2.55% increase.

The Q2 results come amid a challenging banking environment characterized by deposit competition and evolving customer expectations for payment solutions. Comerica has positioned itself strategically by balancing "small bank service" with "large bank capabilities" to differentiate in the marketplace.

Quarterly Performance Highlights

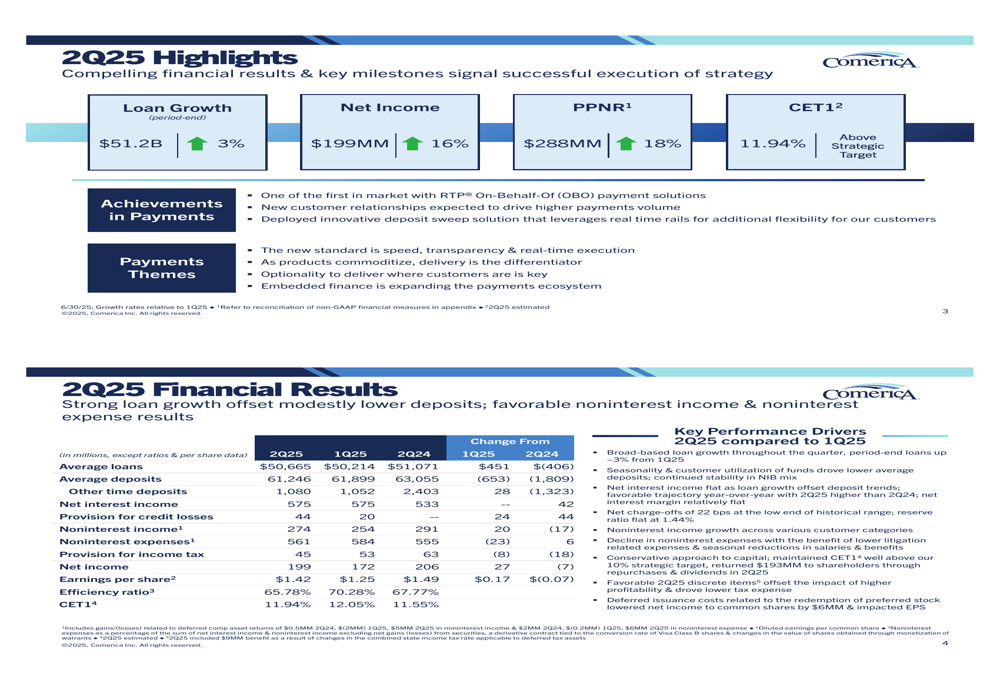

Comerica reported a 16% increase in net income to $199 million and an 18% rise in pre-provision net revenue (PPNR) to $288 million for Q2 2025. Earnings per share reached $1.42, up 14% from $1.25 in the previous quarter, though slightly below the $1.49 reported in Q2 2024.

The bank maintained stable net interest income at $575 million, unchanged from Q1 2025 but up from $533 million in Q2 2024. Period-end loan growth increased by 3% to $51.2 billion, while the CET1 ratio stood at 11.94%, well above the company’s strategic target.

As shown in the following financial results summary:

The efficiency ratio improved to 65.78% in Q2 2025 from 70.28% in Q1 2025, reflecting better cost management and operational effectiveness. This improvement was driven by a 3.9% reduction in noninterest expenses combined with a 7.9% increase in noninterest income.

Detailed Financial Analysis

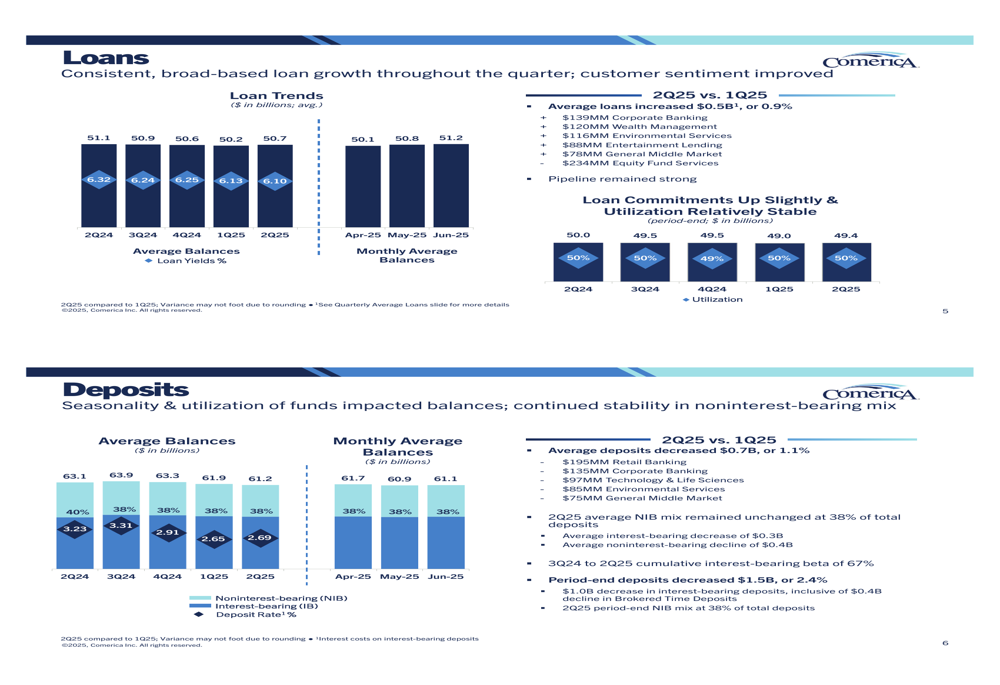

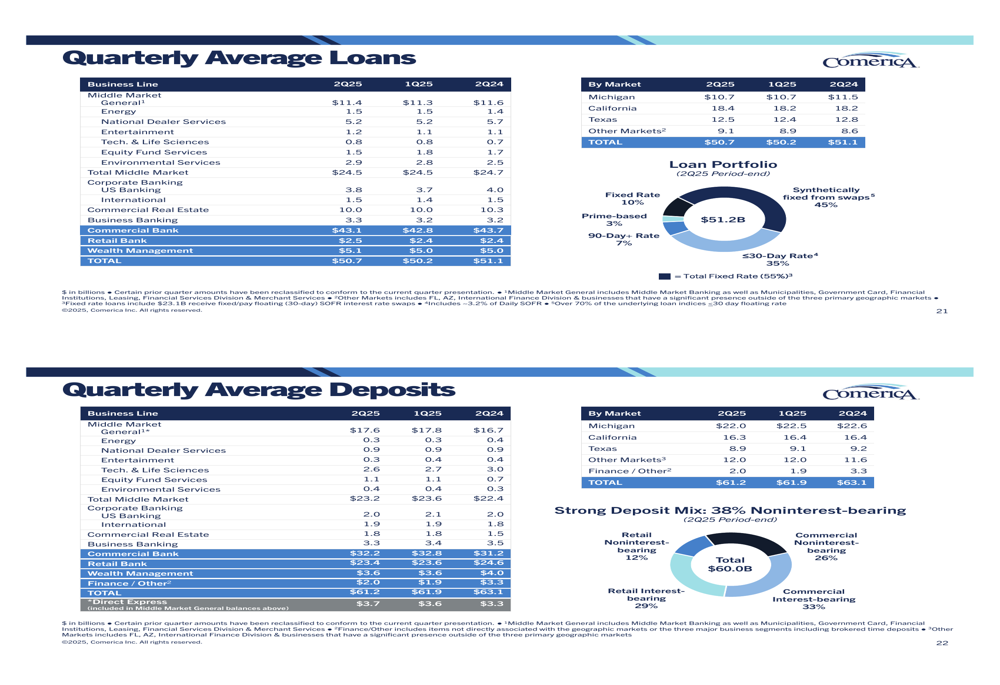

Comerica’s loan portfolio showed steady growth with average loans increasing to $50.67 billion in Q2 2025, up from $50.21 billion in Q1 2025. Growth was broad-based across multiple segments, with notable increases in Corporate Banking ($139 million), Wealth Management ($120 million), and Environmental Services ($116 million).

However, deposit trends remained challenging, with average deposits declining to $61.25 billion in Q2 2025 from $61.90 billion in Q1 2025 and $63.06 billion in Q2 2024. The noninterest-bearing deposit mix remained unchanged at 38% of total deposits.

The following chart illustrates these loan and deposit trends:

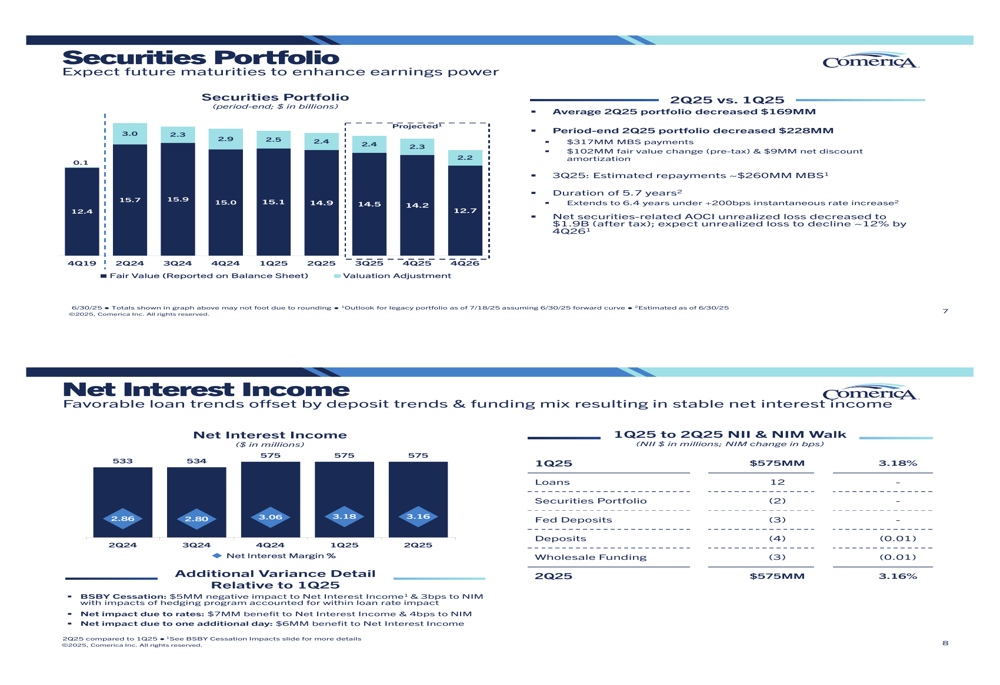

Net interest margin slightly contracted to 3.16% in Q2 2025 from 3.18% in Q1 2025, primarily due to higher funding costs and the impact of BSBY cessation, which had a $5 million negative effect. The securities portfolio decreased by $228 million period-end, with projected repayments of approximately $260 million in MBS for Q3 2025.

As shown in the net interest income breakdown:

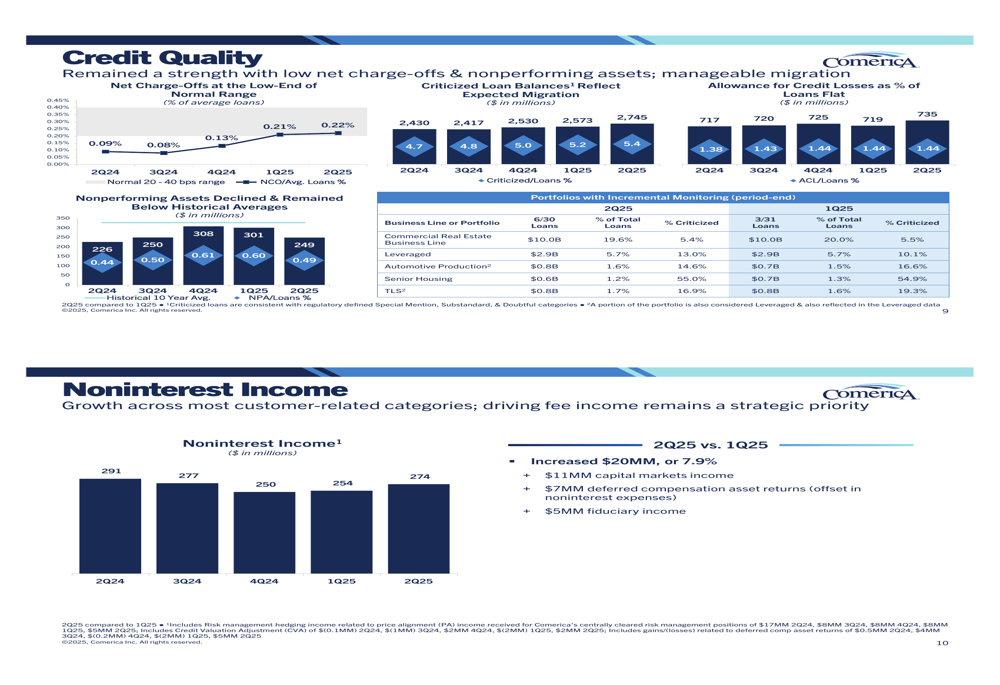

Noninterest income increased to $274 million in Q2 2025 from $254 million in Q1 2025, while noninterest expenses decreased to $561 million from $584 million. This favorable combination contributed significantly to the improved efficiency ratio and overall profitability.

Credit Quality and Risk Management

Comerica’s credit quality metrics showed some signs of stress in Q2 2025. Net charge-offs increased slightly to 0.22% of average loans from 0.21% in Q1 2025 and 0.08% in Q2 2024. Criticized loan balances rose to $2.75 billion, representing 5.4% of total loans compared to 5.2% in Q1 2025.

Certain portfolios remain under incremental monitoring, particularly Senior Housing, which had criticized loans at 55.0% in Q2 2025. The allowance for credit losses stood at $728 million, with the ratio of allowance to loans remaining stable.

The following chart details these credit quality trends:

Strategic Initiatives

Comerica highlighted its strategic focus on payment innovations, noting it was "one of the first in market with RTP® On-Behalf-Of (OBO) payment solutions." The bank also deployed an innovative deposit sweep solution leveraging real-time rails to provide additional flexibility for customers.

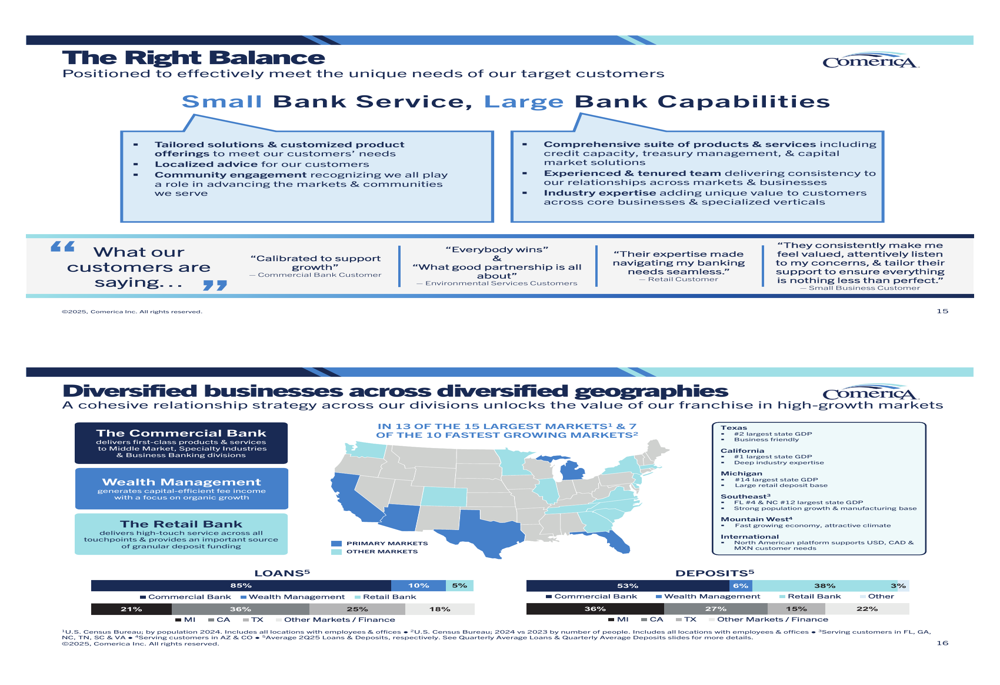

The company emphasized its diversified business model across commercial banking (85% of loans), wealth management (10%), and retail banking (5%), with geographic diversification across markets including Michigan, Texas, and California.

This strategic diversification is illustrated in the following breakdown:

Comerica’s capital management strategy remains focused on maintaining strong capital levels, with the CET1 ratio at 11.94% and tangible common equity ratio improving to 8.04% from 7.82% in Q1 2025. The bank’s interest rate sensitivity analysis suggests it is well-positioned to insulate income as rates decline.

Forward-Looking Statements

Looking ahead to Q3 2025, Comerica’s management expects steady loan growth, moderately higher deposits, and slightly lower net interest income compared to Q2 2025. For the full year 2025 versus 2024, the bank projects:

- Average loans: Flat to down 1%

- Average deposits: Down 2% to 3%

- Net interest income: Up 5% to 7%

- Noninterest income: Up 2%

- Noninterest expenses: Up 2%

- Net charge-offs: Within the low end of the normal 20 to 40 basis points range

- Effective tax rate: Approximately 22%

Management also expects to maintain capital well above the CET1 target of 10%, as shown in their outlook:

Comerica’s focus on payment innovation, diversified business model, and improved operational efficiency positions it well for continued performance, though deposit challenges and credit quality will require ongoing attention as the bank navigates through the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.