Asia FX cautious amid US govt shutdown; yen tumbles after Takaichi’s LDP win

Introduction & Market Context

CommScope Holding Company (NASDAQ:COMM) unveiled its second quarter 2025 results on August 4, announcing a transformative $10.5 billion sale of its Connectivity and Cable Solutions (CCS) business to Amphenol (NYSE:APH) alongside record financial performance. The company’s stock surged 86.26% following the announcement, reflecting investor enthusiasm for both the strategic divestiture and exceptional quarterly results.

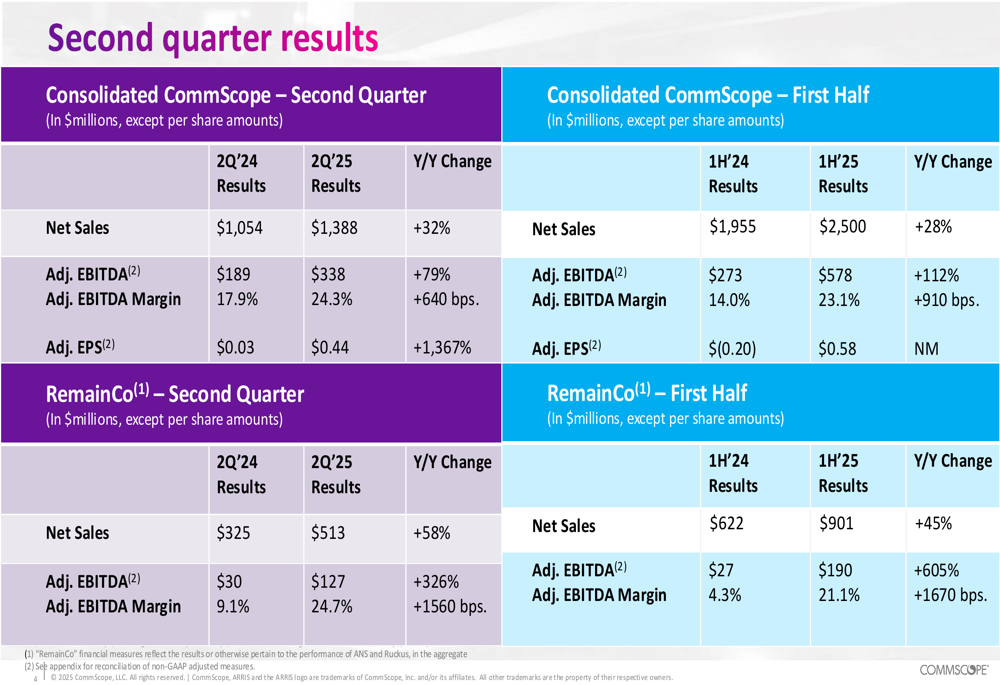

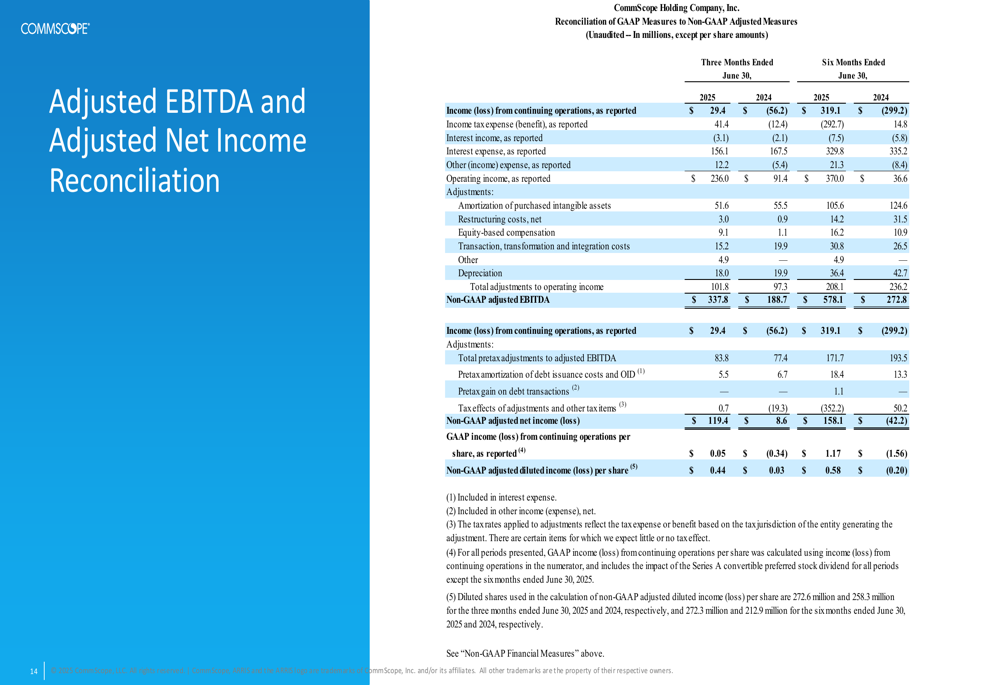

The presentation revealed significant growth across all business segments, with consolidated net sales increasing 32% year-over-year to $1.388 billion and Adjusted EBITDA soaring 79% to $338 million. This performance continues the momentum seen in Q1, when CommScope beat earnings expectations and saw its stock begin a substantial upward trajectory.

Strategic Transformation

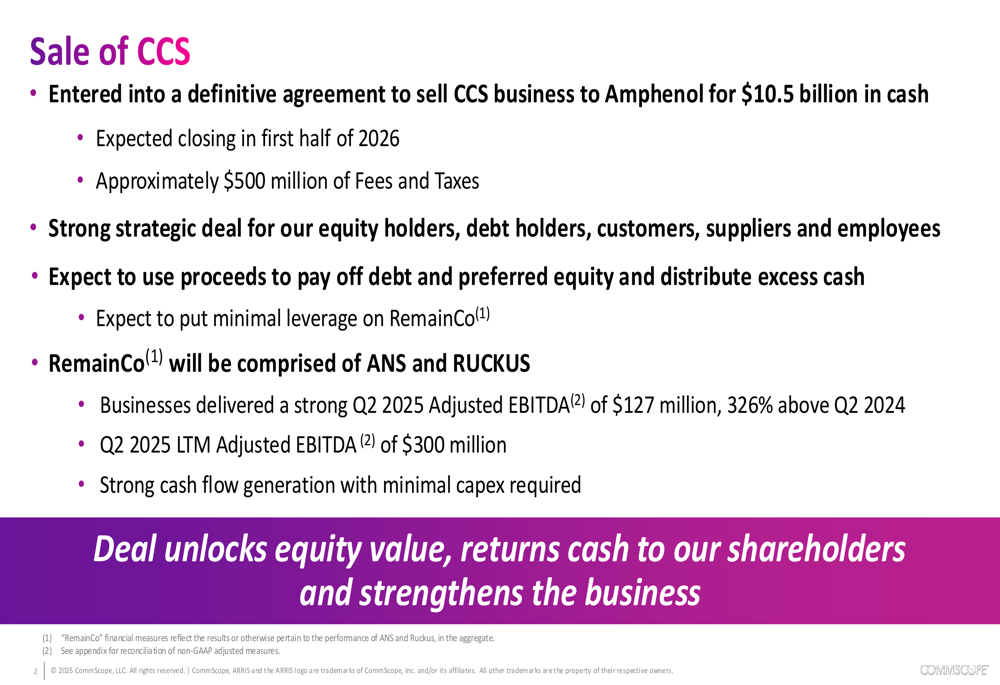

The most significant announcement was CommScope’s agreement to sell its CCS business to Amphenol for $10.5 billion in cash, a transaction expected to close in the first half of 2026. The company plans to use the proceeds to pay off debt and preferred equity while distributing excess cash to shareholders.

As shown in the following strategic overview:

Post-divestiture, "RemainCo" will consist of the Access Network Solutions (ANS) and RUCKUS businesses, which together delivered Q2 2025 Adjusted EBITDA of $127 million—a remarkable 326% increase from Q2 2024. Management emphasized that the deal is strategically beneficial for all stakeholders, including equity holders, debt holders, customers, suppliers, and employees.

The transaction aims to position RemainCo with minimal leverage while maintaining strong cash flow generation capabilities. This represents a significant shift for CommScope, which currently carries a 6.6x net leverage ratio.

Quarterly Performance Highlights

CommScope’s Q2 2025 results demonstrated exceptional growth across all key metrics, with the fifth consecutive quarter of sequential Adjusted EBITDA improvement. The comprehensive financial results show substantial year-over-year improvements:

Particularly noteworthy was the expansion in Adjusted EBITDA margin, which increased 640 basis points year-over-year to 24.3%. Adjusted earnings per share jumped dramatically from $0.03 in Q2 2024 to $0.44 in Q2 2025, reflecting the company’s improved operational efficiency and revenue growth.

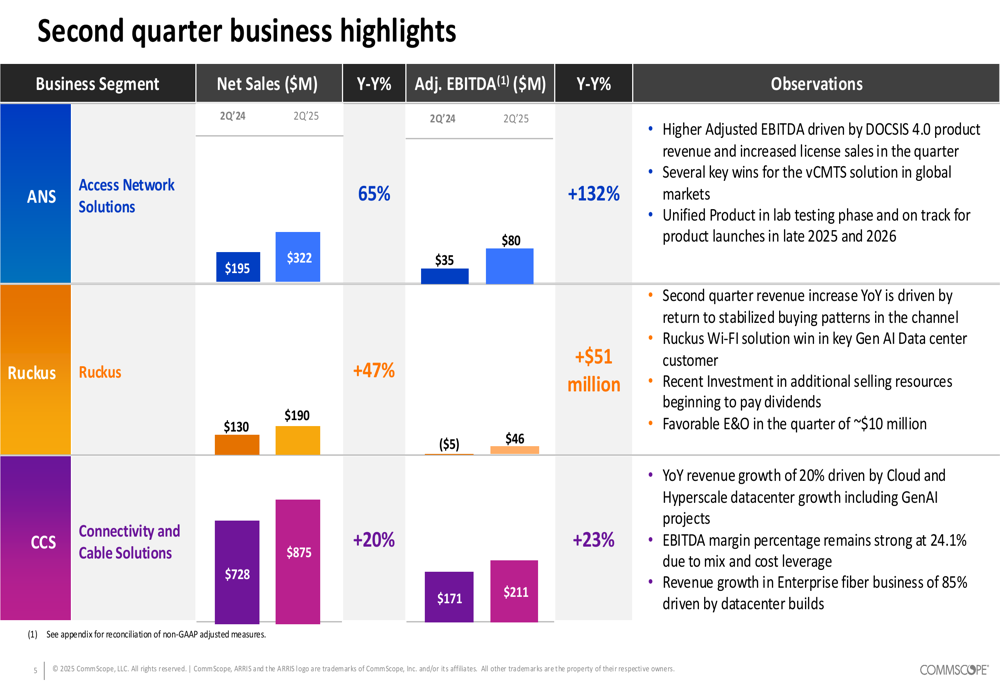

All three business segments contributed to the strong performance, with each showing significant growth in both sales and profitability:

The ANS segment delivered the strongest relative performance with a 65% increase in net sales to $322 million and a 132% jump in Adjusted EBITDA to $80 million, driven by DOCSIS 4.0 product revenue and increased license sales. Ruckus also showed impressive growth with net sales up 47% to $190 million and a $51 million improvement in Adjusted EBITDA. The CCS segment, which is set to be divested, grew net sales by 20% to $875 million and EBITDA by 23% to $211 million, benefiting from Cloud and Hyperscale datacenter growth including GenAI projects.

Financial Position

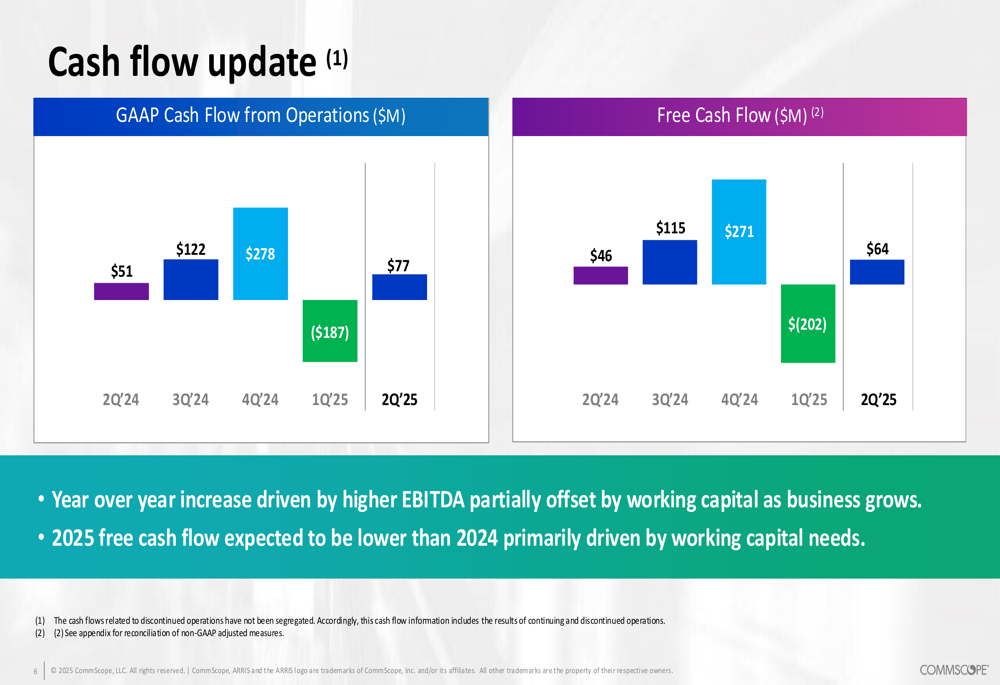

CommScope’s cash flow performance showed year-over-year improvement, though the company noted that 2025 free cash flow is expected to be lower than 2024 primarily due to working capital needs associated with business growth.

The quarterly cash flow trends demonstrate the company’s ability to generate positive free cash flow despite ongoing investments:

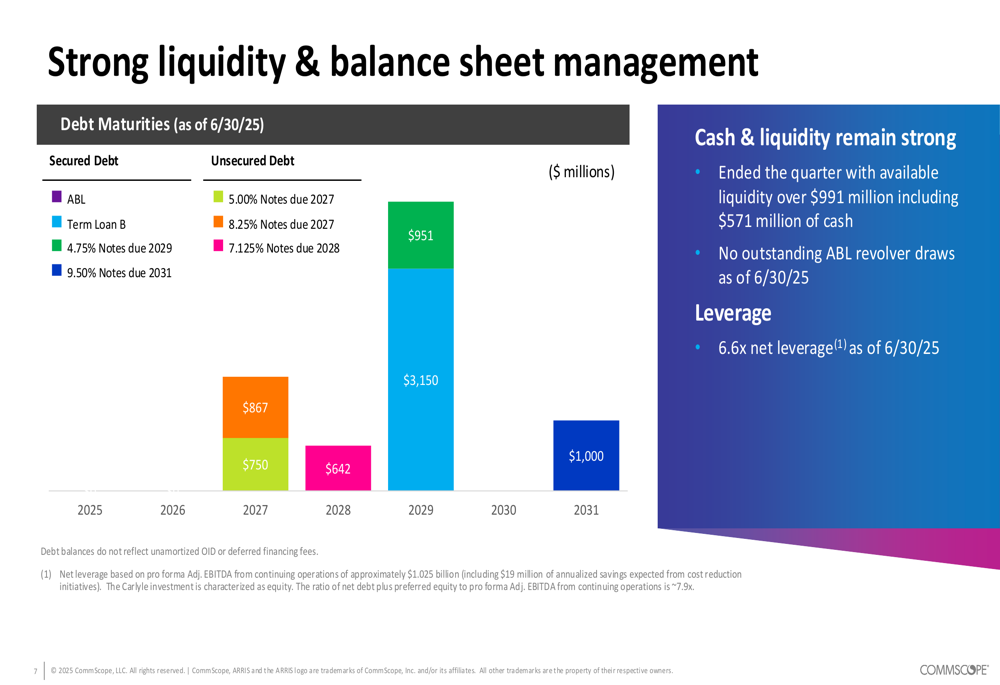

The company’s balance sheet remains heavily leveraged, with debt maturities concentrated in 2027 ($951 million) and 2028 ($3,150 million). However, liquidity appears adequate with $991 million available, including $571 million in cash:

The planned CCS divestiture should significantly improve CommScope’s financial position by providing substantial proceeds to address the debt burden, which has been a persistent concern for investors.

Forward-Looking Statements

Based on the strong first-half performance, CommScope has revised its 2025 Adjusted EBITDA guidance upward to between $1.15 billion and $1.20 billion. For RemainCo specifically, the company expects Adjusted EBITDA to reach between $325 million and $350 million for the full year 2025.

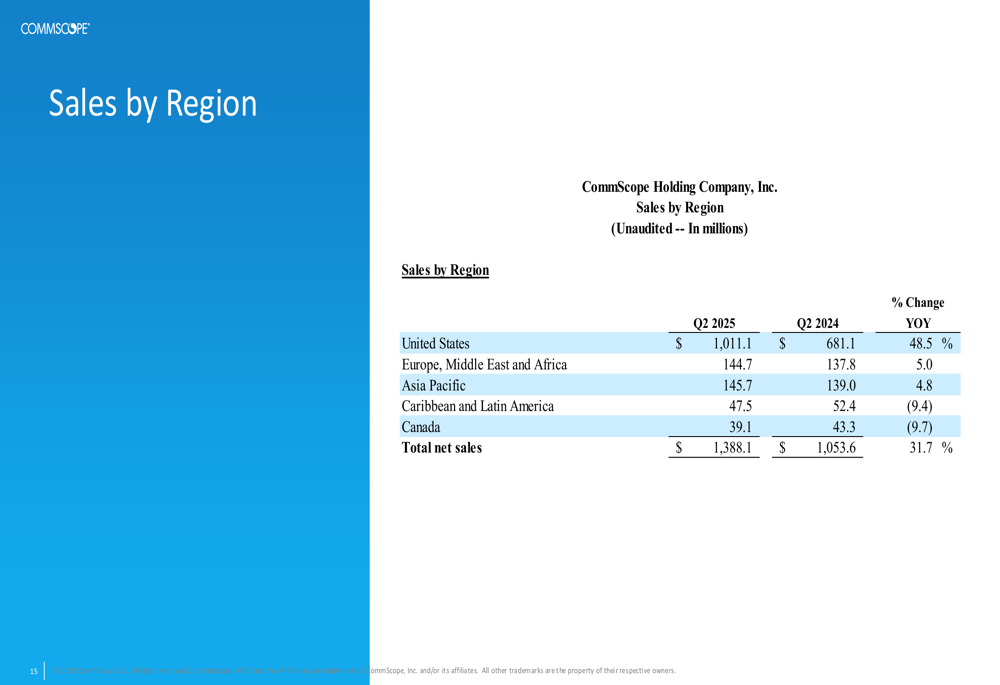

Management highlighted ongoing initiatives to mitigate the effects of tariffs, which remain a potential headwind. The company’s geographic sales breakdown shows continued strength in the U.S. market, which accounted for $1,011.1 million of the $1,388.1 million in total net sales during Q2:

The segment breakdown further illustrates the growth potential of each business unit, with all three segments now achieving similar Adjusted EBITDA margins in the 24-25% range:

Executive Summary

CommScope’s Q2 2025 results and strategic announcements represent a potential inflection point for the company. The planned $10.5 billion divestiture of the CCS business addresses the company’s leverage concerns while allowing management to focus on the high-growth ANS and RUCKUS segments.

The exceptional financial performance across all segments demonstrates CommScope’s strong positioning in growth markets, particularly in DOCSIS 4.0 technologies and cloud infrastructure. With five consecutive quarters of sequential EBITDA improvement and significant margin expansion, the company appears to be executing effectively on both operational and strategic fronts.

Investors have responded enthusiastically to these developments, as evidenced by the 86.26% stock price increase. If the company can successfully complete the CCS divestiture and maintain the growth momentum in its remaining businesses, CommScope may be positioned for a sustainable turnaround after years of challenging performance.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.