Bubble Wrap maker Sealed Air surges on report of buyout talks

Introduction & Market Context

CompoSecure Inc (NASDAQ:CMPO) presented its third quarter 2025 earnings results on November 3, showcasing robust financial performance and announcing a transformative acquisition. The company’s stock surged 28.25% following the announcement, reaching $25.47, well above its previous 52-week high of $21.16.

The metal payment card manufacturer reported strong growth metrics despite mixed regional performance, with domestic strength offsetting international weakness. The company’s presentation highlighted favorable market trends, including the continued expansion of the global payment card market, which is growing at a 7.5% CAGR according to the company’s data.

Quarterly Performance Highlights

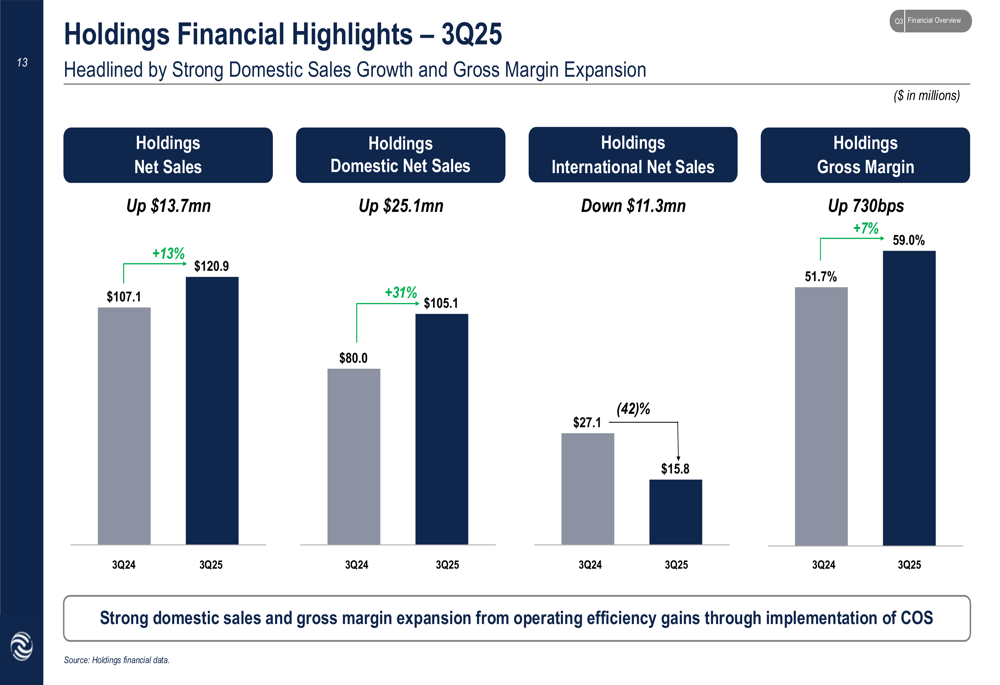

CompoSecure reported Non-GAAP net sales of $120.9 million for Q3 2025, representing a 13% increase year-over-year, exceeding analyst expectations of $117.23 million. The company’s domestic net sales showed particularly strong performance, increasing by $25.1 million or 31% compared to Q3 2024, while international net sales declined by $11.3 million or 42%.

As shown in the following chart of the company’s financial highlights:

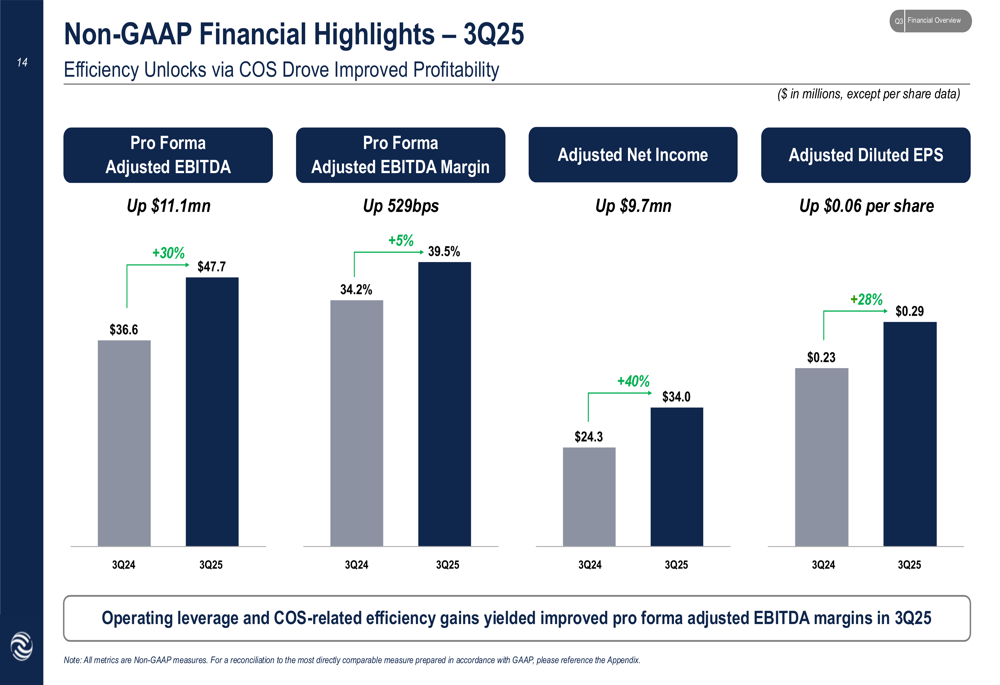

Profitability metrics showed even more impressive gains, with Pro Forma Adjusted EBITDA reaching $47.7 million, up 30% year-over-year. The company’s gross margin expanded significantly to 59.0%, representing a 730 basis point improvement from the prior year period. EBITDA margin also improved substantially, increasing by 529 basis points to 39.5%.

The following chart illustrates these profitability improvements:

CompoSecure maintained a strong balance sheet with $224.6 million in cash and cash equivalents plus $40.7 million in short-term investments, against $190.0 million in total debt. This financial position provides flexibility for both organic growth initiatives and strategic acquisitions.

Strategic Initiatives

The presentation highlighted several recent customer wins, showcasing CompoSecure’s ability to secure partnerships with both traditional financial institutions and fintech companies. These new launches include premium card programs for Citi, Chime, Itau, BAC (Alaska Airlines), BMO, and cryptocurrency platforms like Gemini and Uphold.

The following image displays these recent customer card programs:

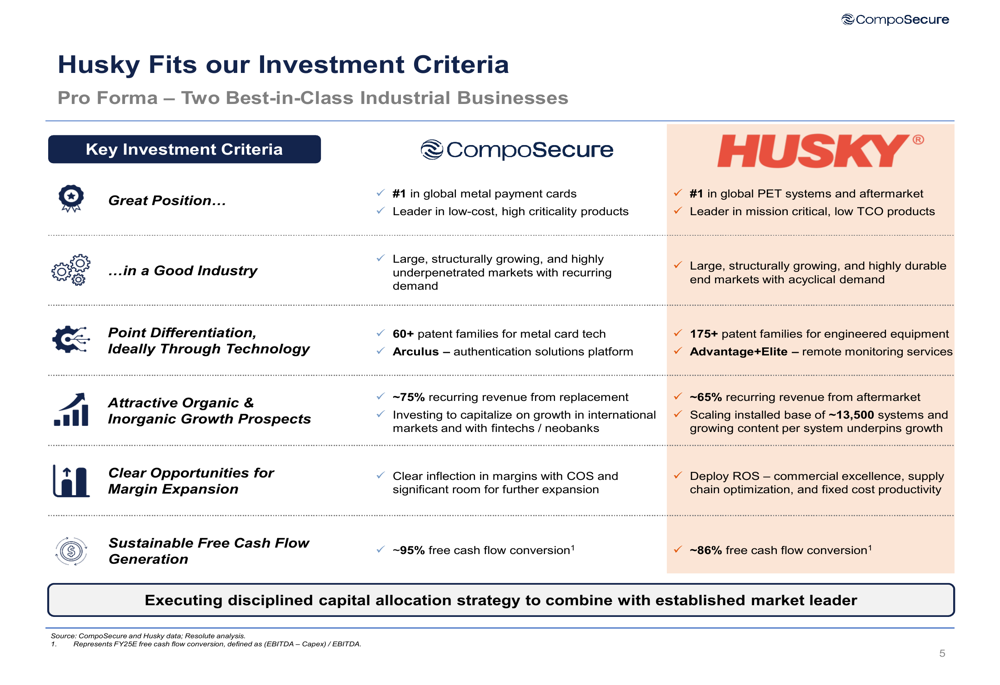

The most significant strategic announcement was CompoSecure’s planned acquisition of Husky Technologies for approximately $5.0 billion. Husky is described as a market-leading manufacturer of engineered equipment and aftermarket services, with approximately $1.58 billion in revenue and $400 million in Net Adjusted EBITDA, representing a 25% margin.

The acquisition rationale is illustrated in the following slide:

Management emphasized that the combination creates a "best-in-class, diversified compounder" with global market leadership positions in complementary industries. The transaction is expected to be funded through equity placements and debt, with an anticipated closing in the first quarter of 2026.

Key metrics of the acquisition target are presented here:

The combined entity is projected to generate approximately $2.22 billion in revenue and $635 million in Net Adjusted EBITDA, with a 29% EBITDA margin. Management expects the transaction to be approximately 20% accretive to earnings.

Forward-Looking Statements

CompoSecure raised its full-year 2025 guidance, now projecting Non-GAAP net sales of approximately $463 million (up from previous guidance of $455 million) and Pro Forma Adjusted EBITDA of $165-170 million (increased from $158 million).

The company also issued its initial 2026 guidance, forecasting Non-GAAP net sales of approximately $510 million and Pro Forma Adjusted EBITDA of approximately $190 million, representing continued growth momentum.

The following chart illustrates the company’s updated guidance:

The pro forma financial projections for the combined entity with Husky Technologies show substantial growth potential:

Competitive Industry Position

CompoSecure’s presentation emphasized the value proposition of metal payment cards for issuers. According to the company, metal cards represent only about 0.5% of total program costs for issuers but can increase customer spend by approximately 5% and drive customer acquisition and retention with a 10%+ increase in demand.

The company highlighted the favorable market backdrop for payment cards, with Visa and Mastercard credit and charge cards in global circulation growing at a 5.2% CAGR from 2021 to 2025. The broader market including debit cards is growing even faster at a 7.5% CAGR.

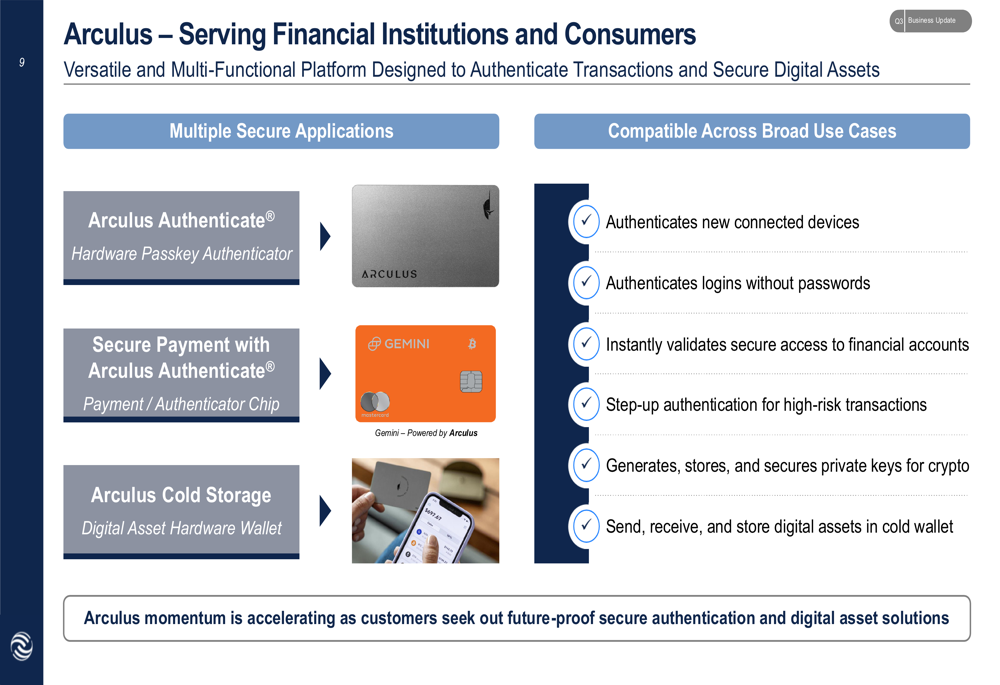

CompoSecure is also expanding beyond traditional payment cards with its Arculus platform, which provides authentication solutions for financial institutions and consumers. The platform includes hardware passkey authenticators, secure payment solutions, and digital asset hardware wallets, positioning the company in the growing digital security market.

As shown in the following image of the Arculus product line:

CEO Jon Wilk expressed optimism about the company’s trajectory, stating, "The progress we have made over the past year is increasingly positive in our financial performance, in the way we operate, and in the culture that is taking shape across the organization." Executive Chairman David M. Cote highlighted the strategic acquisition, saying, "We view the combination of CompoSecure and Husky as the foundation for a best-in-class, diversified compounder."

While domestic growth remains strong, the significant decline in international sales presents a challenge that management will need to address. However, the diversification provided by the Husky acquisition may help mitigate regional performance fluctuations in the future.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.