BETA Technologies launches IPO of 25 million shares priced $27-$33

Introduction & Market Context

Conagra Brands Inc (NYSE:CAG) released its first quarter fiscal 2026 earnings presentation on October 1, 2025, showing signs of recovery in consumption and market share despite ongoing inflationary pressures. The company’s stock traded up 1.58% to $18.60 in premarket trading, building on the previous day’s 1.5% gain to $18.31.

The packaged food giant is navigating a challenging environment characterized by persistent inflation and weak consumer sentiment, which continues to drive value-seeking behavior among shoppers. Despite these headwinds, Conagra maintained its full-year guidance and highlighted progress in its strategic priorities.

Quarterly Performance Highlights

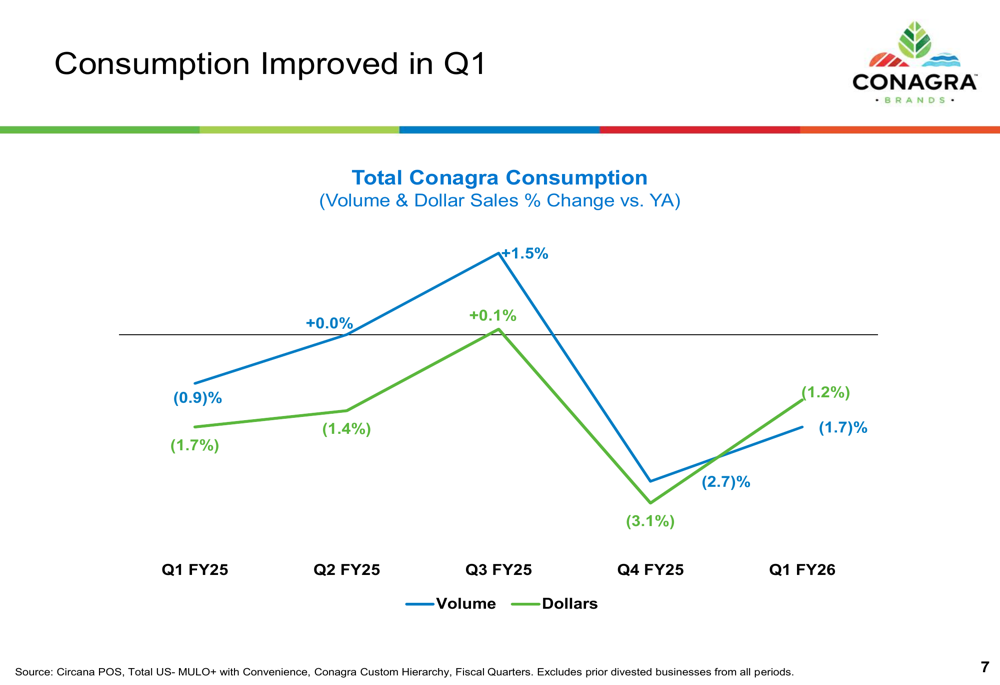

Conagra reported modest improvement in consumption trends compared to the previous quarter. As shown in the following chart of volume and dollar sales changes, the company’s performance recovered from the supply-challenged fourth quarter:

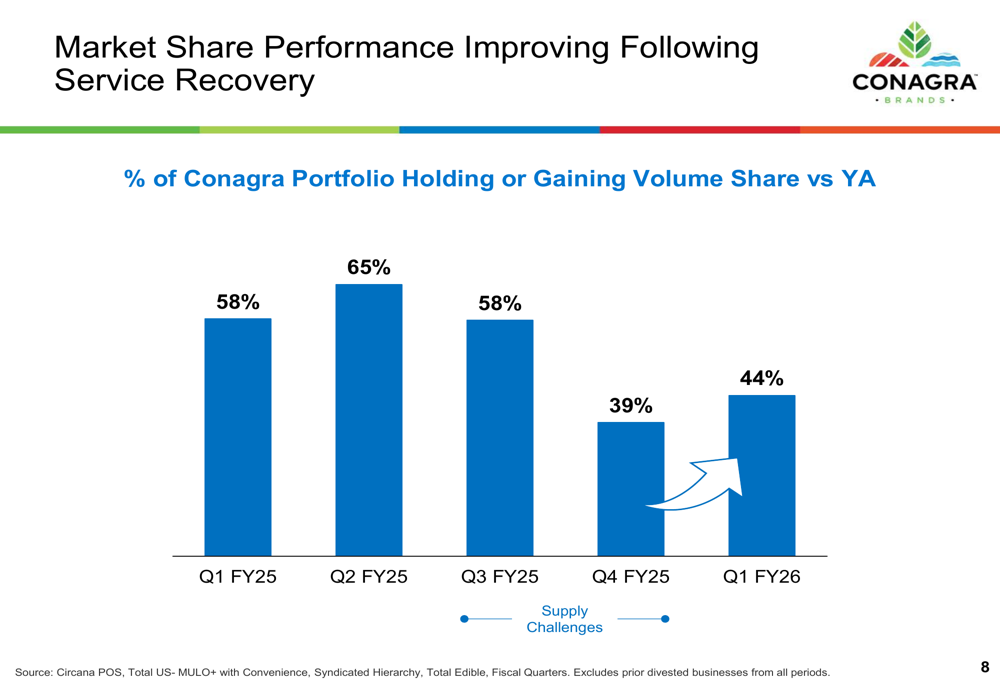

Volume improved from -3.1% in Q4 FY25 to -1.2% in Q1 FY26, while dollar sales improved from -2.7% to -1.7%. This recovery coincided with improvements in market share performance, which had been negatively impacted by supply chain challenges in the previous quarter:

The percentage of Conagra’s portfolio holding or gaining volume share increased to 44% in Q1 FY26, up from 39% in Q4 FY25, though still below the 58-65% range seen in earlier quarters.

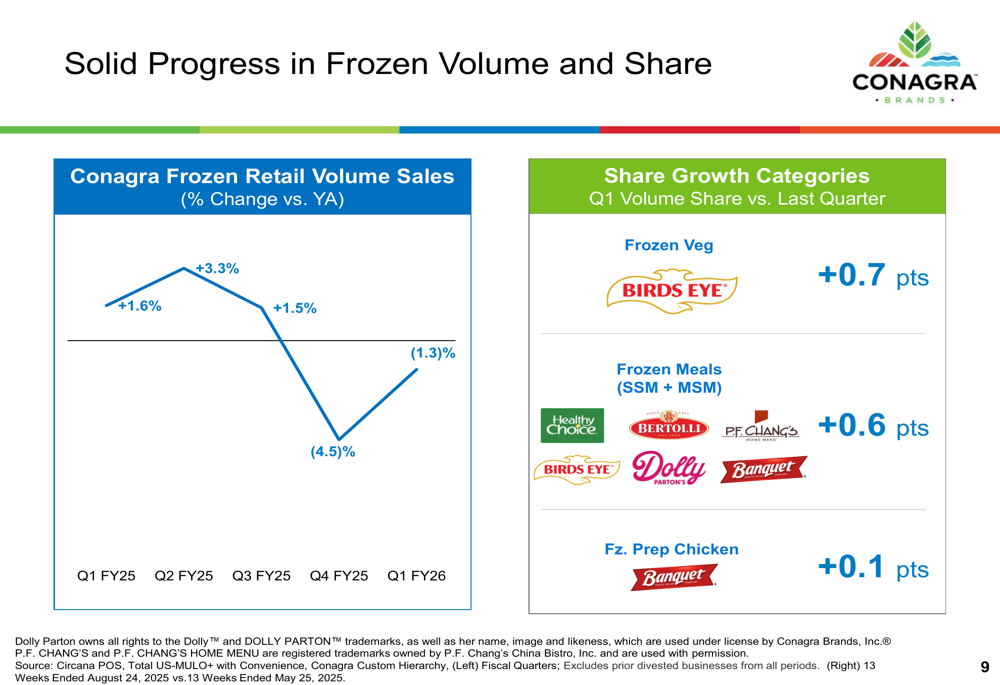

The frozen food segment, a key focus area for Conagra, showed particularly encouraging signs of recovery:

Frozen retail volume sales improved from -4.5% in Q4 FY25 to -1.3% in Q1 FY26. The company also gained market share in several important frozen categories, including frozen vegetables (+0.7 points), frozen meals (+0.6 points), and frozen prepared chicken (+0.1 points).

Detailed Financial Analysis

Conagra reported Q1 FY26 organic net sales of $2,611 million, representing a 0.6% decline compared to the previous year. The company’s adjusted operating margin was 11.8%, down 244 basis points year-over-year, while adjusted EPS came in at $0.39, a 26.4% decrease from Q1 FY25.

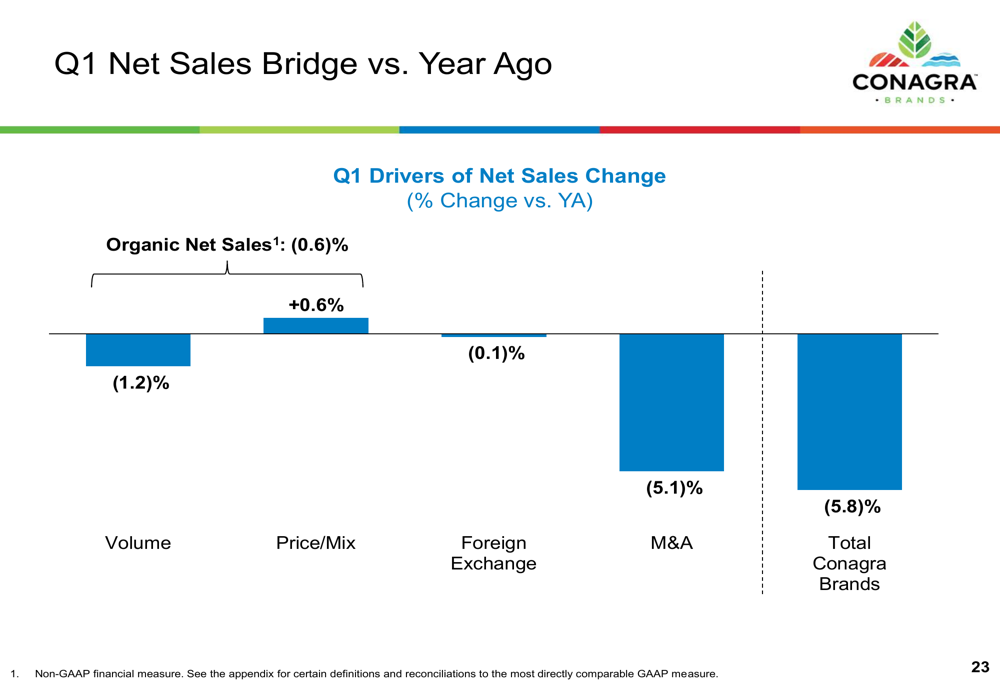

The following bridge chart breaks down the drivers of the net sales performance:

Volume declined 1.2%, partially offset by a 0.6% benefit from price/mix. Foreign exchange had a minimal negative impact of 0.1%, while divestitures (M&A) reduced sales by 5.1%, resulting in a total net sales decline of 5.8%.

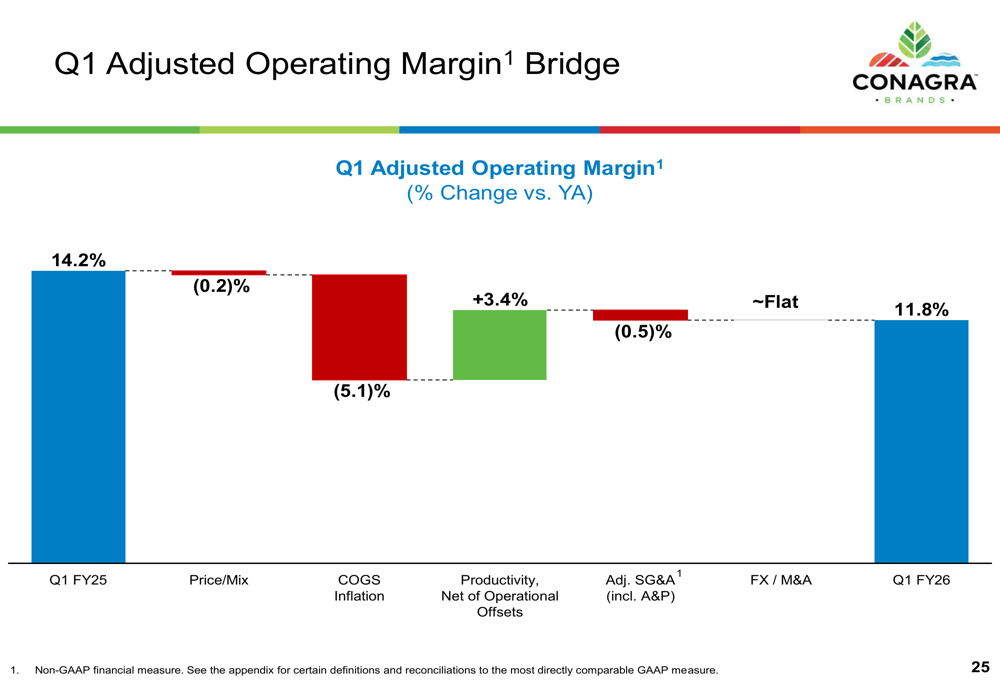

The adjusted operating margin was significantly impacted by inflation, as illustrated in this bridge chart:

Starting from 14.2% in Q1 FY25, the margin was negatively impacted by COGS inflation (-5.1 percentage points) and price/mix (-0.2 percentage points). These headwinds were partially offset by productivity gains of +3.4 percentage points, resulting in the Q1 FY26 adjusted operating margin of 11.8%.

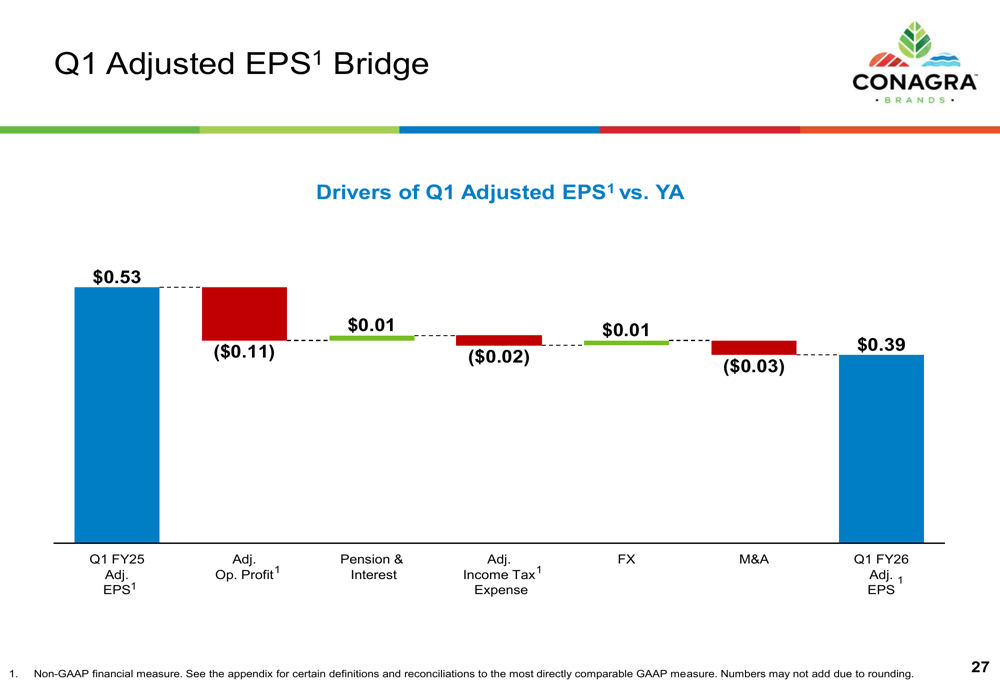

The decline in adjusted EPS can be attributed to several factors:

The $0.14 decrease from Q1 FY25’s $0.53 to Q1 FY26’s $0.39 was primarily driven by lower adjusted operating profit (-$0.11) and the impact of divestitures (-$0.03).

Strategic Initiatives

Conagra continued to execute on its portfolio optimization strategy, completing the divestitures of Chef Boyardee, Van de Kamp’s, and Mrs. Paul’s brands during the quarter. The proceeds from these transactions contributed to a reduction in net debt from $8.0 billion in Q4 FY25 to $7.6 billion in Q1 FY26.

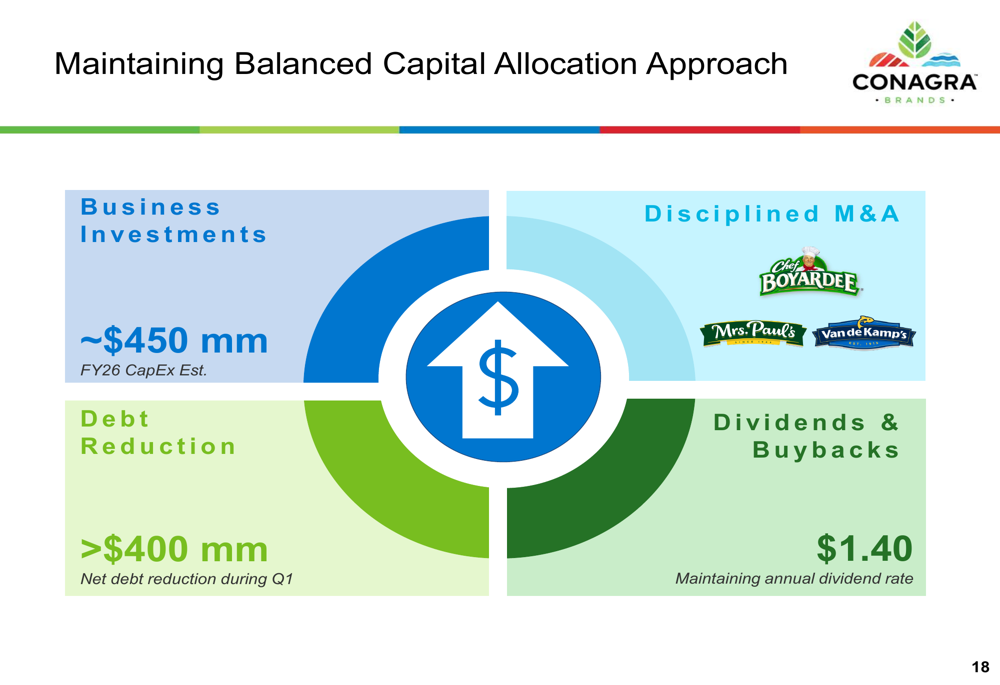

The company maintains a balanced approach to capital allocation, as illustrated in this diagram:

This approach includes business investments (approximately $450 million in FY26 capital expenditures), debt reduction (over $400 million in Q1), disciplined M&A (as evidenced by the completed divestitures), and maintaining the annual dividend rate of $1.40 per share.

Conagra’s supply chain delivered strong performance in the quarter, with service levels reaching 98% and productivity exceeding 5% of cost of goods sold. This operational excellence is crucial as the company works to offset inflationary pressures.

Forward-Looking Statements

Despite the challenging environment, Conagra reaffirmed its fiscal 2026 guidance:

- Organic net sales growth of -1% to +1% versus FY25

- Adjusted operating margin of approximately 11.0% to 11.5%

- Adjusted EPS of $1.70 to $1.85 (53-week fiscal year)

The company expects Q2 organic net sales to be down low single digits, with adjusted operating margin moderately below the full-year guidance range. For the second half of the fiscal year, Conagra anticipates organic net sales growth driven by the wrap of supply constraints and pricing actions, net of elasticity impacts.

Inflation remains a significant headwind, with total inflation now expected in the low 7% range, slightly higher than previous expectations due primarily to proteins. The company plans to offset these pressures through productivity improvements, including tariff mitigation efforts.

Conagra’s priorities for FY26 include growing frozen and snacks categories, increasing investment in supply chain resiliency, implementing targeted pricing, and actively managing for strong productivity and cash flow. These initiatives are designed to position the company for sustainable growth in a challenging consumer environment.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.