Moody’s downgrades Senegal to Caa1 amid rising debt concerns

Introduction & Market Context

Concentra Group Holdings Parent Inc (NYSE:CON), the largest provider of occupational health services in the United States, reported strong second-quarter 2025 results on August 7, with revenue growth accelerating and guidance raised for the full year. The company’s stock responded positively, rising 4.16% to close at $20.20 following the presentation.

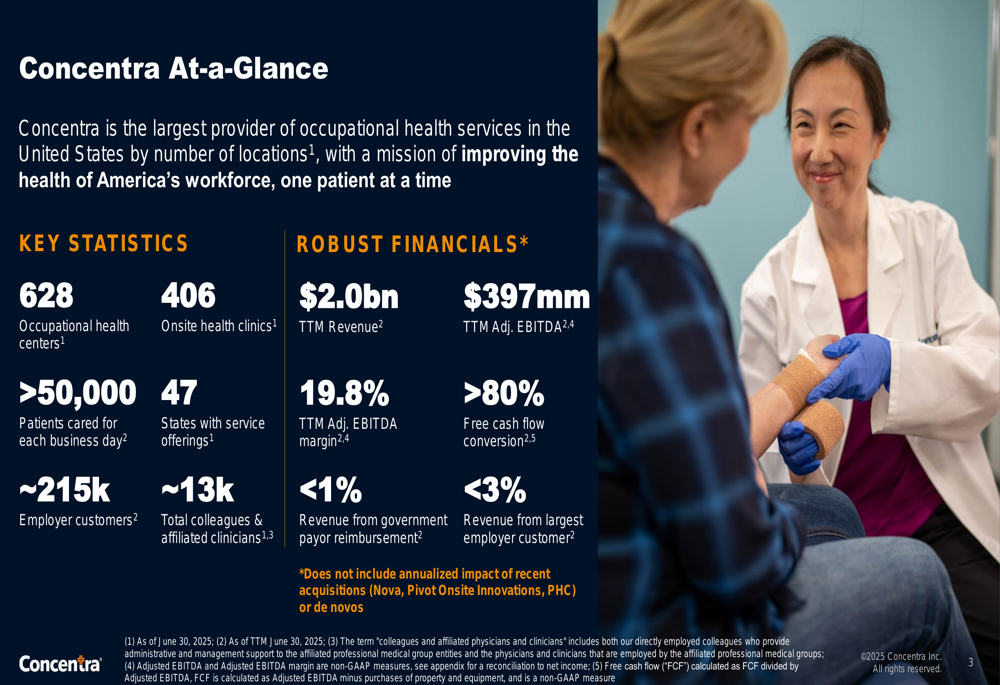

Concentra’s business model remains highly diversified with minimal exposure to government reimbursement, positioning it as what management describes as a "B2B business services provider and a differentiated investment opportunity." The company now operates 628 occupational health centers and 406 onsite health clinics across 47 states, serving approximately 215,000 employer customers.

As shown in the following comprehensive overview of Concentra’s scale and operations:

Quarterly Performance Highlights

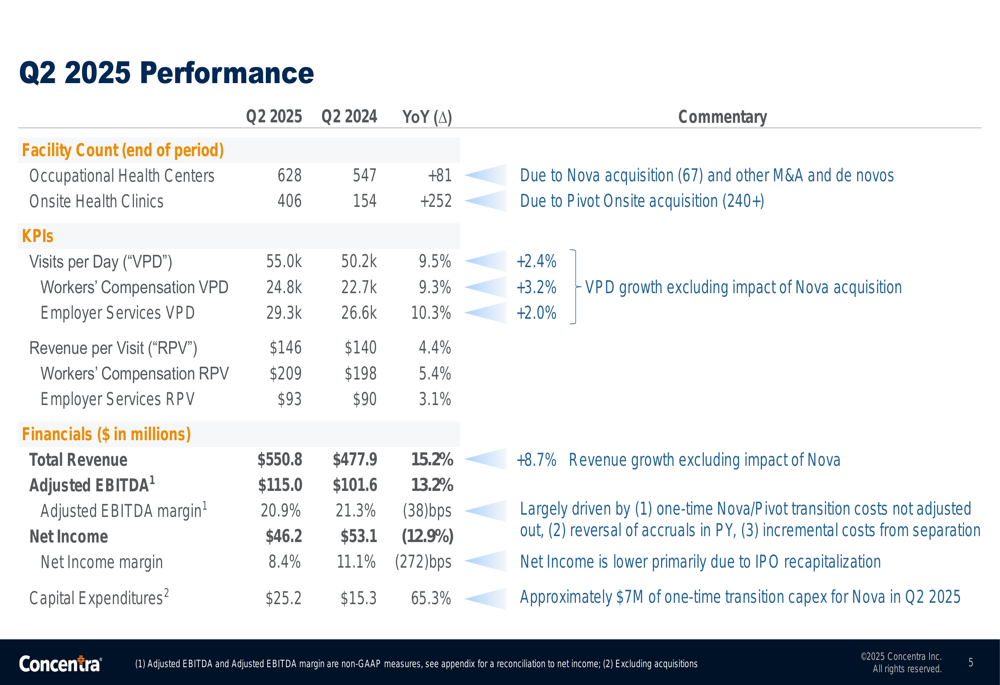

Concentra delivered robust financial results for Q2 2025, with revenue increasing 15.2% year-over-year to $550.8 million. This growth was driven by both acquisitions and organic expansion, with volume growth accelerating in the quarter. The company’s adjusted EBITDA rose 13.2% to $115 million, resulting in a 20.9% adjusted EBITDA margin.

Patient volumes showed significant improvement, with daily visits increasing 9.5% to 55,000. Revenue per visit also grew 4.4% to $146, demonstrating Concentra’s pricing power. However, net income declined 12.9% to $46.2 million, reflecting integration costs and higher expenses associated with the company’s expansion strategy.

The detailed quarterly performance metrics are illustrated in the following slide:

Workers’ compensation services, which typically generate higher revenue per visit ($209 compared to $93 for employer services), saw visits increase 9.3% year-over-year. Meanwhile, employer services visits grew 10.3%, marking the second consecutive quarter of positive growth in this segment.

Strategic Initiatives & Expansion

A key highlight of Concentra’s Q2 presentation was the company’s achievement of surpassing 1,000 total locations for the first time in its history. This milestone was reached through the successful integration of all 67 Nova occupational health centers and the acquisition of Pivot Onsite Innovations, which significantly expanded the company’s onsite clinic footprint.

The company’s progress on its strategic initiatives is outlined in the following slide:

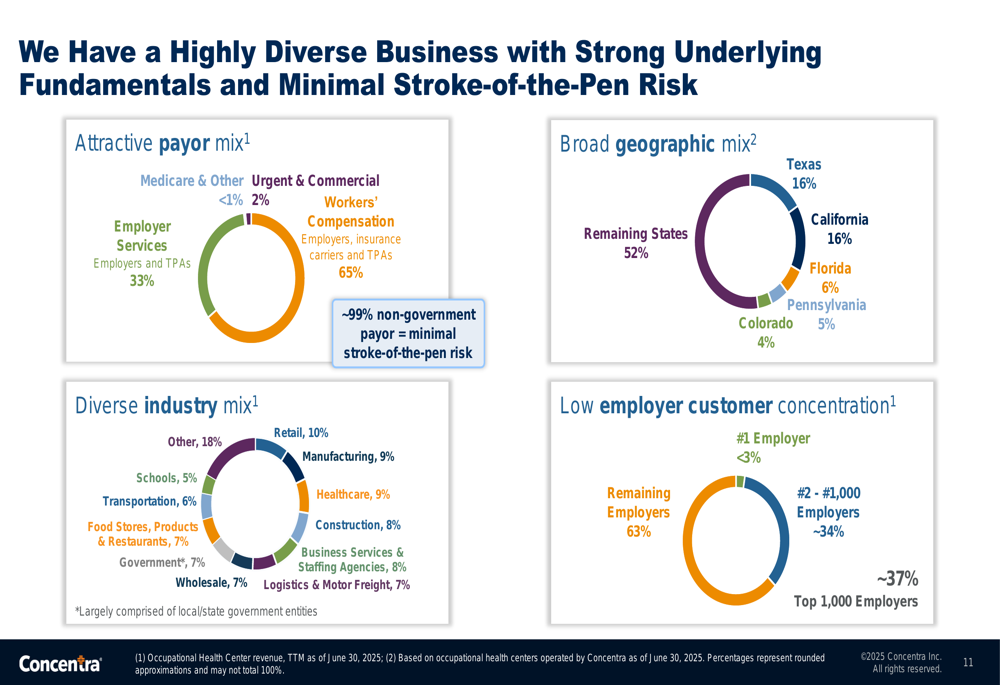

Concentra’s diversified business model minimizes regulatory and reimbursement risks, with less than 1% of revenue coming from government payors. The company maintains a broad geographic footprint and serves a diverse range of industries, with no single employer customer accounting for more than 3% of total revenue.

As illustrated in this breakdown of Concentra’s diversified business:

The company continues to expand organically as well, opening one de novo location in Q2 with plans to open 2-3 more by the end of the year. Capital expenditures increased 65.3% year-over-year to $25.2 million in Q2, reflecting these growth investments.

Balance Sheet & Capital Allocation

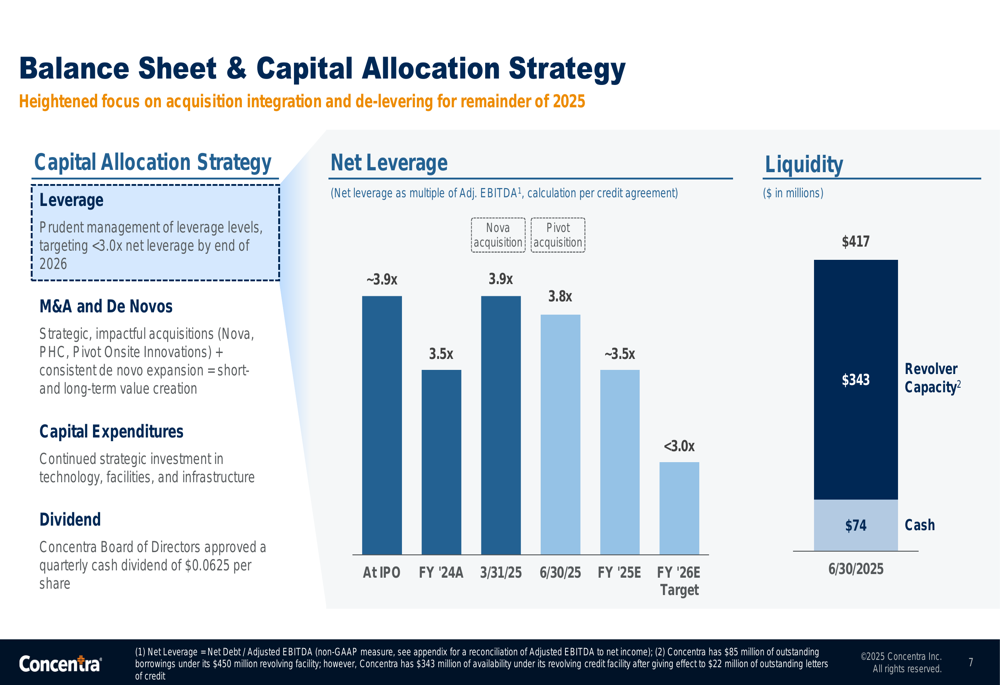

Concentra has prioritized deleveraging while maintaining its dividend and growth initiatives. The company reduced its net leverage ratio to 3.8x in Q2, down from 3.9x at the end of fiscal 2024, and is targeting a ratio below 3.0x by the end of 2026.

As of June 30, 2025, Concentra maintained $417 million in total liquidity, including $74 million in cash and $343 million in available revolving credit facility capacity. The company’s balance sheet and deleveraging progress are shown in the following slide:

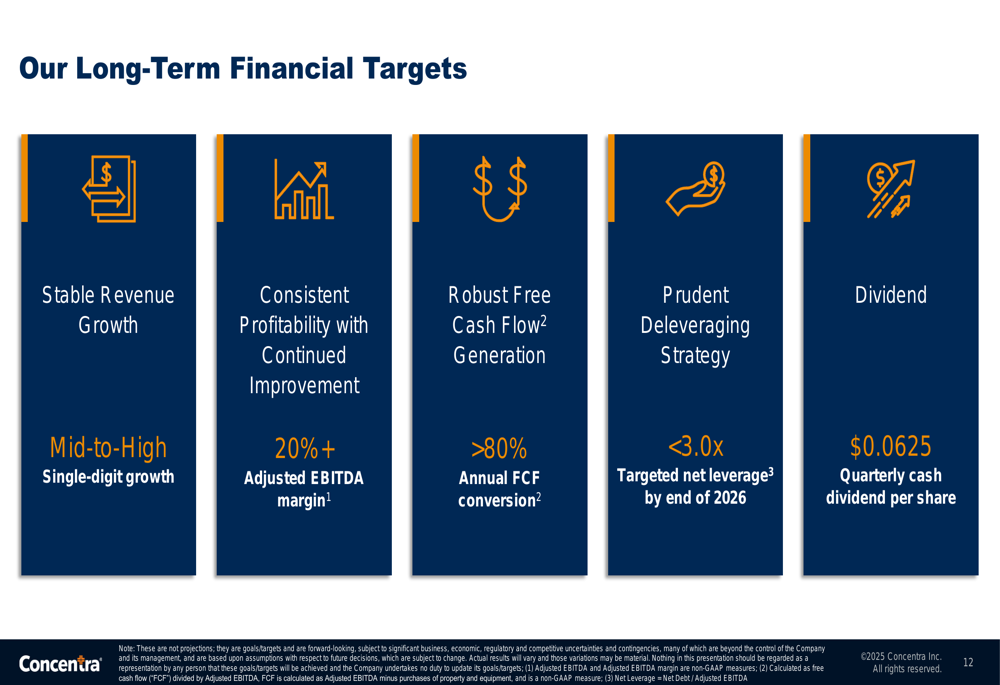

Concentra maintained its quarterly dividend of $0.0625 per share, balancing shareholder returns with its deleveraging goals. The company’s long-term financial targets include mid-to-high single-digit revenue growth, 20%+ adjusted EBITDA margins, and greater than 80% free cash flow conversion.

Forward-Looking Statements & Guidance

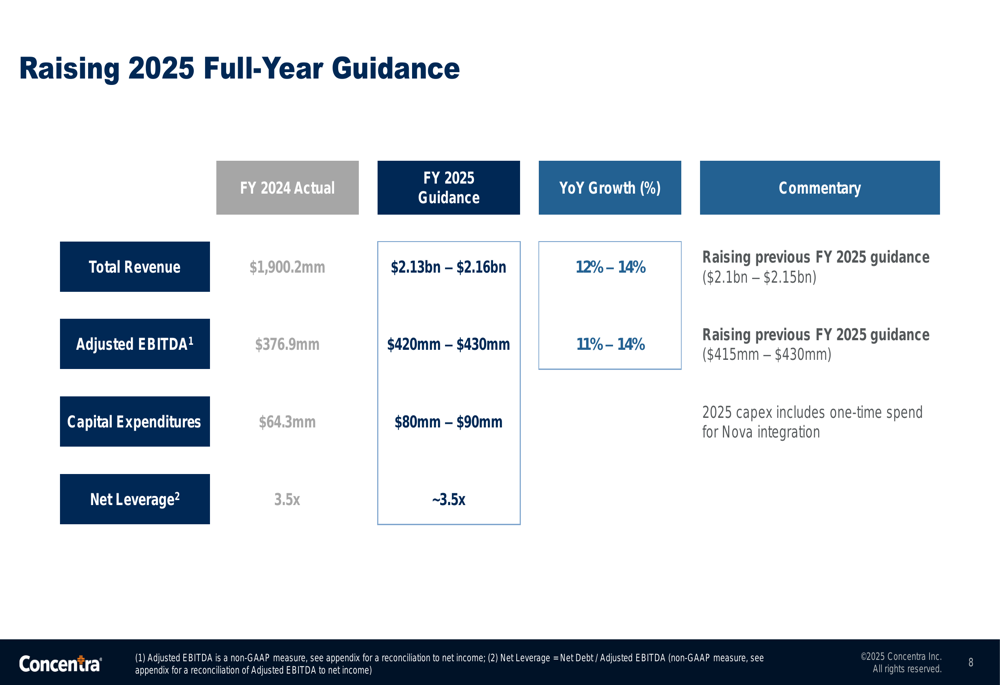

Following the strong Q2 performance, Concentra raised its full-year 2025 guidance. The company now expects revenue of $2.13 billion to $2.16 billion, representing 12-14% year-over-year growth. Adjusted EBITDA guidance was increased to $420 million to $430 million, reflecting 11-14% growth from 2024.

The updated guidance is detailed in the following slide:

Capital expenditures for 2025 are projected to be $80-90 million, supporting continued organic growth. The company expects its net leverage ratio to improve to approximately 3.5x by the end of 2025, in line with its deleveraging strategy.

During the earnings call, CEO Keith Newton expressed confidence in the business environment, stating, "We’re not seeing any indication of slowdown," underscoring the stable demand for Concentra’s occupational health services. The company’s long-term financial targets remain focused on sustainable growth, consistent profitability improvement, and robust free cash flow generation.

With its stock trading at a P/E ratio of 15.1x and currently near the lower end of its 52-week range ($18.89-$24.81), Concentra’s raised guidance and strategic positioning have analysts maintaining a strong buy consensus with price targets ranging from $25 to $30, suggesting potential upside from current levels.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.