Gold is 2025’s best performer. UBS sees more upside

Introduction & Market Context

Concrete Pumping Holdings (NASDAQ:BBCP) presented its Q2 2025 investor slides on June 5, 2025, highlighting the company’s position as the largest concrete pumping service provider in both the U.S. and U.K. markets. The presentation comes at a time when the construction industry faces mixed conditions, with infrastructure spending showing strength while commercial construction exhibits signs of softness.

The company operates in a $1.85 billion U.S. concrete pumping market, where it maintains a dominant position approximately six times larger than its nearest competitor. BBCP’s stock closed at $7.10 on June 5, 2025, showing a slight decline of 0.14% in the most recent trading session.

Executive Summary

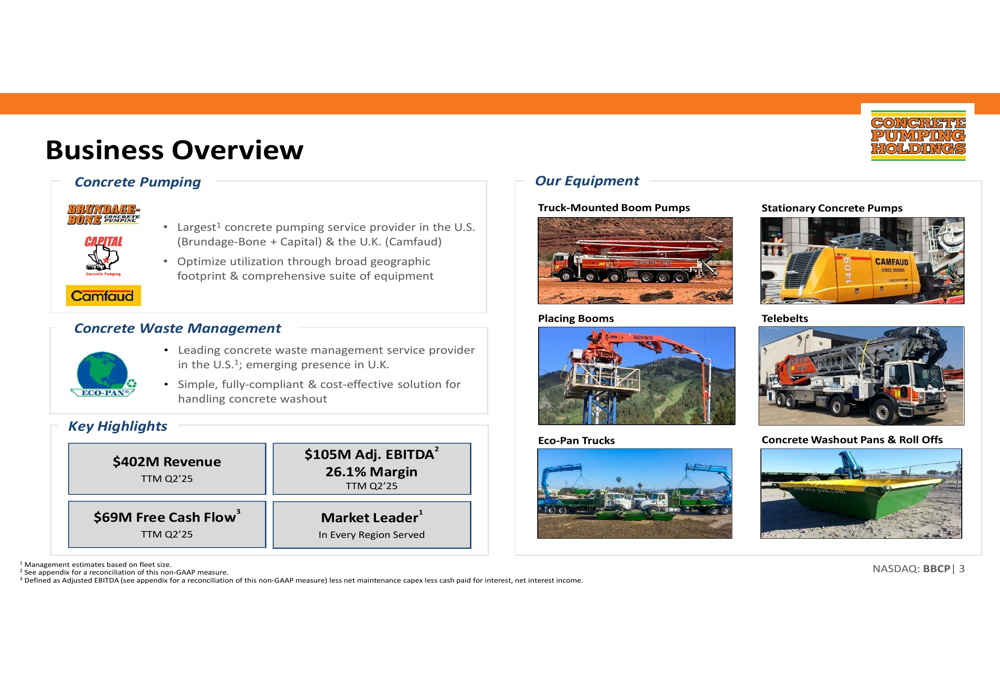

Concrete Pumping Holdings reported trailing twelve months (TTM) Q2 2025 revenue of $402 million with adjusted EBITDA of $105 million, representing a 26.1% margin. Free cash flow for the same period reached $69 million. The company maintains a diversified business model across three segments: U.S. concrete pumping, U.K. concrete pumping (Camfaud), and concrete waste management services (Eco-Pan).

As shown in the following business overview slide, BBCP has established itself as a market leader in every region it serves:

Despite these strong TTM results, the company’s Q1 2025 earnings revealed challenges, with revenue declining 11.6% year-over-year to $86.4 million, though the net loss improved to $3.1 million from $4.3 million in the prior year. Management attributed approximately $5 million of the revenue decline to adverse weather conditions.

Quarterly Performance Highlights

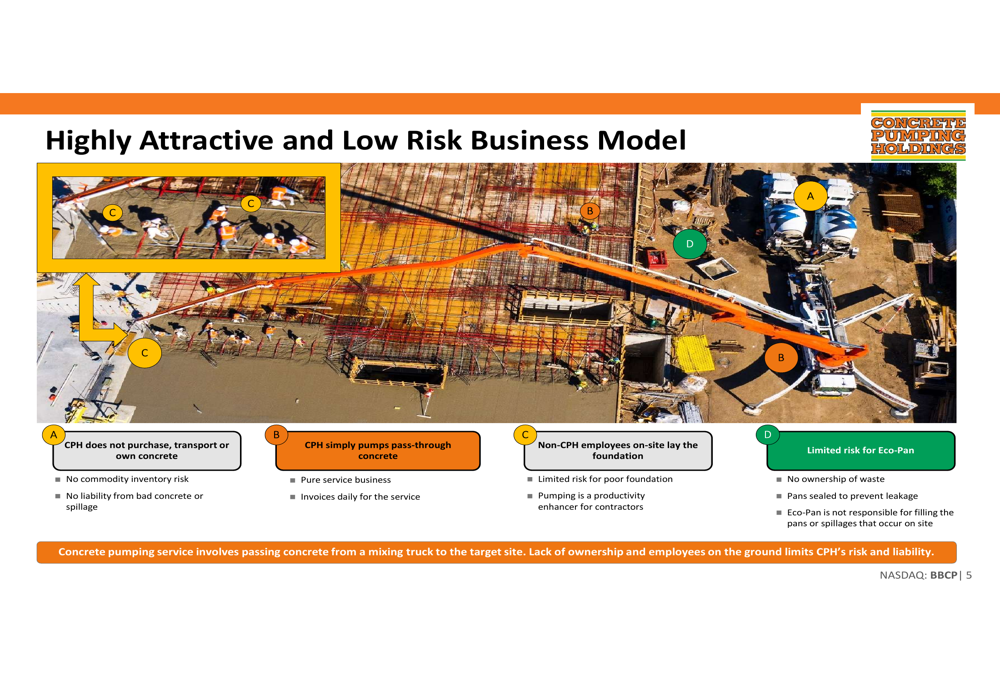

The company’s business model emphasizes its low-risk nature, with BBCP functioning purely as a service provider that doesn’t purchase, transport, or own concrete. This approach limits commodity inventory risk and liability exposure, as illustrated in this operational diagram:

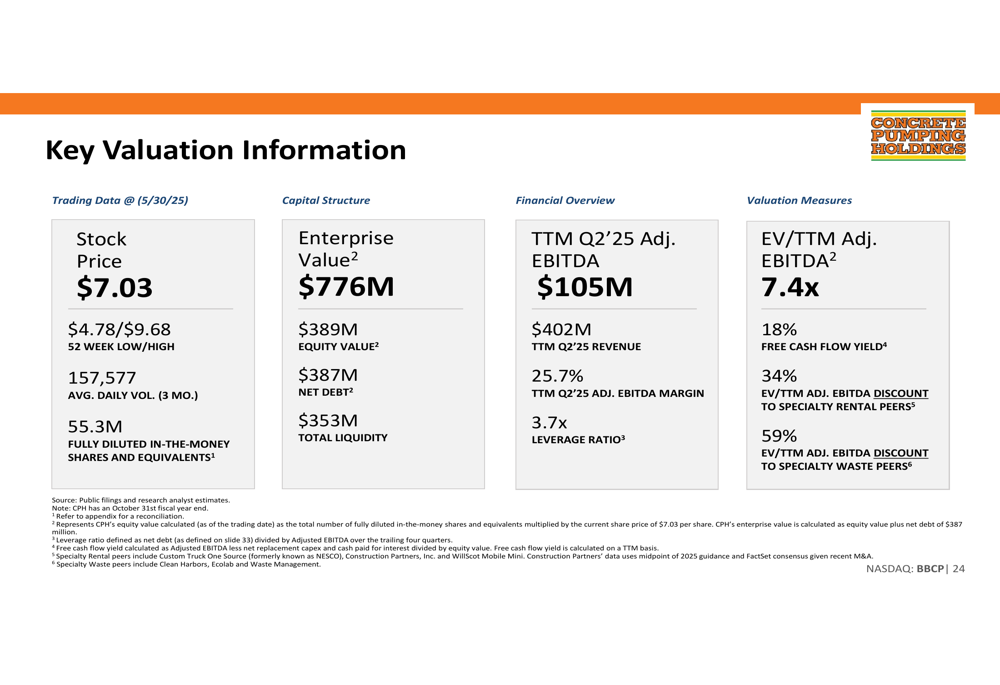

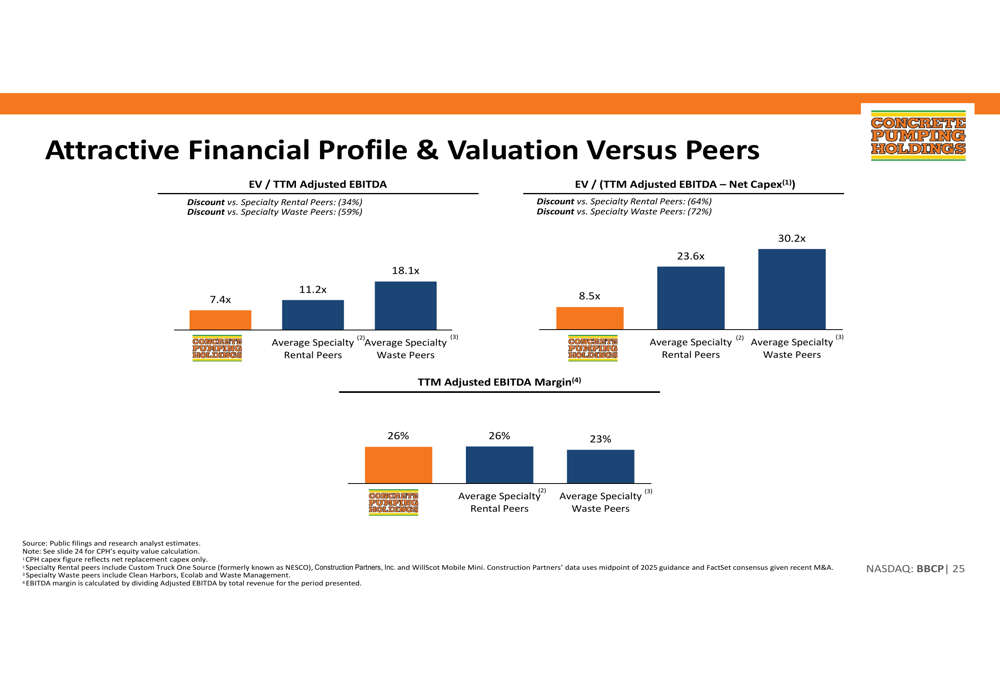

The Q2 2025 TTM financial metrics demonstrate the company’s ability to generate significant cash flow despite market challenges. With an enterprise value of $776 million and equity value of $389 million, BBCP trades at an EV/TTM Adjusted EBITDA multiple of 7.4x, representing a discount to both specialty rental and waste management peers.

The company’s key valuation metrics are summarized in the following slide:

This valuation appears attractive when compared to industry peers, as the company trades at a 34% discount to specialty rental peers and a 59% discount to waste management peers on an EV/TTM Adjusted EBITDA basis.

Strategic Initiatives

BBCP outlined a comprehensive growth strategy focused on five key areas: capturing greater market share, optimizing pricing and utilization, expanding its Eco-Pan waste management business, pursuing strategic acquisitions, and exploring greenfield opportunities.

The Eco-Pan segment represents a particularly promising growth avenue, with management identifying an $850+ million U.S. market opportunity and current penetration of only approximately 8%. This business has demonstrated strong performance with an 18% revenue CAGR from 2016 to 2024.

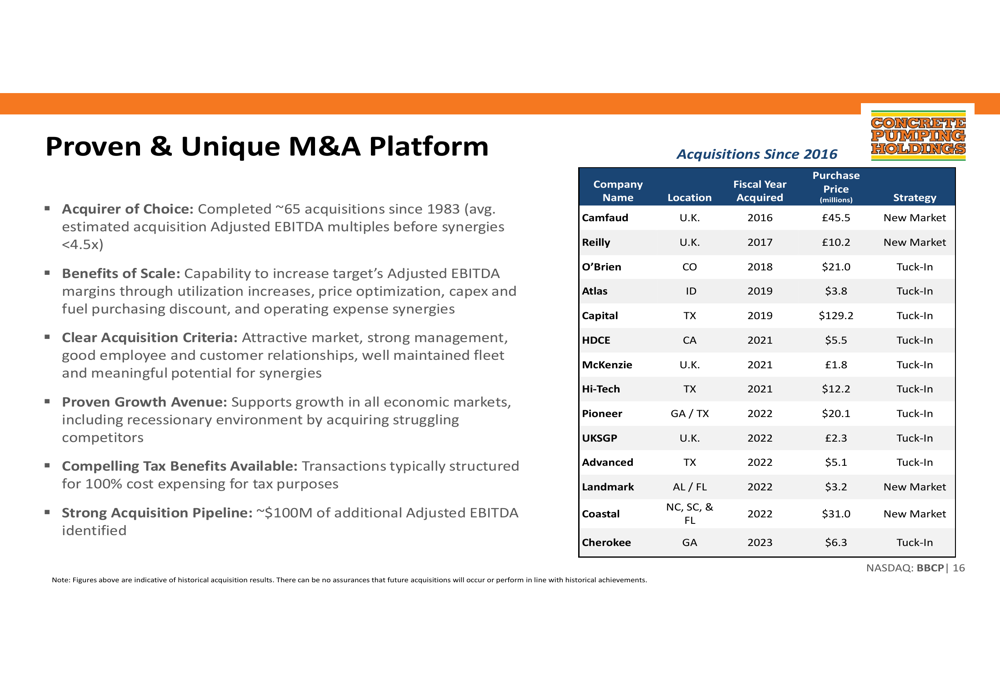

The company’s acquisition strategy has been a key driver of growth, with multiple successful transactions since 2016. Management emphasized that BBCP is positioned as an "acquirer of choice" with a strong pipeline of potential targets.

Forward-Looking Statements

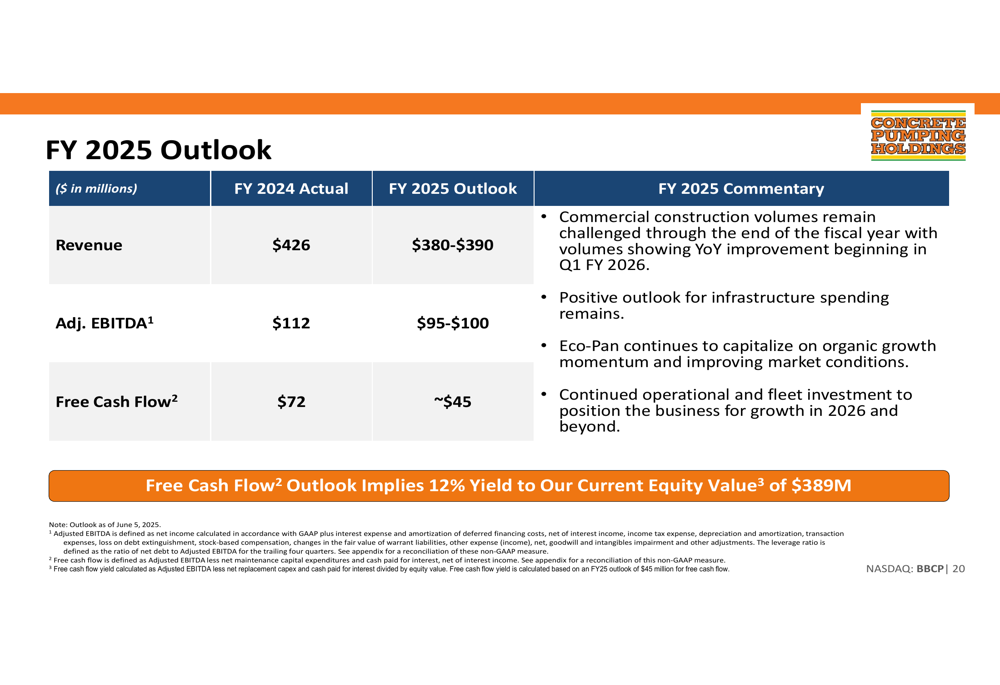

Despite strong TTM results, BBCP’s outlook for fiscal year 2025 reflects a more cautious stance, with projected revenue of $380-$390 million and adjusted EBITDA of $95-$100 million. This guidance suggests a potential decline from current TTM figures, likely reflecting the commercial construction softness mentioned in the Q1 earnings call.

The company’s FY 2025 outlook is detailed in the following slide:

During the Q1 2025 earnings call, CEO Bruce Young emphasized the company’s readiness for a commercial market recovery, stating, "We are well positioned for commercial market recovery." Management also indicated an increased focus on M&A opportunities compared to previous years, potentially as a strategy to offset organic growth challenges.

Competitive Industry Position

BBCP maintains an unrivaled geographic footprint across the U.S. and U.K., with approximately 90 U.S. concrete pumping locations, 35 U.K. concrete pumping locations, and 21 U.S. Eco-Pan locations. The company’s equipment fleet consists of approximately 1,010 units for U.S. concrete pumping, 390 for U.K. operations, and 140 for Eco-Pan.

This extensive network provides BBCP with significant competitive advantages, including purchasing benefits, breadth of services, higher fleet utilization, and the ability to deploy trained operators efficiently. The company competes primarily on customer service, fleet availability, and equipment breadth rather than price.

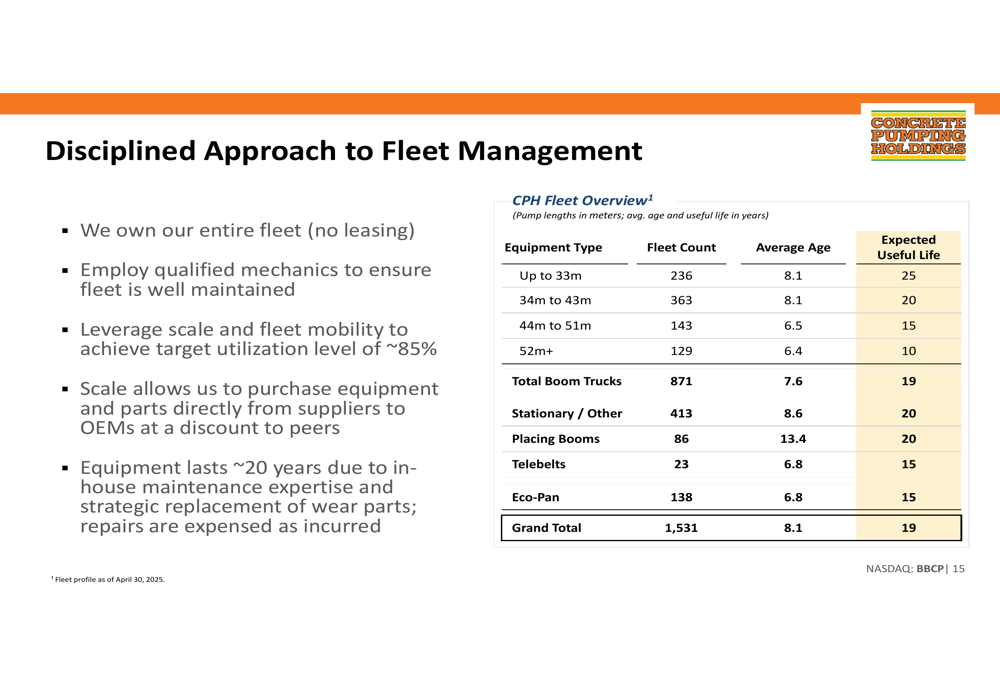

BBCP’s disciplined approach to fleet management is a key competitive differentiator, with the company owning its equipment and employing qualified mechanics to maintain it. This approach results in an extended equipment life of approximately 20 years, significantly longer than industry averages.

Detailed Financial Analysis

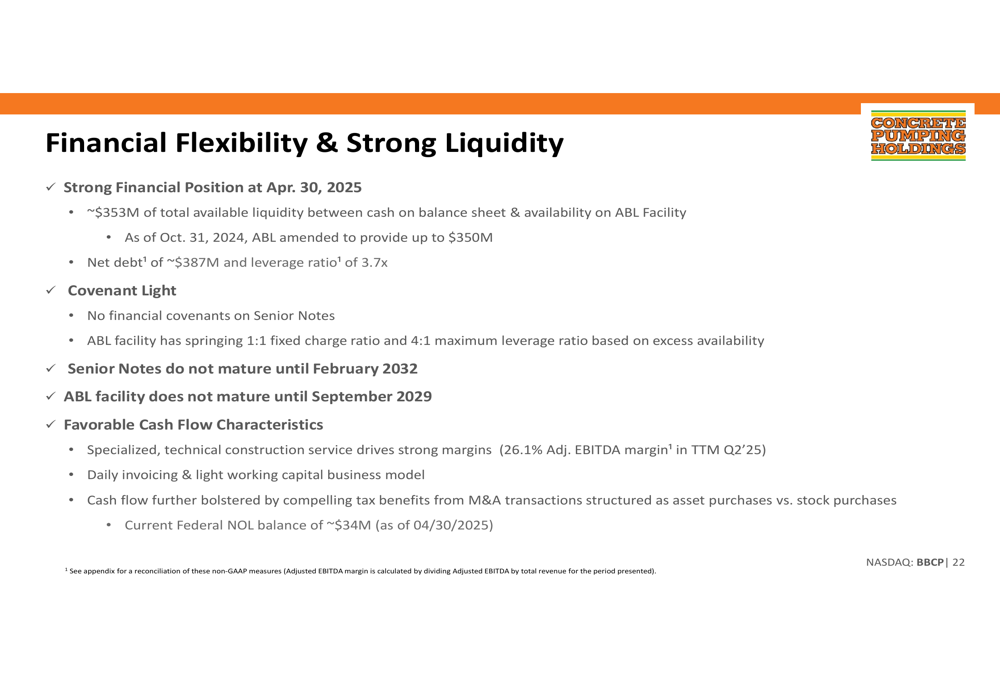

The company’s financial position shows a leverage ratio of 3.7x with net debt of approximately $387 million. BBCP has substantial liquidity with approximately $353 million available and a debt structure that includes no financial covenants. The company’s ABL facility doesn’t mature until September 2029, and Senior Notes don’t mature until February 2032.

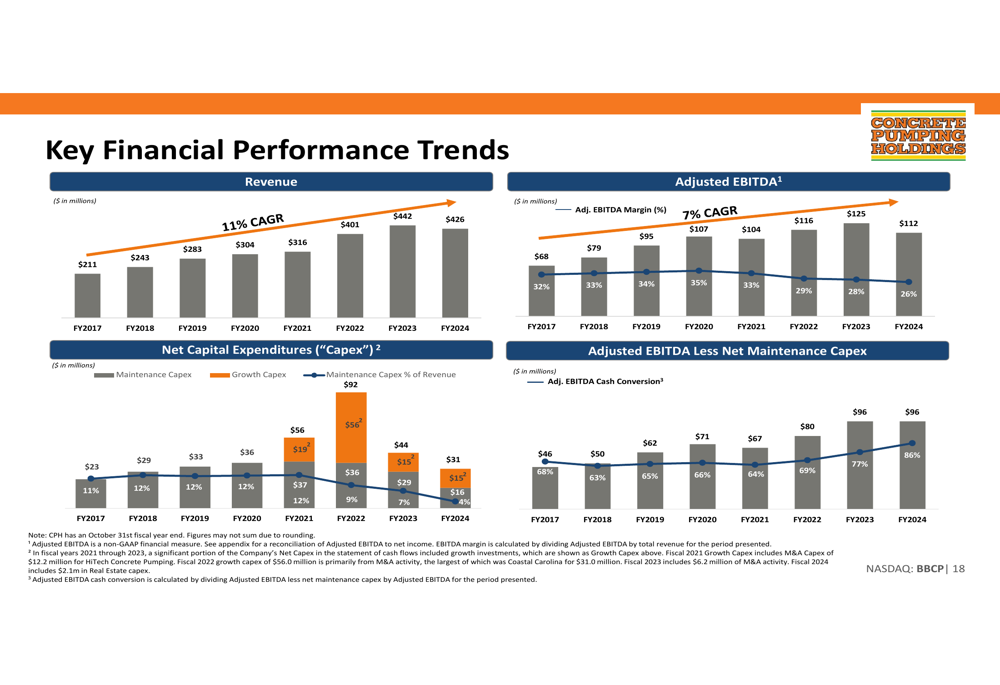

Historical financial performance shows a revenue CAGR of 11% and an adjusted EBITDA CAGR of 7% from FY2017 to FY2024. The company has maintained adjusted EBITDA margins ranging from 32% to 35% during this period.

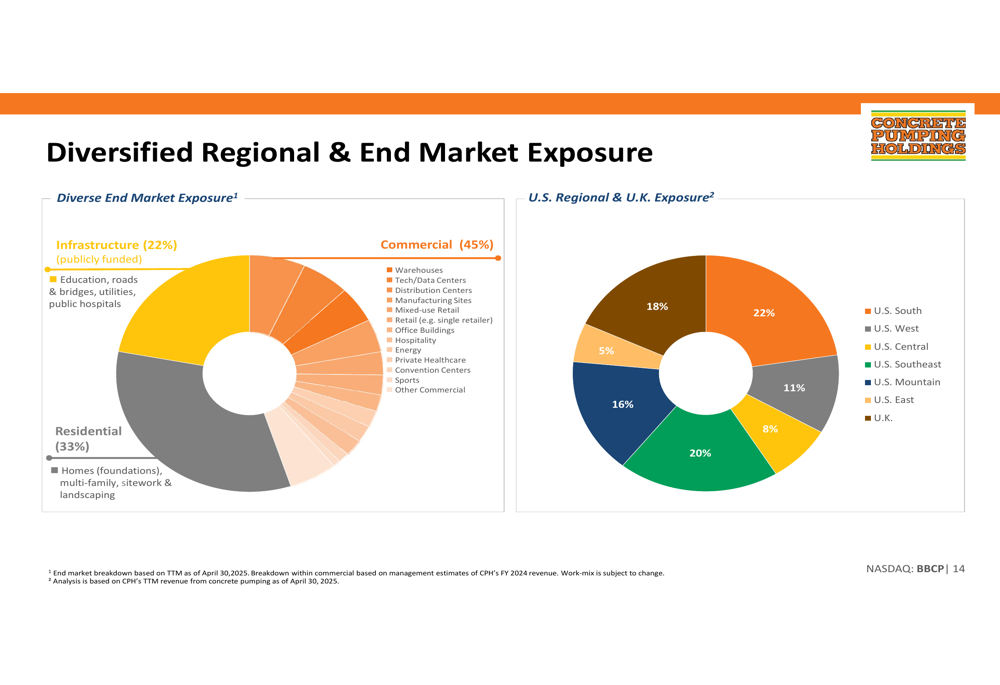

The company’s diversified exposure across end markets (Commercial 45%, Residential 33%, Infrastructure 22%) and regions provides some insulation against sector-specific downturns. This diversification strategy has helped BBCP navigate the current softness in commercial construction while capitalizing on infrastructure spending growth.

In conclusion, Concrete Pumping Holdings’ Q2 2025 presentation depicts a company with strong market leadership and solid TTM financial performance, but facing near-term headwinds in commercial construction. Management’s cautious FY 2025 outlook reflects these challenges, though the company’s diversified business model, acquisition strategy, and Eco-Pan growth opportunity provide multiple avenues for long-term value creation. With valuation metrics suggesting a discount to peers, investors may find BBCP’s risk-reward profile attractive despite the current market uncertainties.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.