Asahi shares mark weekly slide after cyberattack halts production

Introduction & Market Context

Concrete Pumping Holdings (NASDAQ:BBCP) released its Q3 2025 investor presentation on September 4, 2025, revealing how the market leader in concrete pumping services is navigating current construction market challenges while maintaining solid profitability margins. The company’s stock closed at $6.77, up 0.59% on the day, but remains closer to its 52-week low of $4.47 than its high of $8.60.

The presentation comes amid a challenging period for commercial construction, with BBCP’s Q2 2025 earnings showing a net loss of $0.01 per share on revenue of $94 million, missing analyst expectations. Despite these headwinds, the company emphasized its market leadership position and diversified business model as key strengths.

Executive Summary

Concrete Pumping Holdings maintains its position as the largest concrete pumping service provider in both the U.S. and U.K. markets, with a complementary and growing concrete waste management business through its Eco-Pan segment. The company reported trailing twelve months (TTM) Q3 2025 revenue of $396 million and adjusted EBITDA of $100 million, representing a 25.3% margin.

As shown in the following business overview, BBCP operates across multiple segments with strong market positions:

The company’s business model focuses on providing specialized concrete pumping services without taking ownership of the concrete itself, limiting commodity and construction risks. This service-oriented approach has helped BBCP maintain stronger margins than many construction-related businesses despite current market pressures.

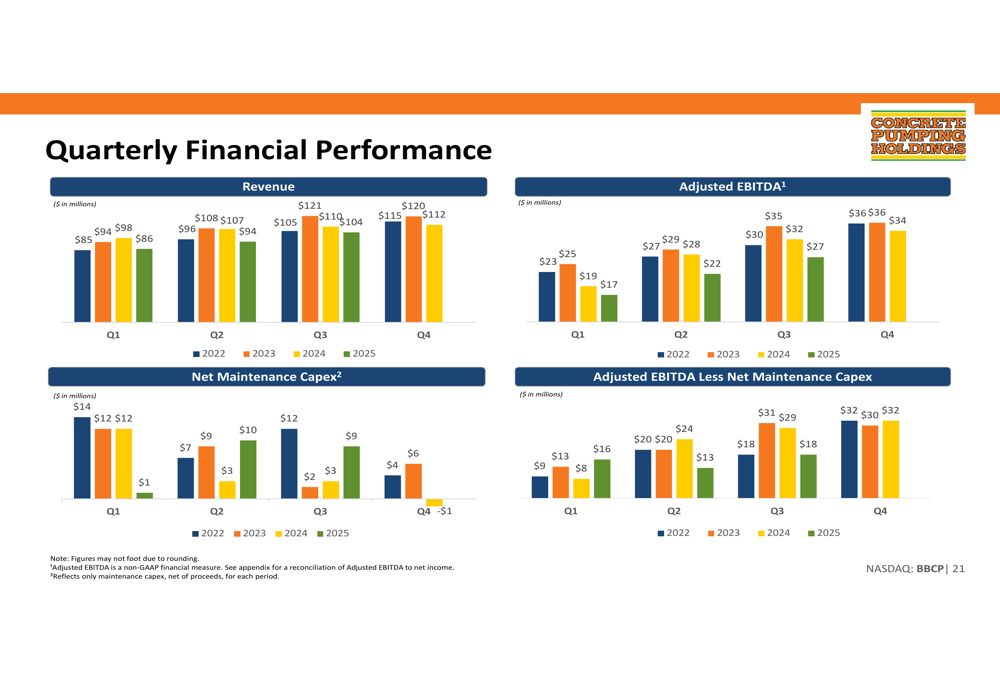

Quarterly Performance Highlights

BBCP’s quarterly performance has shown signs of pressure in recent periods. The Q2 2025 earnings revealed a revenue decline to $94 million from $107.1 million in the prior year, with adjusted EBITDA falling to $22.5 million from $27.5 million. This represents a decrease in adjusted EBITDA margin from 25.7% to 23.9%.

The following chart illustrates the company’s quarterly financial performance trends:

The U.S. Concrete Pumping segment has been most affected by the slowdown, with Q2 2025 revenue dropping to $62.1 million from $74.6 million year-over-year. However, the U.S. Concrete Waste Management segment (Eco-Pan) showed resilience with a 7% revenue increase, highlighting the value of the company’s diversified business model.

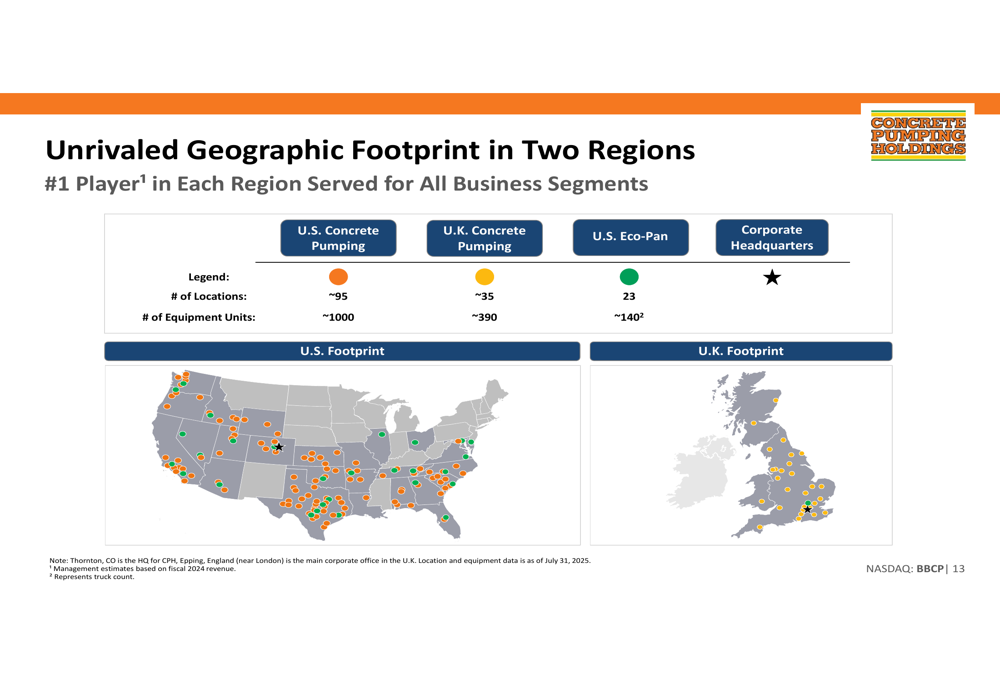

Strategic Positioning and Growth Initiatives

Despite current challenges, BBCP maintains a strong strategic position with significant geographic coverage across the U.S. and U.K. The company’s footprint includes approximately 95 locations for U.S. concrete pumping, 35 locations for U.K. operations, and 23 locations for its Eco-Pan waste management business.

The following map illustrates the company’s extensive geographic presence:

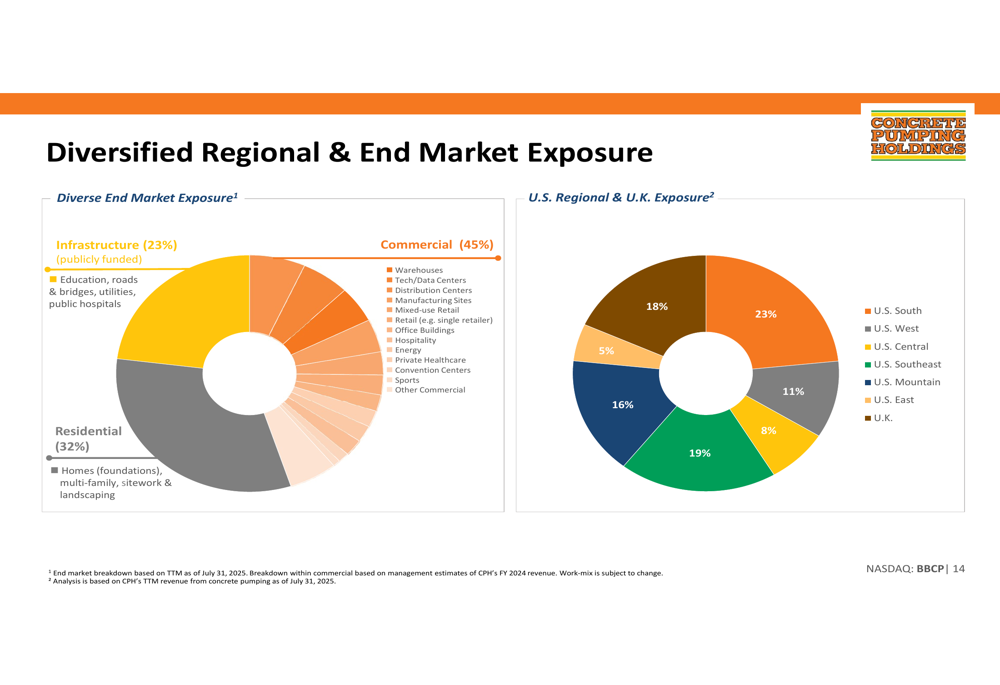

A key strength of BBCP’s business model is its diversification across both geographic regions and end markets. The company serves commercial (45%), residential (32%), and infrastructure (23%) construction projects, providing some insulation from sector-specific downturns.

As shown in the following breakdown of regional and end market exposure:

The company’s Eco-Pan concrete waste management solution represents a particularly promising growth avenue. With only $71 million in revenue (17% of FY 2024 total), but an estimated total U.S. market opportunity of $850+ million, this segment has substantial room for expansion.

The following chart highlights Eco-Pan’s growth trajectory and market opportunity:

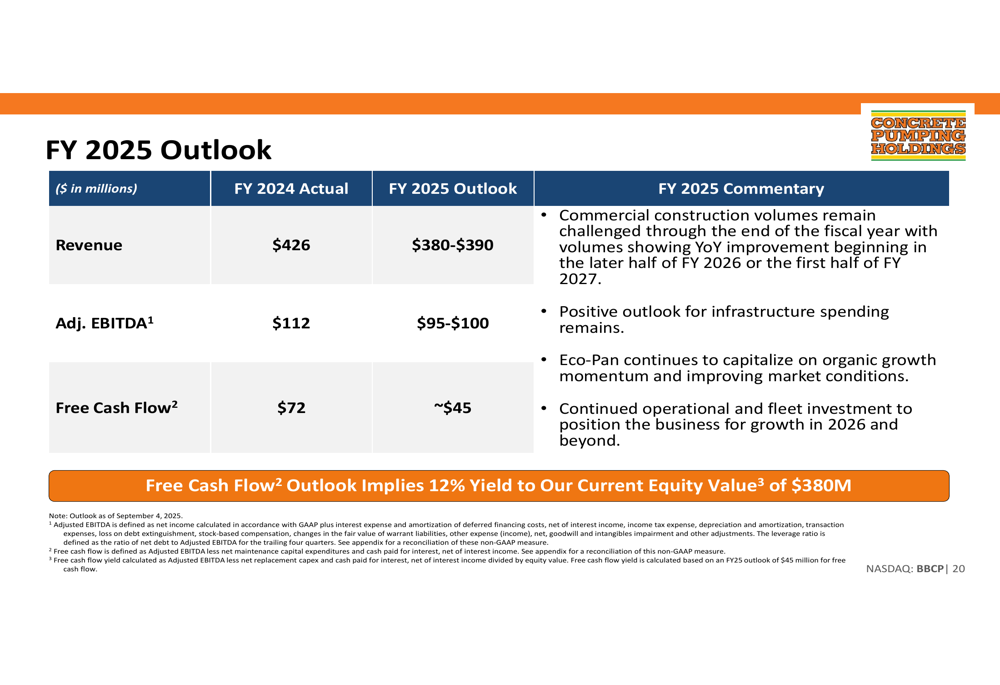

Financial Outlook and Valuation

For FY 2025, BBCP projects revenue between $380-$390 million and adjusted EBITDA of $95-$100 million, representing declines from FY 2024 levels of $426 million and $112 million, respectively. Free cash flow is expected to be approximately $45 million, down from $72 million in FY 2024.

The company’s FY 2025 outlook is summarized in the following slide:

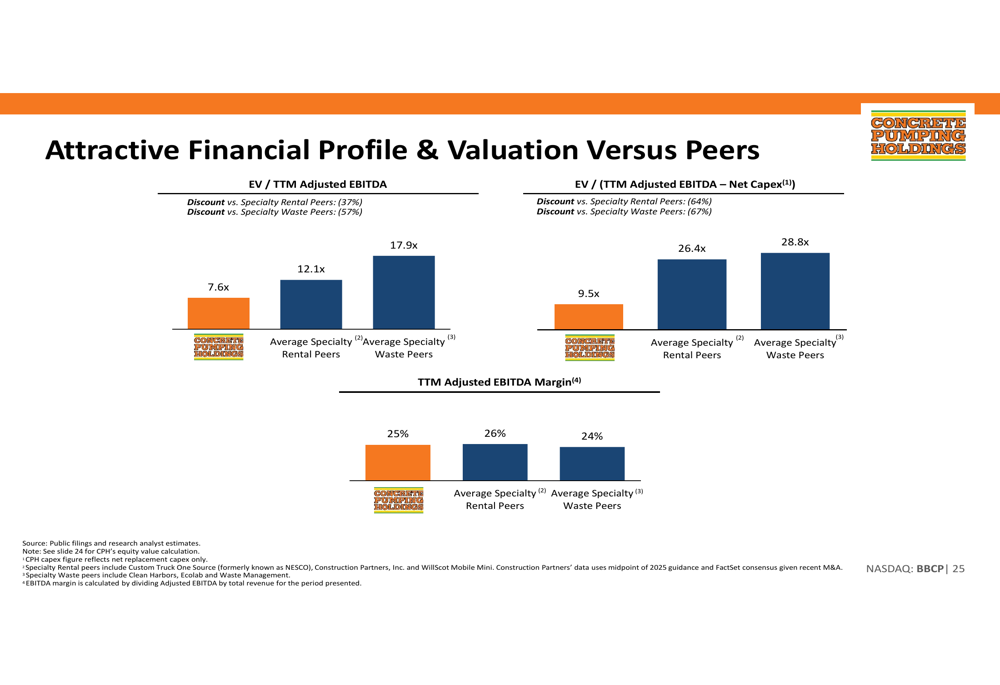

Despite near-term challenges, BBCP highlights its attractive valuation relative to peers. The company trades at 7.6x EV/TTM Adjusted EBITDA, representing a 37% discount to specialty rental peers and a 57% discount to specialty waste peers, while maintaining comparable EBITDA margins.

The following comparison illustrates BBCP’s valuation versus peers:

Fleet Management and Capital Allocation

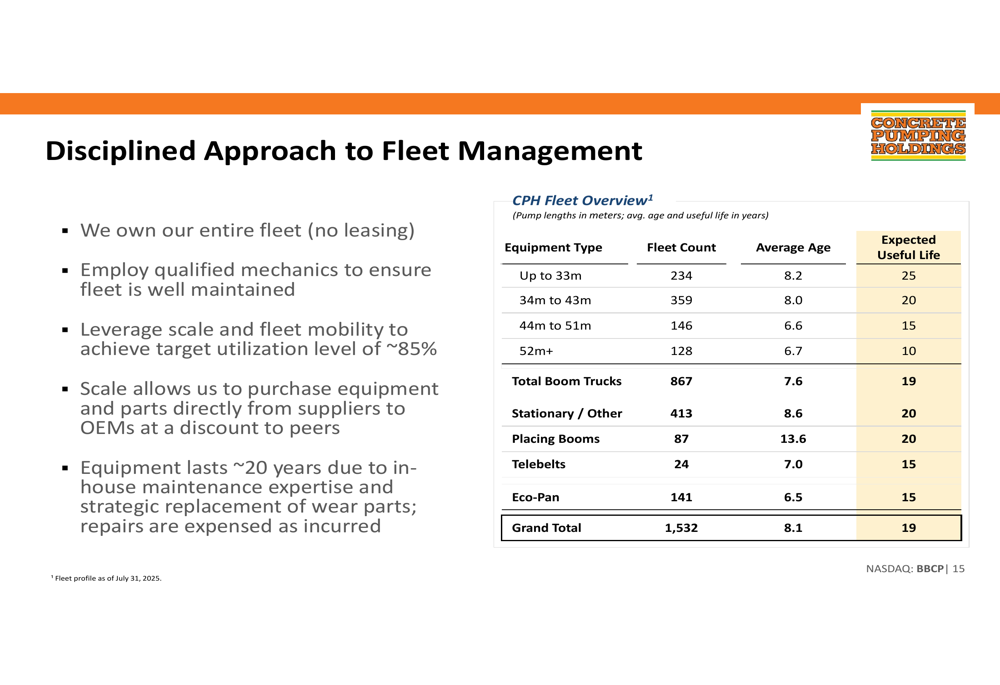

A core strength of BBCP’s business model is its disciplined approach to fleet management. The company owns its entire fleet of approximately 1,532 pieces of equipment with an average age of 8.1 years against an expected useful life of 19 years. This ownership approach, combined with in-house maintenance expertise, allows BBCP to optimize utilization and control costs.

The company’s fleet composition and management strategy are detailed below:

BBCP maintains a prudent approach to capital allocation, with priorities including fleet investment, Eco-Pan growth, strategic M&A, and potential shareholder returns. The company has a strong acquisition track record, having completed approximately 65 acquisitions since 1983 at average estimated EBITDA multiples below 4.5x before synergies.

Challenges and Forward-Looking Statements

While BBCP emphasizes its market leadership and financial flexibility, the company faces several challenges. Commercial construction volumes remain under pressure, with management not expecting significant improvement until late FY 2026 or early FY 2027. Higher interest rates continue to delay project starts, particularly in the commercial sector.

The company’s net debt stands at approximately $384 million with a leverage ratio of 3.8x, which represents a moderate level of financial leverage. However, BBCP highlights its strong liquidity position of $358 million between cash and ABL facility availability, as well as the absence of near-term debt maturities.

During the Q2 2025 earnings call, CEO Bruce Young expressed confidence in the company’s resilient business model and anticipated commercial market recovery following potential interest rate reductions. CFO Ian Humphries emphasized the company’s commitment to prudent capital allocation and flexible investment strategies amid challenging macroeconomic conditions.

With infrastructure spending expected to provide ongoing support and the high-growth potential of the Eco-Pan segment, BBCP is positioning itself to weather current market challenges while preparing for future growth opportunities when construction markets improve.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.