Aspire Biopharma faces potential Nasdaq delisting after compliance shortfall

Introduction & Market Context

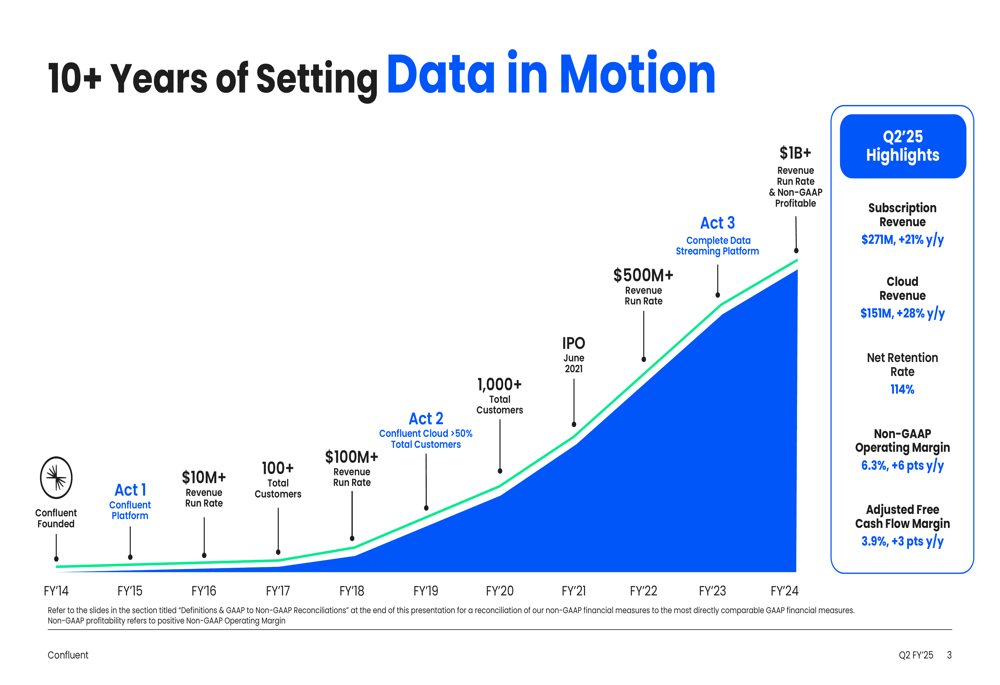

Confluent Inc (NASDAQ:CFLT) presented its Q2 2025 investor slides on July 30, 2025, highlighting strong cloud revenue growth and margin improvements as the company continues to position itself as a central hub for enterprise data streaming. The data streaming specialist, founded by the creators of Apache Kafka, is targeting a total addressable market that has grown from approximately $50 billion in 2021 to over $100 billion in 2025.

Despite the positive performance metrics, Confluent’s stock closed at $23.18 on the day of the presentation, marking a 1.8% decline, with after-hours trading showing a further 2.15% drop to $22.68. This market reaction suggests investors may have had higher expectations or concerns about future growth rates.

Quarterly Performance Highlights

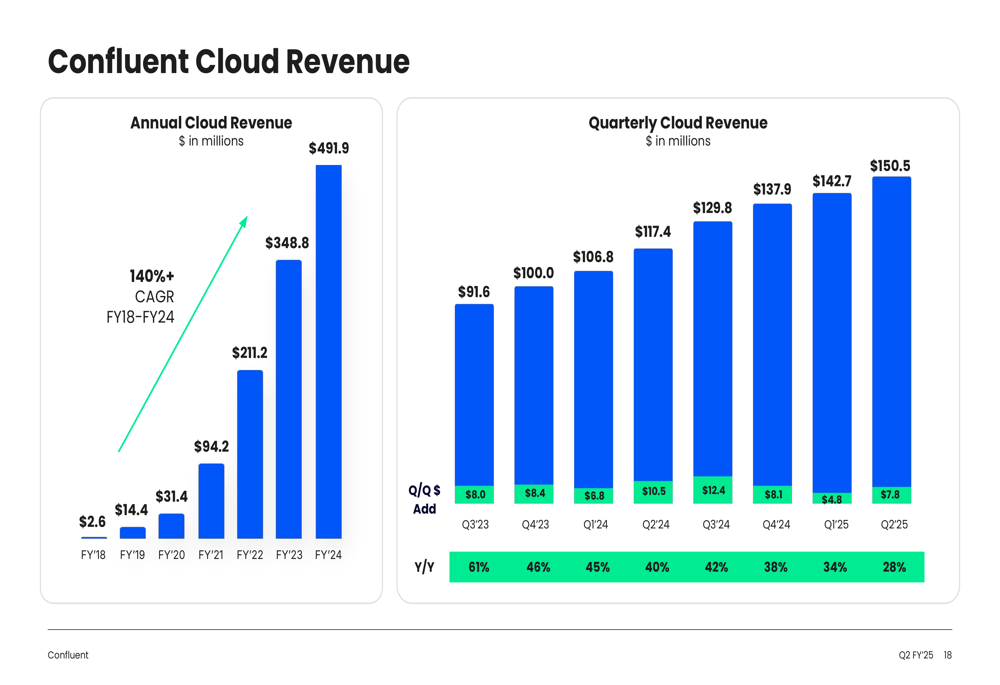

Confluent reported solid financial results for Q2 2025, with subscription revenue reaching $271 million, representing a 21% year-over-year increase. Cloud revenue, a key growth driver, rose to $151 million, up 28% compared to the same period last year.

As shown in the following chart of Confluent’s revenue trajectory over the past decade:

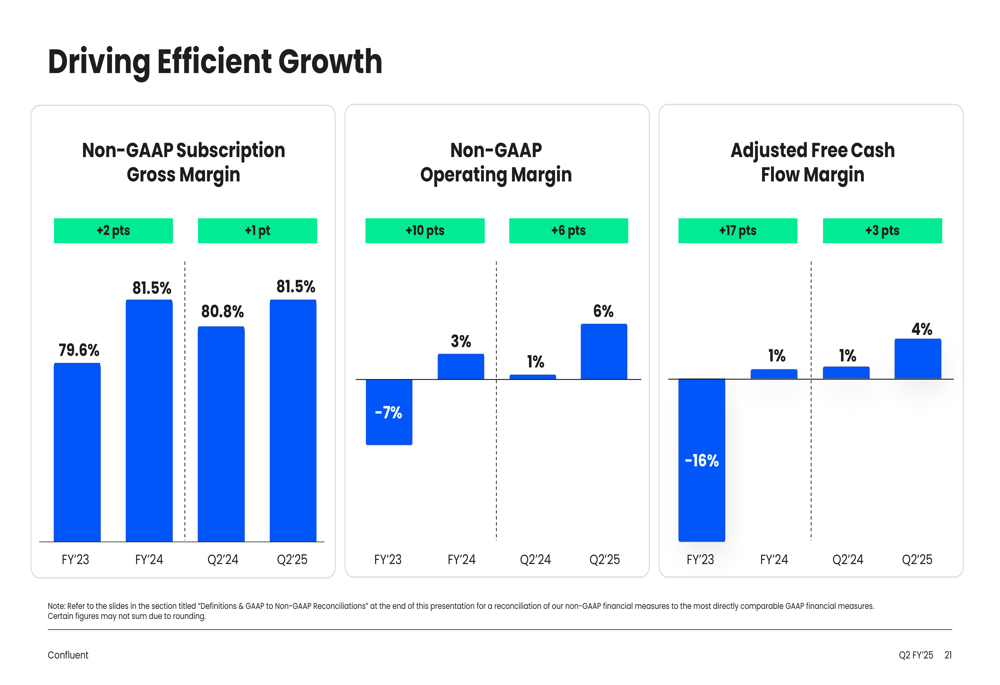

The company also demonstrated meaningful improvements in profitability metrics, with Non-GAAP Operating Margin reaching 6.3% (a 6 percentage point improvement year-over-year) and Adjusted Free Cash Flow Margin at 3.9% (a 3 percentage point improvement). These margin improvements indicate the company’s progress toward sustainable profitability.

Confluent’s cloud business continues to gain momentum, now representing 56% of subscription revenue according to the earnings report. This shift toward cloud-based offerings is illustrated in the following revenue breakdown:

Customer growth metrics show steady expansion across different revenue tiers, with 2,497 customers generating over $20,000 in Annual Recurring Revenue (ARR), up 8% year-over-year. More impressively, customers with over $1 million in ARR grew 24% year-over-year to 219, demonstrating Confluent’s success in expanding relationships with enterprise clients.

Strategic Initiatives

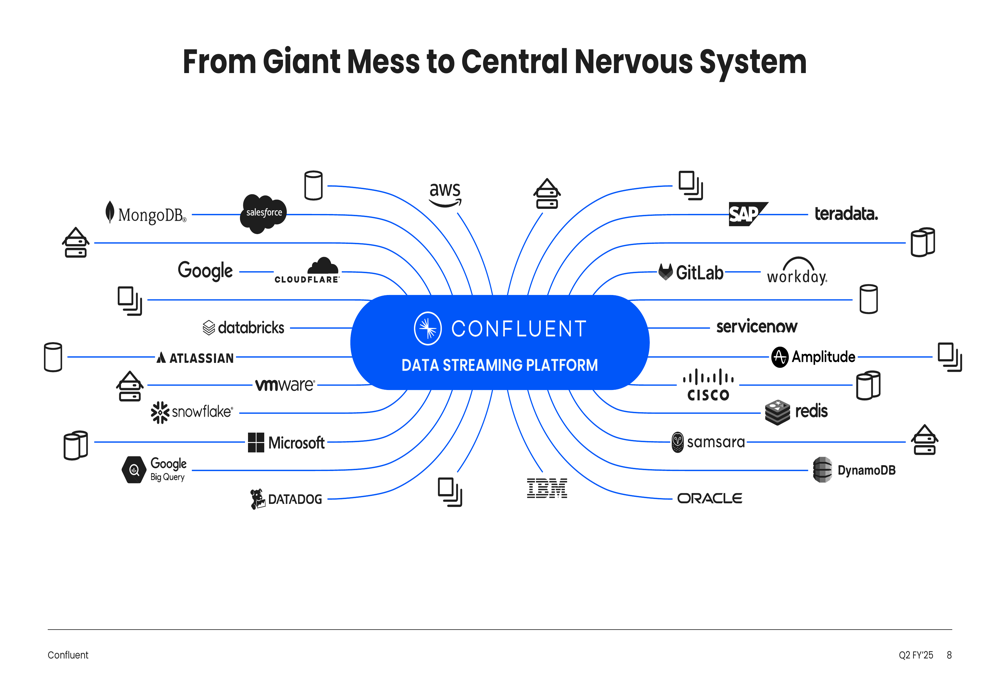

Confluent’s strategic positioning centers on becoming what it calls the "central nervous system" for enterprise data, connecting various data sources and applications across an organization. This approach is visualized in the company’s presentation:

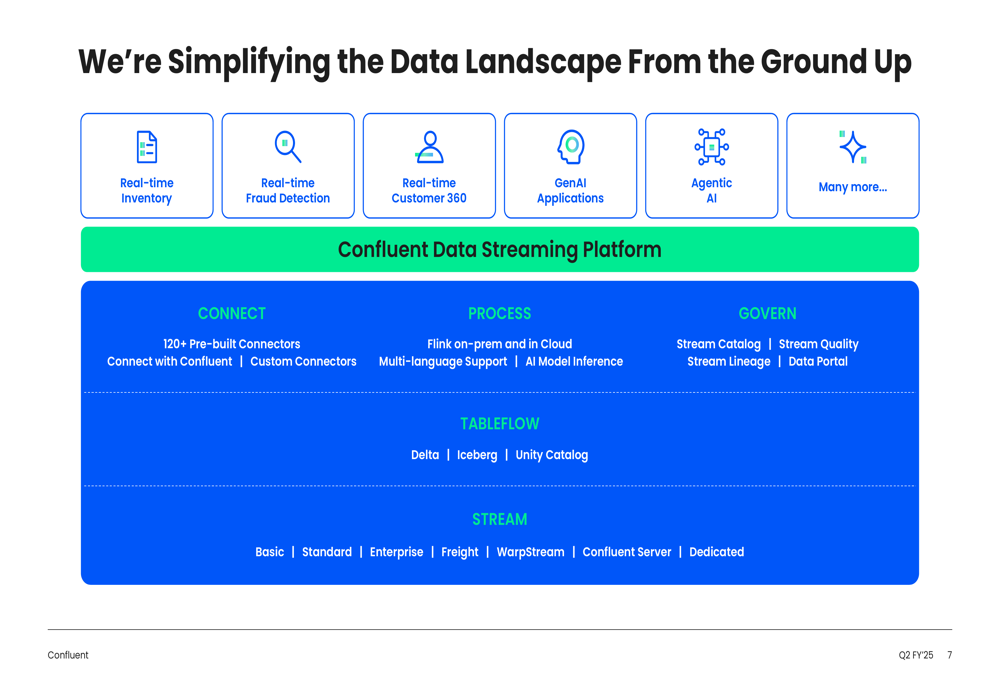

The company is building on its Apache Kafka foundation to create a comprehensive data streaming platform with capabilities for real-time inventory management, fraud detection, customer insights, and AI applications. Confluent’s platform architecture includes multiple layers for connecting, processing, governing, and streaming data:

A key focus for future growth is Confluent’s expansion into AI workloads. CEO Jay Kreps emphasized during the earnings call that the company expects "production AI use cases to grow 10x across a few hundred customers." This aligns with the presentation’s highlighting of AI as a growth driver for the company’s Data Streaming Platform (DSP).

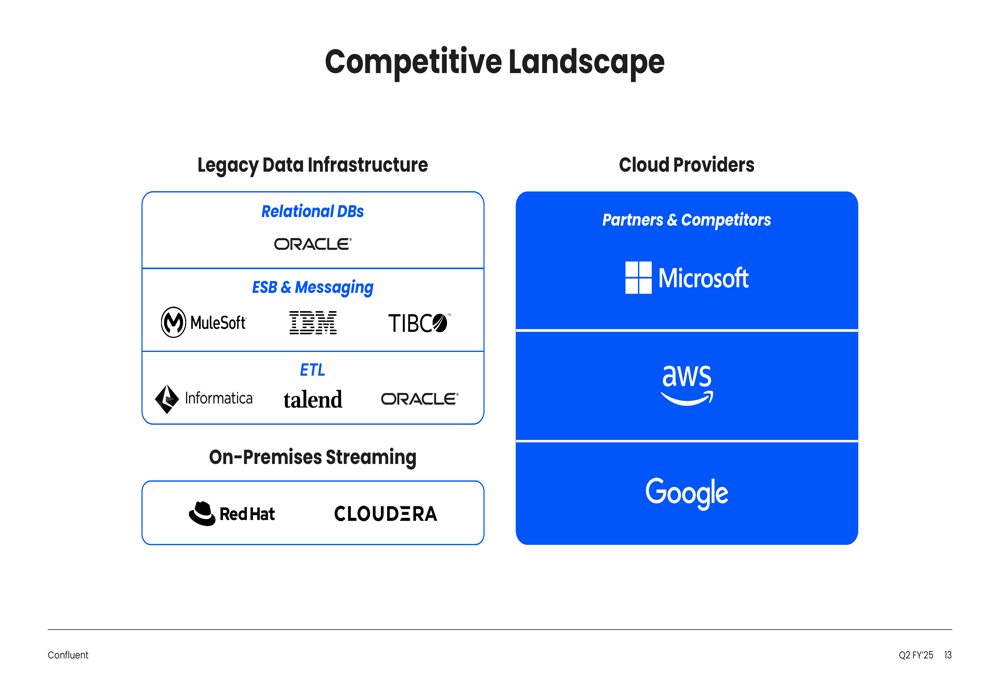

Competitive Industry Position

Confluent positions itself against both legacy data infrastructure providers and major cloud platforms. The company’s competitive landscape slide identifies traditional players like Oracle, IBM, TIBCO, and Informatica, as well as cloud giants Microsoft, AWS, and Google, who serve as both partners and competitors:

The company’s success across multiple industries is evidenced by its growing customer base, which includes major enterprises in financial services, technology, retail, healthcare, and other sectors:

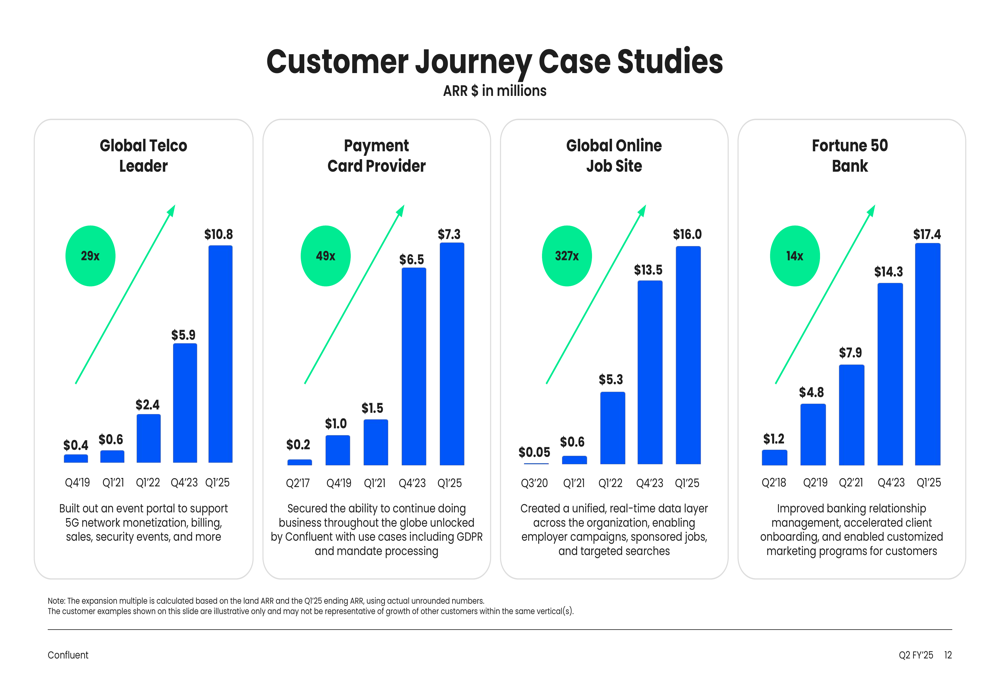

Confluent’s case studies demonstrate significant ARR expansion with key customers. For example, a Fortune 50 bank increased its ARR from $1.2 million in Q2 2018 to $17.4 million in Q1 2025, while a global online job site grew from just $50,000 in Q3 2020 to $16 million in Q1 2025:

Forward-Looking Statements & Challenges

Confluent projects continued growth while focusing on margin improvement and managing stock-based compensation. The company is targeting subscription revenue between $1.105 billion and $1.110 billion for fiscal year 2025, representing approximately 20% year-over-year growth.

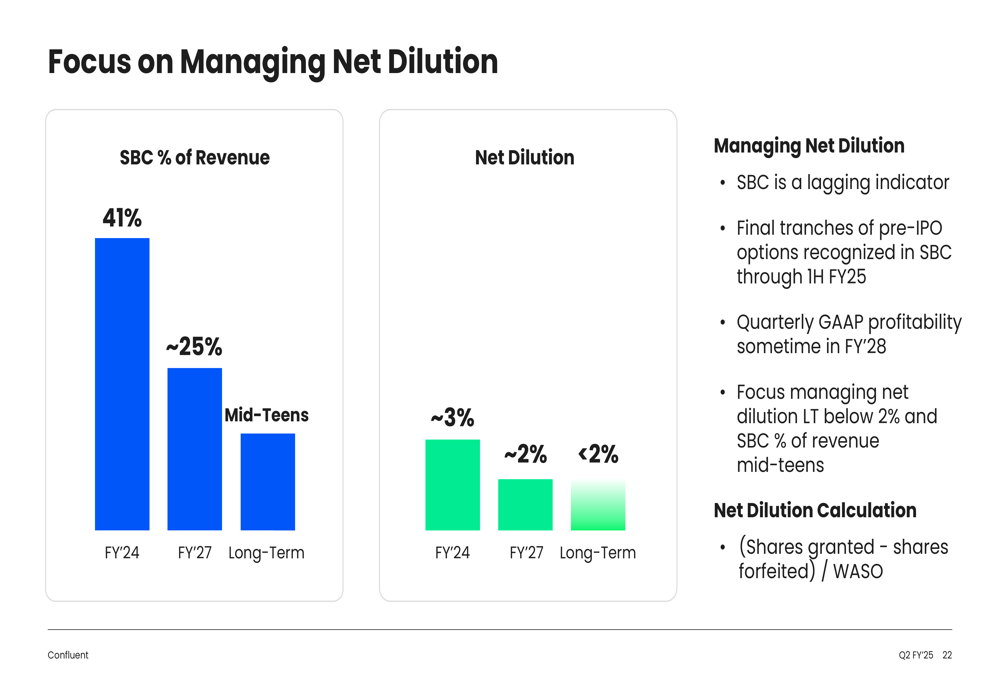

The presentation highlights Confluent’s efforts to manage dilution from stock-based compensation, with plans to reduce SBC as a percentage of revenue from 41% in FY’24 to approximately 25% in FY’27, with a long-term target in the mid-teens:

While Confluent’s growth story remains compelling, the earnings call revealed some challenges, including slower-than-expected cloud growth compared to historical averages and some large customers reverting to on-premise platforms. These factors may explain the market’s tepid response despite the positive metrics.

The company’s margin improvement trajectory shows promising momentum toward sustainable profitability:

As Confluent continues its journey toward its long-term goal of $1 billion+ in revenue with non-GAAP profitability, the company will need to navigate competitive pressures while capitalizing on the growing demand for real-time data streaming solutions, particularly as AI adoption accelerates across enterprises.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.