These are top 10 stocks traded on the Robinhood UK platform in July

Introduction & Market Context

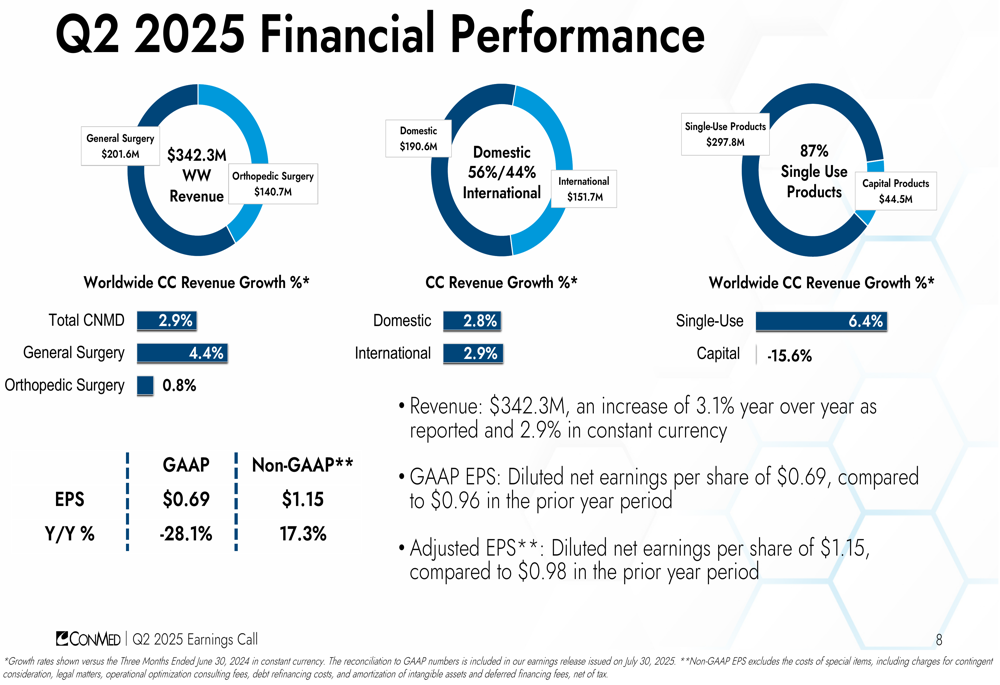

CONMED Corporation (NASDAQ:CNMD) presented its second quarter 2025 financial results on July 30, showcasing a recovery from its disappointing first quarter performance. The medical technology company reported revenue of $342.3 million, representing a 3.1% year-over-year increase as reported and 2.9% in constant currency. Adjusted earnings per share reached $1.15, up 17.3% compared to the same period last year.

The company’s stock closed at $50.29 on the day of the presentation, down slightly by 0.36%, and remains significantly below its 52-week high of $78.19, reflecting ongoing investor caution despite the improved quarterly performance.

Quarterly Performance Highlights

CONMED’s Q2 2025 results demonstrated a notable improvement over its first quarter, when the company missed analyst expectations with an EPS of $0.79 against forecasts of $1.00. The second quarter’s adjusted EPS of $1.15 marks a substantial sequential improvement, though GAAP EPS declined 28.1% year-over-year to $0.69.

Revenue growth was primarily driven by the General Surgery segment, which increased by 4.4% in constant currency to $201.6 million, while Orthopedic Surgery grew more modestly at 0.8% to $140.7 million.

As shown in the following breakdown of Q2 2025 financial performance:

The company’s product mix continues to shift toward recurring revenue streams, with single-use products representing 87% of total sales ($297.8 million) and growing at 6.4% in constant currency. In contrast, capital equipment sales declined by 15.6%, highlighting CONMED’s strategic pivot toward consumables.

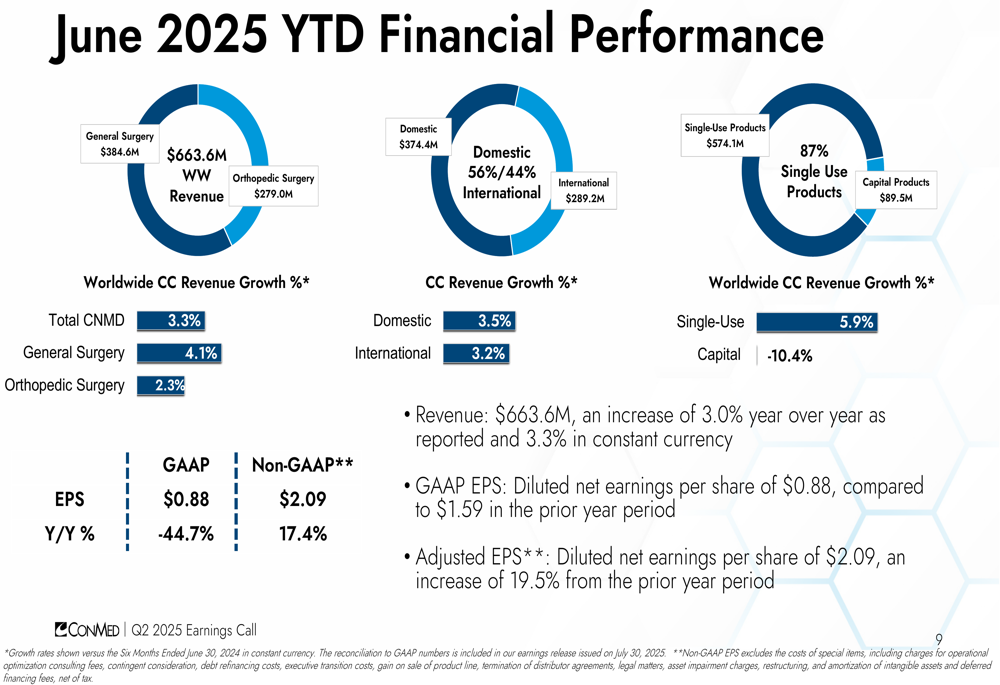

For the first half of 2025, CONMED reported total revenue of $663.6 million, a 3.0% increase as reported and 3.3% in constant currency. Year-to-date adjusted EPS reached $2.09, up 17.4% from the prior year period.

The following chart illustrates the company’s performance through June 2025:

Strategic Industry Position

CONMED operates in several large and attractive medical device markets with significant growth potential. The company’s presentation highlighted the substantial market opportunity across its two main segments:

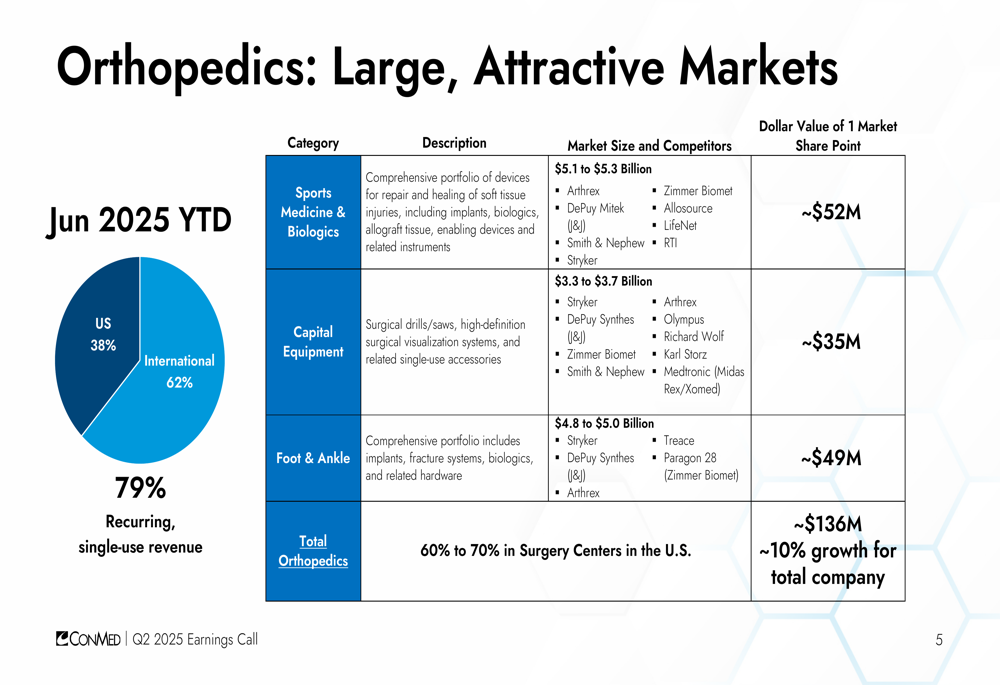

In Orthopedics, CONMED competes in markets valued at approximately $13.2-14.0 billion, including Sports Medicine & Biologics ($5.1-5.3 billion), Capital Equipment ($3.3-3.7 billion), and Foot & Ankle ($4.8-5.0 billion). The company noted that gaining just one percentage point of market share across these segments would represent approximately $136 million in revenue, or about 10% growth for the total company.

The following slide details CONMED’s position in the orthopedics market:

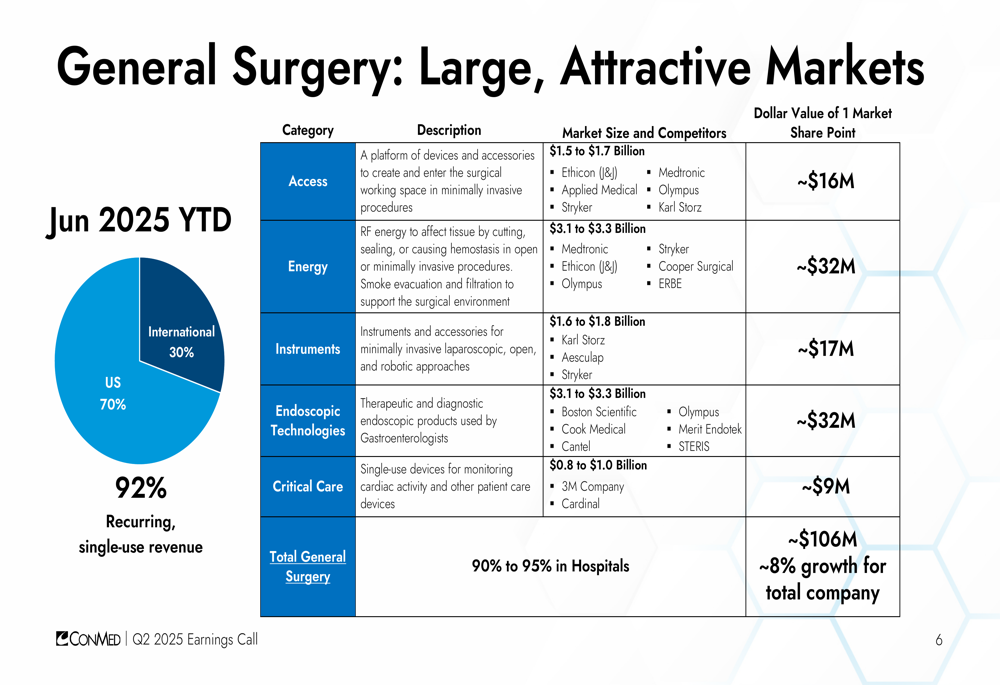

Similarly, in General Surgery, the company operates in markets valued at approximately $10.1-11.1 billion across Access, Energy, Instruments, Endoscopic Technologies, and Critical Care segments. A one percentage point gain in these markets would translate to approximately $106 million in revenue, or 8% growth for the total company.

The company’s General Surgery market positioning is illustrated here:

Strategic Initiatives

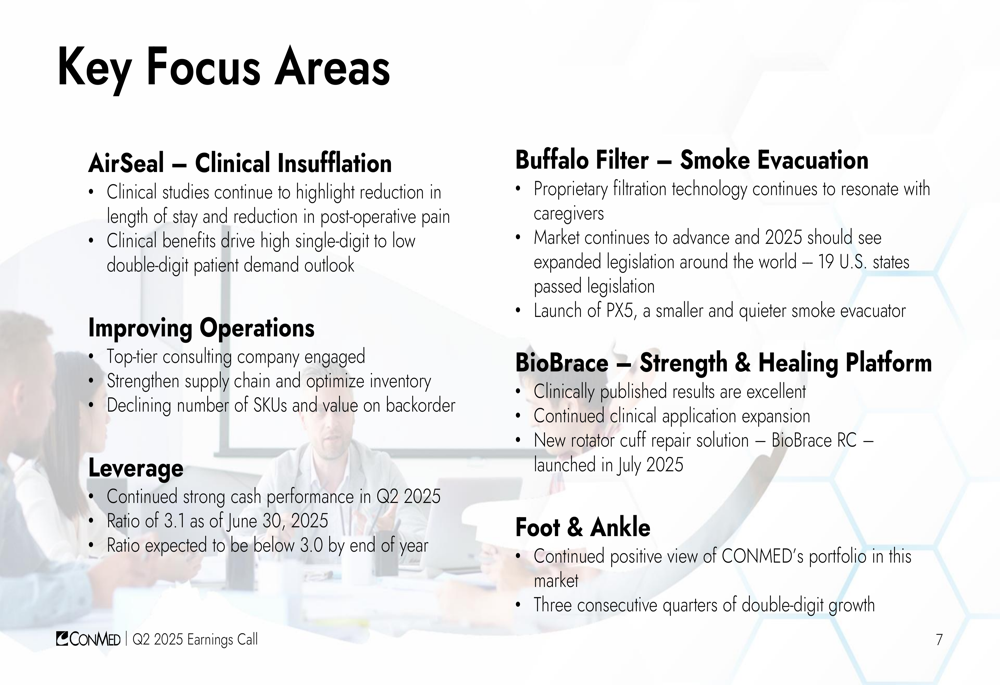

CONMED’s presentation identified four key focus areas driving its growth strategy: AirSeal (clinical insufflation), Buffalo Filter (smoke evacuation), BioBrace (strength & healing platform), and Foot & Ankle.

The company highlighted clinical studies showing AirSeal’s benefits in reducing length of hospital stay and post-operative pain. For Buffalo Filter, CONMED noted that market adoption continues to advance with expanded legislation expected in 2025. The BioBrace platform was cited for excellent clinical results, while the Foot & Ankle segment maintains a positive outlook.

These strategic priorities are detailed in the following slide:

The company’s overall vision centers on "Empowering healthcare providers worldwide to deliver exceptional outcomes for patients," with a focus on "People, Products, Profitability" as shown in their corporate vision statement:

Forward-Looking Statements

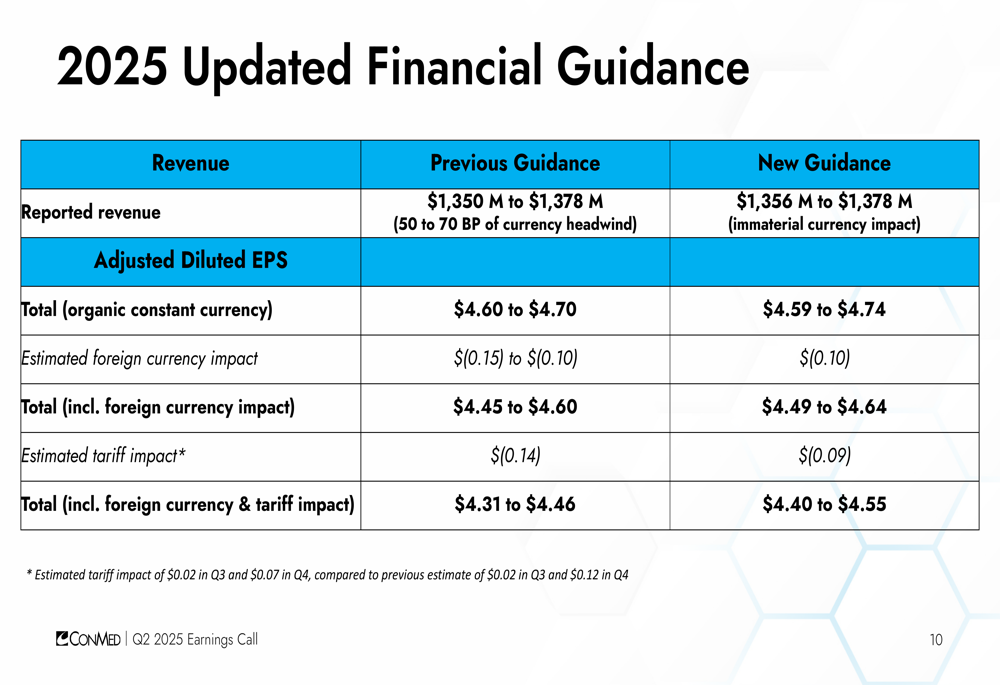

CONMED updated its full-year 2025 guidance, reflecting increased confidence in its revenue outlook while maintaining similar EPS projections. The company now expects reported revenue between $1,356 million and $1,378 million, compared to the previous range of $1,350 million to $1,378 million. The updated guidance notes that currency impact is now expected to be immaterial, an improvement from the previously anticipated 50 to 70 basis point headwind.

For adjusted diluted EPS, CONMED projects a range of $4.59 to $4.74, a slight adjustment from the previous guidance of $4.60 to $4.70. This guidance incorporates the company’s assessment of foreign currency and tariff impacts.

The updated financial guidance is presented in the following slide:

Financial Analysis

CONMED’s Q2 results reflect the company’s ongoing transition toward higher-margin, recurring revenue streams. The 87% of revenue now coming from single-use products provides greater stability and predictability compared to capital equipment sales, which continue to decline.

The company’s leverage ratio improved to 3.1 as of June 30, 2025, down from 3.2 reported in the previous quarter, indicating strengthened cash performance and financial position. This improvement aligns with the company’s shareholder objectives of increasing profitability and evolving its product mix toward higher-growth, higher-margin offerings.

Geographic revenue distribution remains relatively balanced, with domestic sales accounting for 56% ($190.6 million) and international sales representing 44% ($151.7 million) of Q2 revenue. Both regions showed similar growth rates of 2.8% and 2.9% respectively in constant currency.

The significant gap between GAAP EPS (-28.1% year-over-year) and adjusted EPS (+17.3%) suggests substantial one-time costs or adjustments affecting reported earnings, though the company did not provide detailed reconciliation in the presentation materials.

Overall, CONMED’s Q2 2025 presentation indicates a company in transition, successfully pivoting toward recurring revenue streams while managing through challenges in capital equipment sales, resulting in modest but steady overall growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.