Trump to impose 100% tariff on China starting November 1

ConocoPhillips (NYSE:COP) reported improved first-quarter 2025 results on Wednesday, with adjusted earnings rising to $2.7 billion and adjusted earnings per share reaching $2.09, exceeding the previous quarter’s performance. The company’s stock showed positive momentum, trading up 1.81% in premarket activity at $89.30 ahead of the earnings call.

Quarterly Performance Highlights

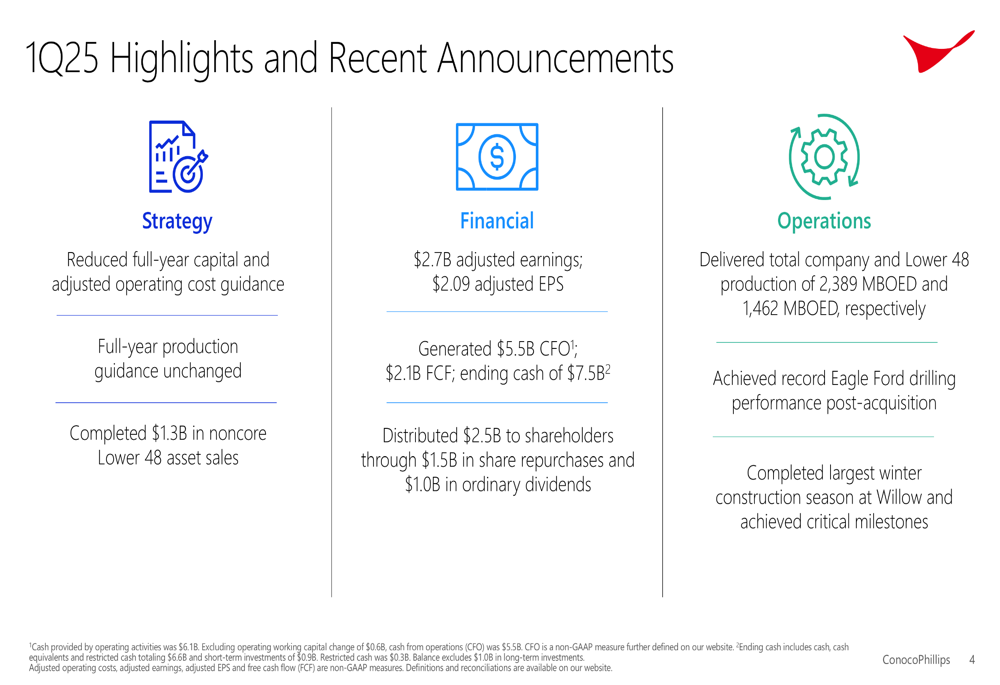

The energy giant delivered total production of 2,389 thousand barrels of oil equivalent per day (MBOED) in the first quarter, with Lower 48 production accounting for 1,462 MBOED. This represents the first full quarter following the Marathon Oil (NYSE:MRO) acquisition, which has strengthened the company’s domestic operations.

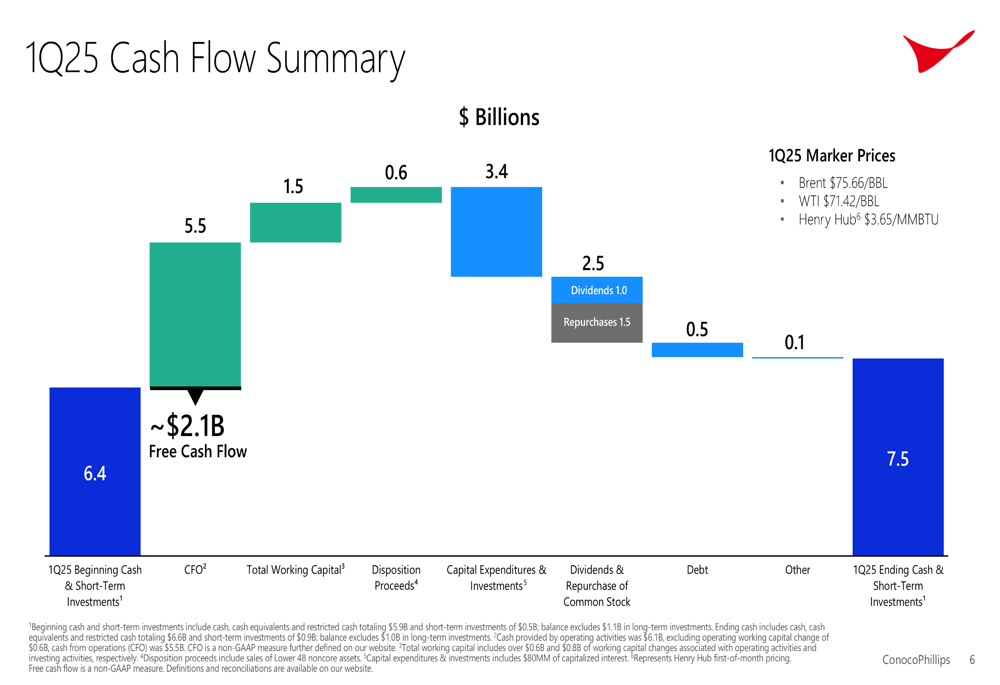

"We generated $5.5 billion in cash from operations and $2.1 billion in free cash flow during the quarter," the company stated in its presentation, highlighting its continued focus on shareholder returns with $2.5 billion distributed through $1.5 billion in share repurchases and $1.0 billion in dividends.

The company’s financial position remained robust, with cash and short-term investments increasing from $6.4 billion at the beginning of the quarter to $7.5 billion by quarter-end, despite significant capital expenditures and shareholder distributions.

As shown in the following cash flow summary:

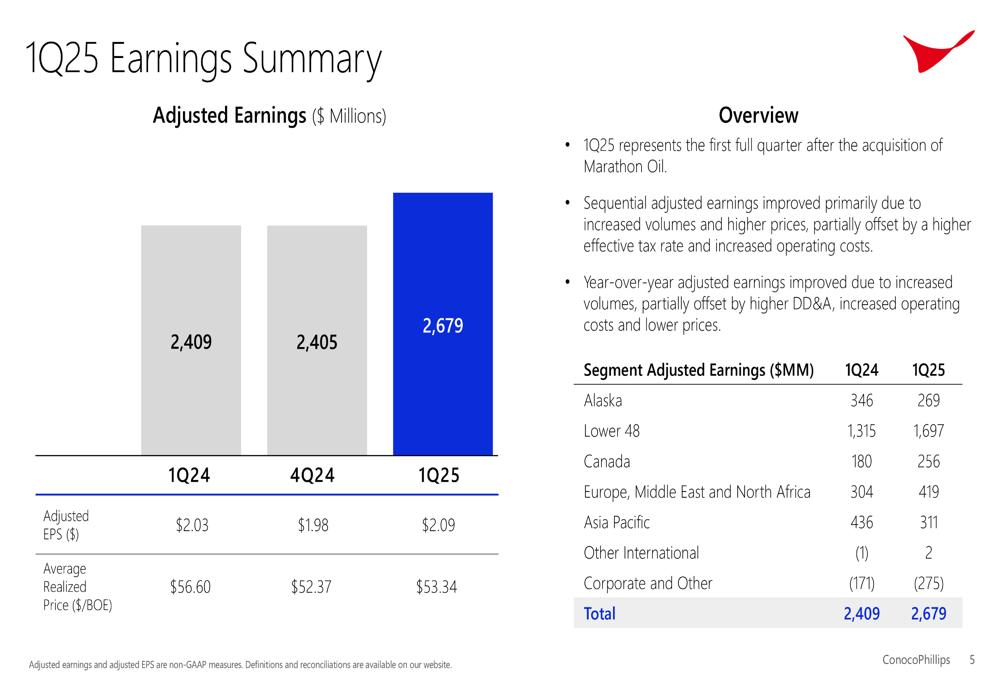

The first quarter saw adjusted earnings improve sequentially from $2,405 million in Q4 2024 to $2,679 million, while adjusted EPS rose from $1.98 to $2.09. Average realized prices increased slightly to $53.34 per barrel of oil equivalent (BOE) from $52.37 in the previous quarter, though still below the $56.60 realized in Q1 2024.

The earnings breakdown by segment reveals particularly strong performance in the Lower 48, where adjusted earnings reached $1,697 million compared to $1,315 million in the same quarter last year:

Strategic Initiatives

ConocoPhillips highlighted several strategic accomplishments during the quarter, including the completion of $1.3 billion in noncore Lower 48 asset sales, which aligns with the company’s portfolio optimization strategy.

The integration of Marathon Oil appears to be proceeding smoothly, with the company noting that "Marathon Oil integration and synergy capture [are] ahead of schedule." This successful integration has already yielded tangible benefits, with the company achieving "record Eagle Ford drilling performance post-acquisition."

The company also made significant progress on its Willow project in Alaska, completing what it described as the "largest winter construction season" while achieving "critical milestones" for this long-term development.

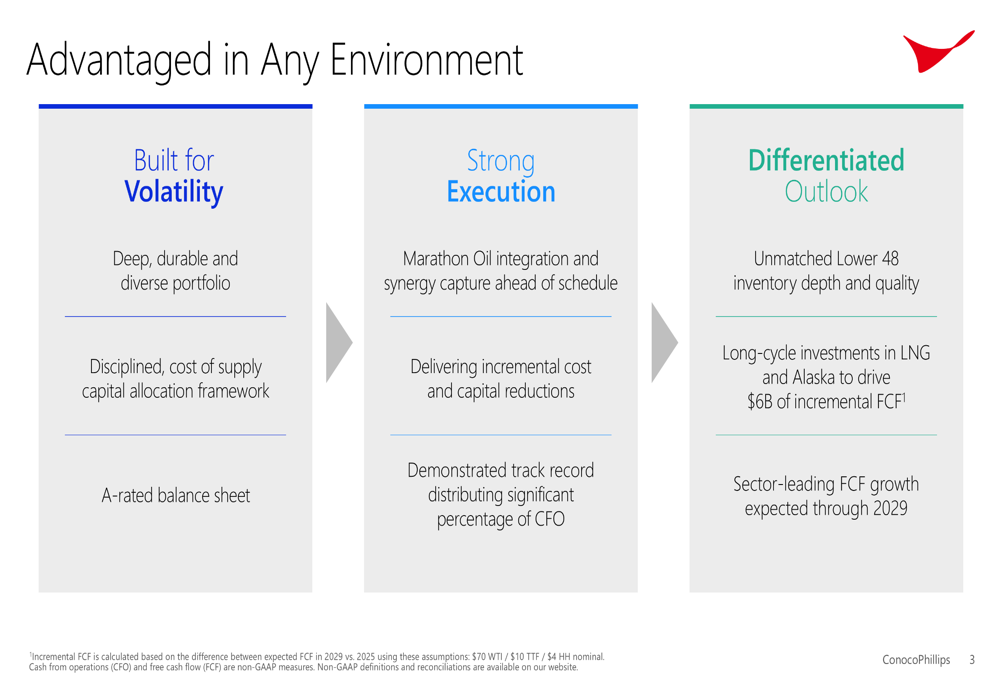

These strategic initiatives form part of ConocoPhillips’ broader positioning as shown in this overview:

Forward-Looking Statements

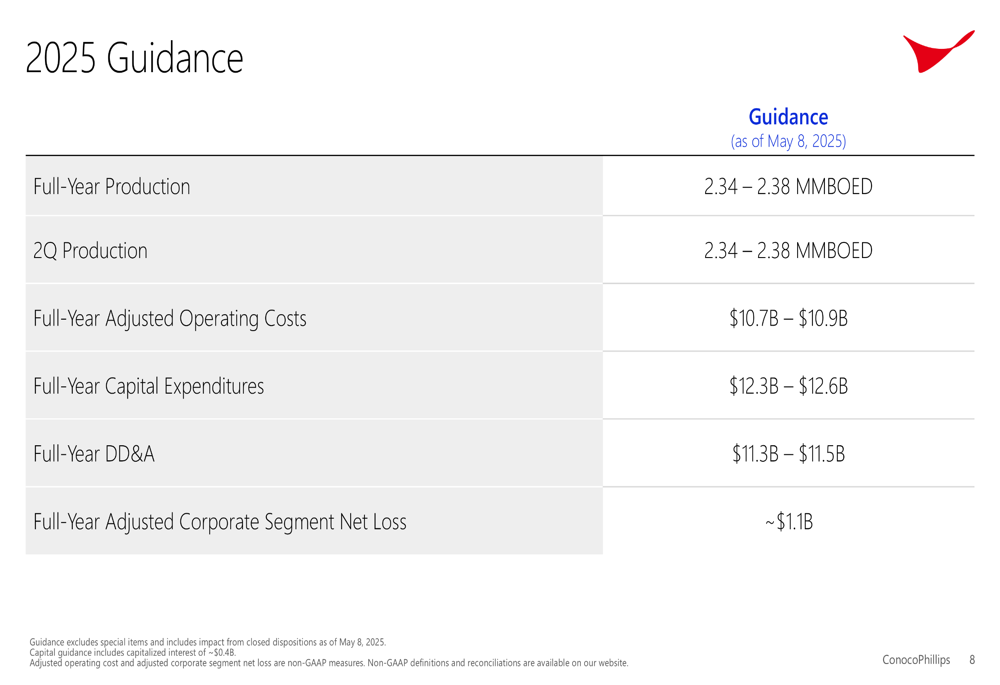

In a positive signal to investors, ConocoPhillips maintained its full-year production guidance of 2.34-2.38 million barrels of oil equivalent per day while reducing both its capital expenditure and operating cost forecasts. The company now projects full-year adjusted operating costs of $10.7-10.9 billion and capital expenditures of $12.3-12.6 billion.

The company’s detailed 2025 guidance provides a comprehensive outlook for investors:

ConocoPhillips emphasized its long-term growth trajectory, noting that "sector-leading FCF growth [is] expected through 2029," with long-cycle investments in LNG and Alaska projected to drive $6 billion of incremental free cash flow.

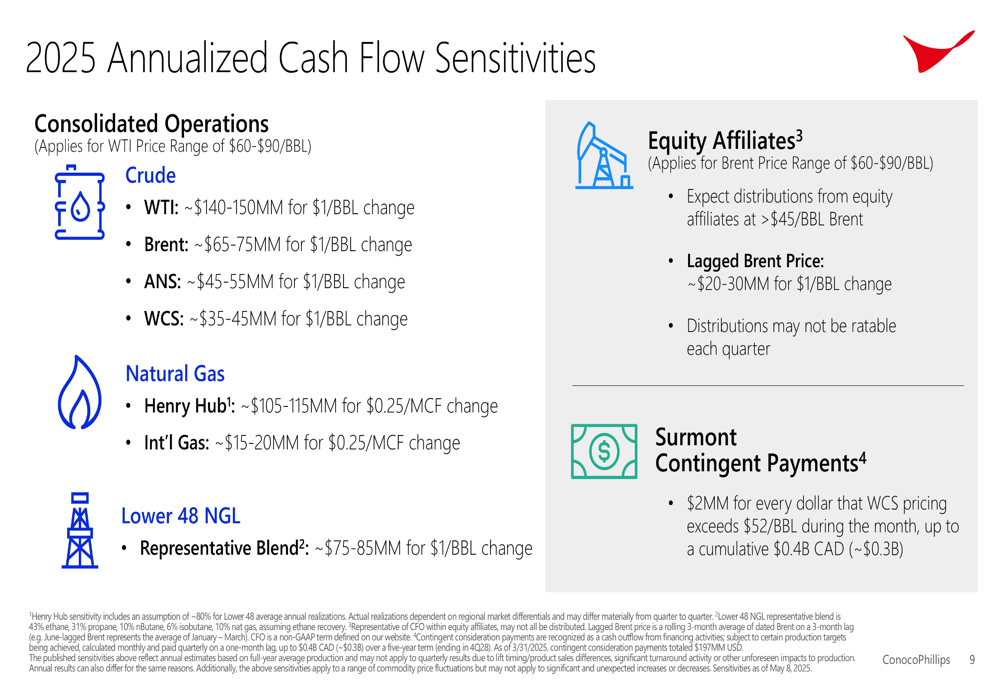

The company also provided detailed sensitivity analysis to help investors understand potential impacts from commodity price fluctuations:

Financial Analysis

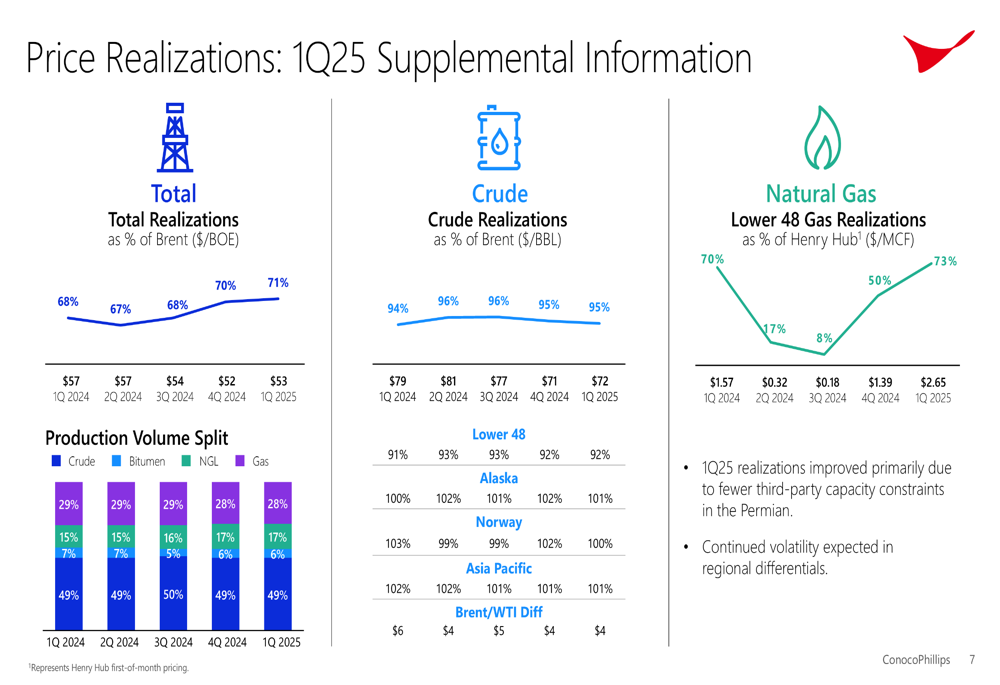

Price realizations improved in the first quarter, with total realizations as a percentage of Brent increasing to 71% from 70% in the previous quarter. Lower 48 gas realizations showed particularly strong improvement, rising to 73% of Henry Hub from 50% in Q4 2024.

The company attributed this improvement primarily to "fewer third-party capacity constraints in the Permian," though it cautioned that "continued volatility [is] expected in regional differentials."

This detailed breakdown of price realizations provides insight into the company’s revenue drivers:

ConocoPhillips’ first-quarter highlights across strategy, financial performance, and operations demonstrate the company’s continued focus on disciplined execution and shareholder returns:

The company’s stock has traded between $79.88 and $124.23 over the past 52 weeks, with the current price representing a potential value opportunity according to some analysts. With its strong cash generation, disciplined capital allocation, and strategic positioning across diverse assets, ConocoPhillips appears well-positioned to navigate the volatile energy market environment through 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.