InvestingPro’s Fair Value model captures 63% gain in Steelcase ahead of acquisition

Introduction & Market Context

Consensus Cloud Solutions Inc (NASDAQ:CCSI) released its second quarter 2025 preliminary unaudited results on August 7, 2025, showing a return to overall revenue growth driven by strong performance in its corporate segment. The cloud fax and digital delivery solutions provider saw its stock rise 4.22% to close at $20.97 following the announcement.

The company's Q2 results demonstrate its continued strategic focus on expanding its corporate business while managing the planned decline in its Small Office/Home Office (SoHo) segment. This approach appears to be yielding results, with total revenue returning to growth for the first time in several quarters.

Quarterly Performance Highlights

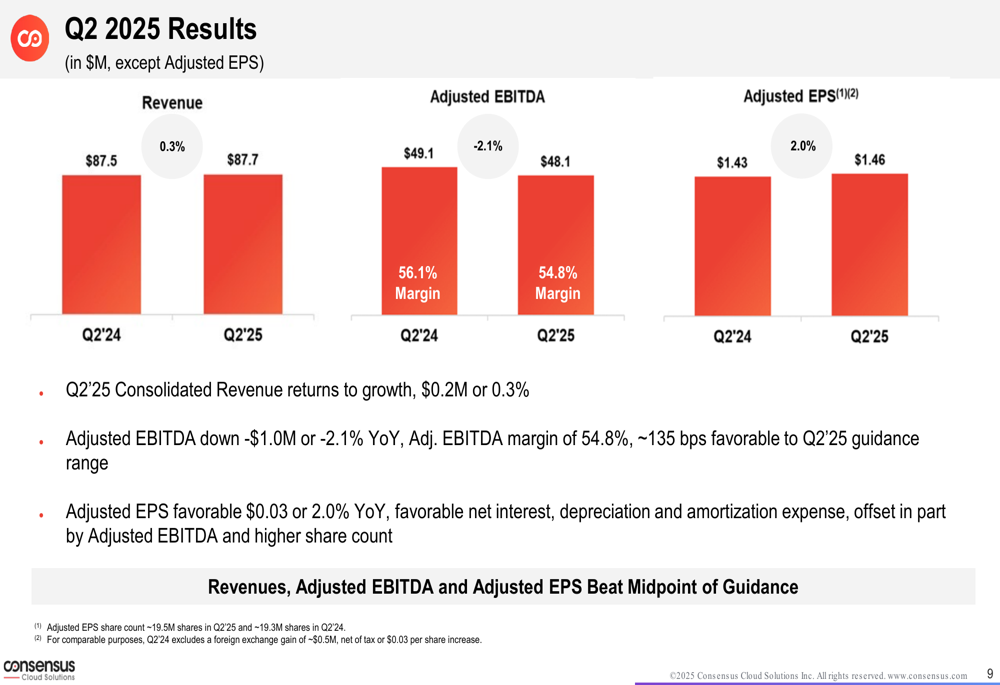

Consensus Cloud reported Q2 2025 revenue of $87.7 million, representing a modest 0.3% increase compared to $87.5 million in the same period last year. While the growth rate is small, it marks an important milestone in the company's transition strategy.

Adjusted EBITDA came in at $48.1 million with a 54.8% margin, down 2.1% year-over-year but approximately 135 basis points better than the company's guidance range. Adjusted earnings per share increased by 2.0% to $1.46, compared to $1.43 in Q2 2024.

As shown in the following chart of quarterly financial results:

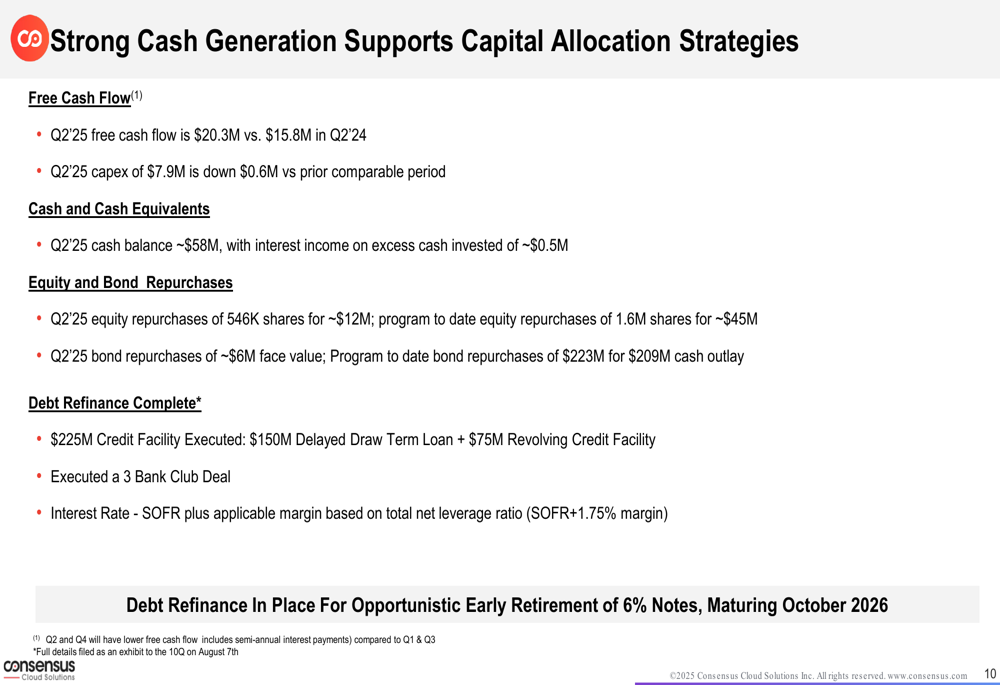

Free cash flow improved significantly to $20.3 million, up from $15.8 million in Q2 2024, while capital expenditures decreased by $0.6 million compared to the prior year period. The company maintained a healthy cash balance of approximately $58 million at the end of the quarter.

Segment Analysis: Corporate vs SoHo

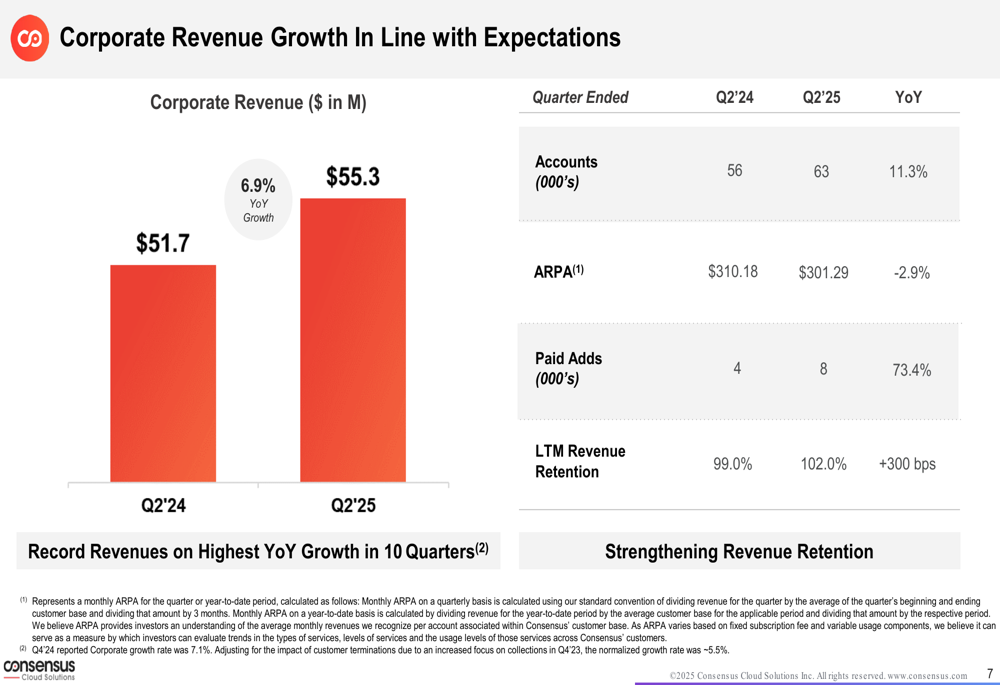

The corporate segment continued its strong performance with revenue reaching $55.3 million, a 6.9% increase compared to $51.7 million in Q2 2024. This growth was driven by an 11.3% expansion in the corporate customer base, which grew to 63,000 accounts compared to 56,000 in the prior year. The company also reported a revenue retention rate of 102%, up from 99% in Q2 2024, indicating improved customer satisfaction and upselling success.

The following chart illustrates the corporate segment's revenue growth:

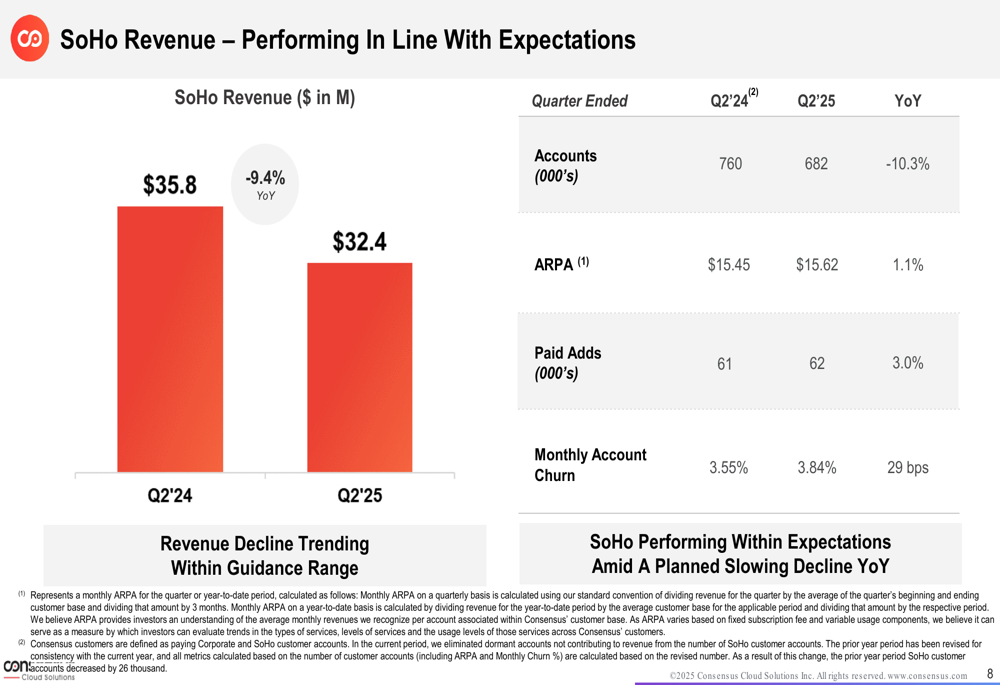

In contrast, the SoHo segment continued its expected decline with revenue of $32.4 million, down 9.4% from $35.8 million in Q2 2024. The SoHo account base decreased to 682,000 from 702,000 in Q1 2025, with monthly churn increasing slightly to 3.84% from 3.52% in the previous quarter.

The company's presentation highlighted that the SoHo segment is performing in line with expectations, as shown in this chart:

Management noted that they continue to focus on "optimizing profitability" in the SoHo segment while "maximizing the efficiency of advertising investments." This approach aligns with the company's strategy of managing the SoHo decline while investing in corporate growth opportunities.

Financial Position & Capital Allocation

Consensus Cloud continued to demonstrate strong cash generation capabilities, supporting its capital allocation strategies. The company completed a debt refinancing with a new $225 million credit facility, consisting of a $150 million delayed draw term loan and a $75 million revolving credit facility. The new facility features an interest rate of SOFR plus a margin based on total net leverage ratio (currently SOFR+1.75%).

During the quarter, the company repurchased 546,000 shares for approximately $12 million, bringing the total program-to-date repurchases to 1.6 million shares for approximately $45 million. Additionally, the company repurchased bonds with a face value of approximately $6 million during Q2, with program-to-date bond repurchases totaling $223 million for a cash outlay of $209 million.

The following slide details the company's cash generation and capital allocation activities:

Forward-Looking Statements & Guidance

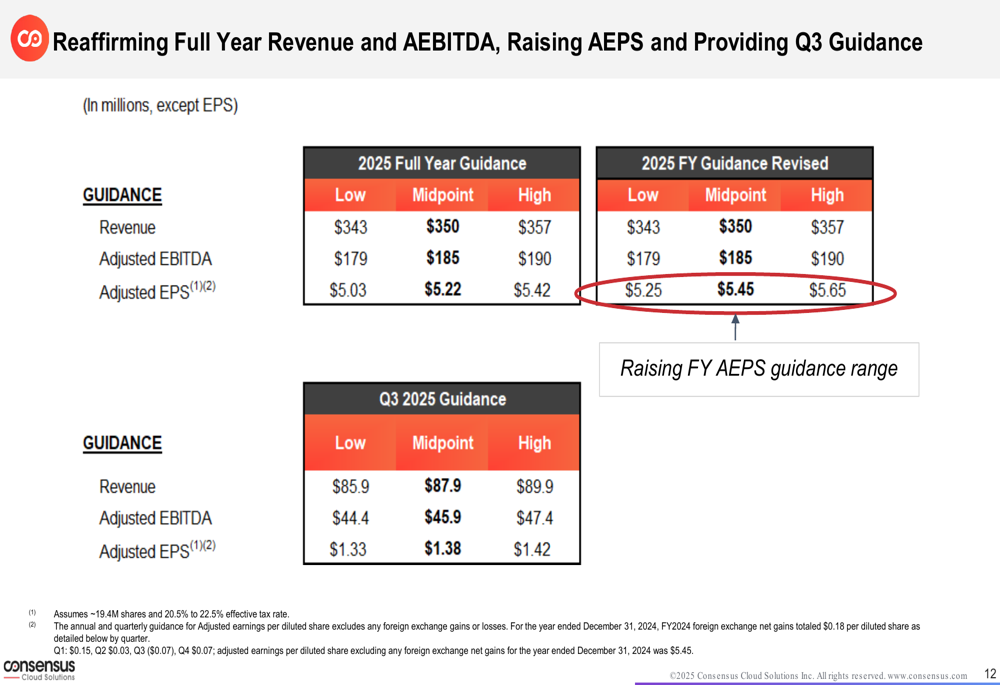

Consensus Cloud reaffirmed its full-year 2025 revenue guidance of $343-357 million and Adjusted EBITDA guidance of $203-211 million. However, the company raised its Adjusted EPS guidance to $5.42-5.54 from the previous range of $5.30-5.42.

For Q3 2025, the company expects revenue between $86-90 million, Adjusted EBITDA between $47-49 million, and Adjusted EPS between $1.35-1.45.

The following guidance table provides a detailed breakdown of the company's expectations:

The revised guidance suggests management's confidence in continued execution of its strategy, with particular emphasis on maintaining strong profitability metrics despite the ongoing transition in its business mix.

Strategic Initiatives

The company's presentation highlighted several strategic initiatives driving its corporate business growth. These include a sustained usage increase of cloud fax with a focus on the healthcare industry, high retention rates, large account expansion, and contributions from strategic partnerships.

For the SoHo segment, the company continues to strategically focus on optimizing profitability while managing the expected decline. Management noted that the success of corporate e-commerce changes is affecting the SoHo base composition, suggesting some migration between segments.

The corporate segment saw over 5,800 e-commerce offering eFax Protect and Corporate upsells in Q2 2025, indicating strong adoption of the company's enhanced service offerings.

Consensus Cloud's Q2 2025 results demonstrate that its strategy of focusing on corporate growth while managing the SoHo decline is beginning to yield positive results, with overall revenue returning to growth and improved profitability metrics. The company's strong cash generation capabilities and active capital allocation approach further support its strategic direction.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.