These are top 10 stocks traded on the Robinhood UK platform in July

Corteva Inc. (NYSE:CTVA) reported strong margin expansion in its first quarter of 2025, despite a slight decline in revenue, according to the company’s earnings presentation delivered on May 8, 2025. The agricultural inputs provider reaffirmed its full-year guidance, projecting double-digit EBITDA growth for 2025 while navigating mixed agricultural fundamentals and potential tariff impacts.

Quarterly Performance Highlights

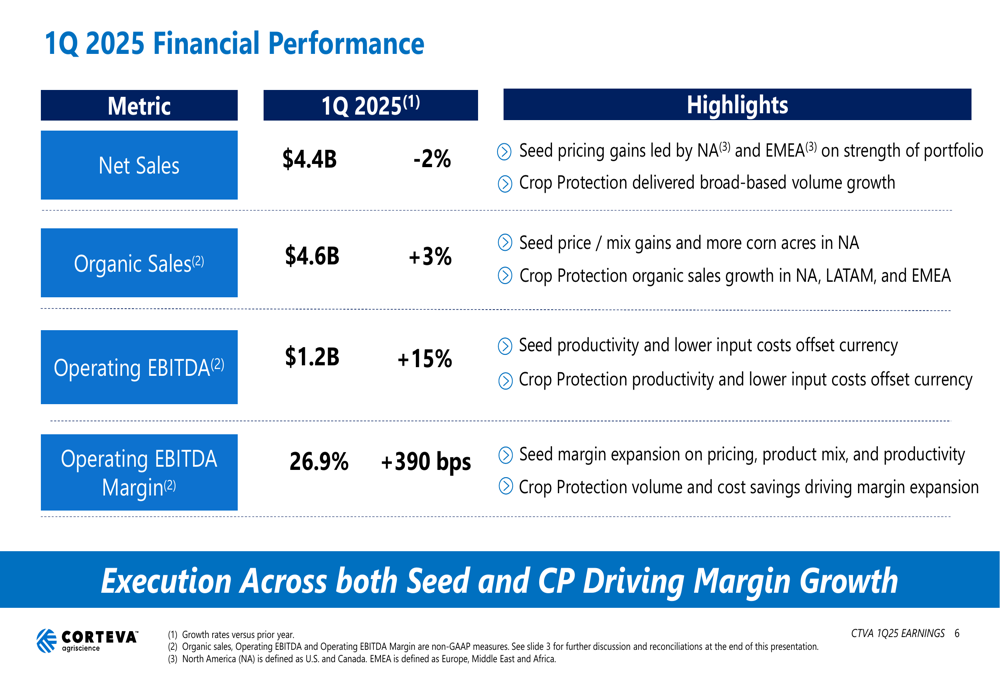

Corteva reported Q1 2025 net sales of $4.4 billion, representing a 2% decrease compared to the same period last year. However, organic sales grew by 3%, demonstrating underlying strength when excluding currency impacts. The company achieved significant profitability improvements, with operating EBITDA increasing by 15% to $1.2 billion and operating EBITDA margin expanding by 390 basis points to 26.9%.

As shown in the following summary of Q1 2025 financial performance:

The company’s operating EPS rose 27% to $1.13, while GAAP EPS from continuing operations increased 83% to $0.97. These strong bottom-line results were driven by productivity improvements, lower input costs, and pricing gains in the Seed segment.

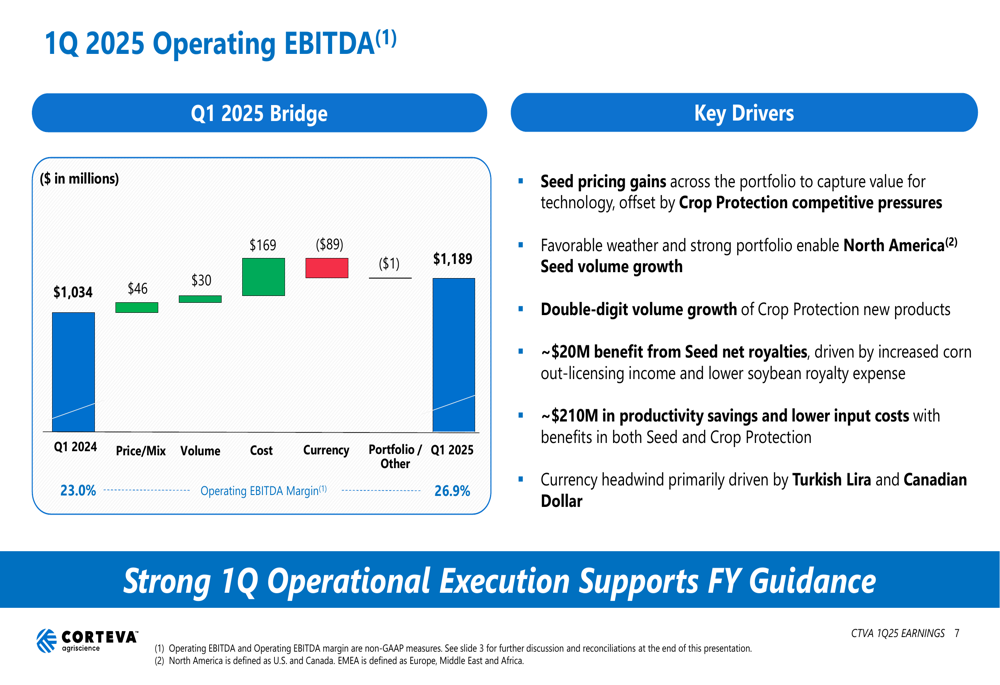

The following bridge analysis illustrates the key drivers behind Corteva’s Q1 2025 Operating EBITDA growth:

Cost savings contributed $169 million to the EBITDA improvement, while price/mix added $46 million and volume growth added $30 million. These positive factors were partially offset by $89 million in currency headwinds, primarily from the Turkish Lira and Canadian Dollar.

Segment Analysis

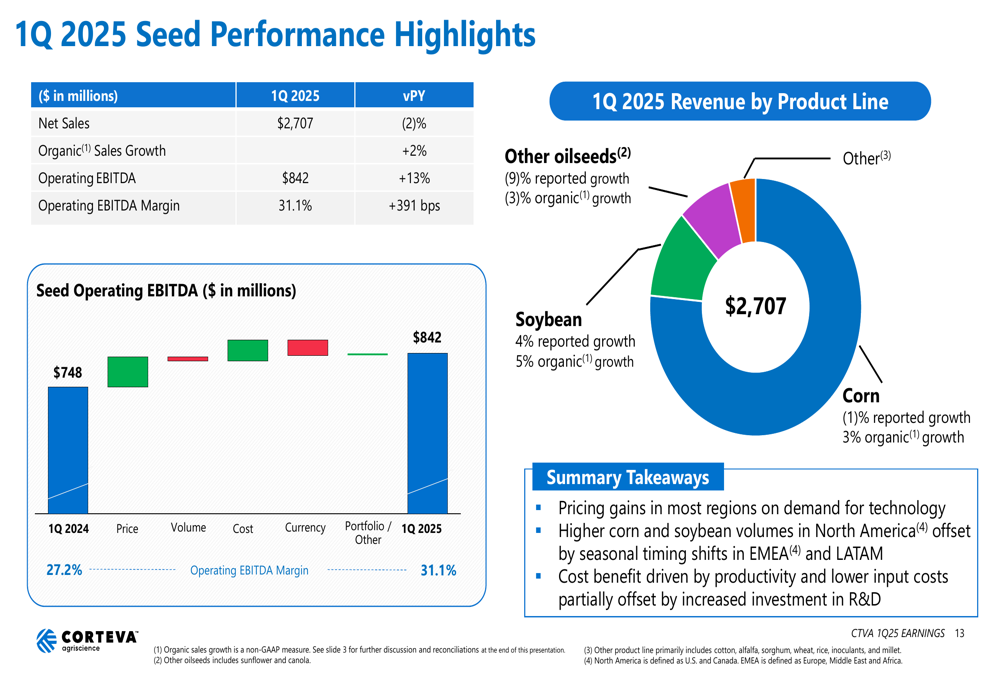

Corteva’s Seed segment reported net sales of $2.7 billion, a 2% decrease year-over-year, though organic sales grew by 2%. The segment’s operating EBITDA increased 13% to $842 million, with margin expanding by 391 basis points to 31.1%. This performance was driven by price gains in most regions due to strong demand for technology, higher corn and soybean volumes in North America, and cost benefits from productivity improvements and lower input costs.

The following chart details the Seed segment’s performance:

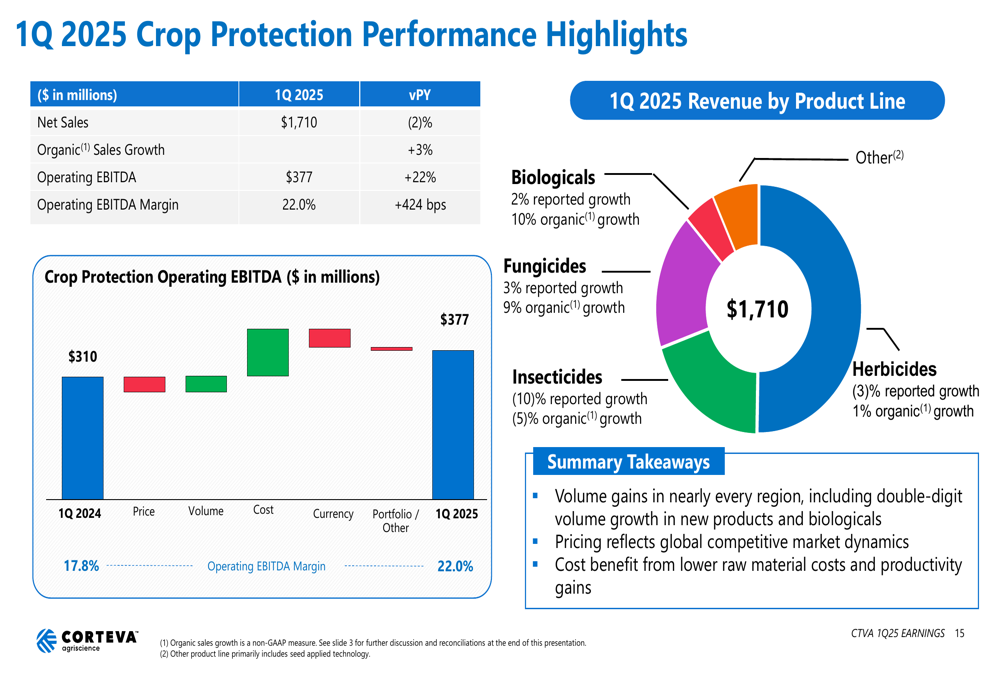

In the Crop Protection segment, net sales were $1.7 billion, down 2% year-over-year, but organic sales grew by 3%. Operating EBITDA increased by 22% to $377 million, with margin expanding to 22.0%. Volume gains were led by new products and biologicals, which showed 10% organic growth, while pricing reflected competitive pressures in select regions.

As illustrated in the Crop Protection performance highlights:

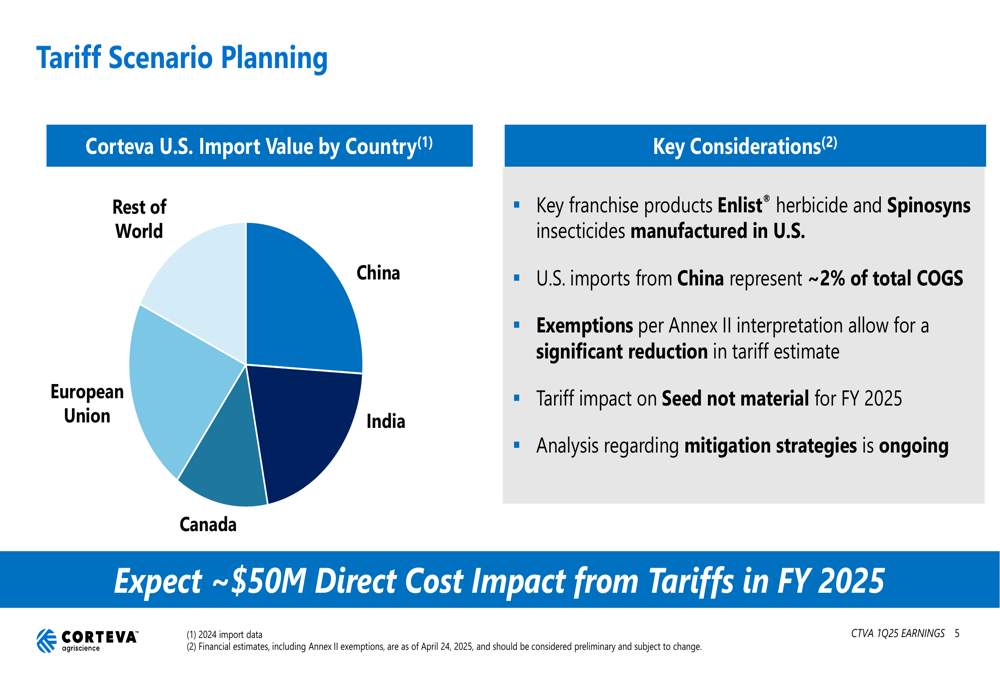

Tariff Impact Assessment

A notable focus of the presentation was Corteva’s analysis of potential tariff impacts on its business. The company expects approximately $50 million in direct cost impact from tariffs in FY 2025, with mitigation strategies currently under development.

The following chart provides a breakdown of Corteva’s tariff scenario planning:

The company noted that key franchise products like Enlist herbicide and Spinosyns insecticides are manufactured in the U.S., limiting exposure. U.S. imports from China represent approximately 2% of total cost of goods sold, and exemptions per Annex II interpretation allow for a significant reduction in the tariff estimate.

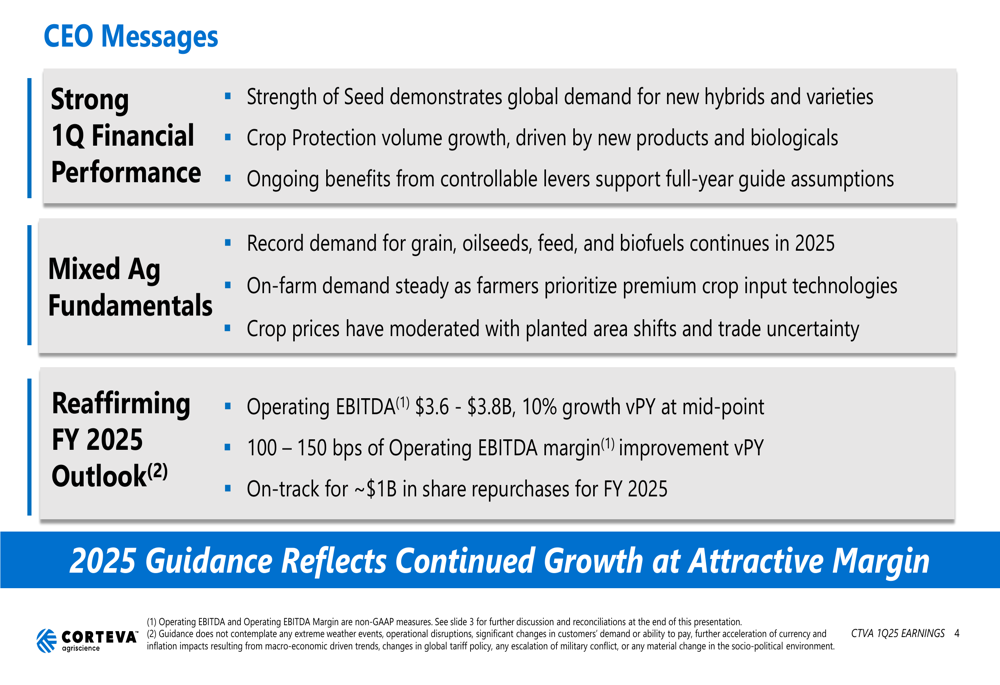

Forward-Looking Statements and Guidance

Corteva reaffirmed its full-year 2025 guidance, projecting operating EBITDA of $3.6-$3.8 billion, representing 10% growth at the midpoint compared to the previous year. The company also expects a 100-150 basis point improvement in operating EBITDA margin and remains on track for approximately $1 billion in share repurchases for FY 2025.

The CEO’s key messages highlighted strong financial performance and the company’s outlook:

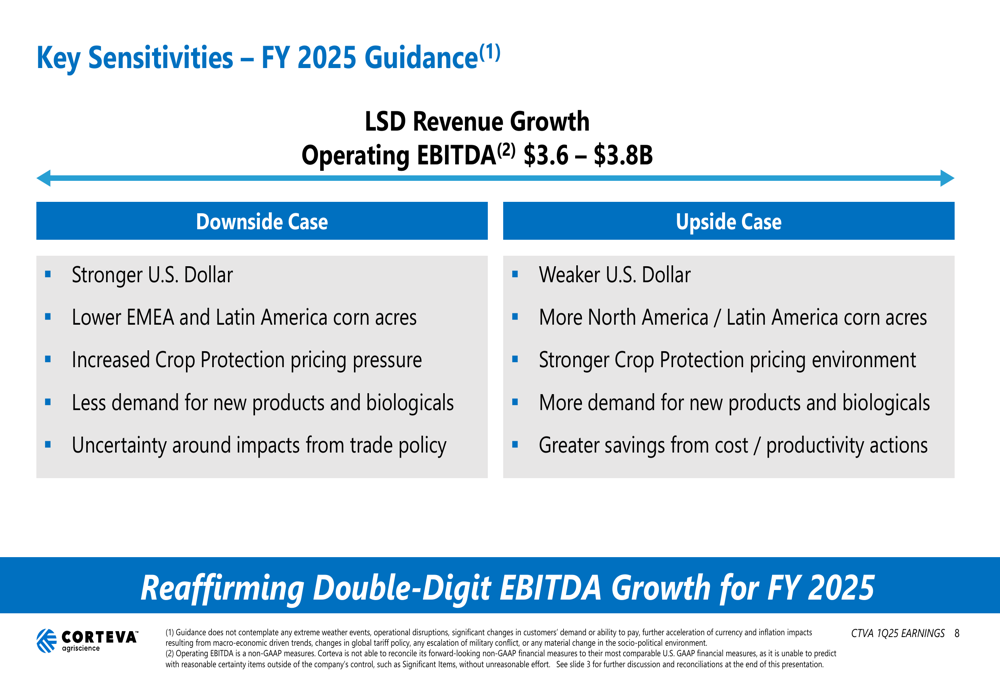

The company identified several key sensitivities that could impact its 2025 guidance, presenting both downside and upside scenarios:

Downside risks include a stronger U.S. dollar, lower corn acres in EMEA and Latin America, increased pricing pressure in Crop Protection, reduced demand for new products, and uncertainty around trade policy impacts. Upside potential could come from a weaker U.S. dollar, increased corn acres in North America and Latin America, a stronger pricing environment, higher demand for new products and biologicals, and greater cost savings.

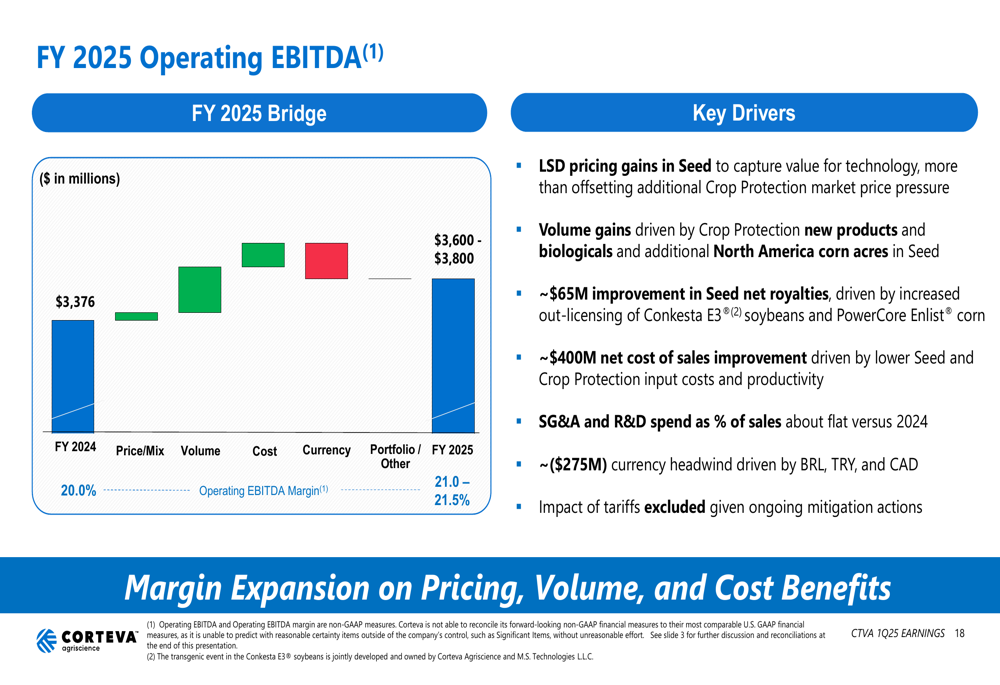

For the full year 2025, Corteva provided the following Operating EBITDA bridge, showing the expected drivers of growth:

The company expects its operating EPS to range between $2.70 and $2.95 for the full year 2025, with a base income tax rate of 22-24%.

In conclusion, Corteva’s Q1 2025 results demonstrate the company’s ability to drive margin expansion through productivity improvements and cost savings, even in the face of revenue challenges. By reaffirming its full-year guidance, Corteva signals confidence in its ability to navigate mixed agricultural fundamentals and potential tariff impacts while delivering double-digit EBITDA growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.