Trump to impose 100% tariff on China starting November 1

Introduction & Market Context

Costco Wholesale Corporation (NASDAQ:COST) released its fourth quarter fiscal 2025 supplemental information on September 25, showcasing strong performance across key metrics. The retail giant reported net sales of $84.4 billion, an 8.0% increase year-over-year, capping off a solid fiscal year despite ongoing economic uncertainties.

The company’s stock responded positively in after-hours trading, rising 0.74% to $952.30, following a slight decline of 0.26% during regular trading hours. This performance comes as Costco continues to execute on its expansion strategy and digital transformation initiatives.

Quarterly Performance Highlights

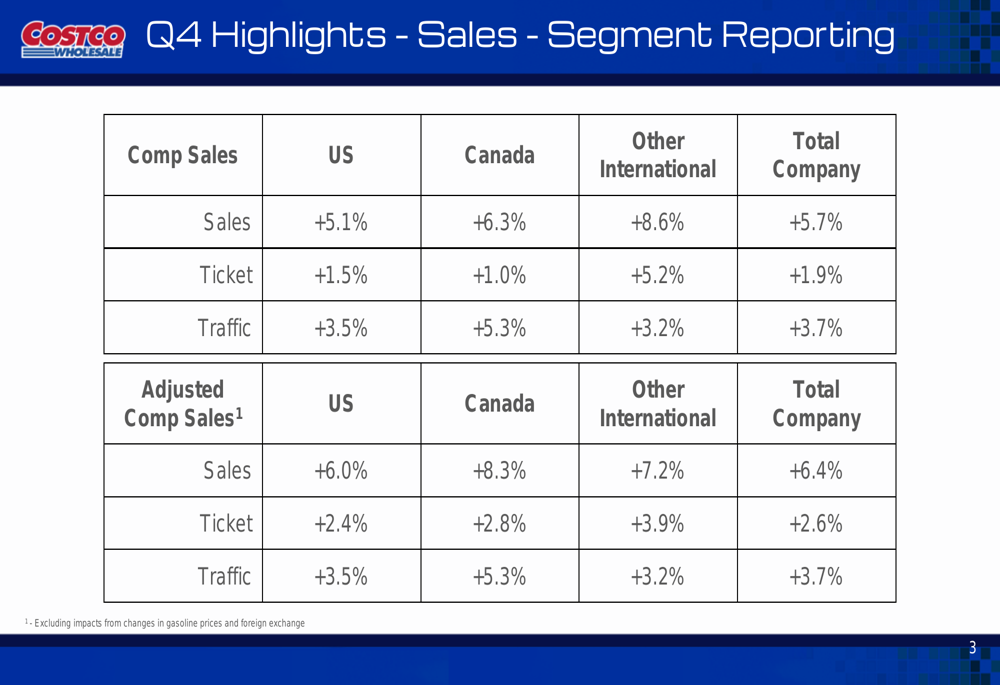

Costco’s Q4 results demonstrated robust growth across multiple metrics. Comparable sales increased 5.7%, or 6.4% when adjusted for impacts from gasoline prices and foreign exchange. The growth was driven by both higher traffic and larger average purchases, with comparable traffic up 3.7% and comparable ticket increasing 1.9% (2.6% adjusted).

As shown in the following chart of Costco’s Q4 sales performance:

The company’s performance varied by geographic region, with international markets showing particularly strong results. Other International segments posted comparable sales growth of 8.6%, outpacing the US at 5.1% and Canada at 6.3%. When adjusted for gasoline and foreign exchange impacts, Canada led with 8.3% growth.

The regional breakdown of comparable sales performance is illustrated here:

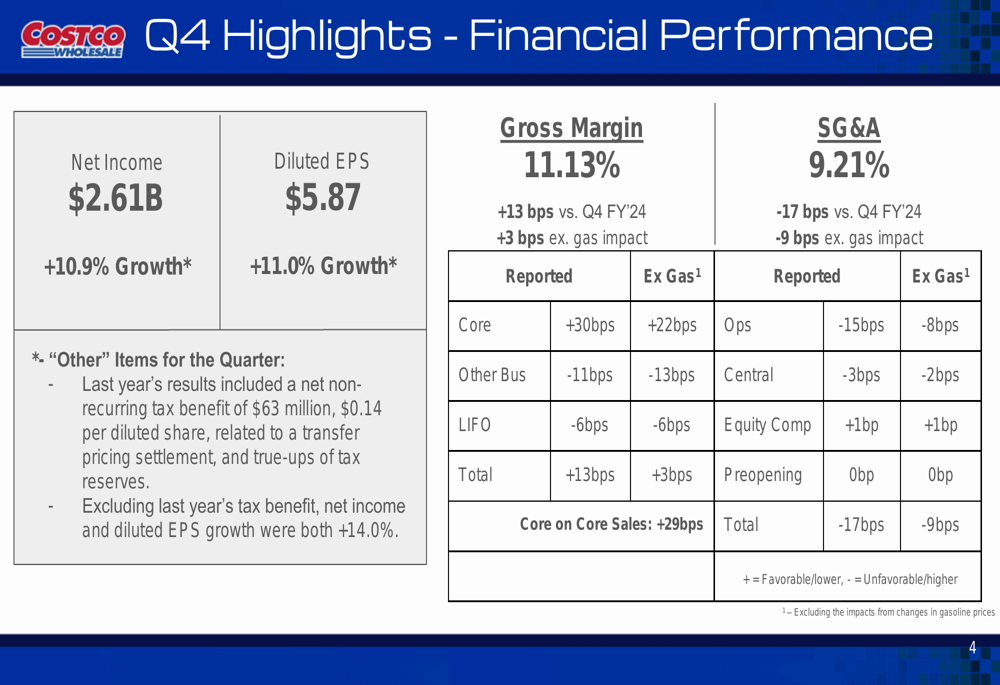

On the earnings front, Costco reported net income of $2.61 billion, representing a 10.9% increase compared to the same period last year. Diluted earnings per share reached $5.87, up 11.0% year-over-year. Notably, excluding last year’s tax benefit, both net income and EPS growth would have been even stronger at 14.0%.

Gross margin improved to 11.13%, up 13 basis points from Q4 FY’24, while SG&A expenses as a percentage of revenue decreased by 17 basis points to 9.21%, demonstrating the company’s operational efficiency.

The following financial performance highlights provide a detailed breakdown:

Membership Growth and Metrics

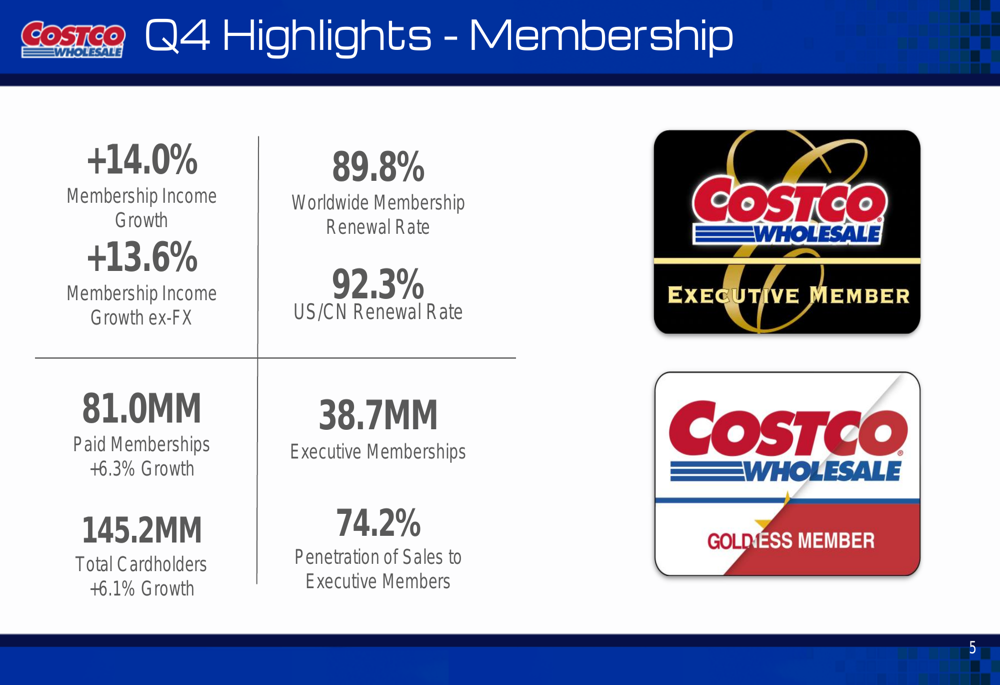

Membership income, a critical component of Costco’s business model, grew by 14.0% (13.6% excluding foreign exchange impacts), outpacing overall sales growth. This metric is particularly important as it represents a high-margin, recurring revenue stream for the company.

Costco’s membership metrics showed continued strength, with worldwide renewal rates reaching 89.8% and US/Canada renewal rates at an impressive 92.3%. Total paid memberships increased 6.3% to 81.0 million, while executive memberships, which generate higher average spending, reached 38.7 million. Executive members now account for 74.2% of Costco’s sales, highlighting the success of the company’s tiered membership strategy.

The following membership highlights illustrate these trends:

Digital and E-commerce Performance

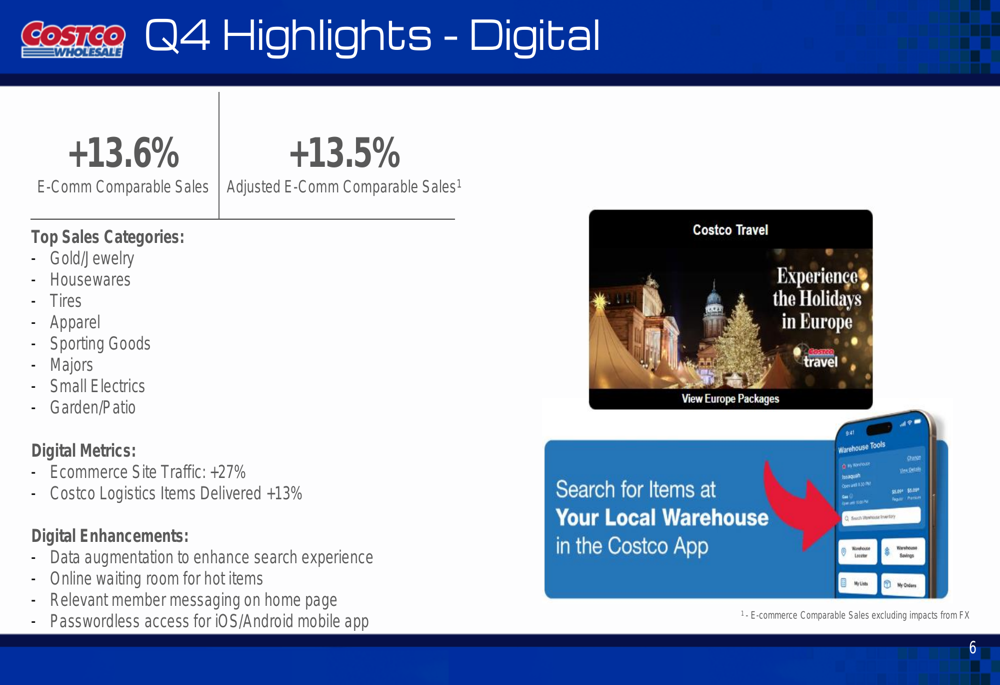

Costco’s digital initiatives continued to gain traction in Q4, with e-commerce comparable sales increasing by 13.6% (13.5% adjusted). This growth significantly outpaced overall company sales growth, reflecting the company’s successful omnichannel strategy.

Site traffic increased by 27%, while Costco Logistics items delivered grew by 13%. The company highlighted several digital enhancements, including data augmentation, an online waiting room feature, relevant member messaging, and passwordless access improvements.

Top-performing e-commerce categories included Gold/Jewelry, Housewares, Tires, Apparel, Sporting Goods, Majors, Small Electrics, and Garden/Patio, demonstrating broad-based strength across the digital platform.

The digital performance metrics and enhancements are shown here:

Expansion Strategy

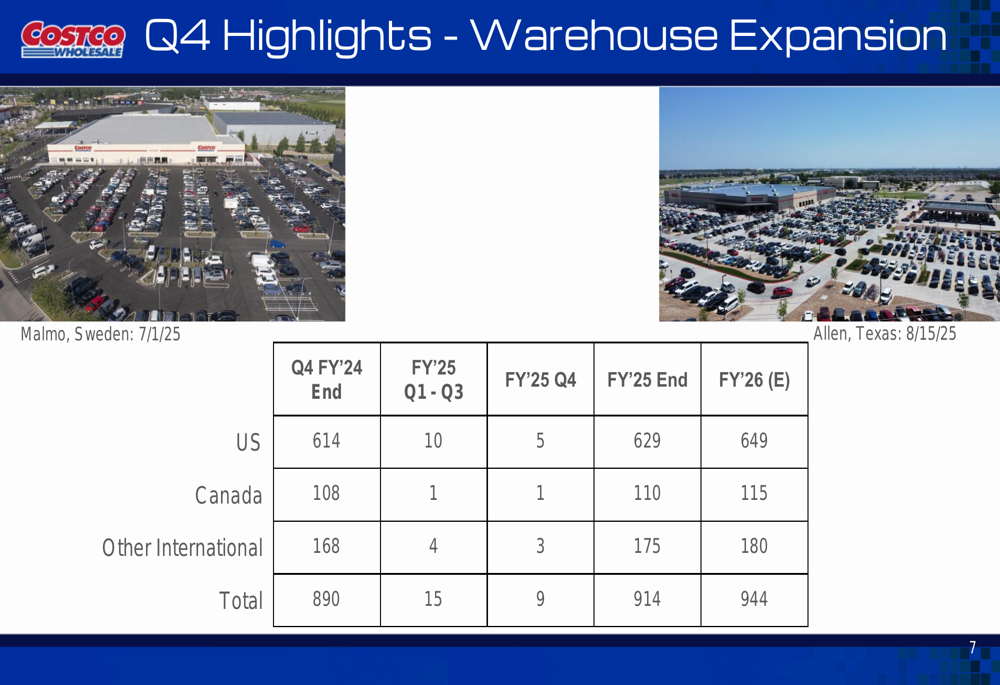

Costco continued its global expansion in Q4, adding new warehouses across multiple regions. The company ended FY 2025 with 922 warehouses globally, up from 890 at the end of FY 2024. The expansion included new locations in international markets, such as the Malmo, Sweden warehouse highlighted in the presentation.

For fiscal year 2026, Costco projects opening approximately 22 new warehouses, bringing its total to 944 locations worldwide. This measured expansion approach has been a hallmark of Costco’s growth strategy, allowing the company to maintain operational excellence while extending its geographic footprint.

The warehouse expansion plan is detailed in this chart:

The company also continues to expand its Kirkland Signature private label offerings, which provide value to members while delivering higher margins for Costco. The presentation highlighted several new Kirkland products, including organic food items and protein products.

As shown in these product highlights:

Forward-Looking Statements

Looking ahead, Costco appears well-positioned for continued growth in fiscal year 2026. The company’s strong membership metrics, expanding warehouse footprint, and growing digital presence provide multiple avenues for revenue growth.

The Q4 results represent an acceleration from the Q3 performance reported earlier, where the company posted net income of $1.9 billion and EPS of $4.28. The sequential improvement in key metrics suggests Costco’s business momentum is building as it enters the new fiscal year.

With a current stock price near $952 and a 52-week range of $867.16 to $1,078.23, Costco continues to trade at a premium valuation compared to many retailers, reflecting investor confidence in the company’s business model and growth prospects. The combination of membership growth, warehouse expansion, and digital acceleration provides a solid foundation for continued performance in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.