Caesars Entertainment misses Q2 earnings expectations, shares edge lower

Introduction & Market Context

Couchbase Inc (NASDAQ:BASE) presented its Q1 fiscal year 2026 investor presentation on June 3, 2025, highlighting continued growth in a rapidly evolving database market. The company’s stock closed at $18.35, up 1.14% during regular trading, and gained an additional 2.07% in after-hours trading, reflecting positive investor sentiment following the results.

The presentation emphasized Couchbase’s position in the database market, which is projected to reach $149.6 billion by 2028 according to IDC data. The company highlighted the ongoing market transition from traditional relational databases to cloud-based, multi-purpose platforms capable of supporting AI-driven applications.

Quarterly Performance Highlights

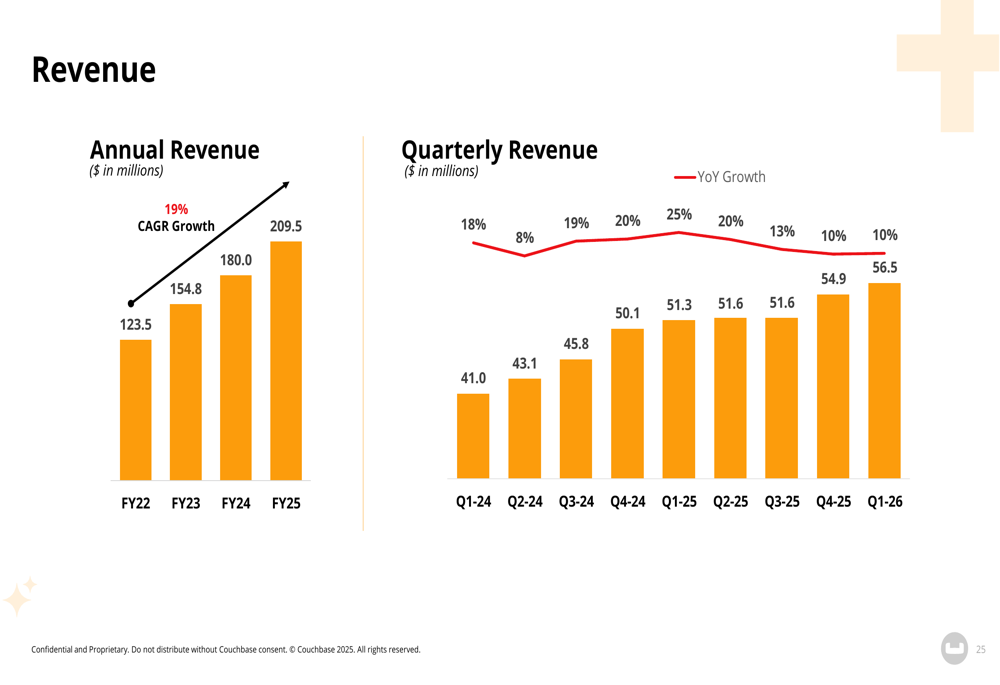

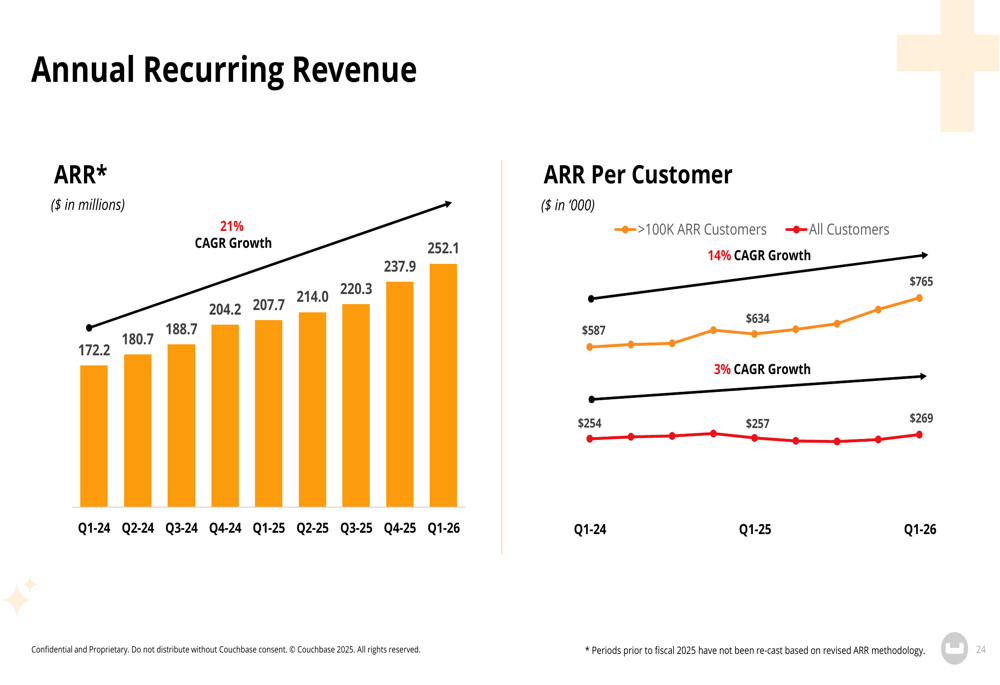

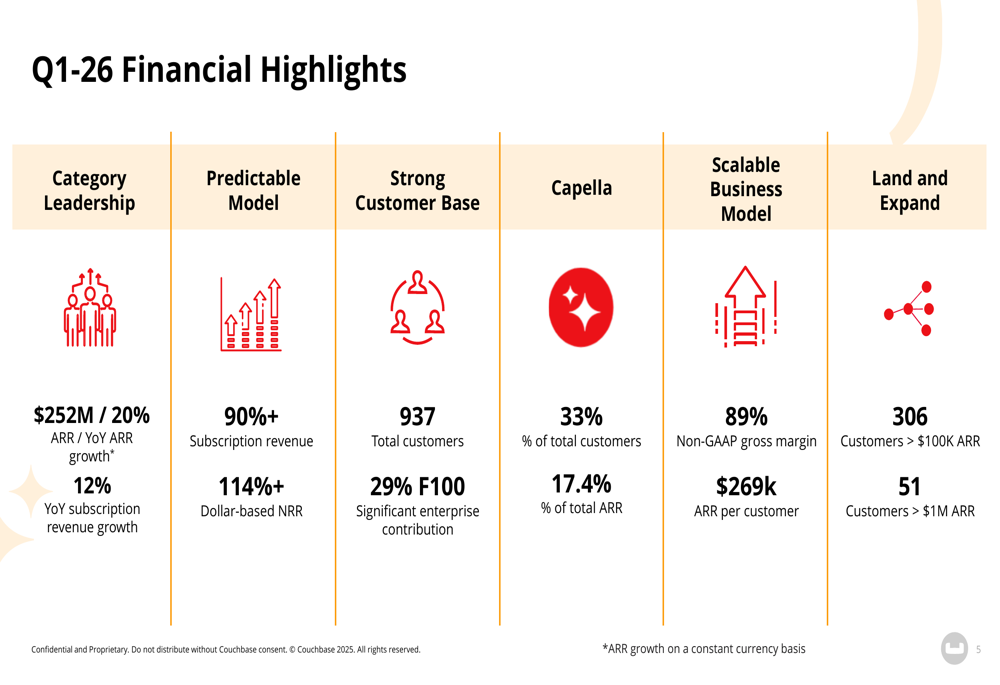

Couchbase reported solid financial performance for Q1 FY26, with annual recurring revenue (ARR) reaching $252.1 million, representing 20% year-over-year growth. Revenue for the quarter came in at $56.5 million, up 10% compared to the same period last year, continuing the trend seen in Q4 FY25.

As shown in the following chart of quarterly revenue growth:

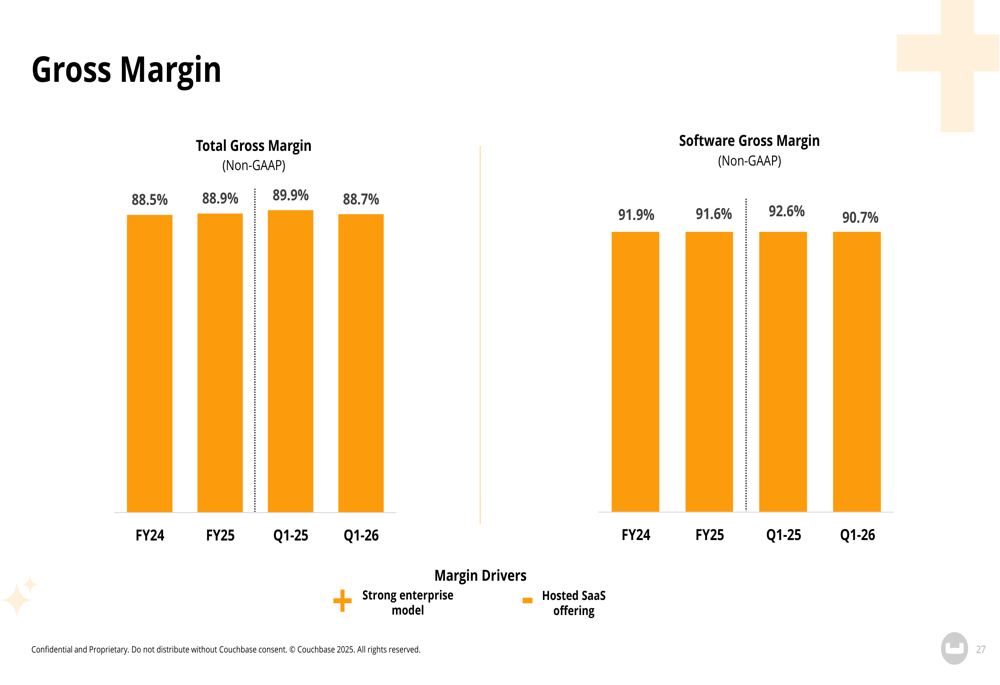

The company maintained impressive gross margins of 88.7% on a non-GAAP basis in Q1 FY26, demonstrating the efficiency of its business model despite ongoing investments in cloud infrastructure for its Capella database-as-a-service offering.

Couchbase’s customer metrics also showed positive momentum, with 937 total customers, including 29% of Fortune 100 companies. The company reported 306 customers with ARR exceeding $100,000 and 51 customers with ARR over $1 million, highlighting its success with enterprise clients. Average ARR per customer increased to $269,000, up from $257,000 in the previous year.

The company’s Q1 financial highlights demonstrate strong performance across key metrics:

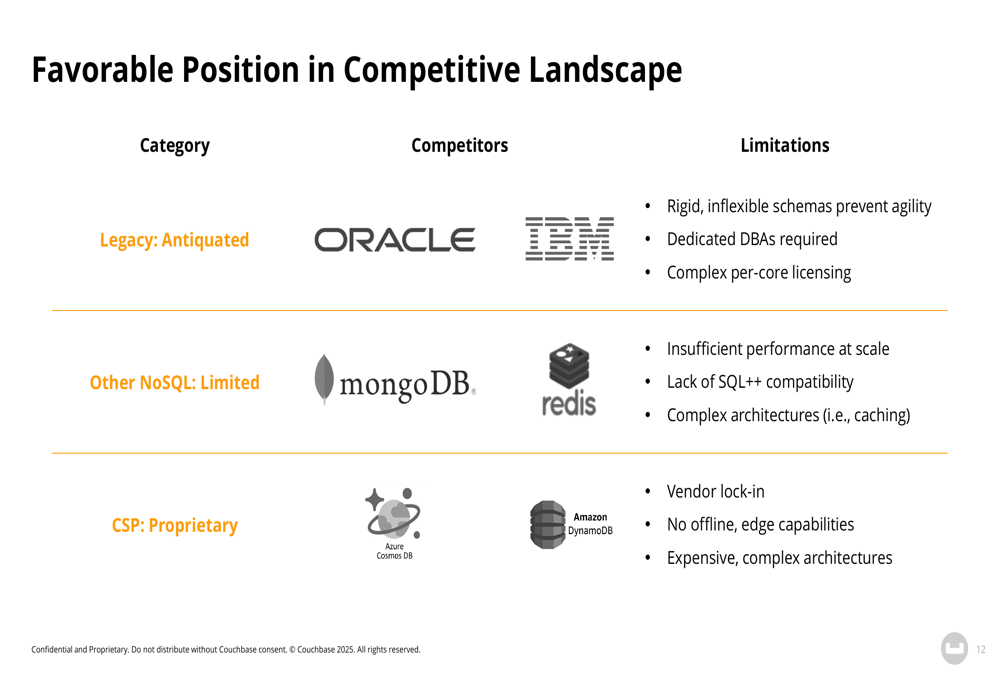

Competitive Industry Position

Couchbase positioned itself as a differentiated player in the database market, contrasting its offerings with legacy relational databases (Oracle (NYSE:ORCL), IBM (NYSE:IBM)), other NoSQL solutions ( MongoDB (NASDAQ:MDB), Redis), and cloud service provider databases (Azure Cosmos DB, Amazon (NASDAQ:AMZN) DynamoDB).

The company emphasized its competitive advantages, including performance at scale, SQL++ compatibility, and cross-platform capabilities that avoid vendor lock-in. These differentiators are particularly important as organizations increasingly adopt AI-driven applications that require flexible, high-performance database solutions.

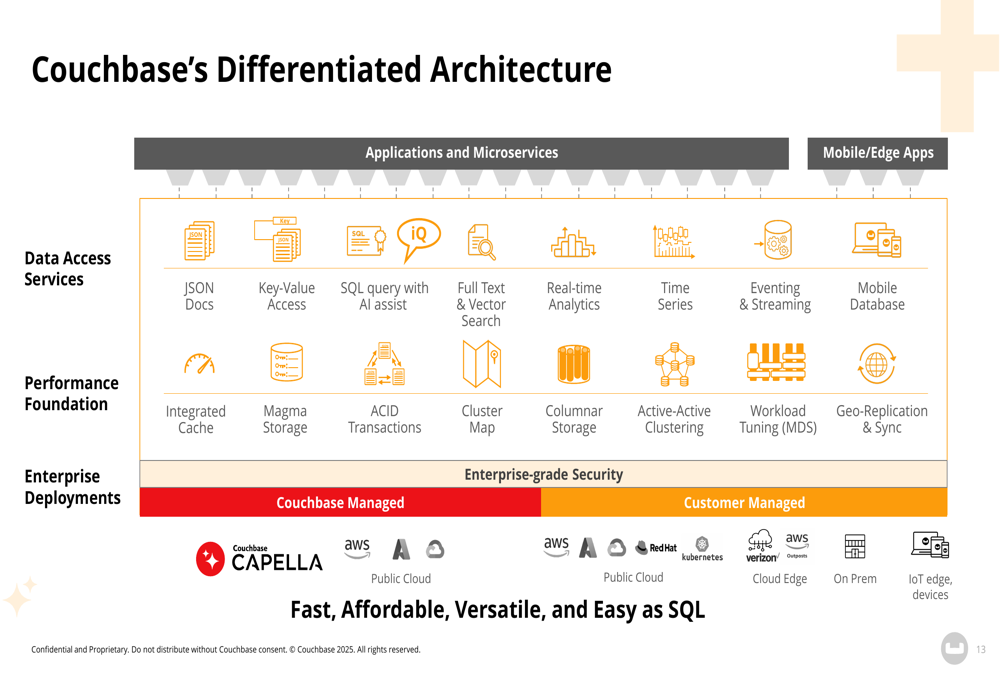

Couchbase’s architecture is designed to support diverse workloads across multiple deployment environments, from public clouds to edge devices. This versatility is a key selling point as companies seek to unify their database infrastructure.

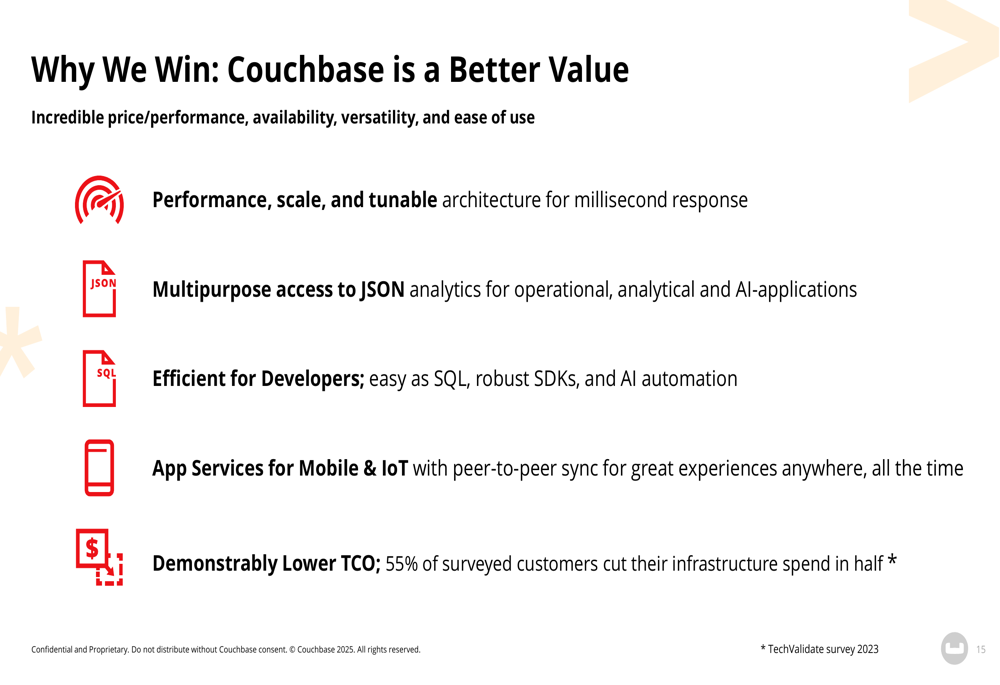

The company’s value proposition centers on performance, flexibility, developer efficiency, mobile/IoT capabilities, and lower total cost of ownership. According to a TechValidate survey cited in the presentation, 55% of surveyed customers cut their infrastructure spend in half by adopting Couchbase.

Strategic Initiatives

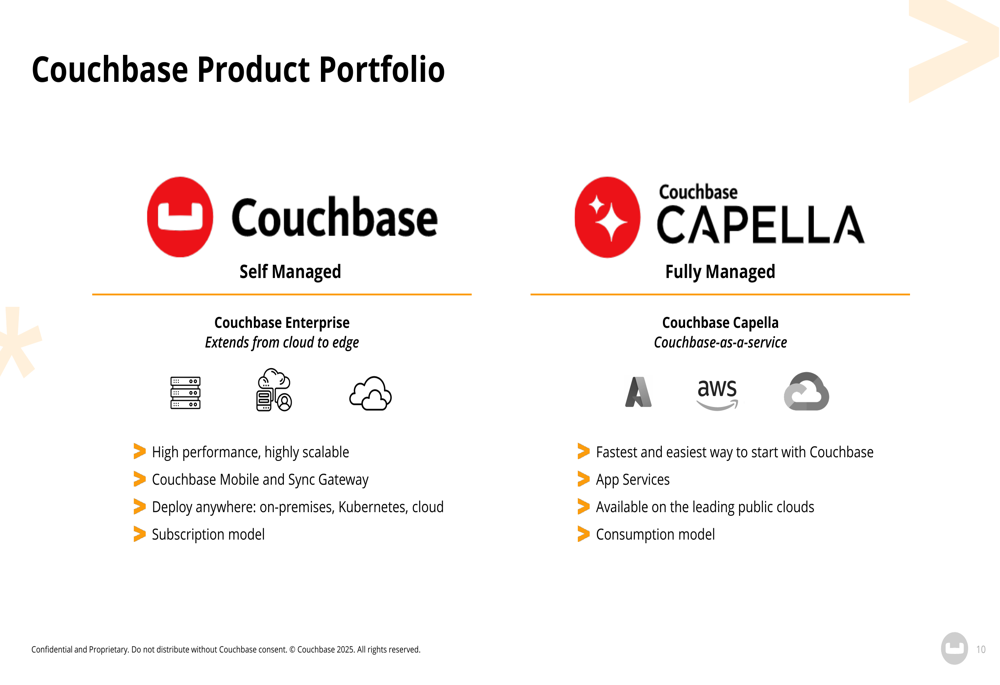

Couchbase’s strategic focus continues to be on its Capella database-as-a-service offering, which represented 33% of total customers and 17.4% of total ARR in Q1 FY26. This fully managed cloud service is available on AWS, Azure, and Google (NASDAQ:GOOGL) Cloud, providing customers with deployment flexibility while simplifying database management.

The company is also emphasizing its capabilities for AI-driven applications, including vector search and AI services introduced in 2024. These features position Couchbase to capitalize on the growing demand for database solutions that can effectively support AI workloads alongside traditional transactional and analytical processing.

Couchbase’s go-to-market strategy combines product-led growth (PLG) with traditional enterprise sales motions. The PLG approach focuses on self-serve trials and developer community engagement, while the enterprise sales motion targets larger accounts through proof-of-concept projects and expansion opportunities.

Forward-Looking Statements

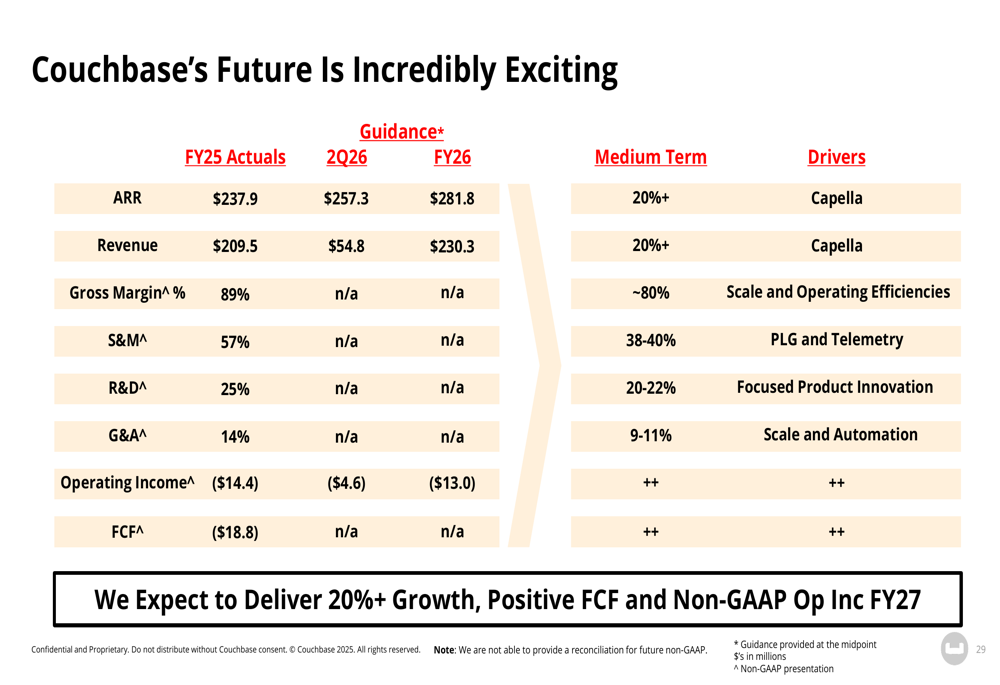

Looking ahead, Couchbase provided guidance for Q2 FY26 with expected ARR of $257.3 million and revenue of $54.8 million. For the full fiscal year 2026, the company forecasts ARR of $281.8 million and revenue of $230.3 million.

The company’s long-term financial targets include 20%+ growth for both ARR and revenue, driven primarily by Capella adoption. Couchbase aims to improve operating efficiency across all expense categories, with targets including gross margin of approximately 80%, sales and marketing at 38-40% of revenue (down from 57% in FY25), and R&D at 20-22% of revenue (down from 25%).

Most significantly, Couchbase expects to achieve positive free cash flow and non-GAAP operating income by FY27, marking an important milestone in the company’s path to profitability. This aligns with statements made during the Q4 FY25 earnings call, where management indicated progress toward these financial goals.

The database market’s ongoing evolution, particularly with the rise of AI-driven applications, presents significant growth opportunities for Couchbase. With its differentiated architecture, strong enterprise customer base, and expanding cloud offerings, the company appears well-positioned to capitalize on these trends while improving its financial profile over the coming years.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.