Fubotv earnings beat by $0.10, revenue topped estimates

Introduction & Market Context

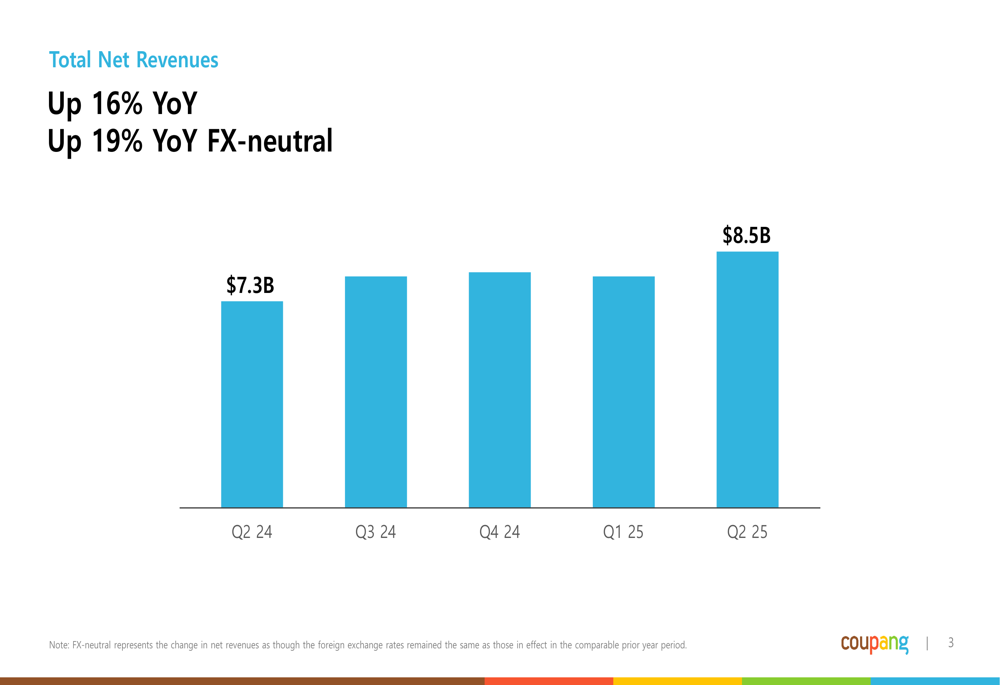

Coupang LLC (NYSE:CPNG) released its Q2 2025 financial results on August 5, 2025, showcasing continued revenue growth and improved profitability metrics. The South Korean e-commerce giant reported total net revenues of $8.5 billion, representing a 16% year-over-year increase (19% on an FX-neutral basis). The company’s stock closed at $29.63 on the day of the announcement, up 0.91% from the previous close, with minimal movement in after-hours trading.

The Q2 results demonstrate a significant improvement from Q1 2025, when Coupang missed analyst expectations with revenue of $7.91 billion and earnings per share of $0.06. The latest quarterly performance suggests the company is successfully executing its growth strategy while enhancing operational efficiency.

Quarterly Performance Highlights

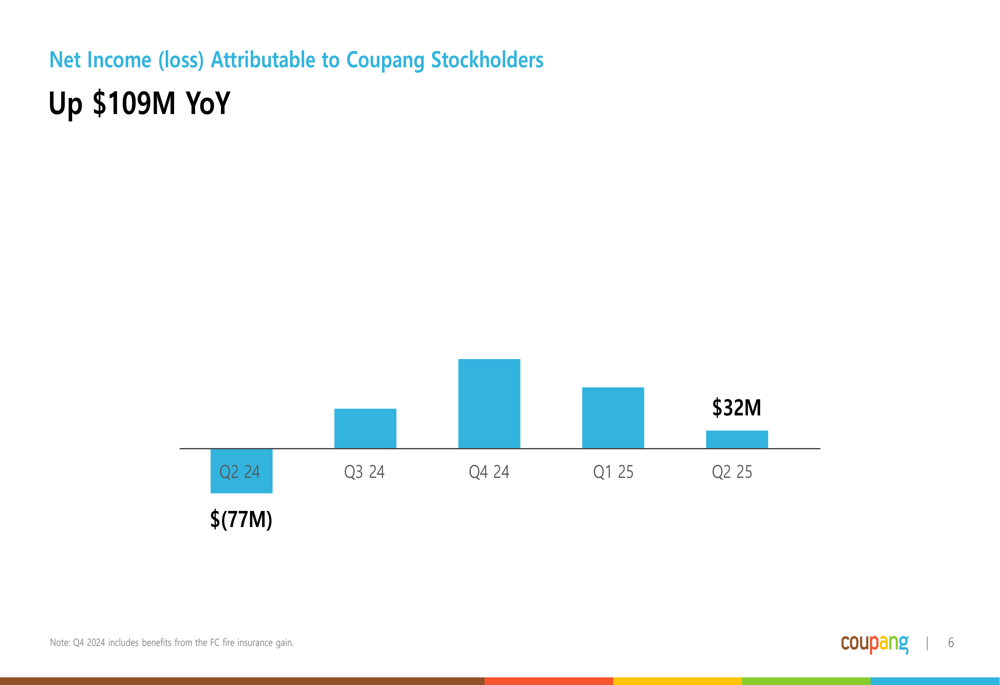

Coupang’s Q2 2025 results show a marked improvement in profitability, with the company reporting net income of $32 million, a $109 million improvement from the $77 million loss recorded in Q2 2024. This transition to profitability comes alongside continued revenue growth and margin expansion.

As shown in the following chart of quarterly revenue growth:

Gross profit for Q2 2025 reached $2.6 billion, up 20% year-over-year (22% FX-neutral), with gross profit margin expanding by 79 basis points to 30.0%. This continues the positive trend seen in Q1, when the company reported a gross profit margin of 29.3%.

The following chart illustrates the company’s improving gross profit and margin:

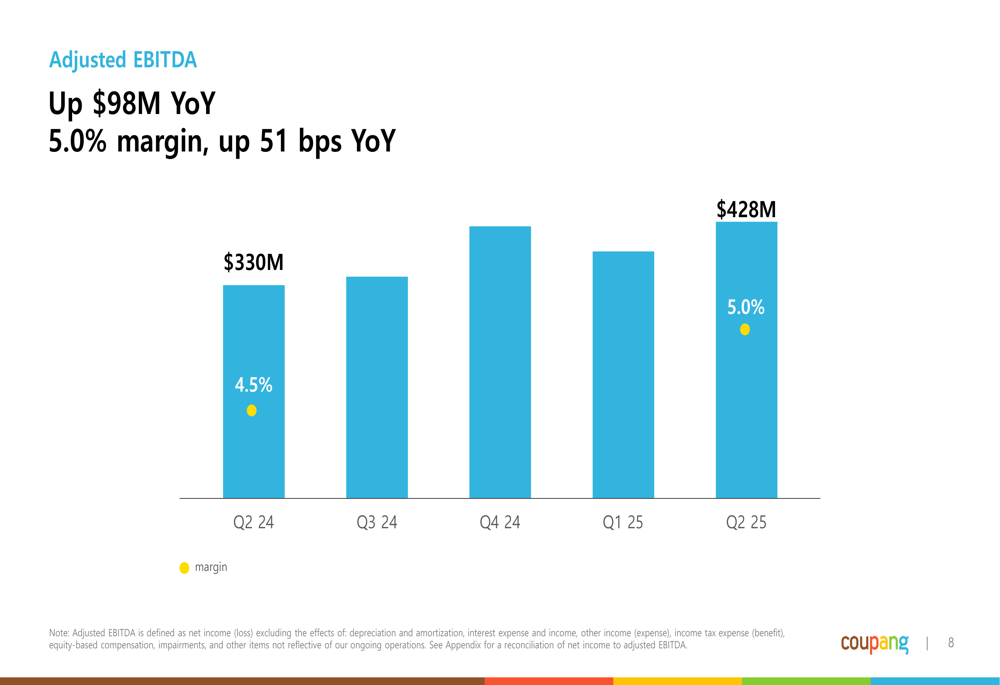

Adjusted EBITDA, a key measure of operational performance, increased by $98 million year-over-year to $425 million in Q2 2025, with the margin improving by 51 basis points to 5.0%.

Detailed Financial Analysis

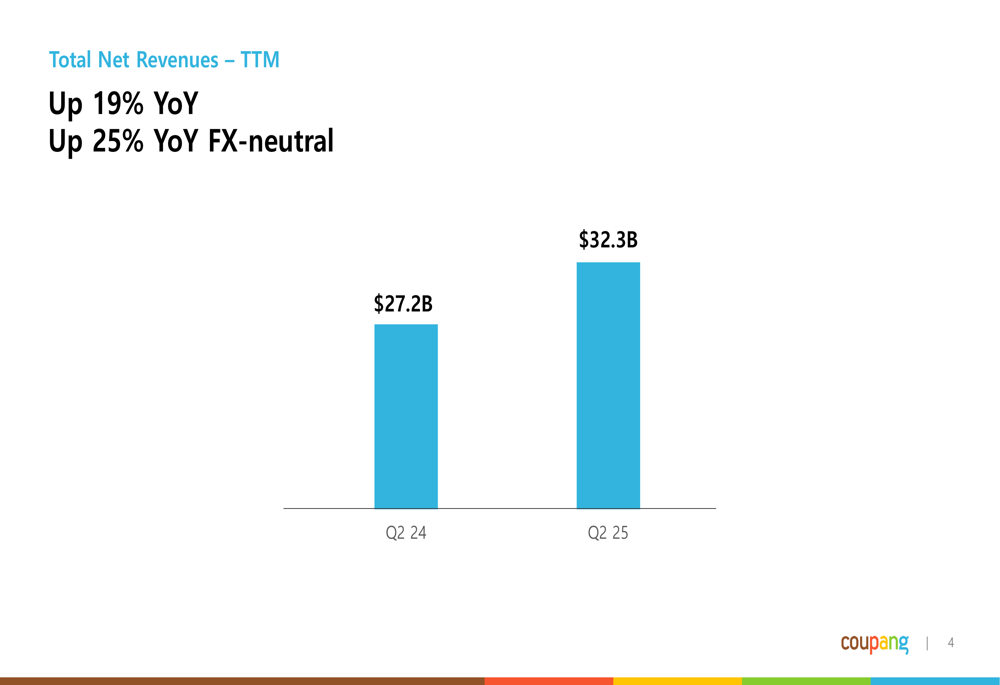

On a trailing twelve-month (TTM) basis, Coupang’s financial performance shows strong revenue growth but mixed results in profitability metrics. Total (EPA:TTEF) net revenues reached $32.3 billion, up 19% year-over-year (25% FX-neutral).

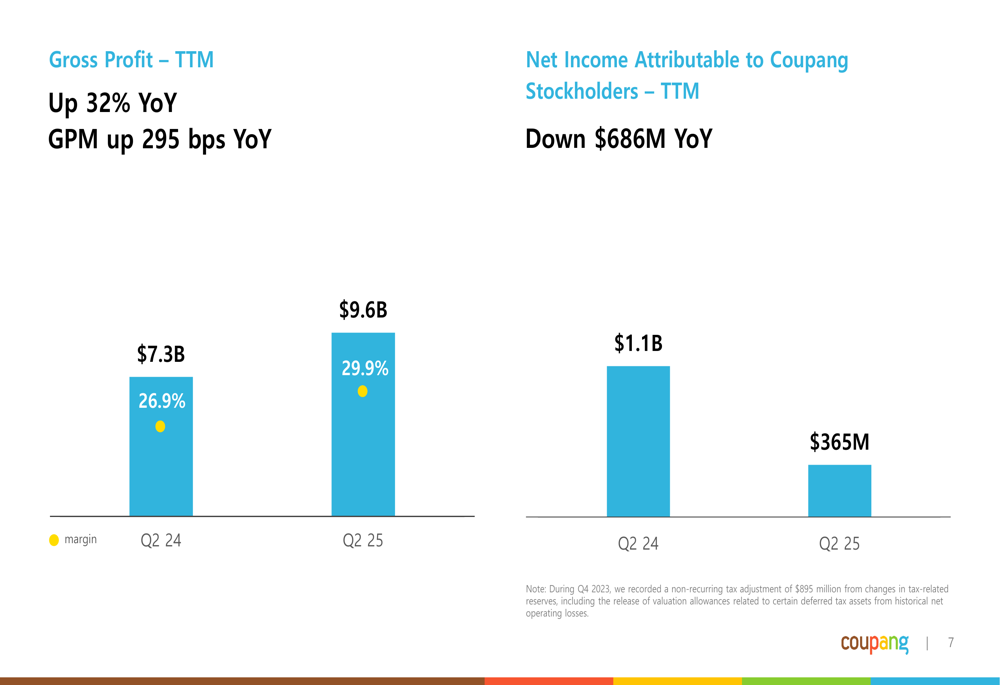

Gross profit on a TTM basis grew to $9.6 billion, up 32% year-over-year, with gross profit margin expanding by 295 basis points to 29.9%. However, TTM net income declined to $365 million from $1.1 billion in the comparable period last year, representing a $686 million decrease. This decline was partially attributed to a non-recurring tax adjustment of $895 million recorded in Q4 2023.

The following chart shows the comparison between TTM gross profit and net income:

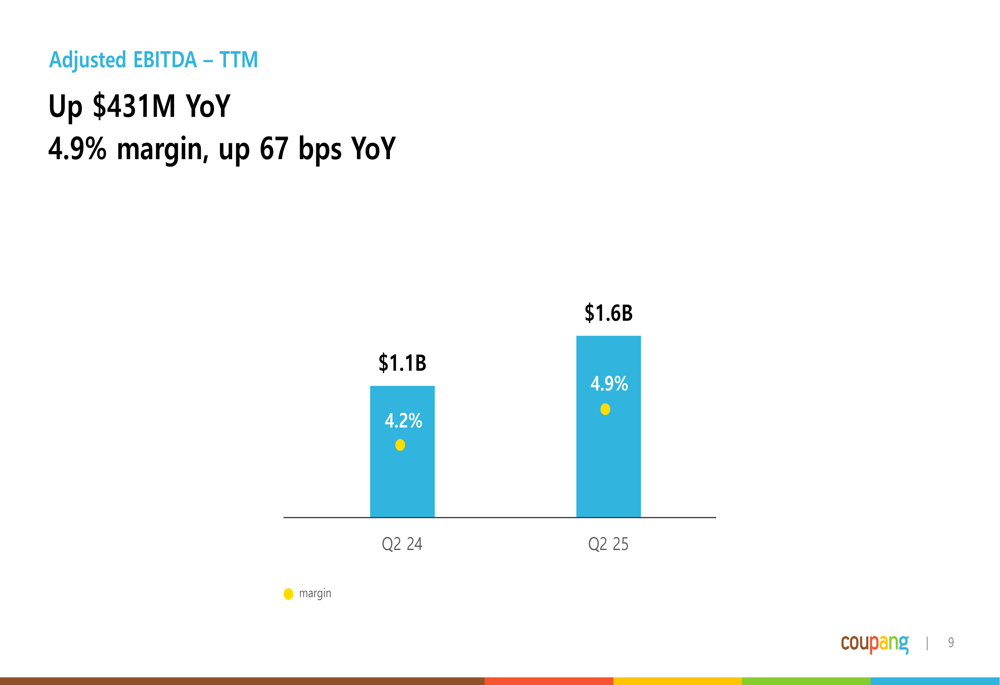

Adjusted EBITDA on a TTM basis showed strong improvement, increasing by $431 million year-over-year to $1.6 billion, with the margin expanding by 67 basis points to 4.9%.

Segment Performance

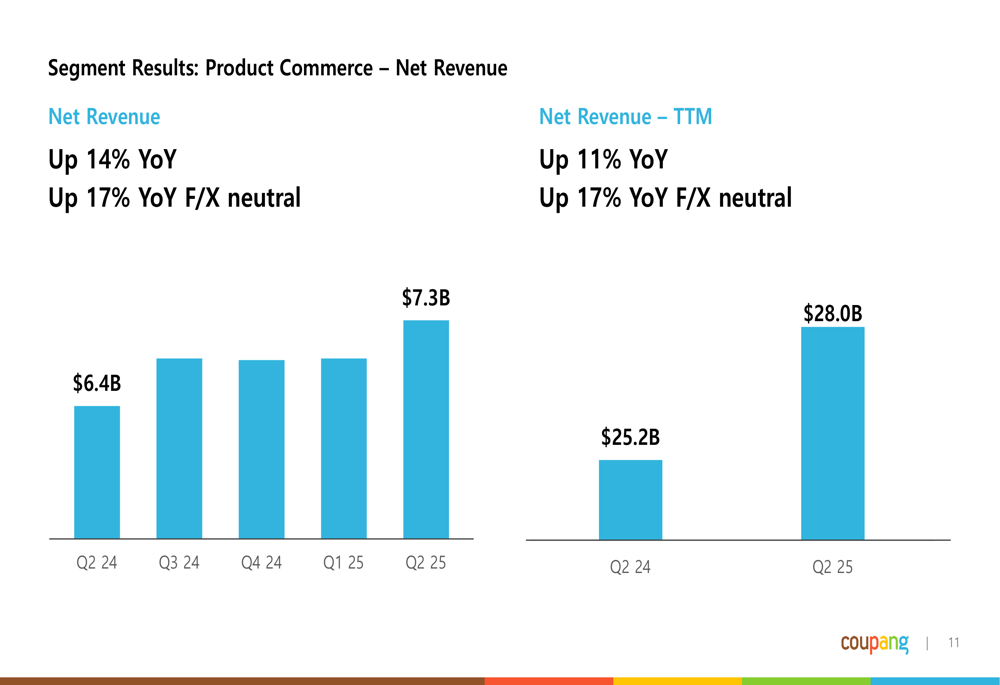

Coupang’s business is divided into two main segments: Product Commerce and Developing Offerings. The Product Commerce segment, which represents the company’s core e-commerce business, reported net revenue of $7.3 billion in Q2 2025, up 14% year-over-year (17% FX-neutral).

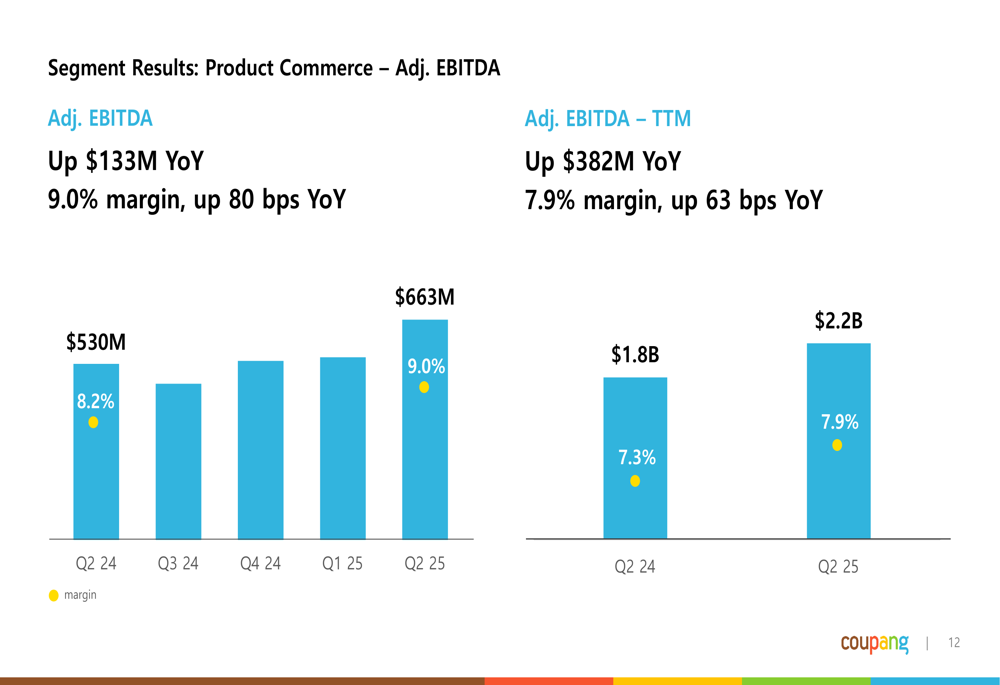

Product Commerce Adjusted EBITDA reached $663 million, up $133 million year-over-year, with the margin improving by 80 basis points to 9.0%. This segment continues to be the primary profit driver for the company.

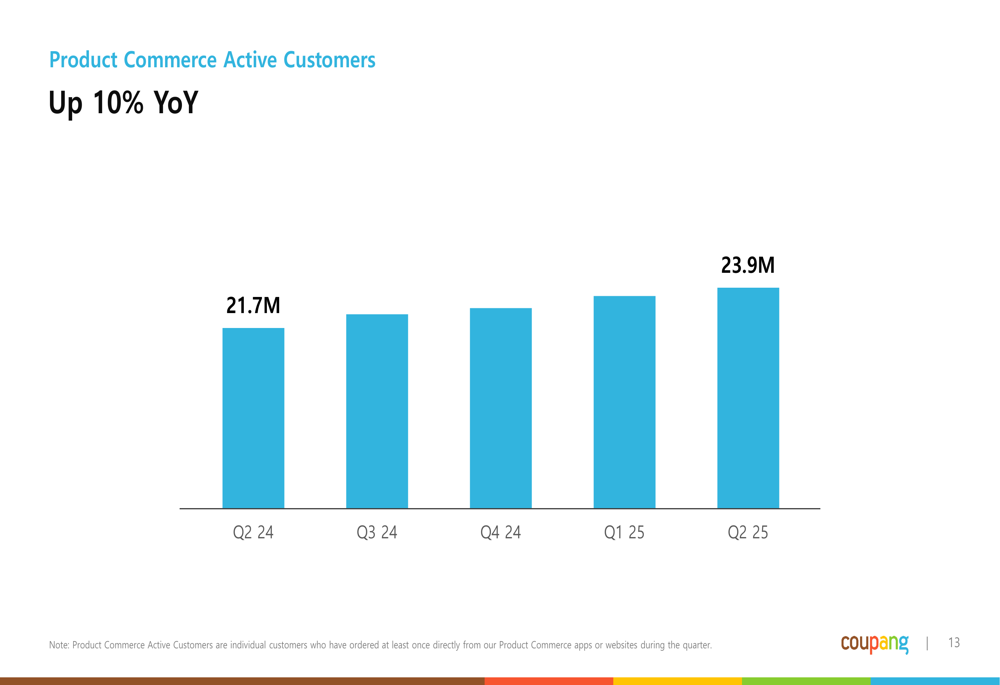

The Product Commerce segment also showed healthy customer growth, with active customers increasing by 10% year-over-year to 23.9 million.

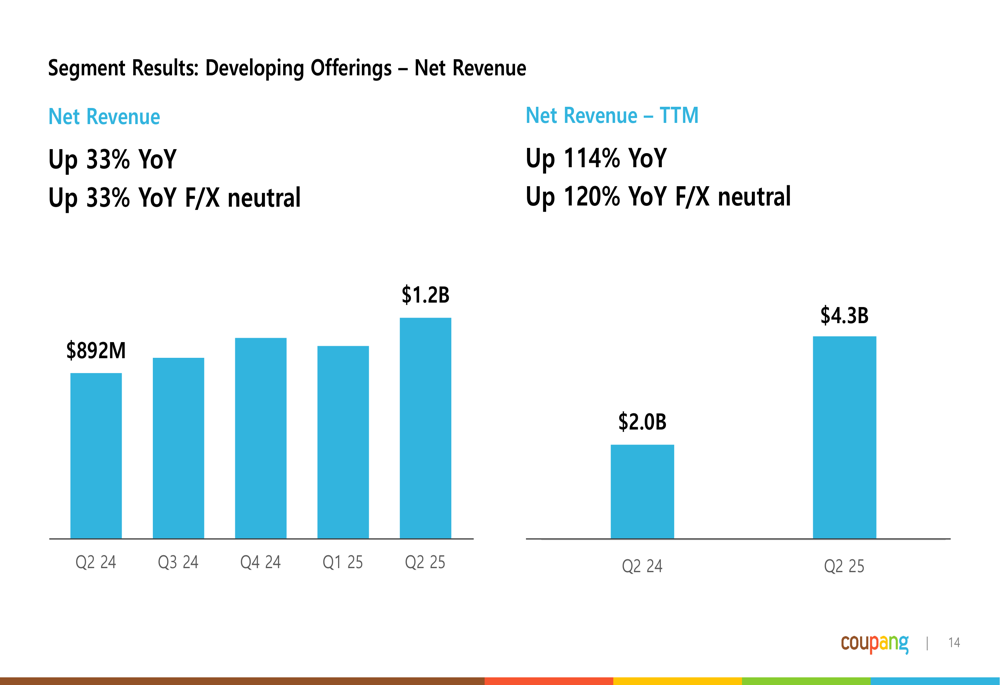

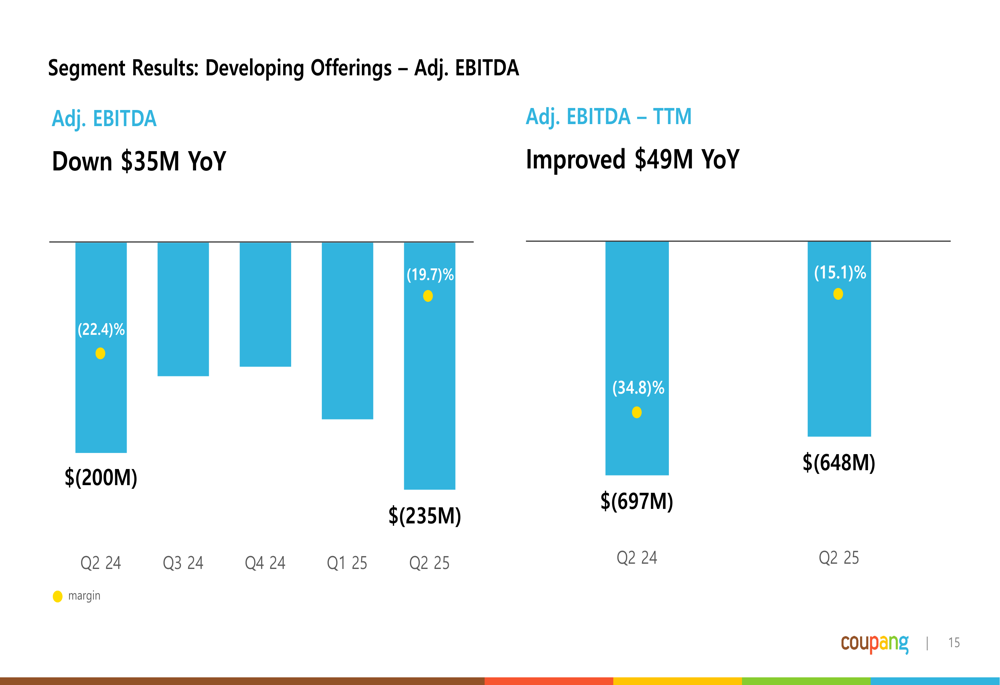

Meanwhile, the Developing Offerings segment, which includes newer initiatives such as food delivery and fintech services, reported strong revenue growth of 33% year-over-year to $1.2 billion in Q2 2025.

However, the Developing Offerings segment continues to operate at a loss, with Adjusted EBITDA declining by $35 million year-over-year to negative $235 million. Despite the increased loss, the margin improved by 270 basis points to negative 19.7%, suggesting progress toward eventual profitability.

Cash Flow and Capital Allocation

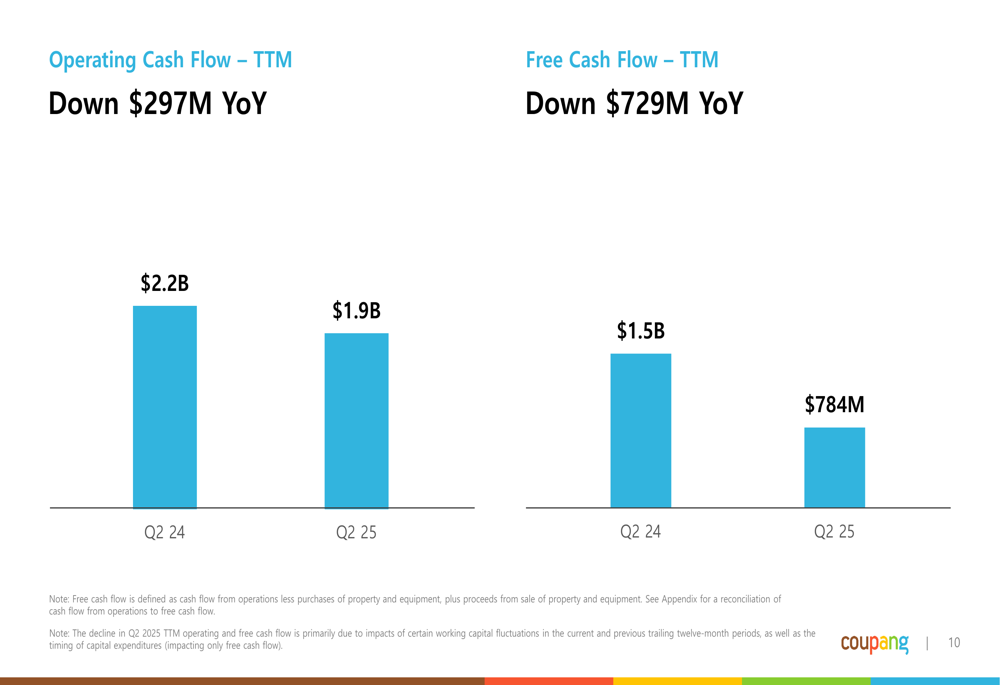

Despite the improving profitability metrics, Coupang’s cash flow performance showed some concerning trends. Operating cash flow on a TTM basis declined by $297 million year-over-year to $1.9 billion, while free cash flow decreased by $729 million to $784 million.

The significant decline in free cash flow suggests increased capital expenditures, potentially related to the company’s expansion initiatives. This aligns with Coupang’s previously announced strategic investments, including the expansion into Taiwan mentioned in the Q1 2025 earnings call.

Forward-Looking Statements

Coupang’s operating tenets, as outlined in the presentation, emphasize the company’s focus on delivering exceptional customer experiences while maintaining disciplined capital allocation. The company prioritizes growth in long-term cash flows and employs technology, process innovation, and economies of scale to drive operating leverage.

While the presentation does not provide specific forward guidance, the Q1 2025 earnings call indicated that Coupang maintains a full-year constant currency consolidated growth target of 20%. The company also expected its developing offerings to incur an adjusted EBITDA loss of $650-750 million, which appears to be on track based on the Q2 results.

The continued expansion of gross profit margins and the transition to profitability suggest that Coupang is making progress toward its long-term margin projections of above 10%. However, the declining cash flow metrics bear watching, as they could impact the company’s ability to fund future growth initiatives while maintaining its recently announced $1 billion share repurchase program.

As Coupang continues to balance growth investments with profitability improvements, investors will be closely monitoring whether the company can maintain its revenue momentum while further enhancing its bottom-line performance in the competitive e-commerce landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.