Intel shares rise as Elon Musk touts potential Tesla chipmaking deal

Covestro AG (OTC:COVTY) presented its third-quarter 2025 financial results on October 30, highlighting the company’s efforts to mitigate challenging market conditions through cost-saving initiatives. The chemical manufacturer reported a 12% year-over-year sales decline to €3.2 billion, while EBITDA fell 15.7% to €242 million.

Quarterly Performance Highlights

Covestro’s Q3 2025 results reflect ongoing economic challenges across key markets, particularly in Europe. Despite these headwinds, the company maintained a positive free operating cash flow of €111 million for the quarter.

As shown in the following financial overview:

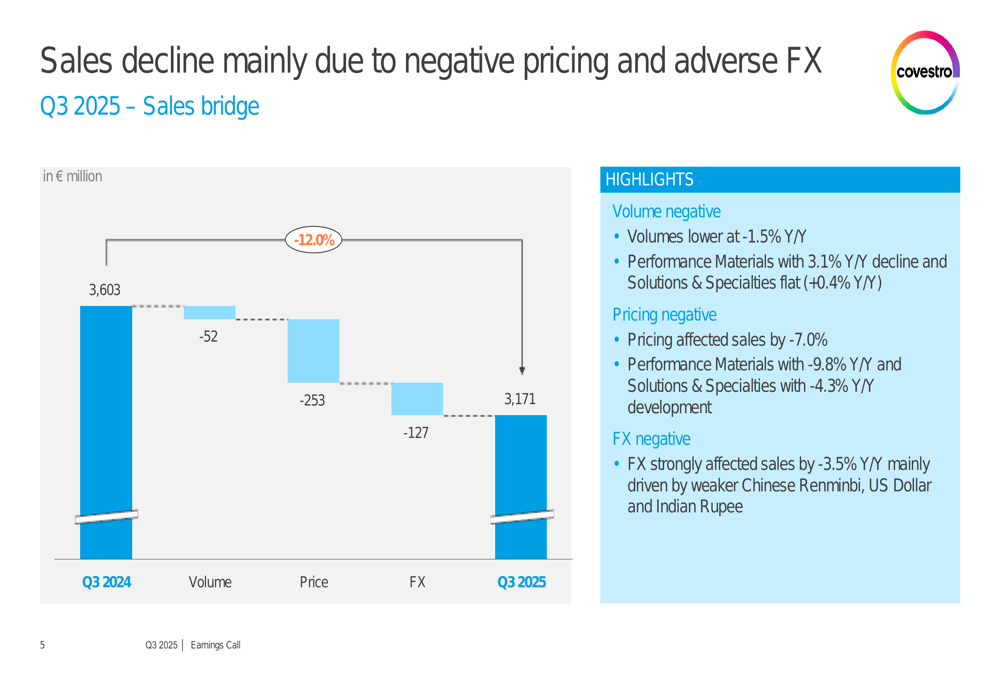

The sales decline was primarily attributed to negative pricing (-7.0%), adverse foreign exchange impacts (-3.5%), and lower volumes (-1.5%). The company’s performance was particularly affected by weakness in the EMLA (Europe, Middle East, and Africa) region, where volumes decreased by 8.0% year-over-year.

The following waterfall chart illustrates the components of Covestro’s sales decline:

On the EBITDA front, Covestro’s results were stabilized by self-help measures that partially offset negative market impacts. While pricing delta (-€102 million) and raw material costs (-€253 million) significantly pressured earnings, the company achieved €88 million in positive contributions from cost contingencies and structural savings.

This breakdown of EBITDA development demonstrates how cost-saving initiatives helped cushion market headwinds:

Segment Performance Analysis

Covestro’s two main business segments showed divergent performance patterns during Q3 2025.

The Solutions & Specialties segment experienced a 7.7% year-over-year sales decline, driven by lower prices (-4.3%) and negative foreign exchange impacts (-3.8%), while volumes remained essentially flat (+0.4%). Despite these challenges, the segment’s EBITDA margin improved to 12.0%.

The Performance Materials segment faced more significant headwinds with a 16.2% sales decline, resulting from lower prices (-9.8%), reduced volumes (-3.1%), and negative currency effects (-3.3%). However, the segment’s EBITDA was bolstered by a €75 million internal insurance booking related to the Dormagen incident, helping to increase the EBITDA margin to 11.7%.

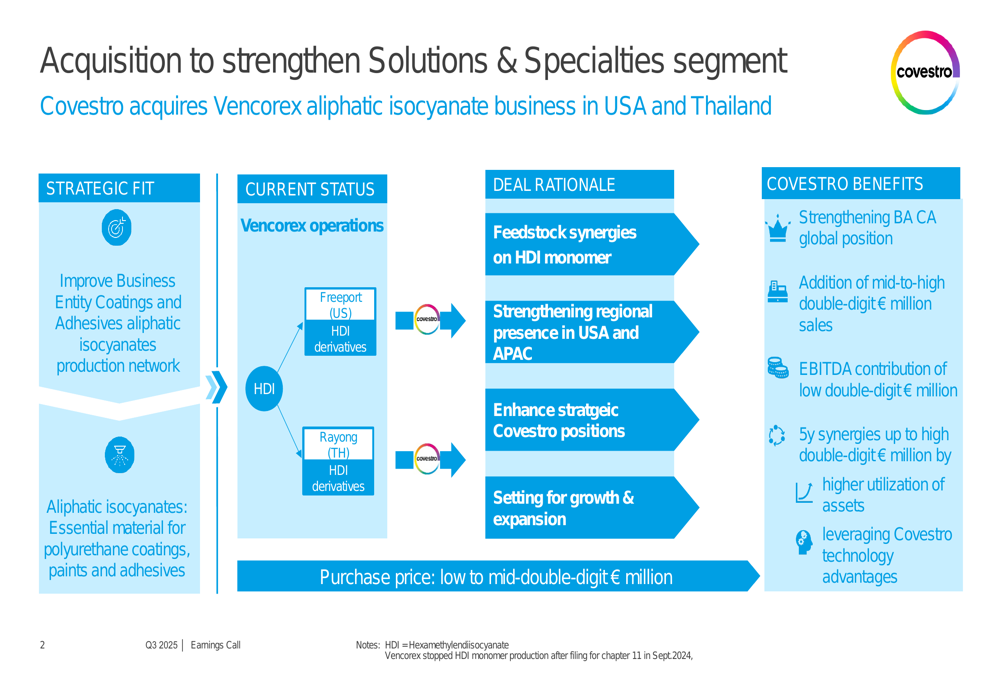

Strategic Initiatives & Acquisitions

Despite market challenges, Covestro continues to pursue strategic growth opportunities. The company announced the acquisition of Vencorex’s aliphatic isocyanate business in the USA and Thailand, which is expected to strengthen its Solutions & Specialties segment.

The acquisition details are outlined in the following slide:

This strategic move is expected to add mid-to-high double-digit € million in sales and low double-digit € million in EBITDA contribution, with five-year synergies potentially reaching high double-digit € million.

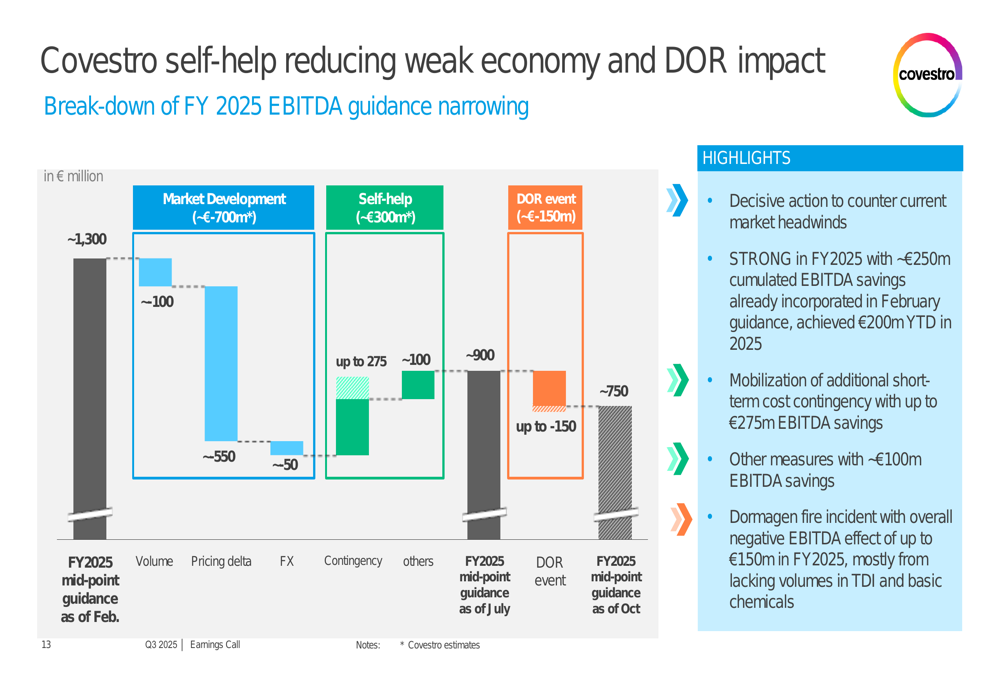

Additionally, Covestro is making significant progress with its cost-saving program. The company’s "STRONG" initiative is expected to deliver approximately €250 million in cumulated EBITDA savings for FY 2025, complemented by additional short-term cost contingencies that could provide up to €275 million in EBITDA savings.

The following chart illustrates how these self-help measures are helping to offset market headwinds:

Forward-Looking Statements

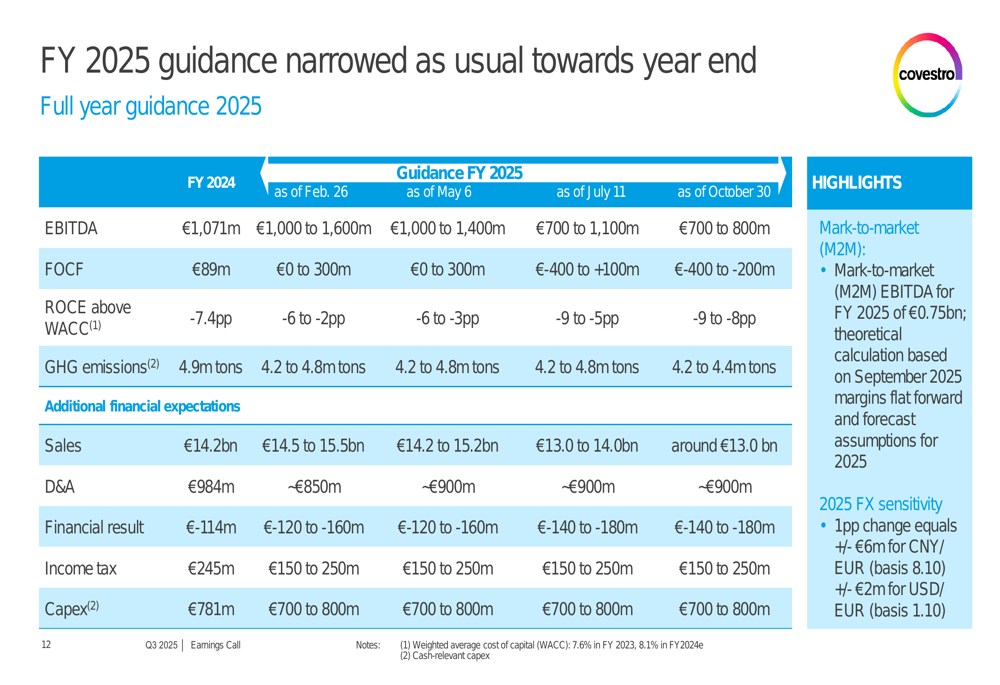

Covestro has narrowed its full-year 2025 guidance, reflecting both ongoing challenges and the impact of its cost-saving initiatives. The company now expects:

The company also provided an update on its pending acquisition by XRG, noting that regulatory approvals are progressing as expected with 78% of necessary approvals already secured. The transaction remains on track for closing before December 2, 2025.

The regulatory approval status is visualized in the following slide:

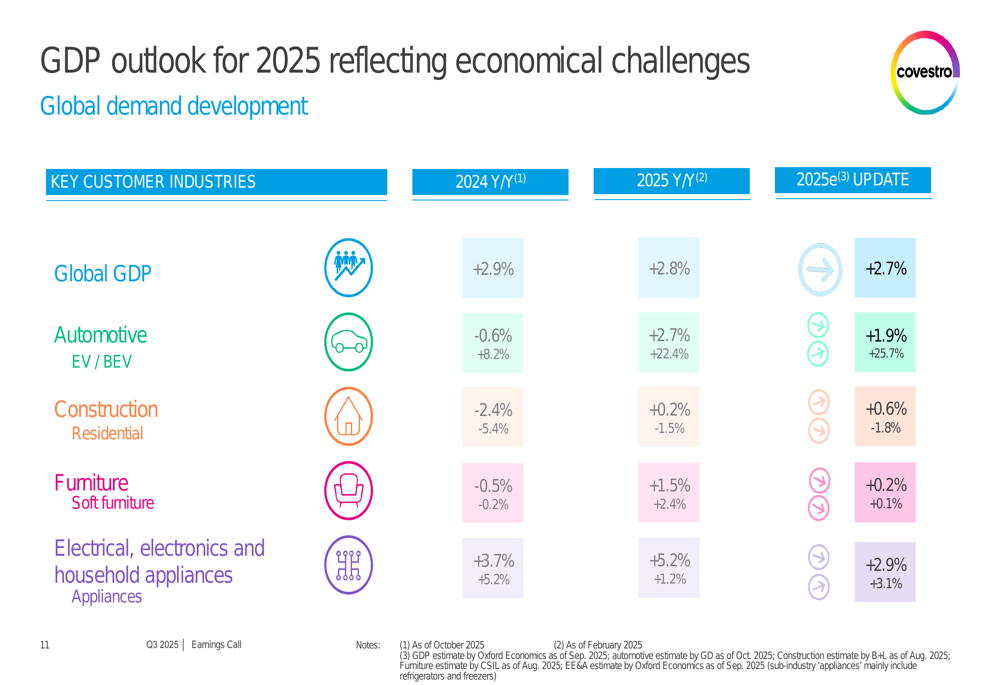

Looking ahead, Covestro faces a mixed economic outlook across its key customer industries. While global GDP is projected to grow by 2.7% in 2025, construction and furniture markets remain sluggish with expected growth rates of 0.6% and 0.2% respectively.

Covestro’s CEO commented on the challenging market environment, stating, "Global market conditions remained challenging throughout Q3," according to the earnings call transcript. However, management expressed confidence in the company’s self-help measures and strategic initiatives to navigate these headwinds.

With a Baa2 credit rating (stable outlook) confirmed by Moody’s in April 2025, Covestro maintains its commitment to a solid investment grade rating despite an increased net debt to EBITDA ratio of 3.8x at the end of Q3 2025, compared to 3.0x in the same period last year.

Covestro shares traded at €60.4 following the earnings presentation, showing a modest 0.33% increase, suggesting that investors were largely anticipating the results and remain focused on the pending XRG transaction.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.