Lisa Cook sues Trump over firing attempt, emergency hearing set

Introduction & Market Context

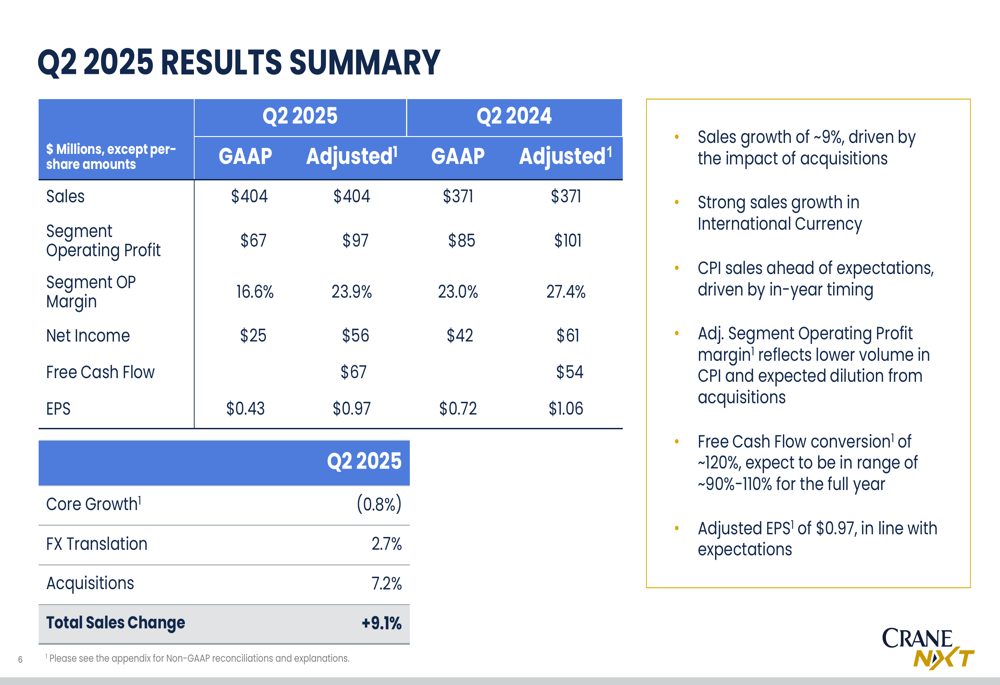

Crane NXT Co (NYSE:CXT) presented its second quarter 2025 financial results on August 7, 2025, reporting sales growth of 9.1% and adjusted earnings per share of $0.97, in line with company expectations. The stock closed at $57.32 on August 6, down 1.66% ahead of the earnings presentation, but still well above its 52-week low of $41.54.

The company’s performance reflects its ongoing transformation into a market leader in authentication technologies, with strong growth in its Security & Authentication Technologies segment offsetting weakness in its Crane Payment Innovations business. This quarter’s results follow a strong Q1 2025, when Crane NXT beat earnings expectations with an adjusted EPS of $0.54 compared to the forecasted $0.5279.

Quarterly Performance Highlights

Crane NXT reported total sales of $404 million for Q2 2025, up from $371 million in the same period last year, representing a 9.1% increase. This growth was primarily driven by acquisitions (+7.2%) and favorable currency translation (+2.7%), which offset a slight core sales decline of 0.8%.

As shown in the following comprehensive financial summary:

Adjusted segment operating profit was $97 million compared to $101 million in Q2 2024, with adjusted segment operating margin declining to 23.9% from 27.4% in the prior year. Adjusted earnings per share came in at $0.97, down from $1.06 in Q2 2024, reflecting the dilutive impact of recent acquisitions and lower volumes in certain segments.

Free cash flow showed significant improvement, reaching $67 million compared to $54 million in Q2 2024, with adjusted free cash flow conversion of approximately 120%, well above the company’s full-year target range of 90-110%.

Segment Performance

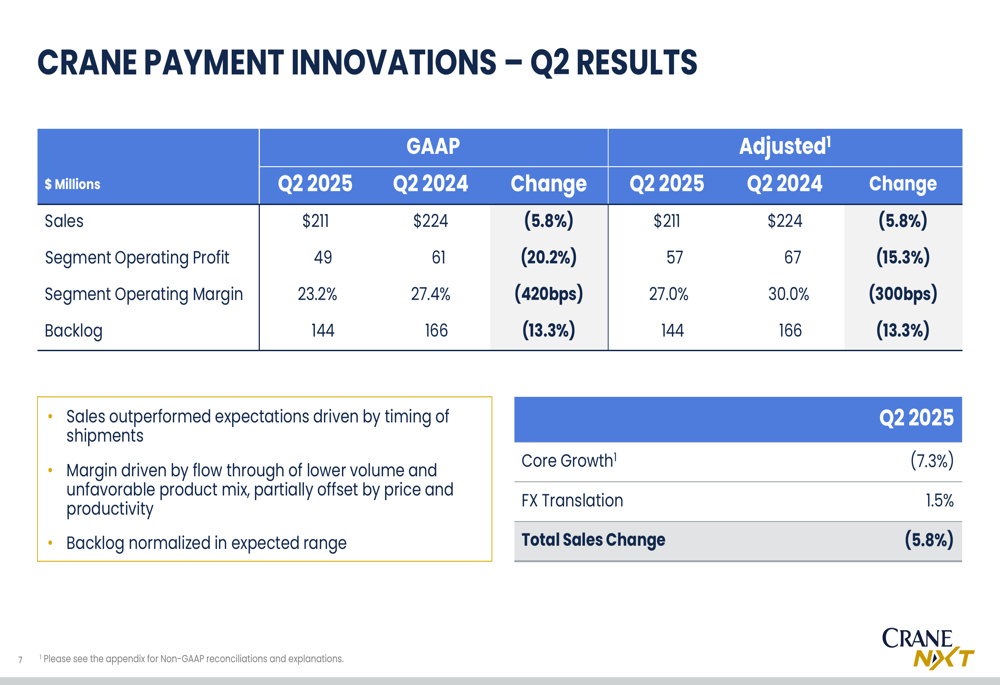

Crane NXT’s two business segments delivered divergent results in Q2 2025. The Security & Authentication Technologies (SAT) segment showed robust growth, while the Crane Payment Innovations (CPI) segment experienced a decline.

The CPI segment, which focuses on payment and connectivity solutions, reported sales of $211 million, down 5.8% from $224 million in Q2 2024. This decline was primarily due to a 7.3% drop in core sales, partially offset by favorable currency translation of 1.5%.

The following slide details CPI’s performance metrics:

Despite the sales decline, CPI’s performance exceeded management’s expectations, driven by better-than-anticipated timing of shipments. The segment’s adjusted operating margin decreased to 27.0% from 30.0% in the prior year, reflecting the impact of lower volume and unfavorable product mix, partially offset by pricing actions and productivity improvements.

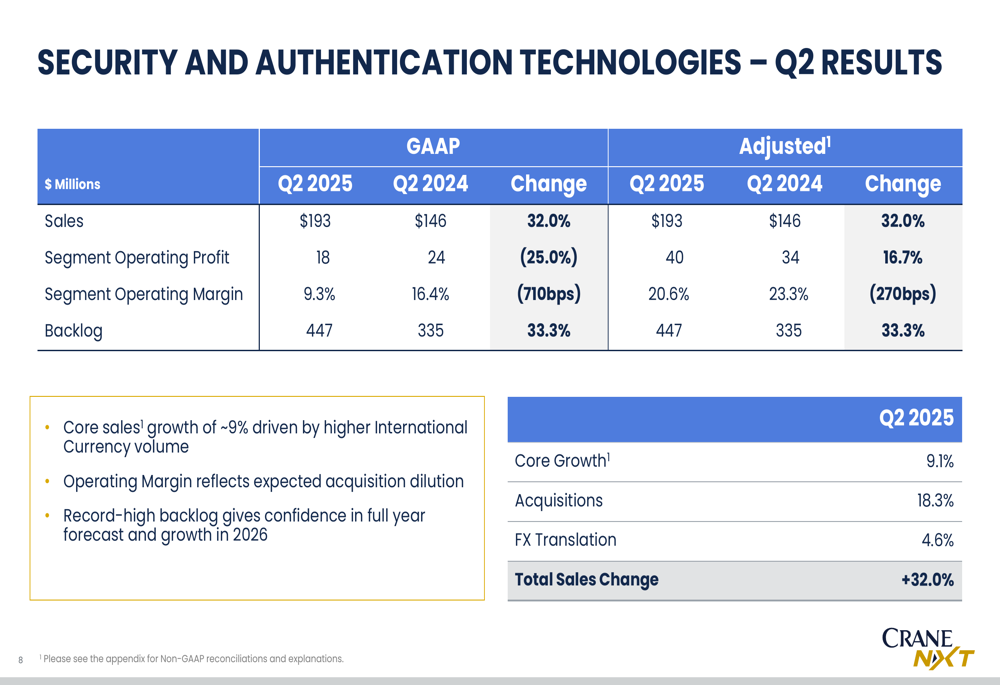

In contrast, the Security & Authentication Technologies segment delivered strong results, with sales increasing 32.0% to $193 million, compared to $146 million in Q2 2024:

The SAT segment’s growth was driven by a combination of core sales growth (+9.1%), acquisitions (+18.3%), and favorable currency translation (+4.6%). The segment’s adjusted operating margin decreased to 20.6% from 23.3%, primarily due to the expected dilution from acquisitions. Notably, the segment’s backlog reached a record high of $447 million, up 33.3% from the prior year, providing confidence in the company’s full-year forecast and growth prospects for 2026.

Strategic Initiatives

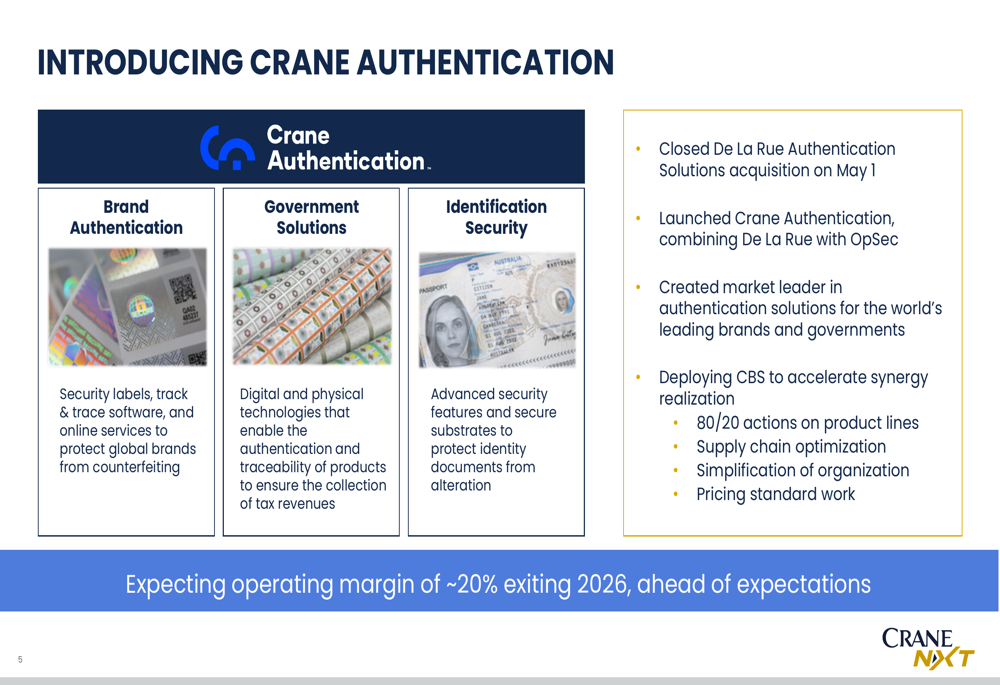

A key strategic focus for Crane NXT is the development of its authentication technologies business. The company recently formed Crane Authentication by combining the acquired De La Rue (LON:DLAR) Authentication Solutions with its existing OpSec business:

This new business unit offers solutions across three key areas: Brand Authentication (security labels and track & trace software), Government Solutions (digital and physical technologies for product authentication), and Identification Security (security features for identity documents). Management expects Crane Authentication to achieve an operating margin of approximately 20% by the end of 2026, ahead of initial expectations, through the deployment of the Crane Business System to accelerate synergy realization.

The company’s overall strategy centers on becoming a market leader in authentication technologies, with a clear organizational structure:

This structure positions Crane NXT to leverage its technology leadership across both segments, with Security & Authentication Technologies projected to generate approximately $735 million in 2025 sales and Crane Payment Innovations expected to contribute around $860 million.

Forward-Looking Statements

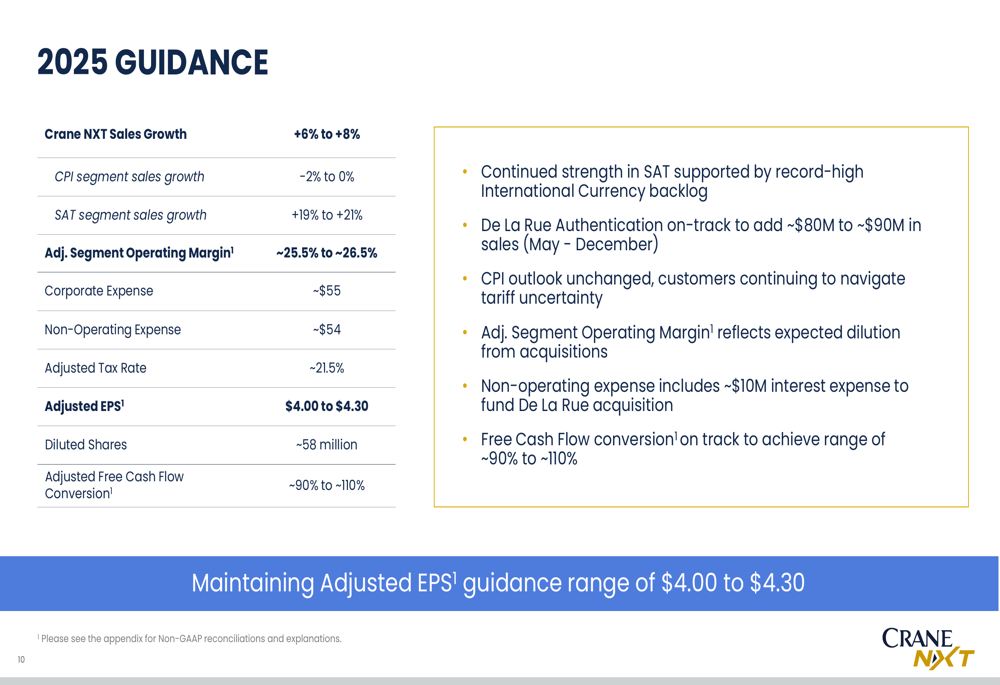

Crane NXT maintained its full-year 2025 guidance, projecting overall sales growth of 6-8% and adjusted earnings per share of $4.00 to $4.30:

The company expects continued strength in the Security & Authentication Technologies segment, supported by the record-high International Currency backlog. The De La Rue Authentication acquisition is on track to add approximately $80-90 million in sales for the year.

For the CPI segment, the outlook remains unchanged, with customers continuing to navigate tariff uncertainty. The adjusted segment operating margin guidance of 25.5-26.5% reflects the expected dilution from acquisitions.

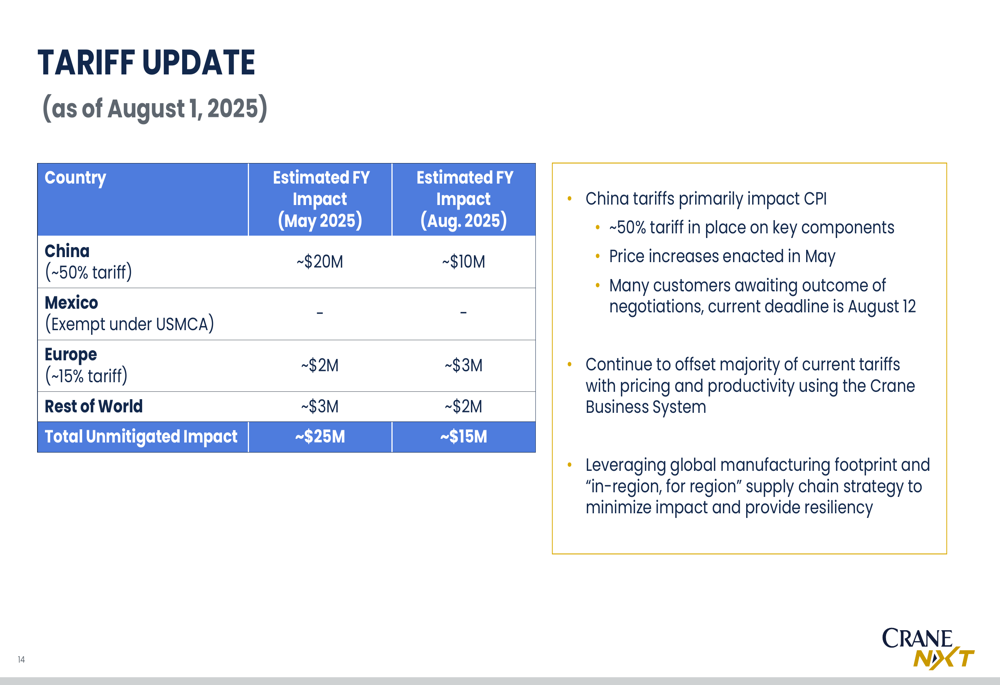

Crane NXT also provided an update on tariff impacts, noting a reduction in the estimated full-year impact:

The company has reduced its estimate of the unmitigated tariff impact from approximately $25 million in May to approximately $15 million as of August 1, 2025. This improvement reflects the company’s efforts to offset tariffs through pricing actions and productivity improvements using the Crane Business System, as well as leveraging its global manufacturing footprint.

Financial Position

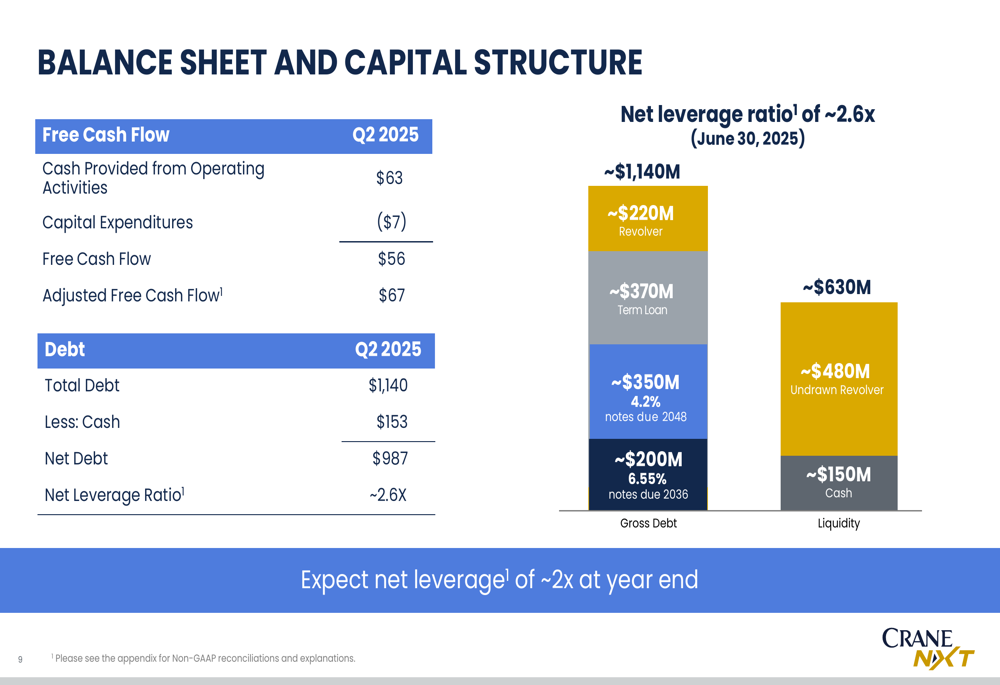

Crane NXT maintains a solid balance sheet despite recent acquisition activity. The company reported total debt of $1,140 million and cash of $153 million, resulting in net debt of $987 million and a net leverage ratio of approximately 2.6x:

Management expects to reduce the net leverage ratio to approximately 2x by year-end, demonstrating its commitment to maintaining financial flexibility. The company’s debt structure includes a mix of revolving credit, term loans, and long-term notes, with an undrawn revolver capacity of approximately $480 million providing additional liquidity.

The strong free cash flow generation, with conversion exceeding 120% in Q2, supports the company’s capital allocation priorities, including debt reduction, strategic acquisitions, and potential shareholder returns.

Conclusion

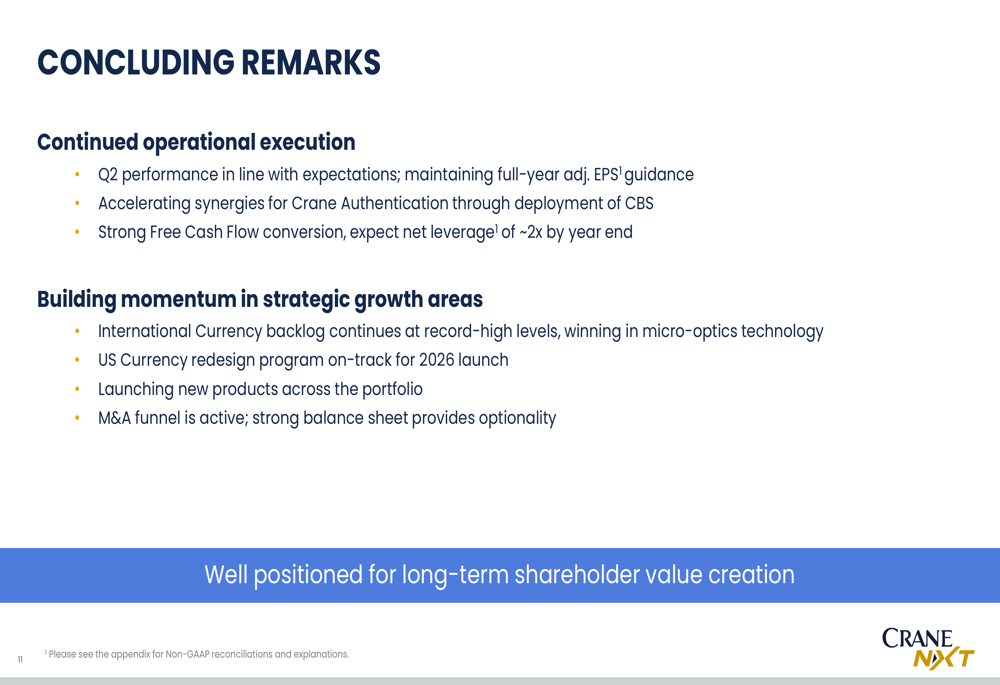

Crane NXT’s Q2 2025 results demonstrate the company’s ability to navigate a complex operating environment while executing its strategic transformation into a market leader in authentication technologies. The record-high backlog in the International Currency business and successful integration of recent acquisitions provide a solid foundation for future growth, despite challenges in the payment innovations segment and ongoing tariff uncertainties.

As summarized in the company’s concluding remarks:

With its strong free cash flow conversion, active M&A pipeline, and technology leadership in key markets, Crane NXT appears well-positioned to deliver on its full-year guidance and long-term growth objectives. Investors will be watching closely to see if the company can maintain this momentum through the second half of 2025 and successfully integrate its recent acquisitions to drive enhanced shareholder value.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.