China smartphone shipments slumped in June on inventory overhang: Jefferies

Introduction & Market Context

Crescent Energy Co (NYSE:CRGY) released its Q1 2025 earnings presentation on May 6, 2025, highlighting strong operational and financial performance despite challenging market conditions. The company’s stock has faced pressure recently, trading at $8.10 in after-hours trading, down 1.58% following a 4.64% decline during the regular session. This continues a pattern seen in previous quarters where strong operational results haven’t translated to stock price gains.

The company emphasized its ability to generate substantial free cash flow while maintaining operational discipline across its portfolio, particularly in the Eagle Ford and Uinta basins.

Quarterly Performance Highlights

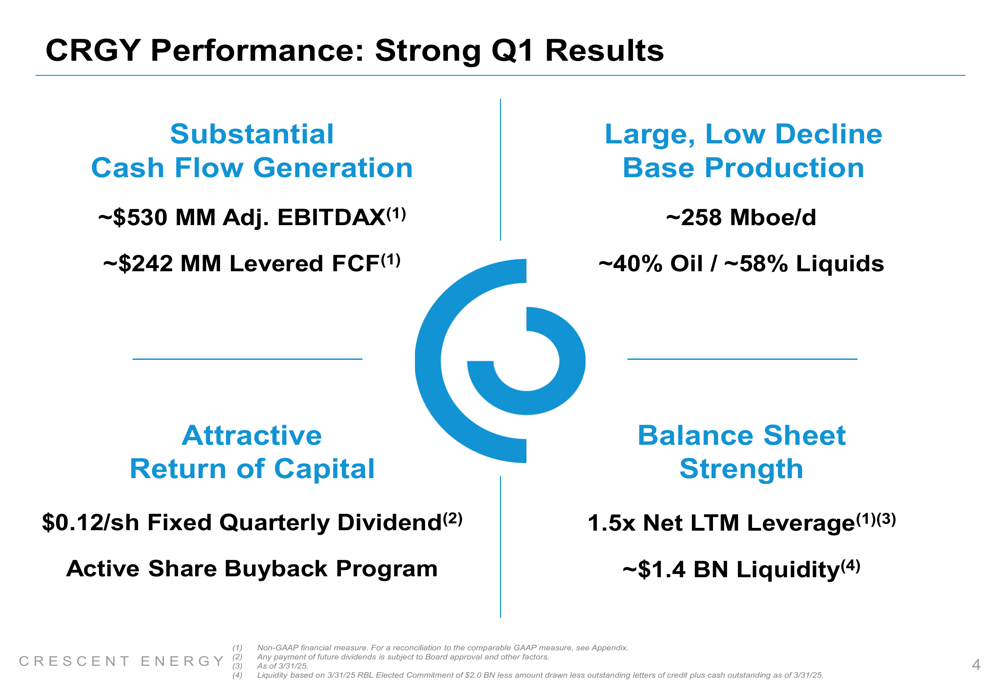

Crescent Energy delivered robust financial results in Q1 2025, generating approximately $530 million in adjusted EBITDAX and $242 million in levered free cash flow. The company maintained production of approximately 258 Mboe/d with a favorable production mix of 40% oil and 58% total liquids.

As shown in the following comprehensive performance overview:

The company’s balance sheet remains solid with a net leverage ratio of 1.5x and approximately $1.4 billion in liquidity. This financial strength allows Crescent to pursue its strategic priorities while returning capital to shareholders through its fixed quarterly dividend of $0.12 per share and active share repurchase program.

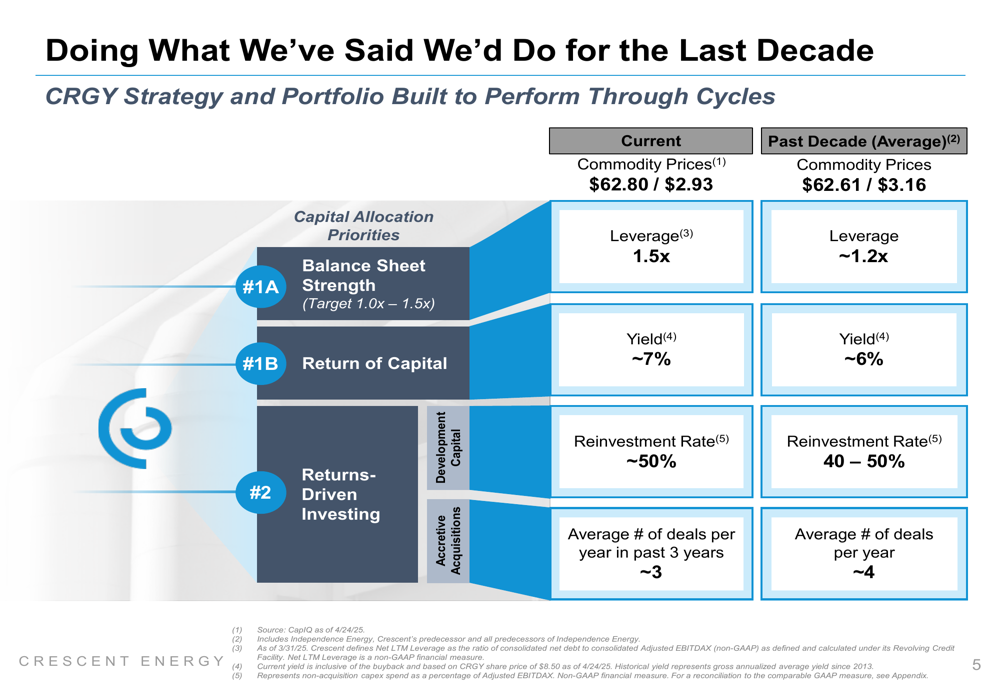

Crescent’s Q1 performance aligns with its long-term strategy of maintaining consistent financial metrics through commodity price cycles, as illustrated in this historical comparison:

Operational Efficiencies

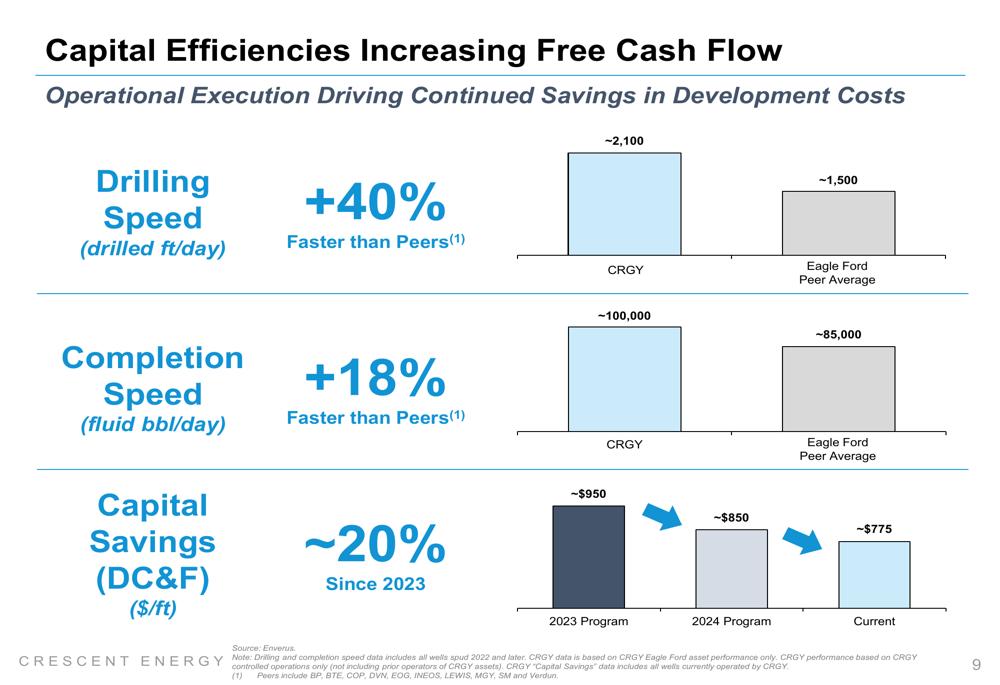

A key driver of Crescent’s financial performance has been its focus on operational efficiencies, particularly in its Eagle Ford assets. The company reported significant improvements in drilling and completion speeds compared to peers, along with substantial capital savings in development costs.

The following chart demonstrates these operational advantages:

These efficiency gains have translated directly to improved capital productivity and higher free cash flow generation. Crescent’s Eagle Ford assets produced approximately 165 Mboe/d in Q1, representing about 64% of the company’s total production. The successful integration of the Ridgemar acquisition, which closed on January 31, has further strengthened the company’s Eagle Ford position.

Competitive Industry Position

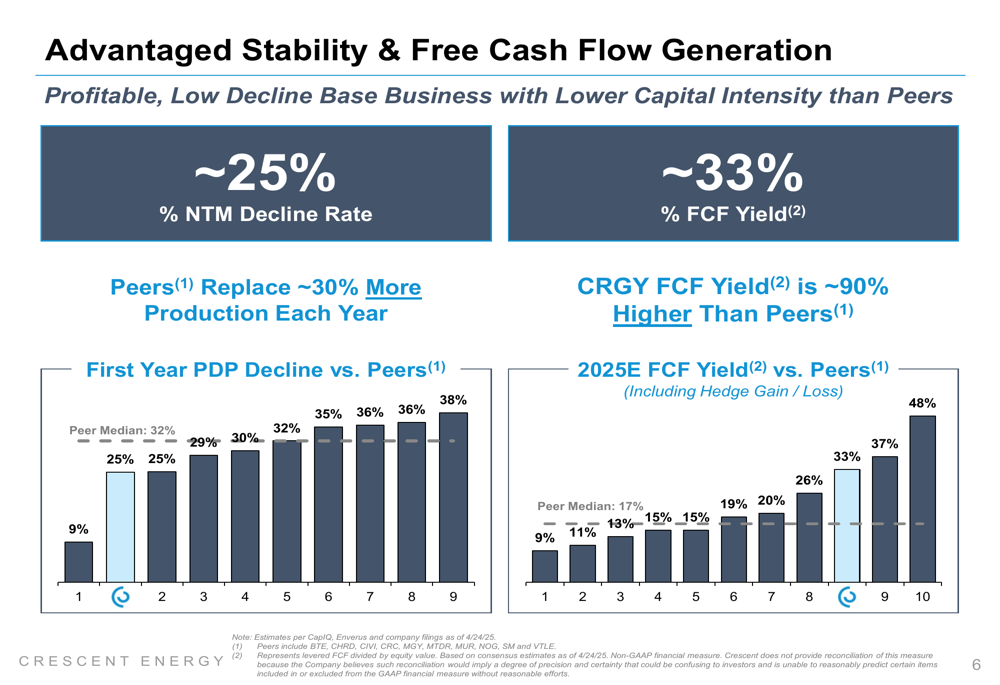

Crescent Energy emphasized its advantaged position relative to peers, highlighting its lower decline rates and higher free cash flow yield. The company’s business model delivers a low decline base business with lower capital intensity than industry peers.

As illustrated in the following comparative analysis:

This advantaged position allows Crescent to generate approximately 90% higher free cash flow yield than peers while replacing less production each year. The company’s first-year PDP decline rate of approximately 25% compares favorably to the peer median of around 32%, resulting in more stable production and lower maintenance capital requirements.

Strategic Initiatives

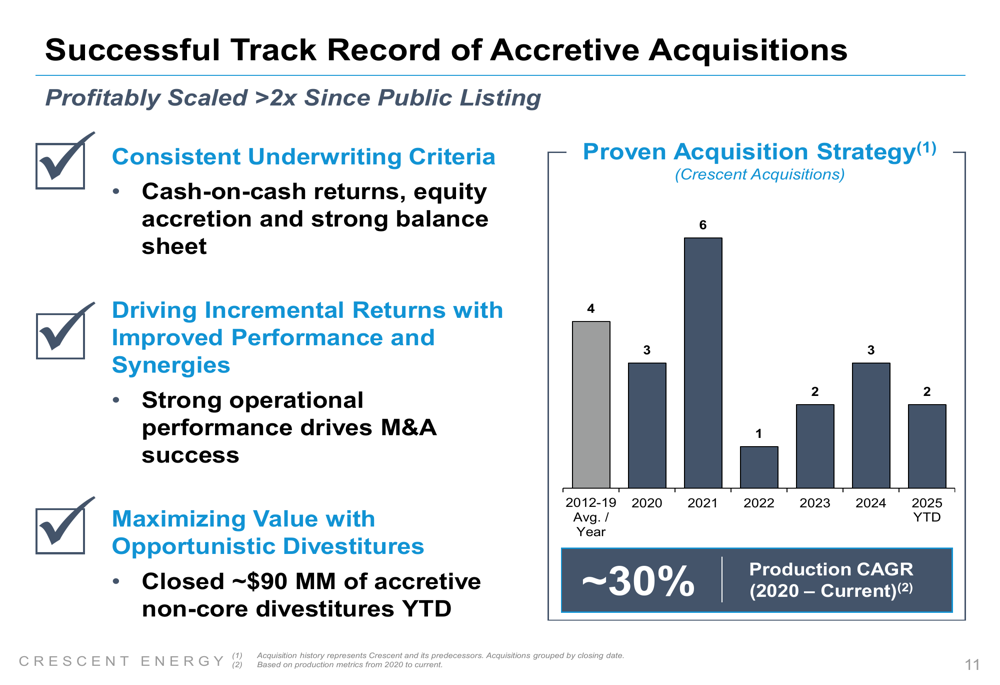

Crescent Energy continues to execute on its strategic priorities, including portfolio optimization through acquisitions and divestitures. The company closed approximately $90 million of non-core divestitures year-to-date, accelerating debt reduction efforts.

The company has maintained a consistent approach to acquisitions, as shown in its historical track record:

The recent Ridgemar acquisition in the Eagle Ford represents a continuation of this strategy, adding approximately 80,000 net acres and 20 Mboe/d of production. The company expects to realize $15-20 million in annual synergies and efficiencies from this transaction.

Additionally, Crescent has transformed its equity positioning by simplifying its corporate structure and transitioning to a single class of common stock with full conversion of Class B shares. This has resulted in a significant increase in public ownership and trading liquidity.

Forward-Looking Statements

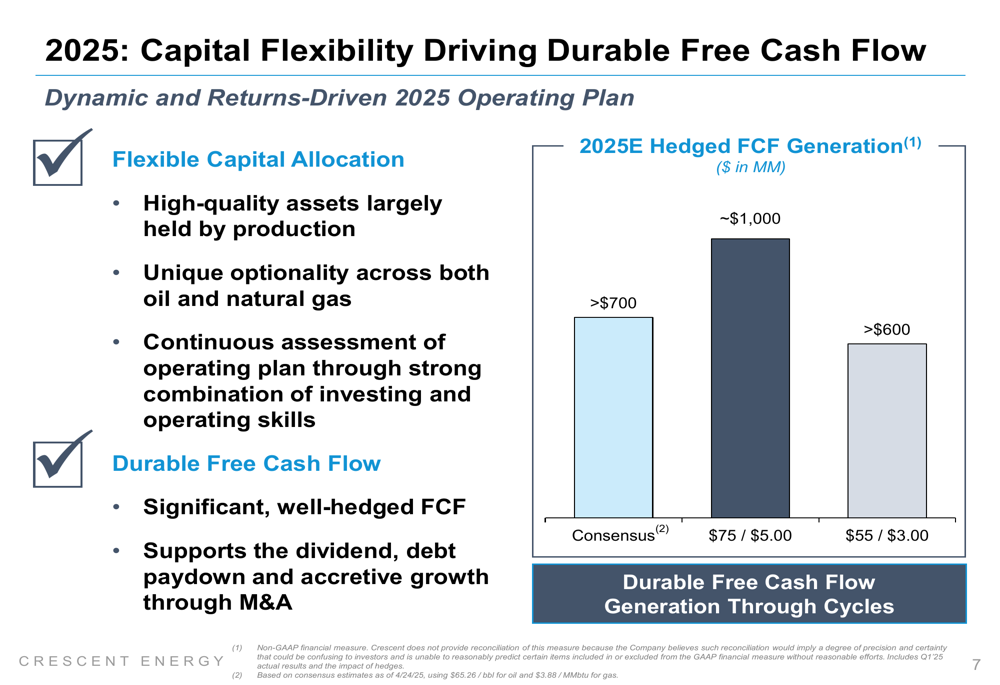

Looking ahead to the remainder of 2025, Crescent Energy emphasized its capital flexibility and ability to generate durable free cash flow across various commodity price scenarios. The company’s hedging program, with approximately 60% of both oil and gas production hedged for 2025, provides downside protection while maintaining upside exposure.

The following chart illustrates projected free cash flow generation under different price scenarios:

Crescent’s 2025 capital expenditure guidance remains at $925-1,025 million, with a flexible allocation approach that can shift between oil-weighted, mixed commodity, and dry gas opportunities based on market conditions.

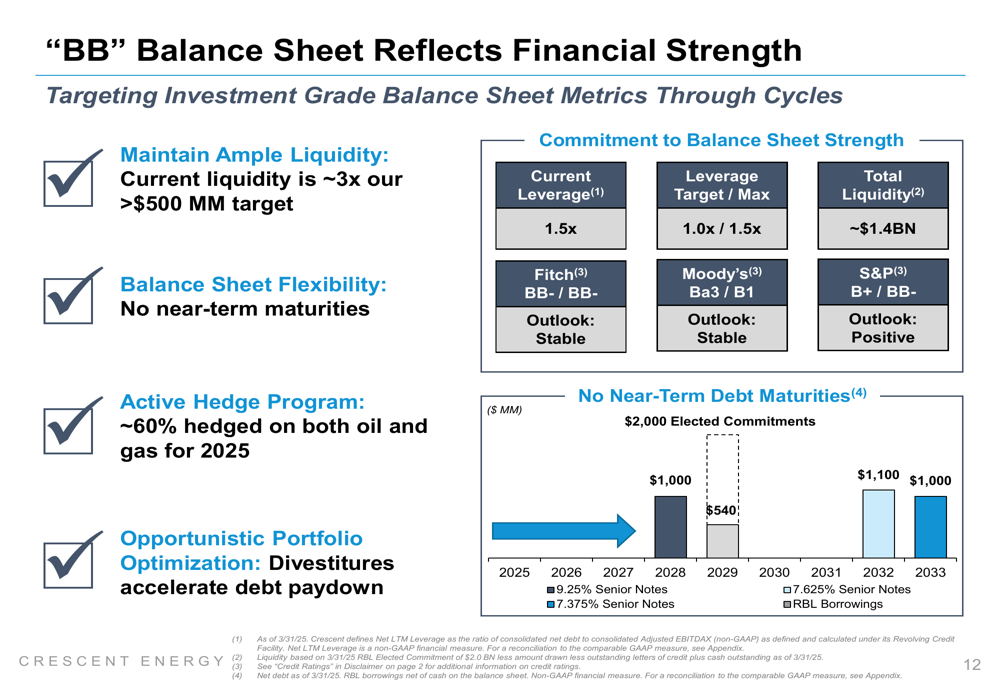

Balance Sheet & Shareholder Returns

Maintaining balance sheet strength remains a priority for Crescent Energy, with a target leverage ratio of 1.0-1.5x. The company currently has no near-term debt maturities and maintains a "BB" credit rating with a positive outlook from S&P.

As shown in the following debt maturity profile:

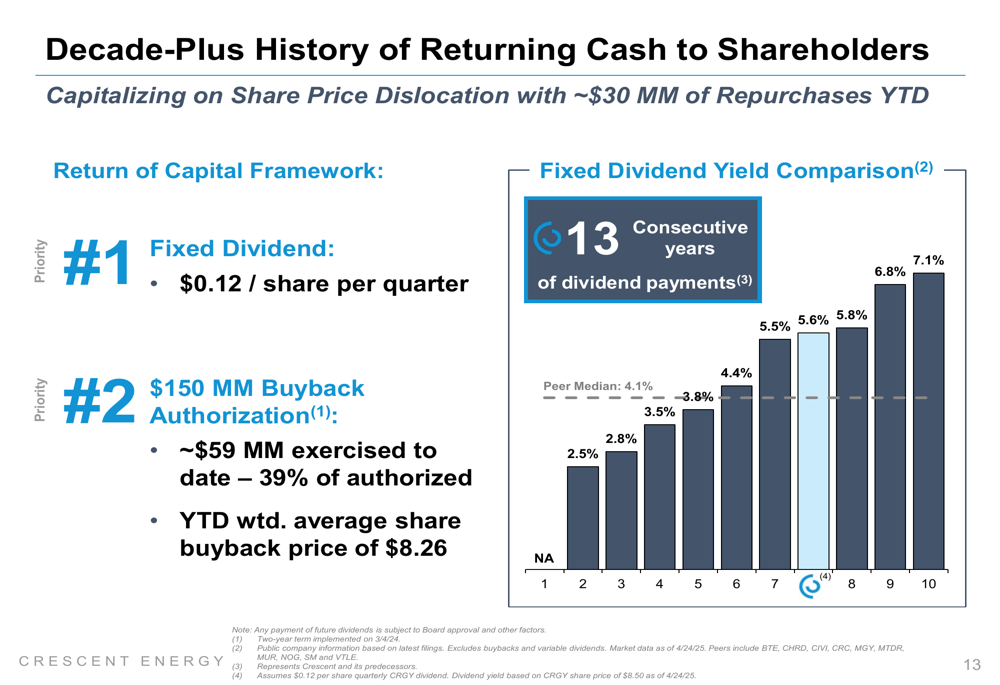

Crescent continues to return capital to shareholders through its fixed quarterly dividend of $0.12 per share, representing a yield of approximately 6.8% based on current share prices. This dividend yield compares favorably to the peer median of 4.1%. Additionally, the company has repurchased approximately $30 million of shares year-to-date at an average price of $8.26 per share.

The following chart illustrates Crescent’s dividend yield relative to peers:

Executive Summary

Crescent Energy’s Q1 2025 results demonstrate the company’s ability to generate substantial free cash flow through operational efficiencies and strategic portfolio management. Despite challenging market conditions reflected in recent stock price performance, the company continues to execute on its strategic priorities while maintaining financial discipline.

Key achievements in the quarter included strong cash flow generation, continued operational improvements in the Eagle Ford, successful integration of the Ridgemar acquisition, and return of capital to shareholders through dividends and share repurchases. The company’s focus on maintaining balance sheet strength while pursuing accretive acquisitions and divestitures positions it well for sustainable long-term value creation.

As Crescent moves forward in 2025, its flexible capital allocation approach and active hedging strategy should provide resilience across various commodity price scenarios, supporting its commitment to generating durable free cash flow and returning capital to shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.