Gold prices slid below $4,000/oz amid profit-taking on Gaza ceasefire

CrowdStrike Holdings Inc (NASDAQ:CRWD) reported strong second-quarter fiscal 2026 results on August 27, 2025, showcasing continued momentum in its platform adoption strategy and financial performance. The cybersecurity leader posted 21% year-over-year revenue growth and record quarterly profitability, driven by its AI-native platform approach and Flex licensing model.

Quarterly Performance Highlights

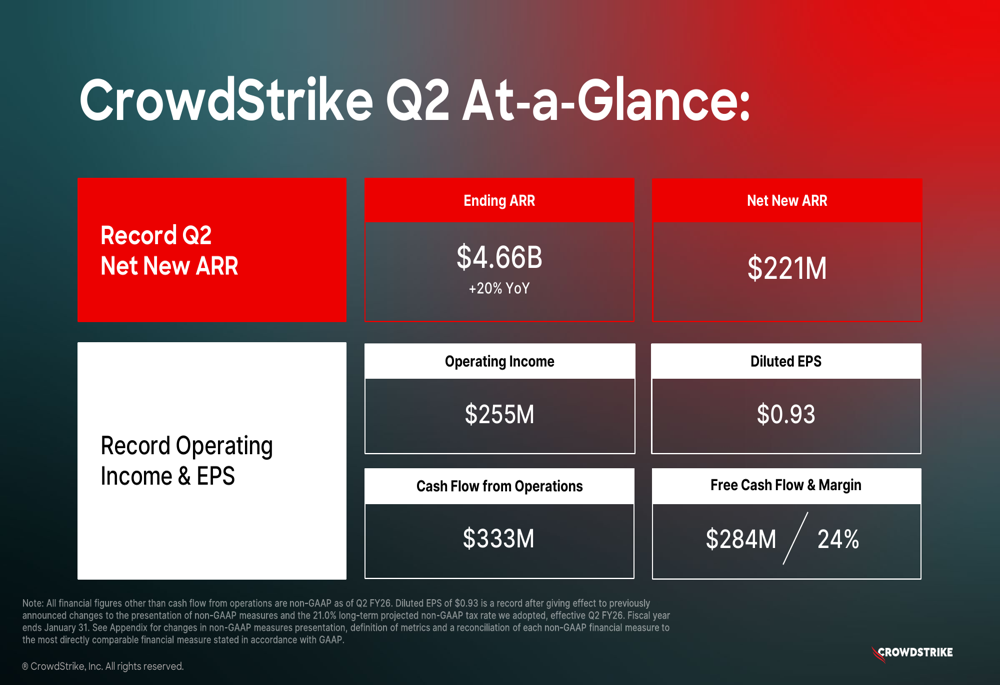

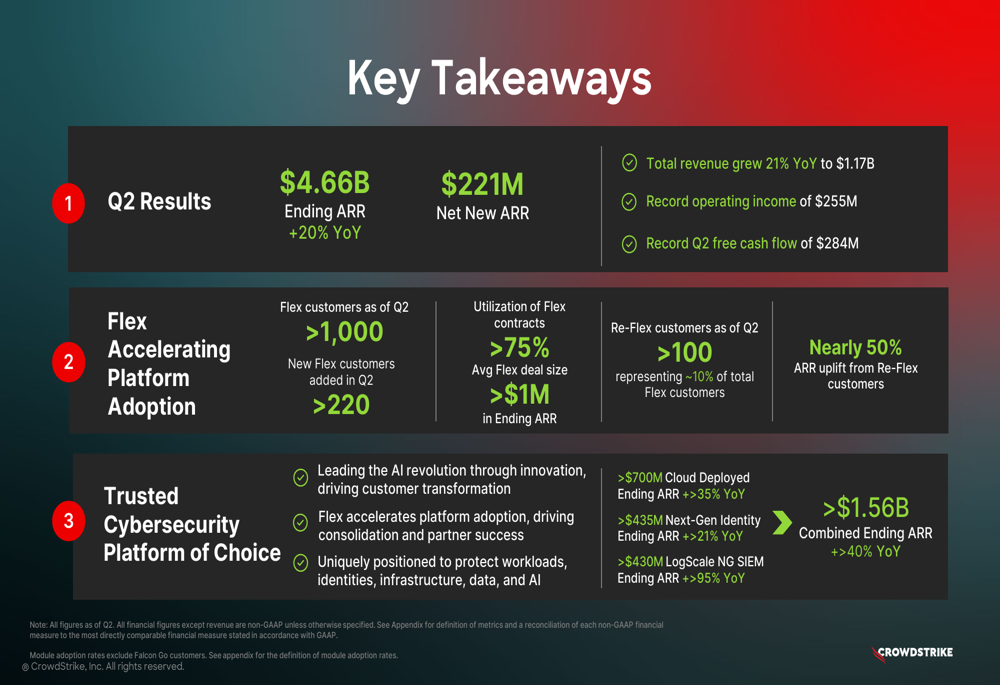

CrowdStrike delivered robust financial results for Q2 FY2026, with total revenue reaching $1.17 billion, up 21% year-over-year. The company reported record Q2 net new annual recurring revenue (ARR) of $221 million, bringing total ending ARR to $4.66 billion, representing 20% year-over-year growth.

As shown in the following summary of key Q2 metrics, CrowdStrike achieved record operating income and earnings per share:

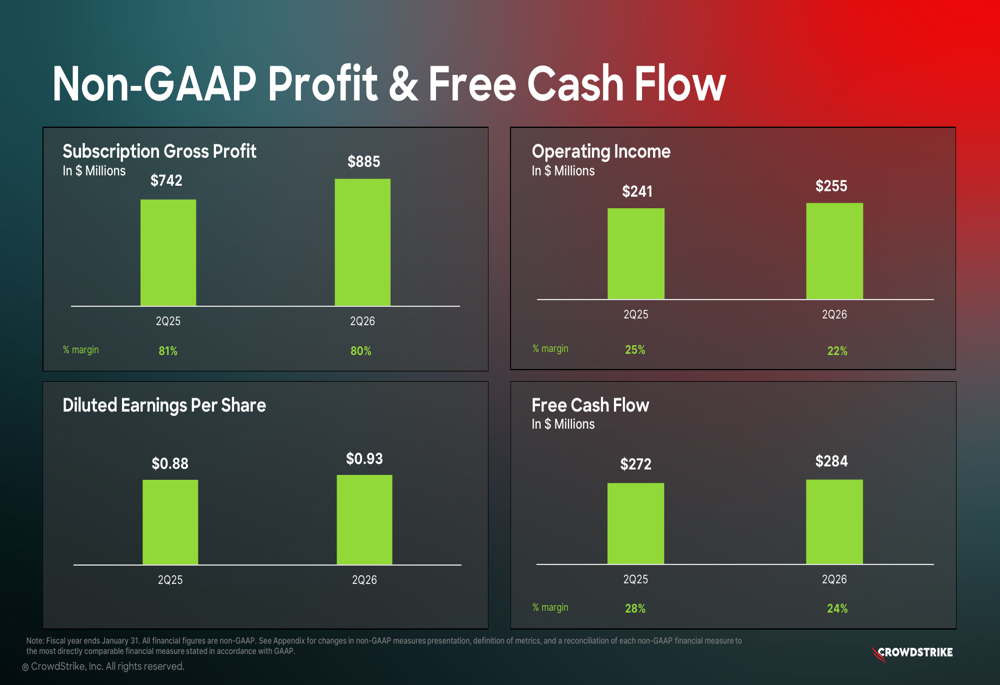

Non-GAAP operating income reached $255 million with a 22% margin, while diluted earnings per share hit $0.93. The company generated $333 million in cash flow from operations and $284 million in free cash flow, representing a 24% free cash flow margin.

CrowdStrike’s stock responded positively to the results, trading up 1.05% in aftermarket trading at $422, according to the fundamentals data provided.

Platform Adoption and Growth

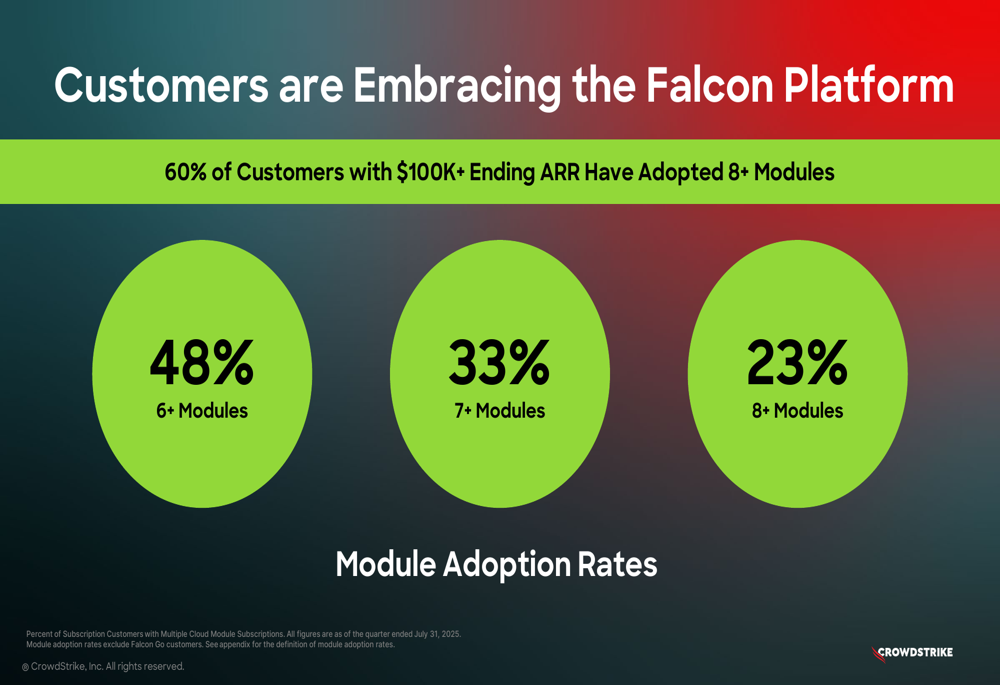

CrowdStrike’s platform strategy continues to gain traction, with 60% of customers having $100K+ in ARR adopting 8 or more modules. This demonstrates the company’s success in expanding beyond its core endpoint security offerings.

The following slide illustrates the strong module adoption rates among CrowdStrike’s customer base:

The company’s Flex licensing model is accelerating platform adoption, with over 1,000 Flex customers as of Q2, including more than 220 new Flex customers added during the quarter. The average Flex deal size exceeds $1 million in ending ARR, and utilization of Flex contracts is above 75%.

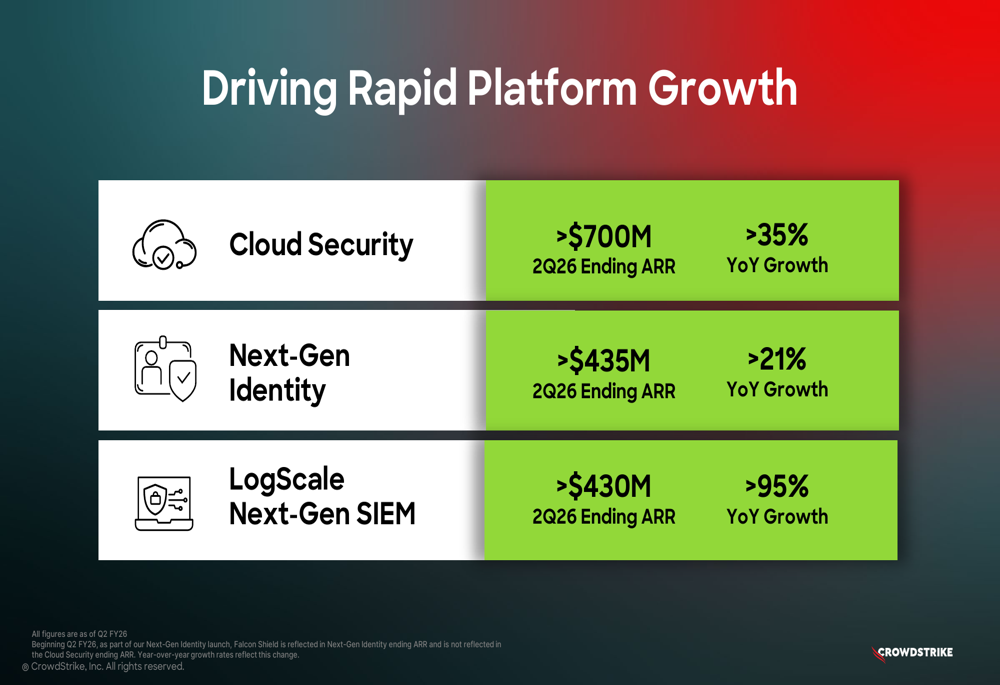

CrowdStrike’s platform components are experiencing rapid growth, with combined ending ARR for Cloud Security, Next-Gen Identity, and LogScale Next-Gen SIEM exceeding $1.56 billion and growing over 40% year-over-year:

Particularly impressive is the growth of LogScale Next-Gen SIEM, which saw a 95% year-over-year increase in ending ARR to over $430 million. Cloud Security grew over 35% to more than $700 million in ending ARR, while Next-Gen Identity increased more than 21% to over $435 million.

Industry Recognition and Market Opportunity

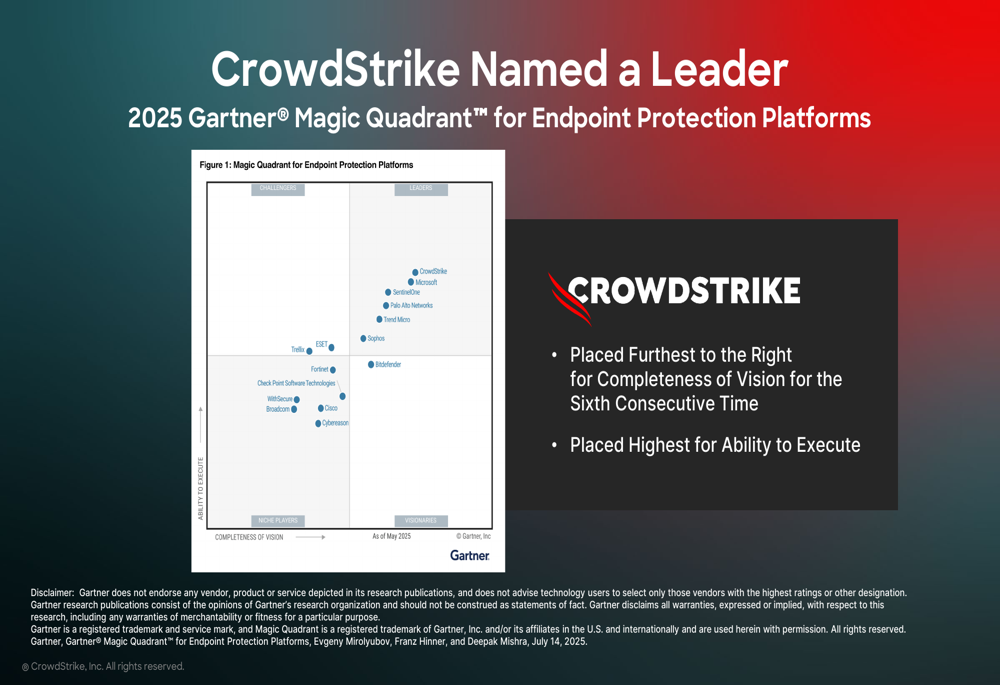

CrowdStrike continues to strengthen its leadership position in the cybersecurity market, as evidenced by its recognition in the 2025 Gartner Magic Quadrant for Endpoint Protection Platforms:

The company was positioned furthest to the right for Completeness of Vision for the sixth consecutive time and highest for Ability to Execute, reinforcing its status as a market leader.

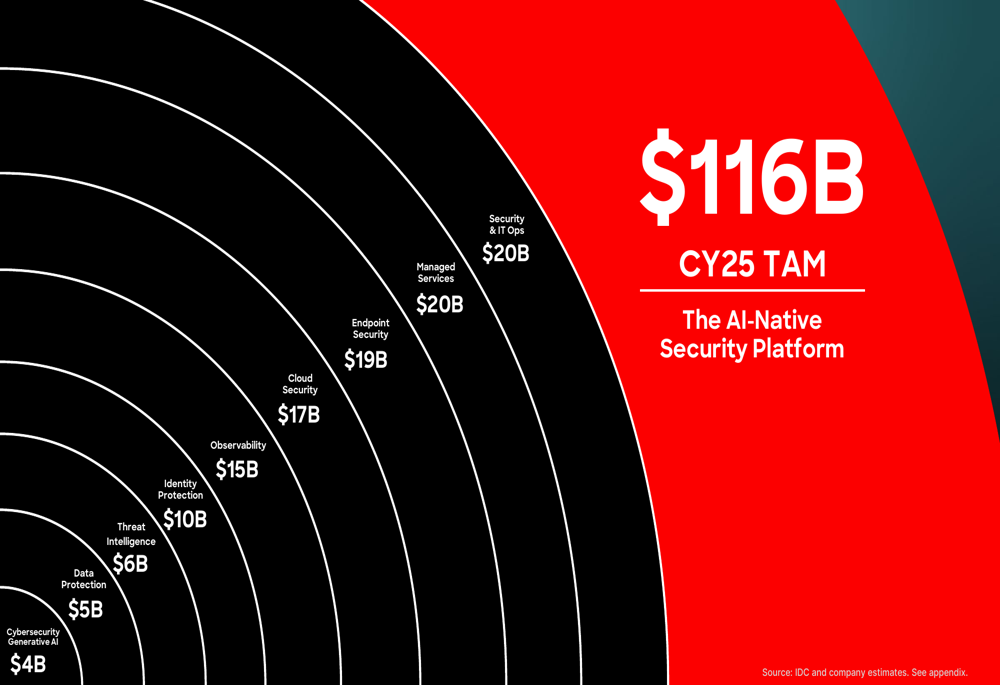

CrowdStrike estimates its total addressable market (TAM) at $116 billion in calendar year 2025, with significant growth potential across multiple security segments:

The company’s AI-native platform approach positions it to address this expanding market by consolidating point security products and simplifying cybersecurity for customers:

Financial Analysis

CrowdStrike’s financial performance demonstrates continued growth at scale, with strong revenue expansion and improving profitability metrics:

The company’s subscription gross profit increased to $885 million in Q2 FY2026, up from $742 million in the same period last year, while maintaining a strong 80% gross margin:

It’s worth noting that while non-GAAP results show strong profitability, GAAP results reflect a net loss of $77.7 million for Q2 FY2026, primarily due to stock-based compensation expenses. This represents a shift from the GAAP net income of $47 million reported in Q2 FY2025.

Guidance and Outlook

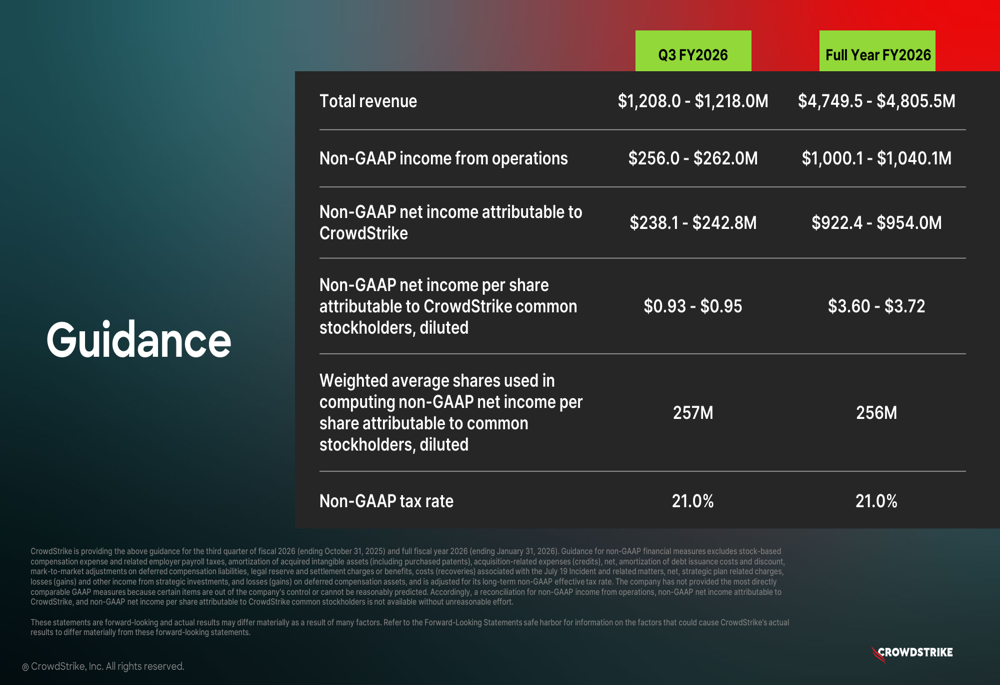

Looking ahead, CrowdStrike provided optimistic guidance for Q3 FY2026 and the full fiscal year:

For Q3 FY2026, the company expects total revenue between $1,208 million and $1,218 million, with non-GAAP operating income between $256 million and $262 million, and diluted EPS between $0.93 and $0.95.

For the full fiscal year 2026, CrowdStrike projects total revenue of $4,749.5 million to $4,805.5 million, representing approximately 21% year-over-year growth at the midpoint. Non-GAAP operating income is expected to be between $1,000.1 million and $1,040.1 million, with diluted EPS between $3.60 and $3.72.

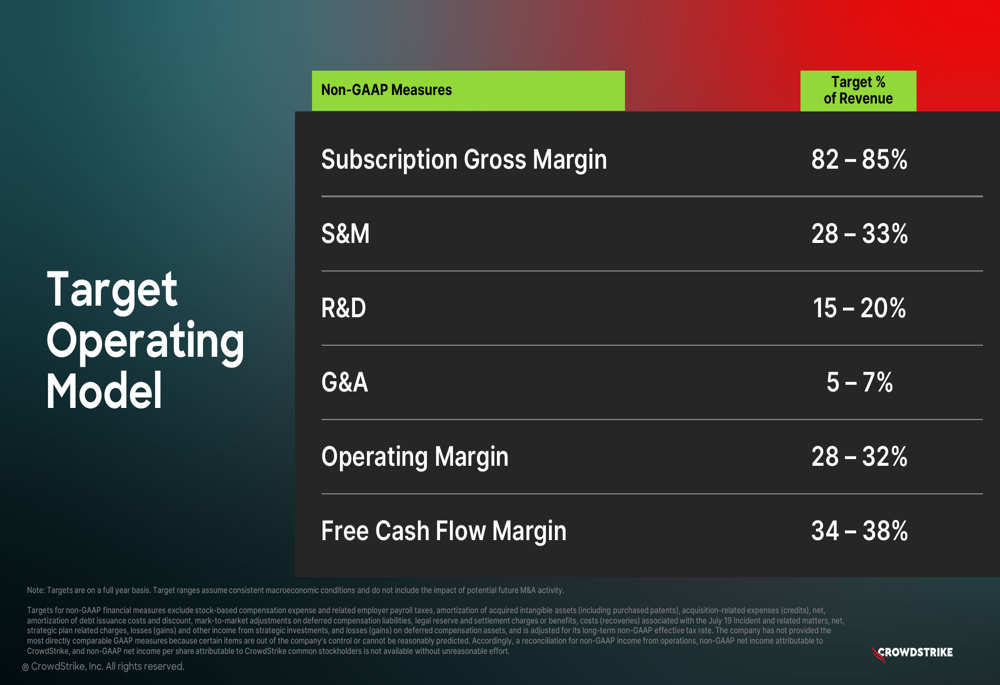

The company also shared its long-term target operating model, which includes subscription gross margins of 82-85%, operating margins of 28-32%, and free cash flow margins of 34-38%:

Key Takeaways

CrowdStrike’s Q2 FY2026 results demonstrate the company’s successful execution of its platform strategy and continued market leadership in cybersecurity. The following slide summarizes the key takeaways from the quarter:

With strong financial performance, accelerating platform adoption through its Flex model, and leadership in high-growth segments like cloud security and next-generation SIEM, CrowdStrike appears well-positioned to capitalize on the expanding cybersecurity market opportunity.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.