Street Calls of the Week

Introduction & Market Context

Crown Castle International Corp (NYSE:CCI) released its first quarter 2025 financial results on April 30, showing resilience in its core tower business despite overall revenue declines. The company’s stock closed at $103.70, up 1.99% for the day, reflecting investor confidence in its strategic direction.

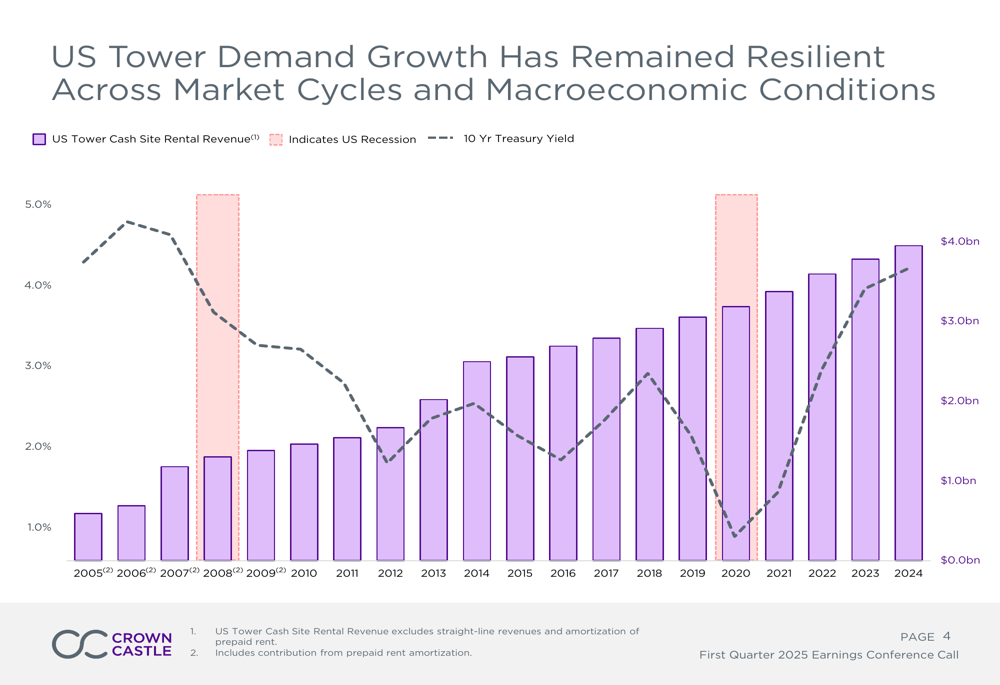

The presentation highlighted the historical resilience of Crown Castle’s tower business through various economic cycles, positioning it as a stable infrastructure investment even during periods of recession and fluctuating treasury yields.

As shown in the following chart of US Tower Demand Growth compared to economic indicators:

Quarterly Performance Highlights

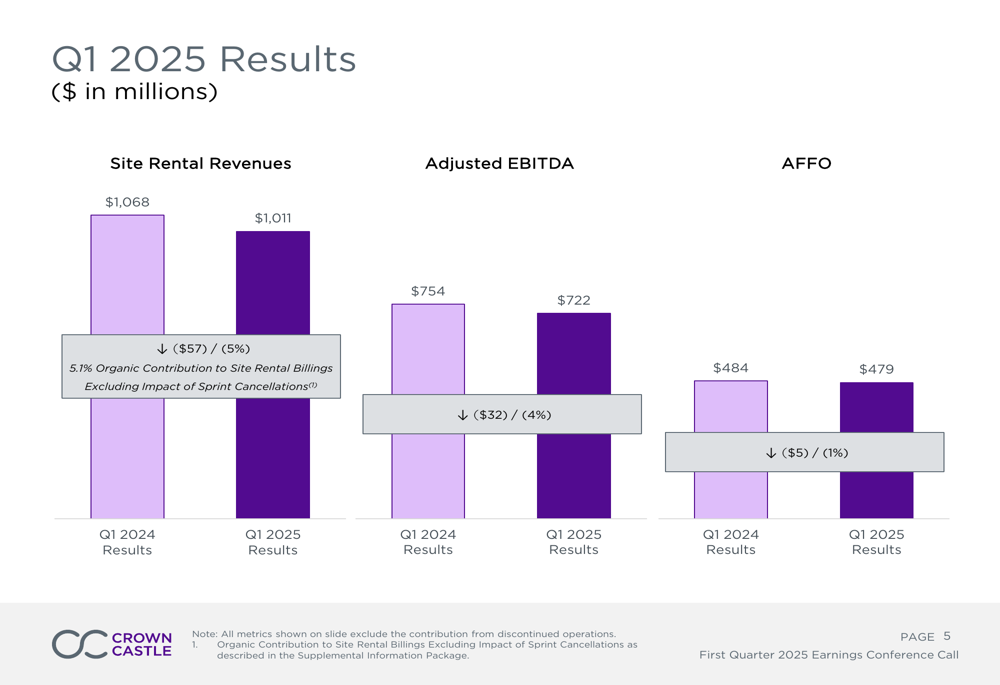

Crown Castle reported declines across its key financial metrics for Q1 2025 compared to the same period last year, primarily impacted by Sprint cancellations. However, the company emphasized its underlying tower business strength with 5.1% organic contribution to site rental billings when excluding these cancellations.

The quarterly results showed:

- Site Rental Revenues of $1,011 million, down 5% year-over-year

- Adjusted EBITDA of $722 million, a 4% decrease

- AFFO (Adjusted Funds From Operations) of $479 million, down 1%

The following chart illustrates these quarterly performance metrics:

Full Year Outlook

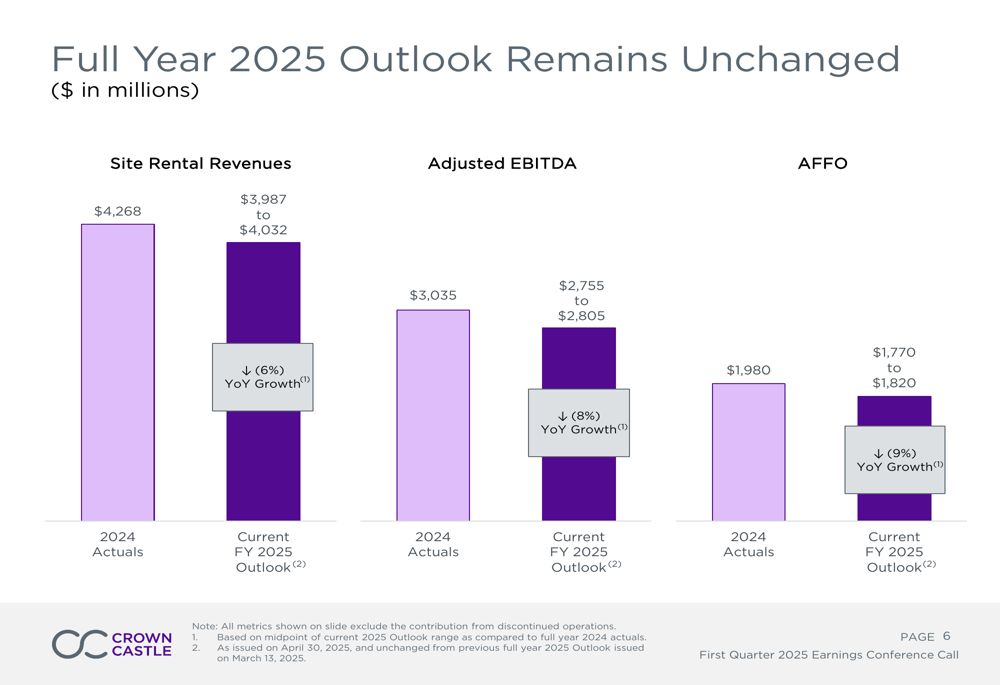

Crown Castle affirmed its full year 2025 outlook, maintaining the guidance it previously issued in March. The company expects:

- Site Rental Revenues between $3,987 million and $4,032 million, representing a 6% year-over-year decline

- Adjusted EBITDA between $2,755 million and $2,805 million, down 8%

- AFFO between $1,770 million and $1,820 million, a 9% decrease

These projections exclude contributions from discontinued operations and reflect the impact of Sprint cancellations while highlighting the underlying 4.5% tower organic growth.

The following chart shows the full year 2025 outlook compared to 2024 actuals:

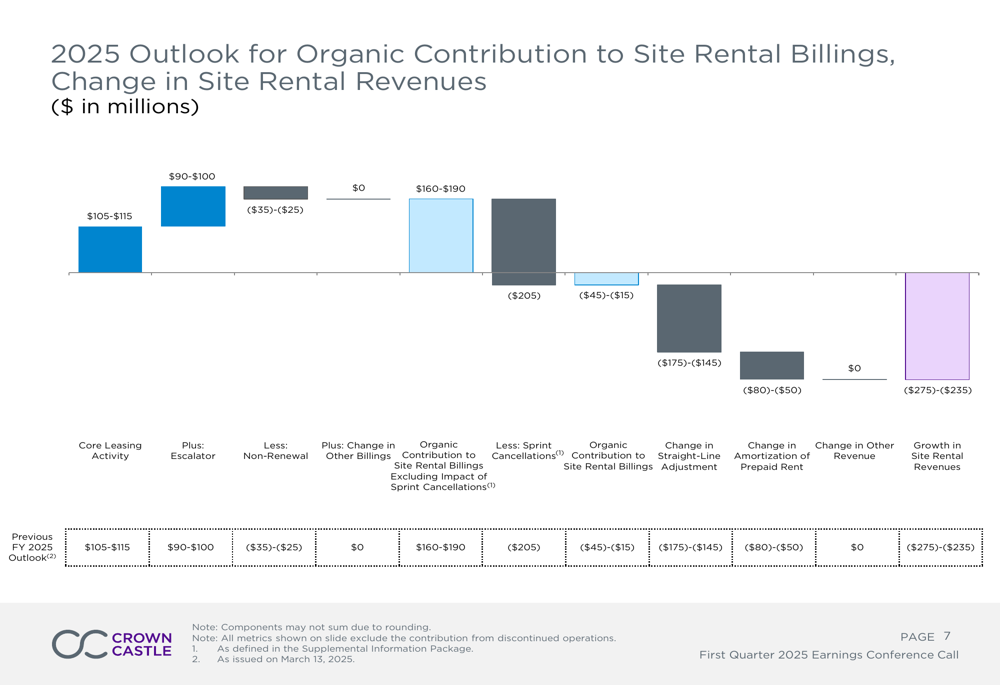

A more detailed breakdown of the factors affecting site rental revenues shows the significant impact of Sprint cancellations ($205 million) offsetting positive contributions from core leasing activity ($105-$115 million) and escalators ($90-$100 million):

Strategic Initiatives and Fiber Business Sale

Crown Castle reported that it remains on track to successfully close the sale of its fiber business in the first half of 2026, a key strategic move that will position the company as a pure-play tower business focused on the U.S. market.

The company highlighted several key strategic initiatives in its presentation:

- Delivering strong operational results in the tower business

- Successfully managing the transition to a standalone tower company

- Positioning to maximize shareholder value after the fiber business divestiture

As shown in the following map and strategic highlights:

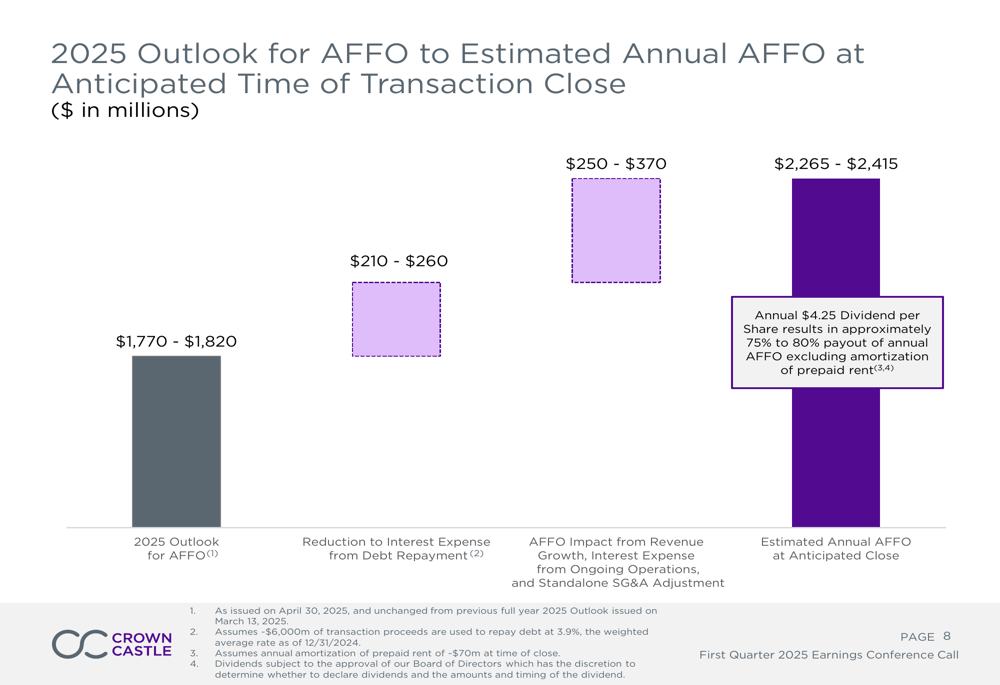

Forward-Looking Statements

The presentation provided insight into Crown Castle’s expected financial position following the completion of the fiber business sale. The company projects that its annual AFFO will improve significantly after the transaction closes, primarily due to:

- Reduction in interest expense from debt repayment: $210-$260 million

- Additional AFFO impact from revenue growth, interest expense changes, and SG&A adjustments: $250-$370 million

This would bring the estimated annual AFFO at the anticipated close time to $2,265-$2,415 million, a substantial improvement from the 2025 outlook of $1,770-$1,820 million.

The company plans to use approximately $6 billion of the transaction proceeds to repay debt at an average rate of 3.9%. Crown Castle also noted that its annual dividend of $4.25 per share represents approximately 75-80% payout of annual AFFO excluding amortization of prepaid rent.

The following chart illustrates the expected AFFO trajectory:

Despite the near-term financial impacts from Sprint cancellations, Crown Castle’s presentation emphasized the company’s confidence in its strategic direction and the long-term value of its tower infrastructure assets in the growing U.S. wireless market. The company’s focus on maximizing shareholder value through its transition to a pure-play tower company appears to be resonating with investors, as reflected in the positive stock performance following the earnings release.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.