Asia FX cautious amid US govt shutdown; yen tumbles after Takaichi’s LDP win

Introduction & Market Context

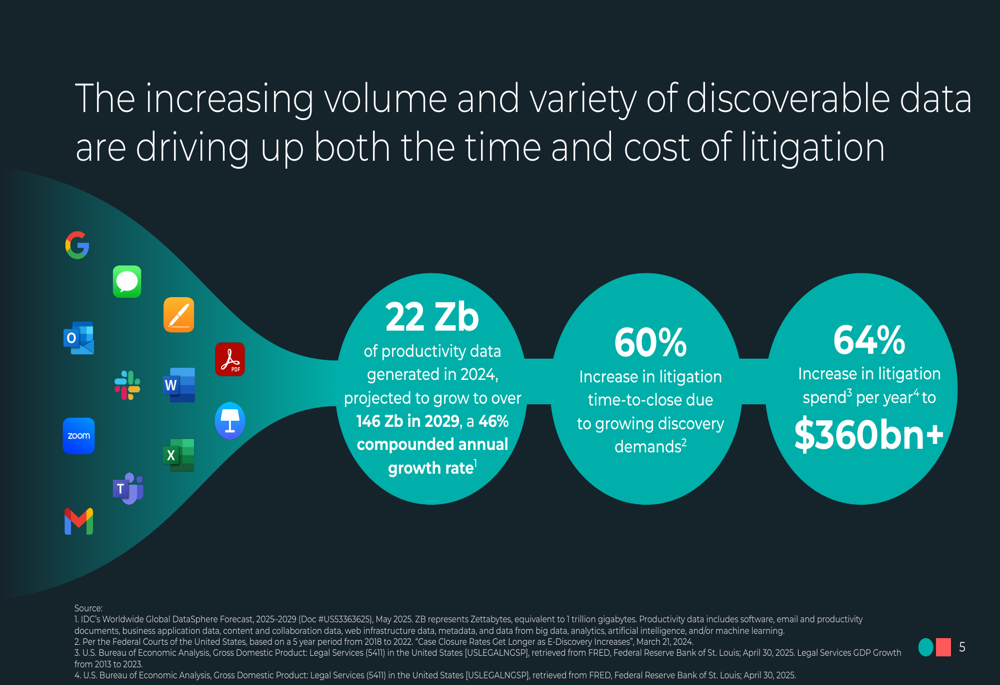

CS Disco (NYSE:LAW), a legal technology company specializing in AI-powered litigation solutions, presented its Q2 FY25 investor slides on August 6, 2025, highlighting both progress and ongoing challenges in its path to profitability. The company operates in a growing market where discovery costs represent over 50% of litigation expenses, with productivity data expected to surge from 22 zettabytes in 2024 to 146 zettabytes by 2029 – a 46% compound annual growth rate.

As shown in the following chart illustrating the market opportunity driven by increasing data volumes:

This data explosion has led to a 60% increase in litigation time-to-close and a 64% increase in annual litigation spend to over $360 billion, creating significant demand for more efficient discovery solutions.

Quarterly Performance Highlights

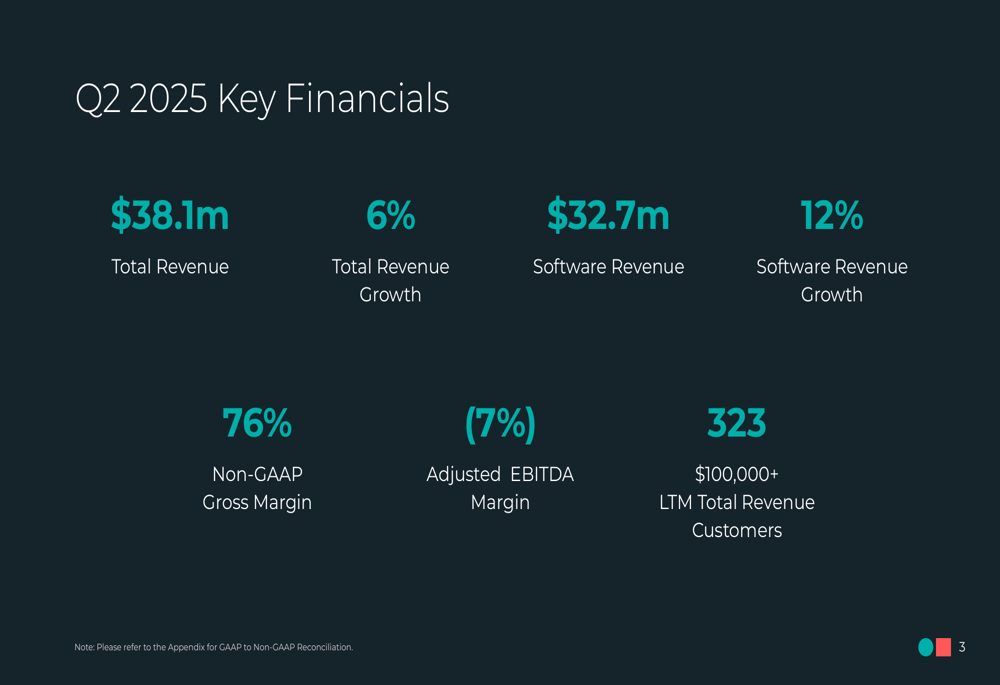

CS Disco reported total revenue of $38.1 million for Q2 FY25, representing 6% year-over-year growth, with software revenue increasing 12% to $32.7 million. However, this fell short of analyst expectations of $37.58 million, resulting in a 12.99% revenue miss despite the positive growth trajectory. The company maintained a healthy non-GAAP gross margin of 76% while improving its adjusted EBITDA margin to -7%, compared to -13% in the same period last year.

The following slide summarizes the key financial metrics for the quarter:

The company’s software revenue has shown consistent growth over the past nine quarters, while services revenue has been more volatile, declining 20% year-over-year in the most recent quarter:

CS Disco reported a narrower EPS loss of $0.04, outperforming the expected loss of $0.07 by 42.86%. Following the earnings release, the stock experienced a modest increase of 0.49%, closing at $4.13 in aftermarket trading, reflecting a cautious investor response to the mixed results.

Strategic Initiatives and AI Focus

The company’s strategic focus centers on its AI-powered litigation technology platform, which aims to streamline the discovery process that accounts for more than half of litigation costs. DISCO’s presentation emphasized how its solutions address the growing pressures faced by law firms, including increasing data volumes and client demands for faster results at lower costs.

As illustrated in this overview of industry and client pressures:

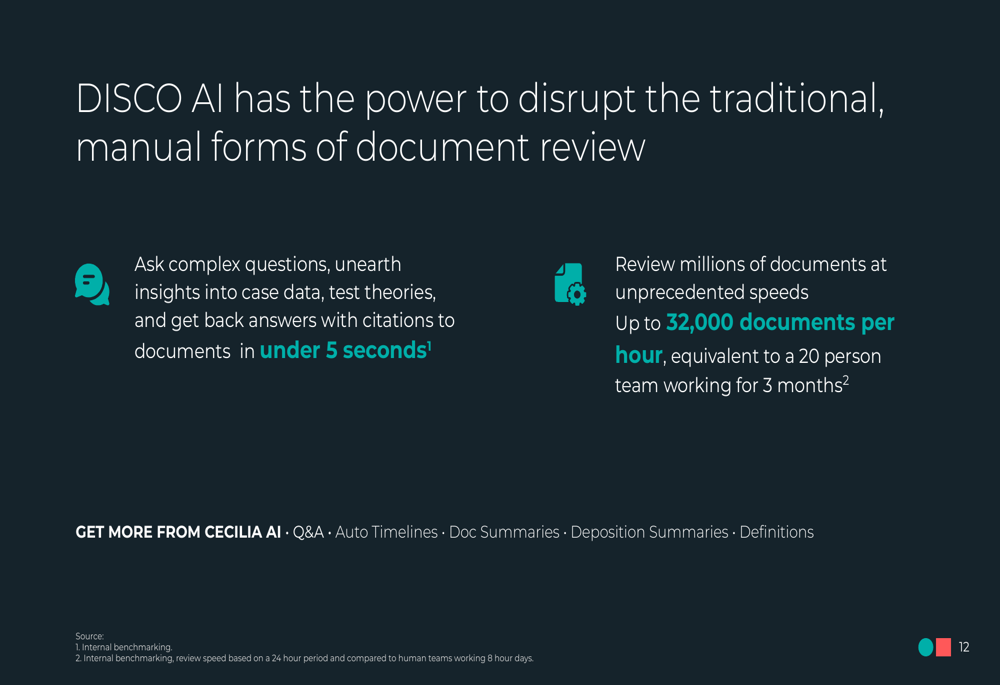

A key competitive differentiator for CS Disco is its AI technology, branded as Cecilia AI, which the company claims can review up to 32,000 documents per hour – equivalent to a 20-person team working for three months. The platform also enables lawyers to ask complex questions and receive answers with document citations in under five seconds.

The following slide highlights the company’s AI capabilities:

During the earnings call, CEO Eric Friedrichsen emphasized the company’s growth potential, stating, "We believe this business can be a 20% plus grower," while addressing analyst questions about the growing adoption of Cecilia AI in large-scale matters.

Financial Trajectory and Path to Profitability

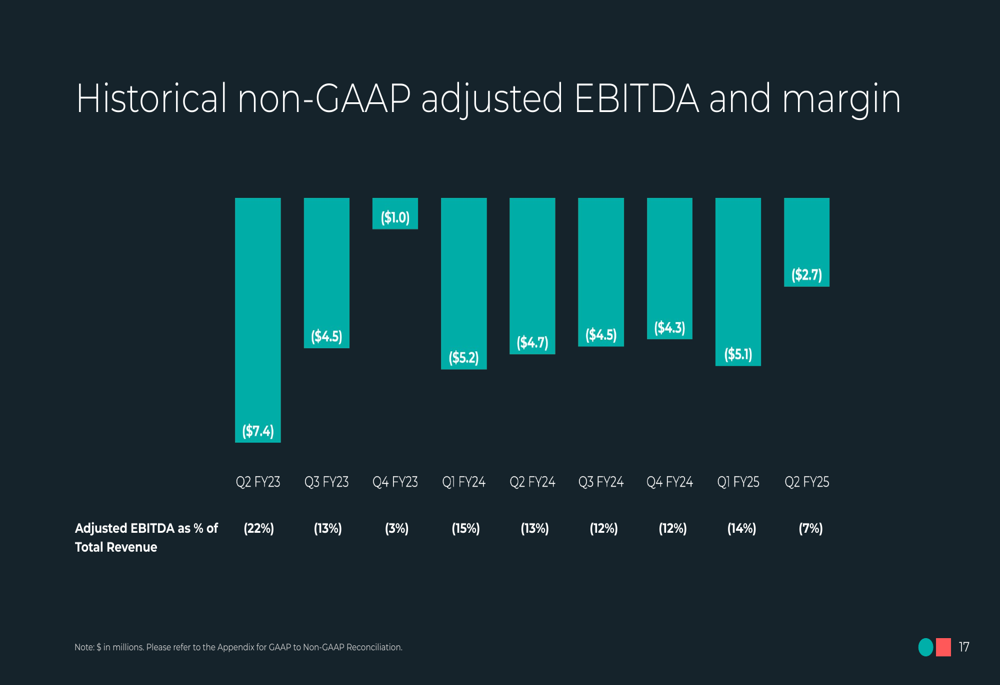

CS Disco has made significant progress in improving its financial trajectory, with adjusted EBITDA loss narrowing from $7.4 million (22% of revenue) in Q2 FY23 to $2.7 million (7% of revenue) in Q2 FY25:

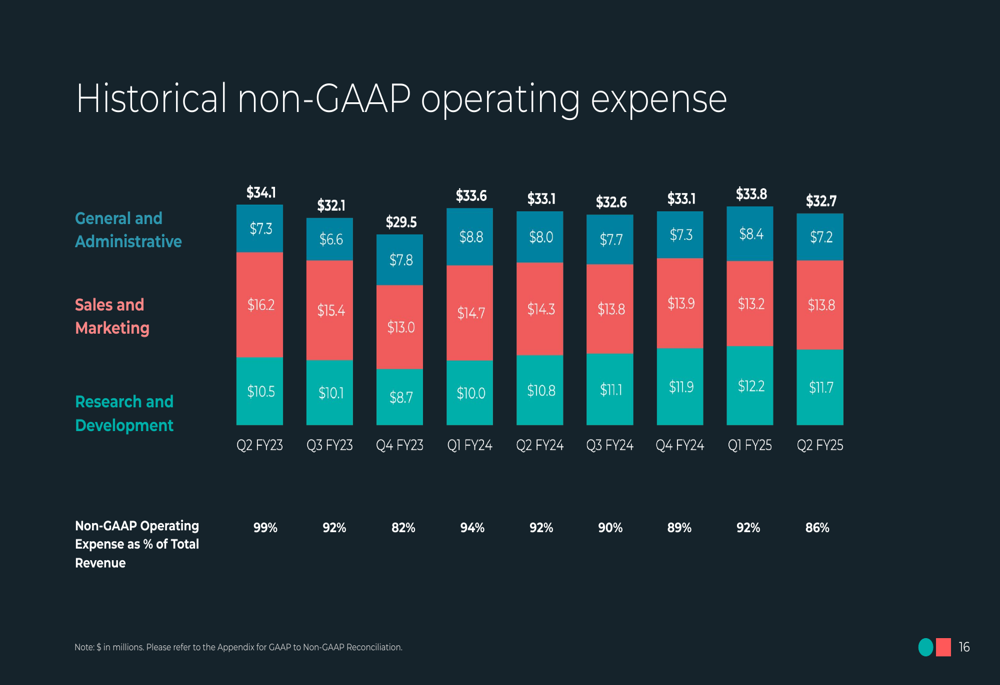

This improvement has been driven by disciplined expense management, with non-GAAP operating expenses decreasing from 99% of revenue in Q2 FY23 to 86% in Q2 FY25:

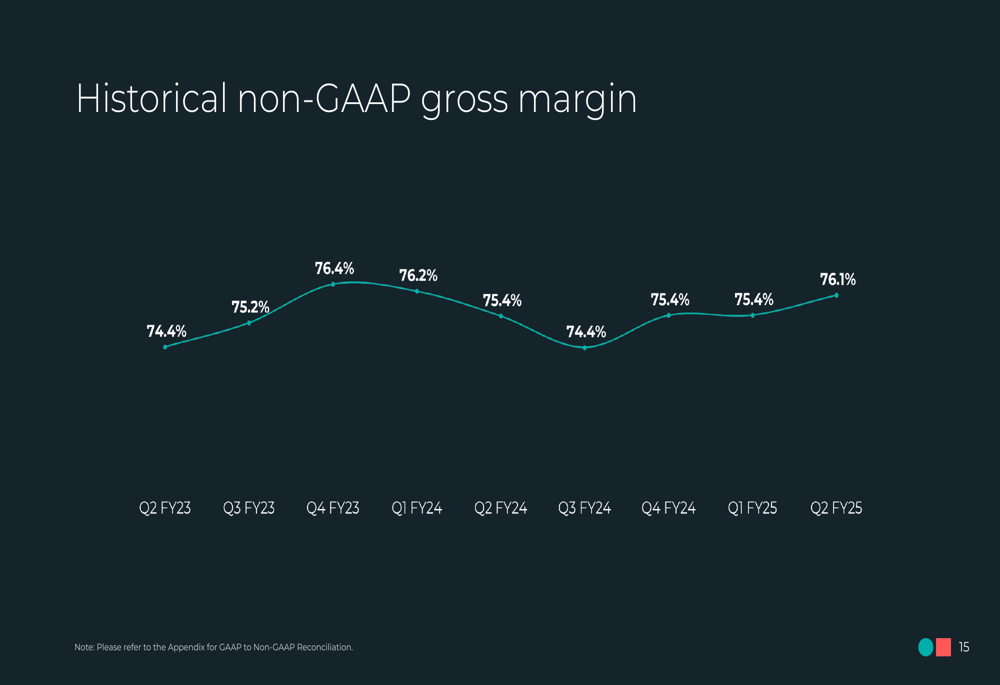

The company has maintained consistent gross margins over the past nine quarters, hovering between 74% and 76%:

CFO Michael LaFaire outlined the company’s financial goals during the earnings call, stating, "Our goal is to be adjusted EBITDA positive or breakeven in 2026." This aligns with the improving trend visible in the financial slides.

Forward-Looking Statements

CS Disco’s growth strategy focuses on expanding wallet share with existing customers, increasing the number of large, multi-terabyte matters, and growing volume commitments while improving sales and marketing efficiency:

Looking ahead, the company projects third-quarter revenue between $37.5 million and $39.5 million, and fiscal year 2025 revenue between $148 million and $158 million. Management remains focused on achieving EBITDA breakeven by 2026, with a target growth trajectory exceeding 20%.

However, the company faces several challenges, including revenue shortfalls against expectations, high competition in the legal tech industry, execution risks with new product launches, and economic uncertainties that could affect customer spending. The company’s ability to achieve its EBITDA breakeven target by 2026 will depend on successfully balancing growth investments with operational efficiency.

With a current stock price of $4.13, well within its 52-week range of $3.31 to $6.64, investors appear to be taking a cautious approach as they monitor the company’s progress toward profitability while evaluating its growth potential in the expanding legal technology market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.