Missed the webinar? Here are Investing.com’s top 10 stock picks for 2026

Introduction & Market Context

CSN Mineração (CMIN3) released its third-quarter 2025 results on November 5, showcasing record operational performance and substantial financial improvements. Despite beating analyst expectations with an earnings per share of $0.1715 (versus forecast of $0.1591) and revenue of $4.25 billion (exceeding the $4.10 billion forecast), the company's stock fell 4.02% in post-market trading to $5.73.

The Brazilian iron ore producer benefited from rising commodity prices during the quarter, with Platts 62% Fe prices increasing from US$99.1/dmt in July to US$105.3/dmt by September. This favorable pricing environment, combined with operational efficiencies, helped drive the company's strongest quarterly performance to date, though investors appeared to focus on broader market concerns rather than the immediate results.

Quarterly Performance Highlights

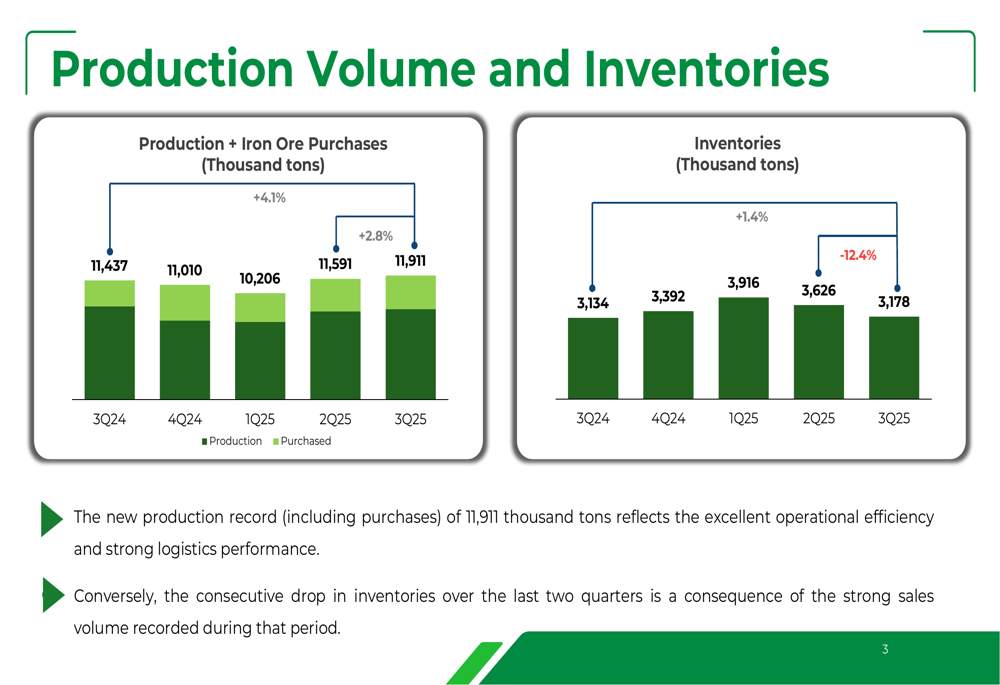

CSN Mineração achieved new quarterly production and sales records, demonstrating the company's operational strength. Production volume (including purchases) reached 11.9 million tons, representing a 4.1% increase compared to the same period last year and a 2.8% improvement over the previous quarter.

As shown in the following chart of production volumes and inventory levels:

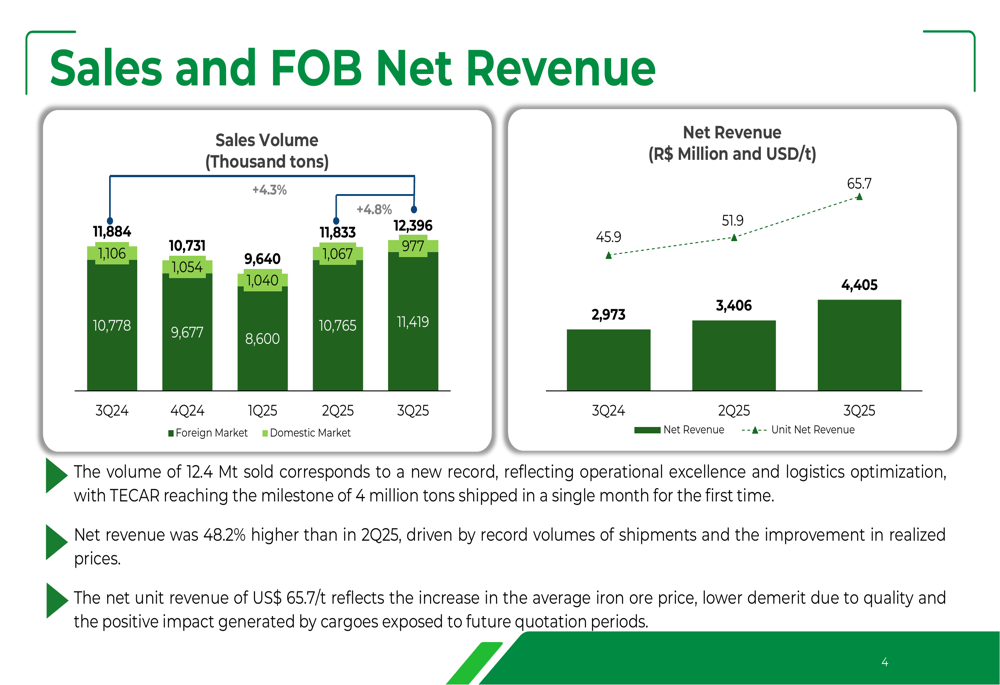

Sales volume set an unprecedented record at 12.4 million tons, marking the first time the company exceeded 12 million tons in quarterly sales. This represents a 4.3% year-over-year increase and a 4.8% improvement from Q2 2025. The strong sales performance contributed to a consecutive drop in inventory levels, which fell by 12.4% quarter-over-quarter to 3.2 million tons.

The record sales volume translated directly into substantial revenue growth, as illustrated in this revenue chart:

Net revenue surged to R$4,405 million, a remarkable 48.2% increase compared to the previous quarter. This growth was driven by both the record shipment volumes and improved unit net revenue, which reached US$65.7/ton, reflecting higher iron ore prices and lower quality demerits.

Detailed Financial Analysis

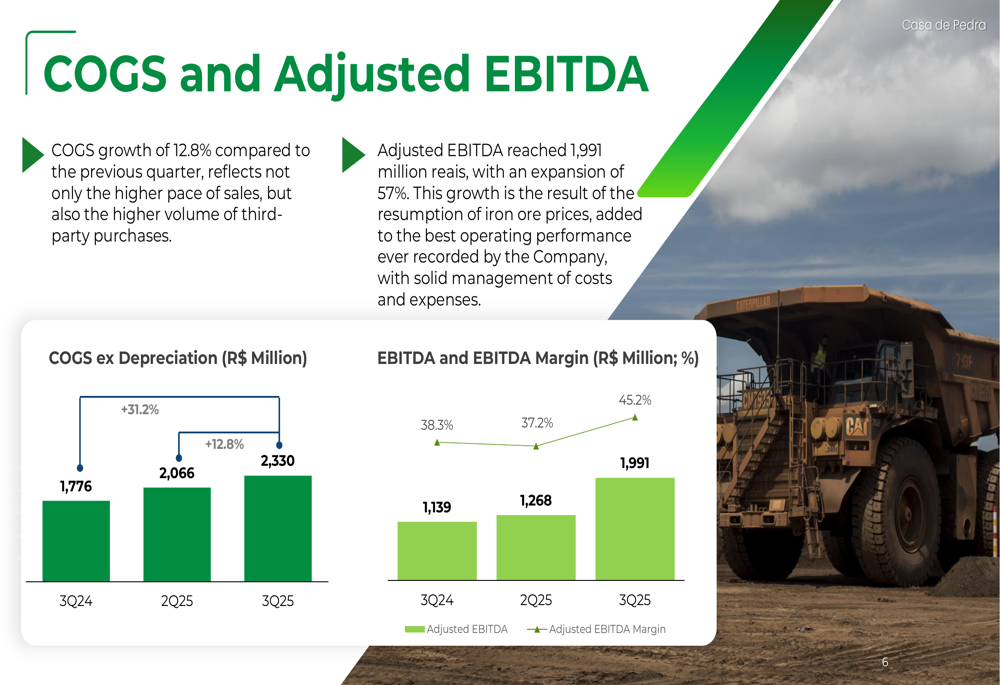

The company's cost of goods sold (excluding depreciation) increased by 12.8% quarter-over-quarter to R$2,330 million, primarily due to higher sales volumes and increased third-party purchases. However, this cost increase was more than offset by revenue growth, resulting in substantial profitability improvements.

The following chart illustrates the relationship between costs and EBITDA:

Adjusted EBITDA reached R$1,991 million with a 45.2% margin, representing a 57% expansion compared to Q2 2025. This remarkable improvement stemmed from higher iron ore prices and the company's best-ever operating performance, supported by effective cost and expense management.

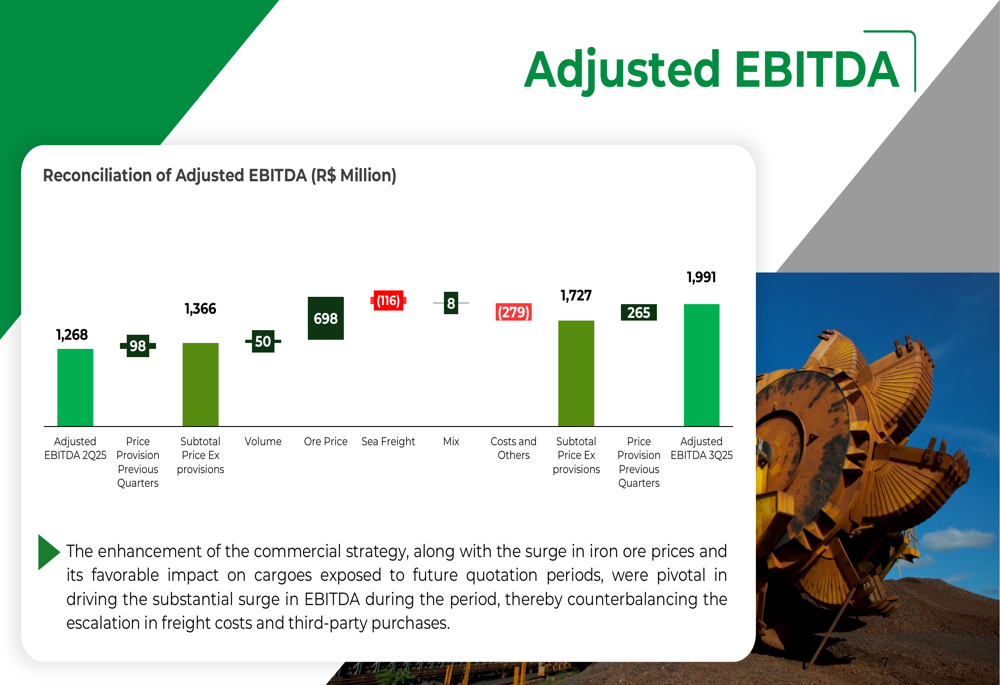

The drivers behind the EBITDA growth are detailed in this reconciliation chart:

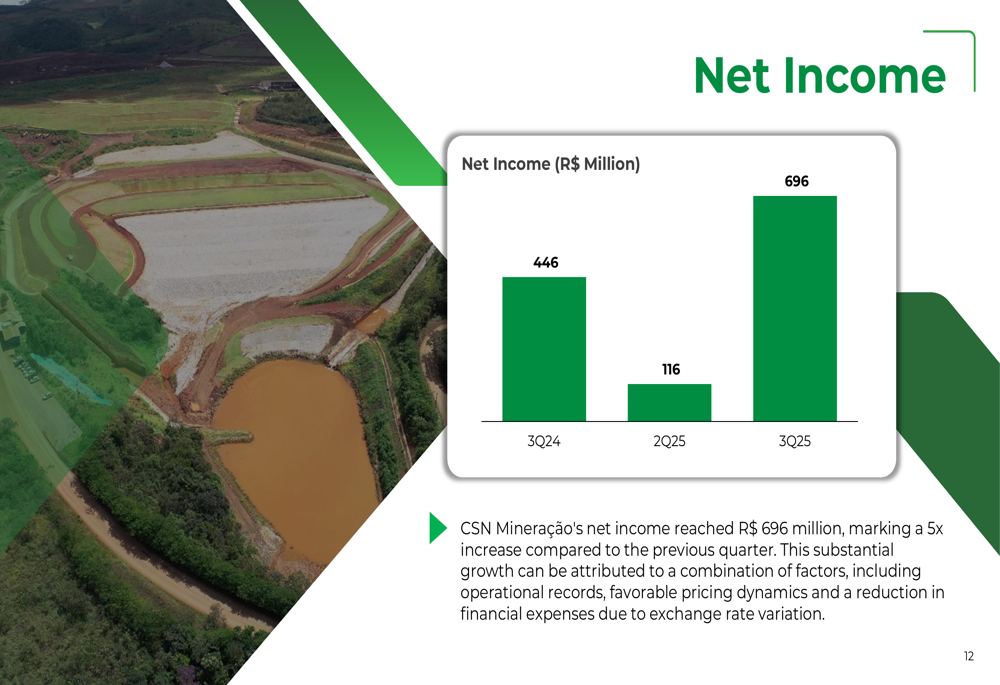

Net income soared to R$696 million, a fivefold increase from the previous quarter's R$116 million. This dramatic improvement can be attributed to the combination of operational records and favorable pricing dynamics, as shown in the following chart:

Despite higher working capital consumption, increased CAPEX, and negative financial expenses, CSN Mineração generated positive adjusted free cash flow of R$284 million. The company maintained a strong balance sheet, ending the quarter with R$13.6 billion in cash and cash equivalents, resulting in a net cash position of R$3.9 billion and a leverage ratio (Net Debt/EBITDA LTM) of -0.59x.

Strategic Initiatives & CAPEX

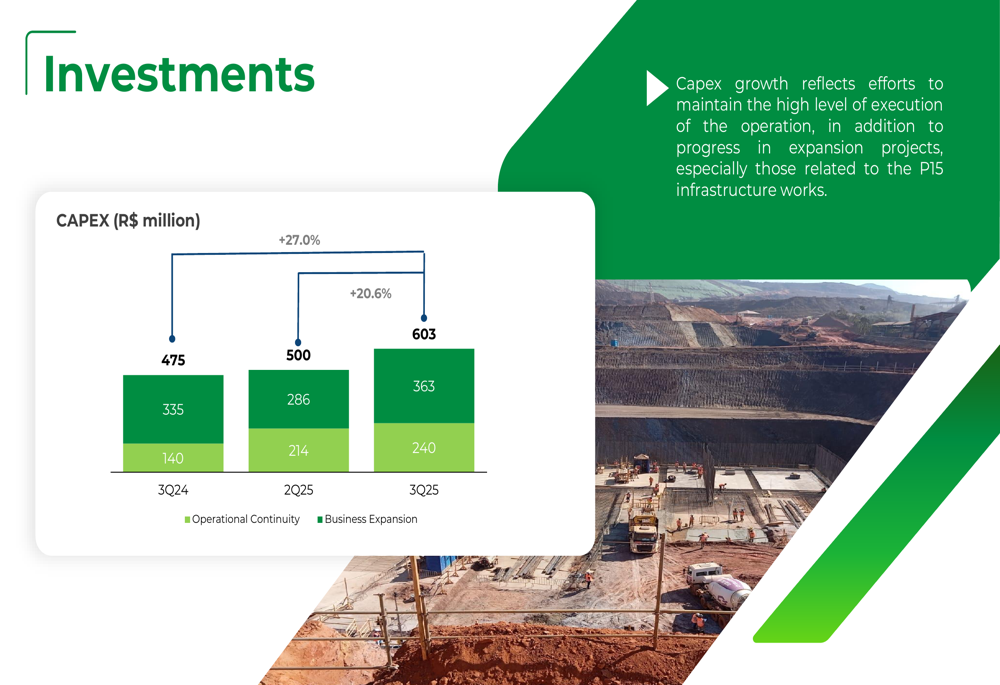

Capital expenditures increased by 20.6% quarter-over-quarter to R$603 million, reflecting the company's commitment to maintaining operational efficiency while advancing expansion projects. The CAPEX was divided between operational continuity (R$363 million) and business expansion (R$240 million), with particular emphasis on infrastructure works related to the P15 project.

The following chart details the CAPEX allocation over recent quarters:

The P15 project represents a significant growth opportunity for CSN Mineração, with expected ramp-up in 2028 according to the earnings call. During the call, management highlighted that this project will deliver "a very appealing return to shareholders," though specific metrics were not disclosed in the presentation.

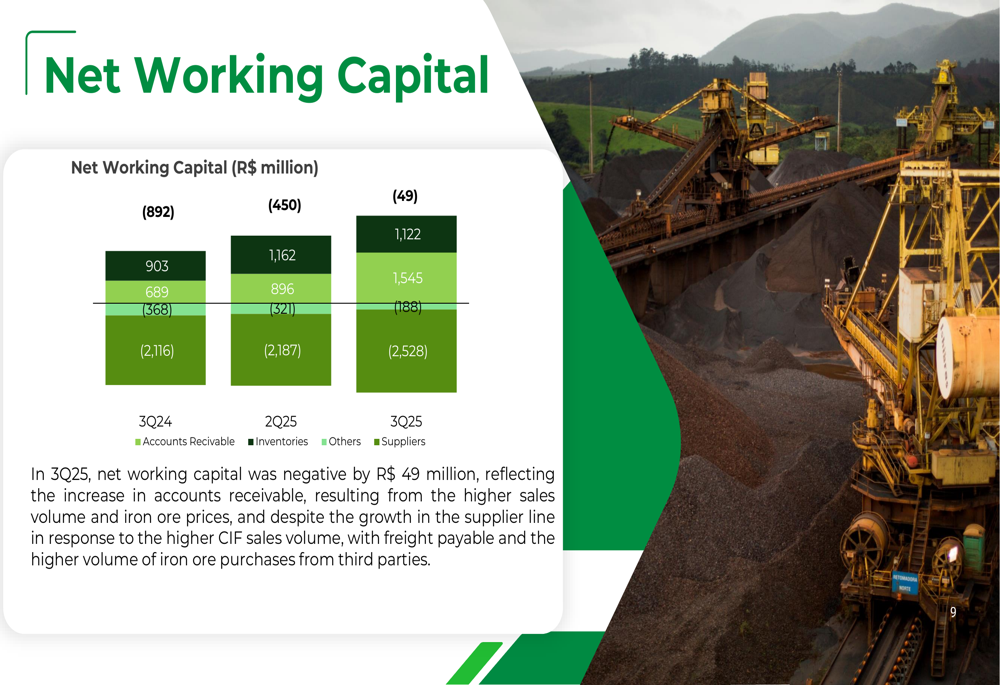

Working capital management showed improvement, with net working capital reduced to a negative R$49 million. This reflects an increase in accounts receivable offset by growth in the supplier line, driven by higher freight payables and increased third-party iron ore purchases.

Forward-Looking Statements & ESG Initiatives

Looking ahead, CSN Mineração has set a volume guidance of 43.5-47.5 million tons for 2026, as mentioned in the earnings call. The company maintains its dividend payout policy of 80-100% of net income, underscoring its commitment to shareholder returns.

On the sustainability front, CSN Mineração highlighted several ESG achievements, including the publication of its 2023/2024 Climate Action Report and recognition as the 7th highest-rated company by Sustainalytics. The company surpassed its 2025 target for female representation, achieving 26.2%, and maintained its strong safety record with over 11 years without fatalities.

During the earnings call, Board President Benjamin Steinbruch expressed optimism about market conditions, stating, "Demand continues very good, prices are good, margins are good." However, investors should note that future EPS forecasts suggest more modest growth, with projections of $0.02 for Q4 2025 and $0.01 for Q1 2026, according to analyst estimates.

Despite the strong operational and financial performance demonstrated in this presentation, market reaction remains cautious, with the stock declining 4.02% following the results announcement. This disconnect between performance and market sentiment may reflect broader concerns about future iron ore demand, particularly related to Chinese steel production, or potential macroeconomic headwinds that could impact commodity prices in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.