SoFi stock falls after announcing $1.5B public offering of common stock

Introduction & Market Context

CSX Corporation (NASDAQ:CSX) presented its second quarter 2025 results on July 23, showing sequential improvement across key metrics despite year-over-year challenges. The railroad operator’s stock closed at $35.23, down 0.78% on the day, but has recovered significantly from its 52-week low of $26.22 following a disappointing first quarter.

The company’s presentation highlighted operational efficiency gains and network performance improvements that helped offset continued pressure in key segments like coal and merchandise. After missing analyst expectations in Q1 with an EPS of $0.34, CSX delivered on its promise that Q1 would represent an "earnings trough," with Q2 showing meaningful sequential improvement.

Quarterly Performance Highlights

CSX reported second quarter volume of 1,580k units, essentially flat year-over-year but up 4% sequentially from Q1. Revenue came in at $3,574 million, down 3% from the same period last year but also up 4% from the first quarter of 2025.

As shown in the following chart of quarterly operational and financial results:

Operating margin improved to 35.9%, representing a significant 550 basis point increase from Q1 2025, though still 320 basis points below Q2 2024 levels. Earnings per share reached $0.44, up 29% sequentially but down 10% year-over-year.

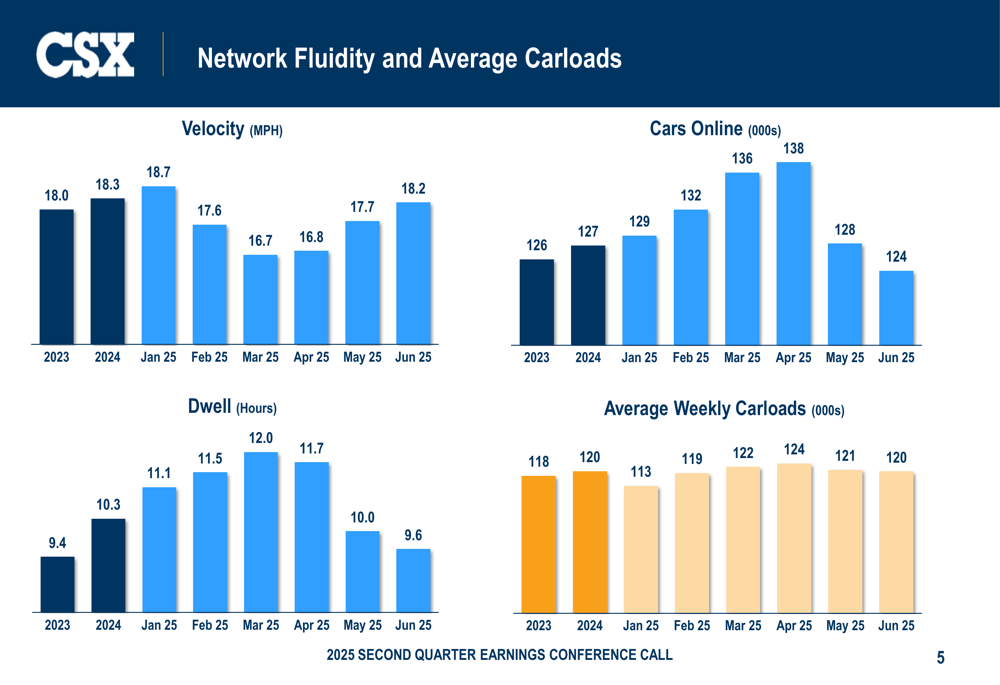

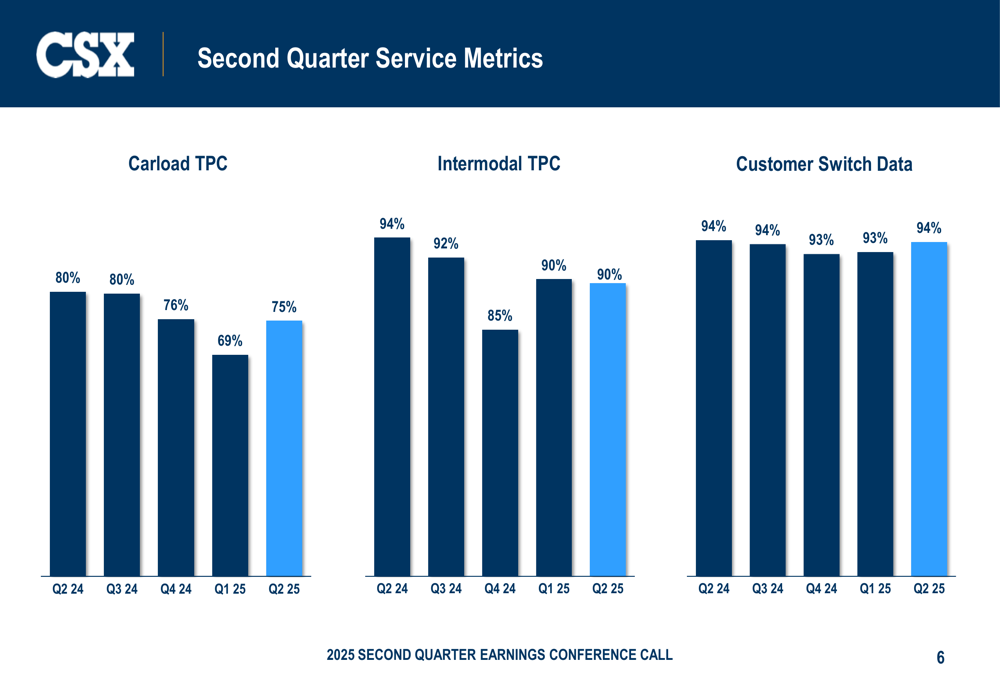

The company’s safety performance showed mixed results. The personal injury frequency index improved year-over-year to 0.99 from 1.33, but the train accident rate increased to 3.70 from 2.86 in the same period last year. Management noted that three-quarters of train accidents occur in yards and terminals, which are now a focus area for improvement.

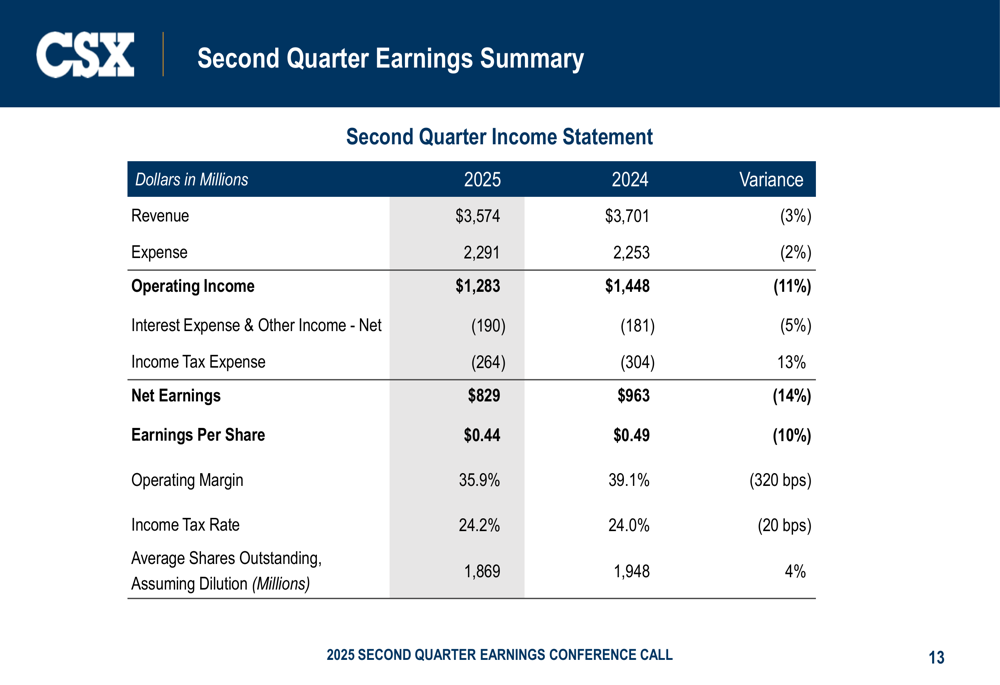

Detailed Financial Analysis

The comprehensive earnings summary reveals the full financial picture for the quarter:

Net earnings totaled $829 million, down 14% from $963 million in Q2 2024. Revenue declines were partially offset by expense management, with operating income reaching $1,283 million compared to $1,448 million in the prior year. The company’s effective tax rate remained relatively stable at 24.2%.

On the expense side, CSX demonstrated cost control with sequential improvements in several categories:

Labor and fringe expenses decreased by $30 million from Q1 to $791 million, though still $25 million higher than the prior year. Purchased services and other expenses saw a significant sequential reduction of $64 million. Fuel expenses provided a $32 million year-over-year benefit, reflecting lower diesel prices.

Cash flow and shareholder returns showed a mixed picture:

Free cash flow before dividends for the first half of 2025 totaled $444 million, substantially lower than the $1,150 million generated in the same period of 2024. This decline reflects higher capital expenditures, including spending on the Blue Ridge rebuild. Despite lower cash generation, CSX increased shareholder distributions, with dividends rising to $1,172 million from $810 million in the prior year period.

Business Segment Performance

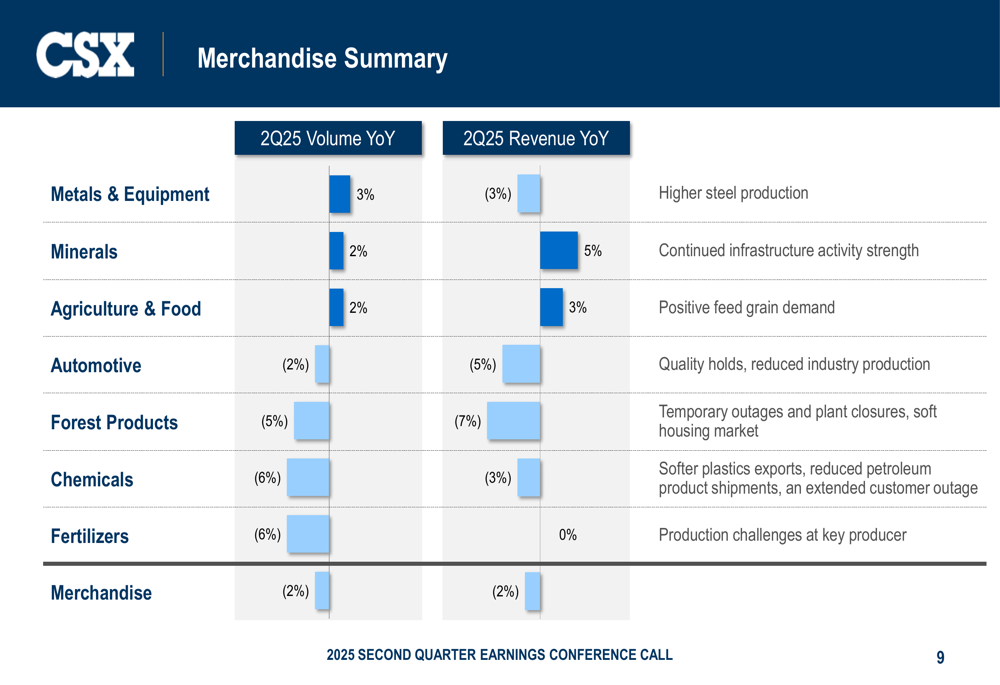

CSX’s merchandise segment, which represents a significant portion of its business, faced modest headwinds with both volume and revenue declining 2% year-over-year:

Within merchandise, performance varied significantly by category. Metals & equipment, minerals, and agriculture & food products all showed positive volume growth, while automotive, forest products, chemicals, and fertilizers experienced declines. The company cited temporary plant outages, a soft housing market, and reduced plastics exports as factors affecting these segments.

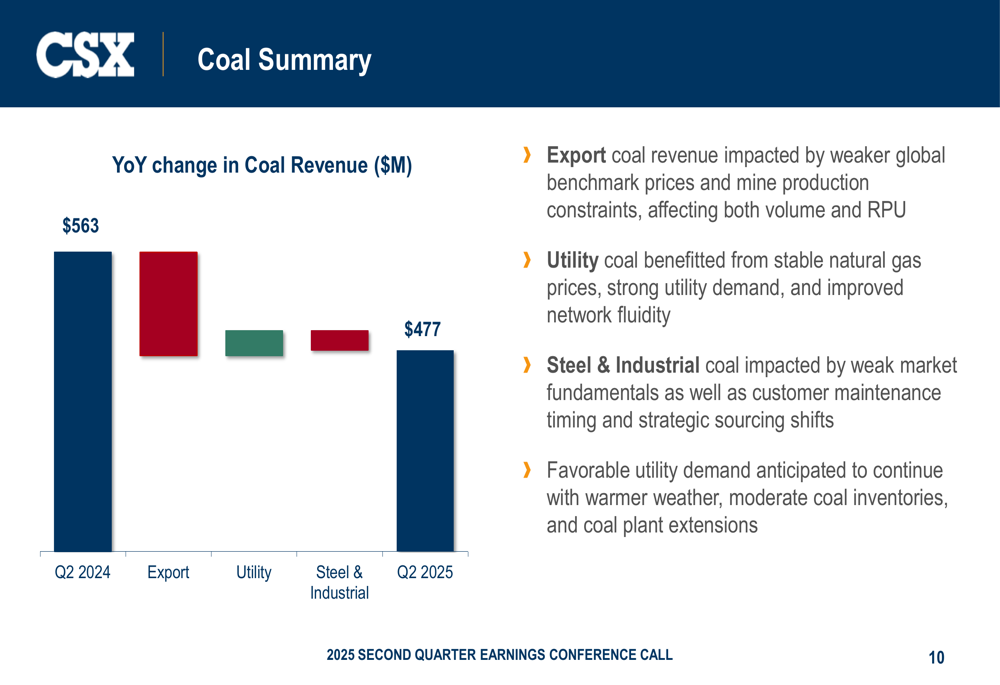

Coal revenue declined substantially from $563 million in Q2 2024 to $477 million in Q2 2025:

The drop in coal revenue was primarily attributed to weaker global benchmark prices and mine production constraints affecting export coal. However, utility coal benefited from stable natural gas prices and strong utility demand, which management expects to continue with warmer weather and moderate coal inventories.

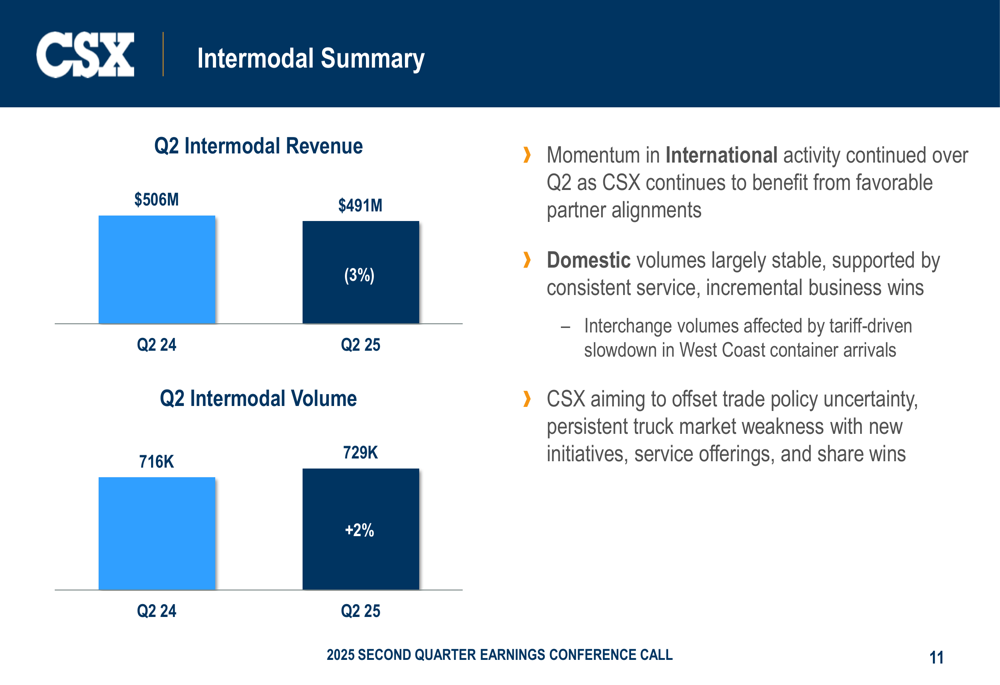

Intermodal showed resilience with volume growth of 2% year-over-year to 729,000 units, though revenue declined 3% to $491 million:

Management highlighted continued momentum in international activity and stable domestic volumes supported by consistent service and incremental business wins. The company is working to offset trade policy uncertainty and persistent truck market weakness through new initiatives, service offerings, and market share gains.

Strategic Initiatives

CSX continues to advance key infrastructure projects that are expected to enhance network capacity and efficiency:

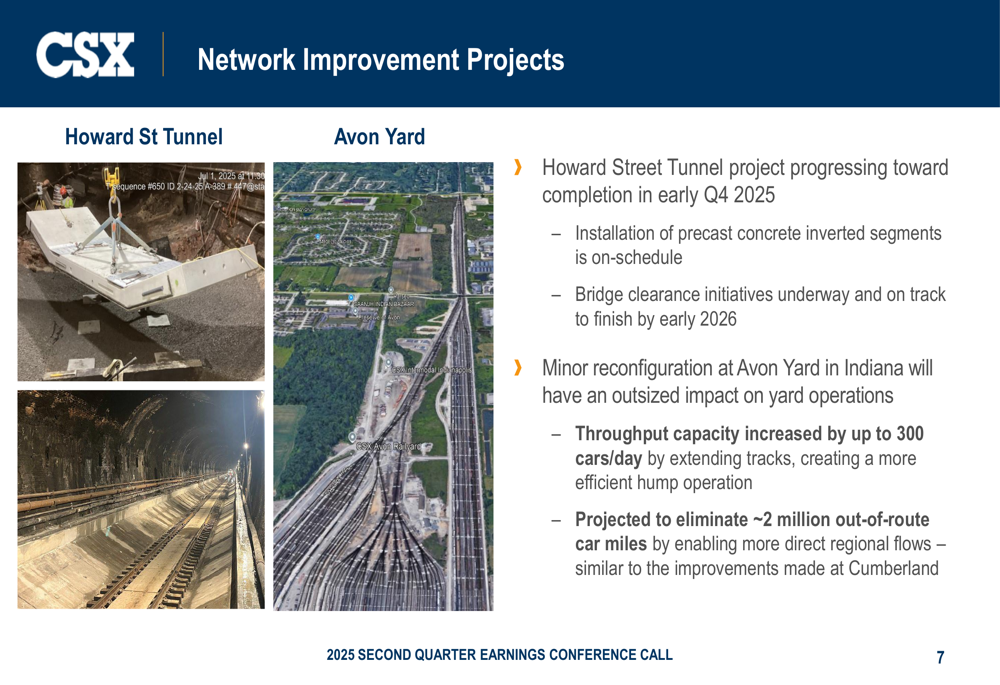

The Howard Street Tunnel project is progressing toward completion in early Q4 2025, with installation of precast concrete segments on schedule. This project, along with bridge clearance initiatives expected to finish by early 2026, will significantly improve the company’s ability to handle double-stack container traffic.

Additionally, the reconfiguration of Avon Yard in Indiana is projected to increase throughput capacity by up to 300 cars per day and eliminate approximately 2 million out-of-route car miles by enabling more direct regional flows.

Forward-Looking Statements

Looking ahead, CSX maintained its outlook for overall volume growth in fiscal year 2025:

Management expects smaller year-over-year revenue headwinds in the second half from lower export coal benchmarks and diesel prices. The company emphasized its continued focus on operational excellence, labor productivity, and efficiency initiatives.

Capital expenditures are expected to remain roughly flat year-over-year, excluding hurricane rebuild spending. CSX also reiterated its commitment to a balanced and opportunistic approach to capital returns, despite the significant decline in free cash flow during the first half of the year.

Executive Commentary

The presentation’s key takeaways emphasized the company’s progress in navigating challenging market conditions:

Management highlighted strong sequential improvement in network performance and ongoing focus on efficiency and cost control. The company remains confident that its operational momentum, service leadership, and new business wins will help it manage through mixed market conditions.

This message aligns with CEO Joe Hinrichs’ comments from the Q1 earnings call, where he identified Q1 as the earnings trough and expressed confidence in the company’s ability to improve performance through the remainder of the year.

As CSX continues to execute on its strategic initiatives while navigating a complex market environment, investors will be watching closely to see if the sequential improvements demonstrated in Q2 can be sustained through the second half of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.