Curb partners with Lyft to integrate ride requests into taxi platform

Introduction & Market Context

CSX Corporation (NASDAQ:CSX) presented its third-quarter 2025 results on October 16, revealing a year-over-year revenue decline but sequential operational improvements across key metrics. The railroad operator’s shares rose 1.49% to $36.78 in after-hours trading following the presentation, suggesting investors were encouraged by the company’s operational progress despite financial headwinds.

The presentation highlighted CSX’s continued focus on efficiency and safety improvements in a challenging economic environment characterized by mixed market conditions across its business segments. While intermodal showed solid growth, coal revenue declined significantly, and merchandise remained essentially flat.

Quarterly Performance Highlights

CSX reported third-quarter revenue of $3.59 billion, a slight decrease from $3.62 billion in the same period last year. Adjusted earnings per share came in at $0.44, down from $0.46 in Q3 2024, reflecting ongoing margin pressure despite operational improvements.

The company’s adjusted operating income was $1.25 billion, compared to $1.35 billion in the prior year, while adjusted operating margin contracted to 34.9% from 37.4%. These results were impacted by a $164 million goodwill impairment charge during the quarter.

As shown in the following earnings summary chart:

The company maintained its capital return program, distributing $1.28 billion in share buybacks and $730 million in dividends year-to-date, both representing increases from the prior year despite lower free cash flow generation.

Operational Improvements

CSX made significant strides in operational efficiency during the third quarter, with improvements across multiple key metrics. Train velocity increased to 18.9 MPH from 18.0 in 2023, while cars online decreased to 121,000 from 126,000. Dwell time improved to 9.5 hours from 11.5 hours in Q1 2025, and trip plan compliance rose to 87% from 84% in 2024.

These operational gains are illustrated in the following chart:

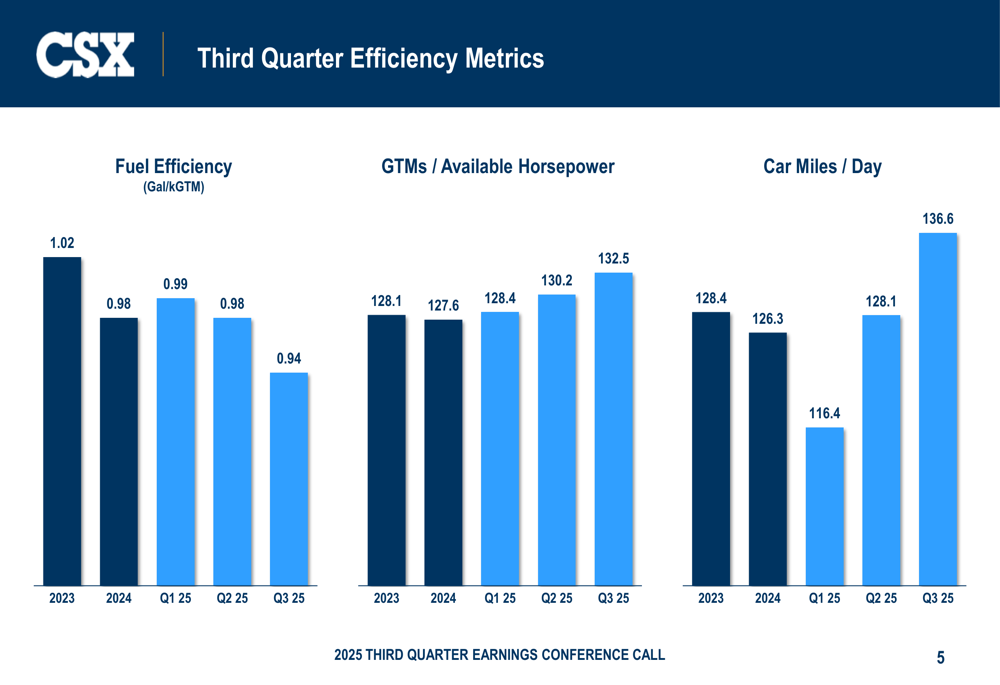

The company also reported notable efficiency improvements, with fuel efficiency enhancing to 0.94 gallons per thousand gross ton-miles from 1.02 in 2023. GTMs per available horsepower increased to 132.5 from 128.1, and car miles per day rose to 136.6 from 128.4.

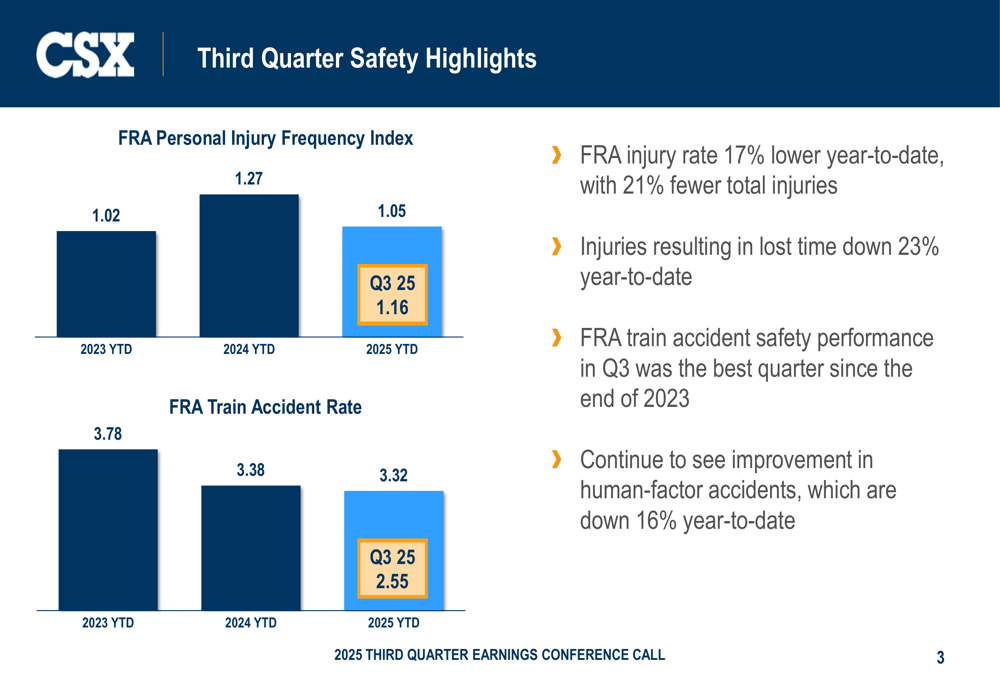

Safety performance showed marked improvement as well, with the FRA personal injury frequency index decreasing to 1.05 year-to-date from 1.27 in 2024. The FRA train accident rate also improved to 3.32 from 3.38, with Q3 performance at 2.55, representing the best safety performance since late 2023.

The following chart highlights these safety improvements:

Segment Performance Analysis

CSX’s business segments delivered mixed results in the third quarter, reflecting varied market conditions across industries.

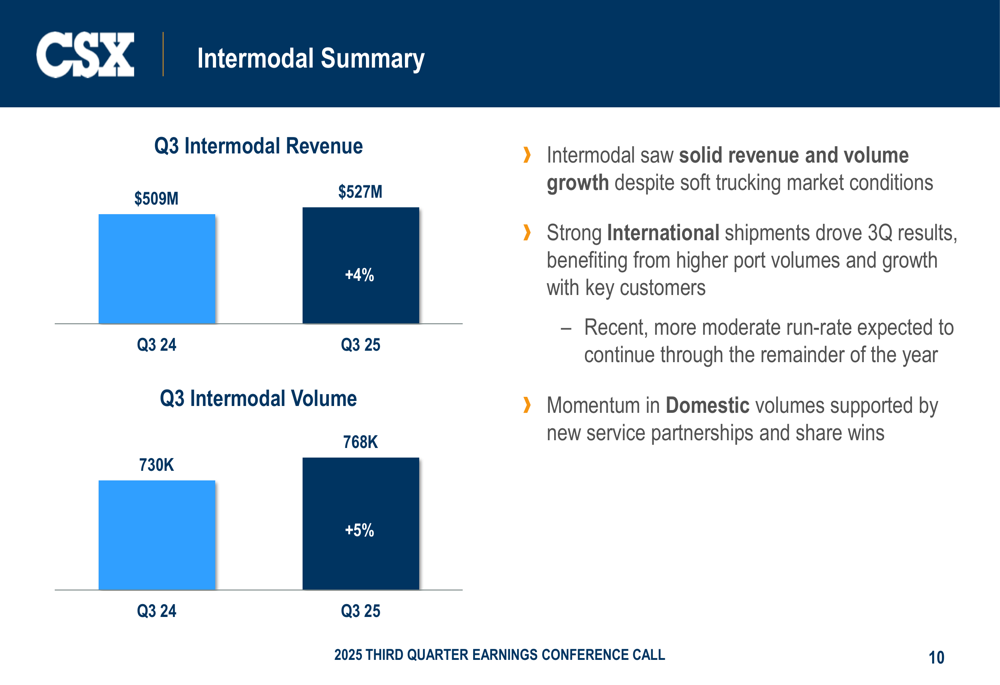

The intermodal business was a bright spot, with revenue increasing 4% to $527 million and volume rising 5% to 768,000 units compared to Q3 2024. Management attributed this growth to strong international shipments benefiting from higher port volumes and growth with key customers, despite a soft trucking market.

As shown in the intermodal performance chart:

The merchandise segment, which encompasses multiple commodity groups, saw both volume and revenue decline by 1% year-over-year. Within this segment, performance varied significantly by commodity:

Minerals showed the strongest performance with 8% volume growth and 12% revenue growth, driven by record aggregates shipments and continued infrastructure demand. Fertilizers and Metals & Equipment also performed well with 7% and 5% volume growth, respectively. However, these gains were offset by declines in Forest Products, Chemicals, and Agriculture & Food, all of which saw 7% volume decreases.

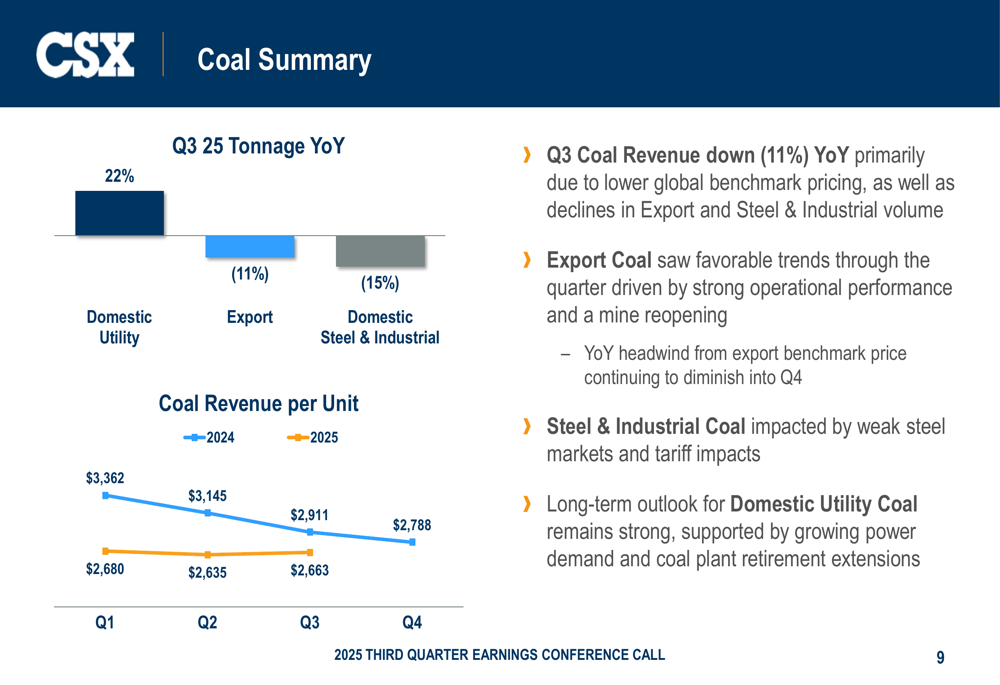

Coal revenue declined 11% year-over-year, primarily due to lower global benchmark pricing and volume declines in export and steel & industrial segments. While domestic utility coal tonnage increased by 22%, export coal fell 11% and domestic steel & industrial dropped 15%.

Financial Position and Capital Allocation

CSX’s third-quarter expense comparison revealed increases across most categories, with a notable $164 million goodwill impairment charge. Labor and fringe expenses increased to $815 million from $806 million, while purchased services rose to $730 million from $676 million. The company attributed these increases to severance costs, inflation, and network disruptions, partially offset by reduced incentive compensation and headcount efficiency.

The following chart details these expense comparisons:

Free cash flow before dividends decreased significantly to $1.07 billion for the first nine months of 2025, compared to $2.22 billion in the same period of 2024. This decline was driven by lower operating cash flow and increased capital expenditures, which rose to $1.79 billion from $1.69 billion.

Despite the cash flow reduction, CSX maintained its commitment to shareholder returns, with year-to-date share repurchases of $1.28 billion and dividends of $730 million, both higher than the prior year.

Forward Guidance

Looking ahead, CSX provided a relatively conservative outlook, projecting overall year-over-year volume growth for the full year 2025. The company expects to build on its operational performance and efficiency gains into the fourth quarter.

Capital expenditures for 2025 are projected at $2.5 billion, excluding hurricane rebuild spending. Management emphasized a balanced and opportunistic approach to capital returns, suggesting continued share repurchases and dividends despite cash flow pressures.

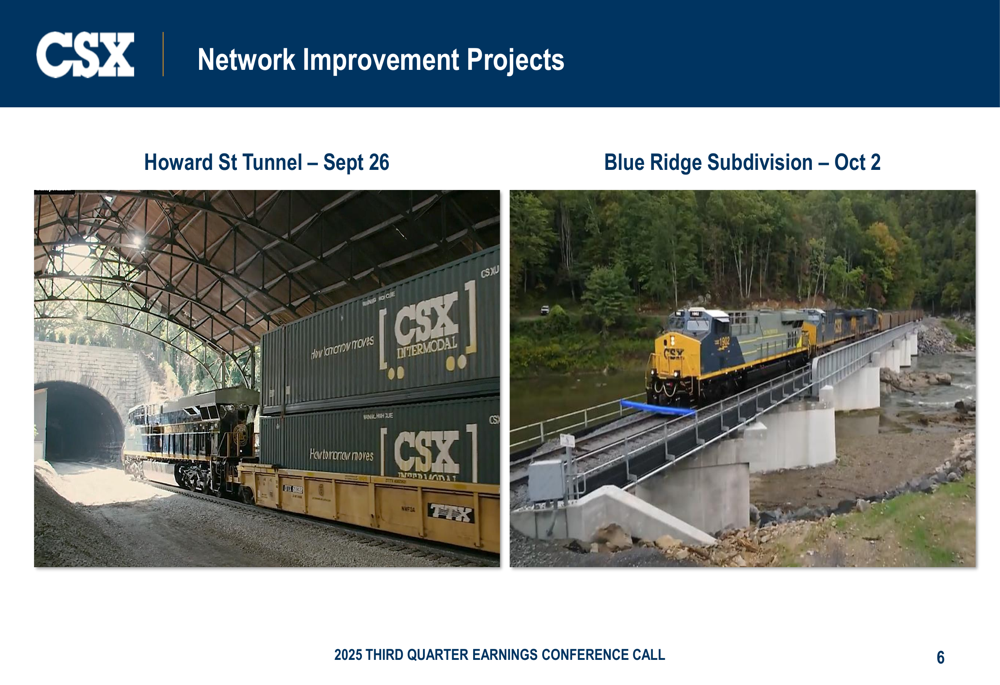

The company highlighted ongoing network improvement projects, including the Howard Street Tunnel and Blue Ridge Subdivision, which are expected to enhance capacity and efficiency. These infrastructure investments are illustrated in the following image:

In the coal segment, management noted that the long-term outlook for domestic utility coal remains strong, supported by growing power demand and coal plant retirement extensions. However, export coal continues to face headwinds from global benchmark pricing, and steel & industrial coal remains impacted by weak steel markets and tariff effects.

For intermodal, the company expects the recent, more moderate run-rate to continue through the remainder of the year, though momentum in domestic volumes is supported by new service partnerships and customer wins.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.