Street Calls of the Week

Introduction & Market Context

Soluciones Cuatroochenta Sa (BME:480S) released its first-half 2025 results on October 7, showcasing strong performance across key financial metrics. The Spanish technology company, which specializes in cybersecurity and software solutions, reported substantial growth that significantly outpaced industry forecasts, with shares rising 9.64% to €16.60 following the presentation.

The company’s diverse business portfolio spans cybersecurity, independent software vendors, value-added reseller services, and professional technology services, serving clients across various sectors including major companies like Mahou, RTVE, Endesa, and Vodafone.

Quarterly Performance Highlights

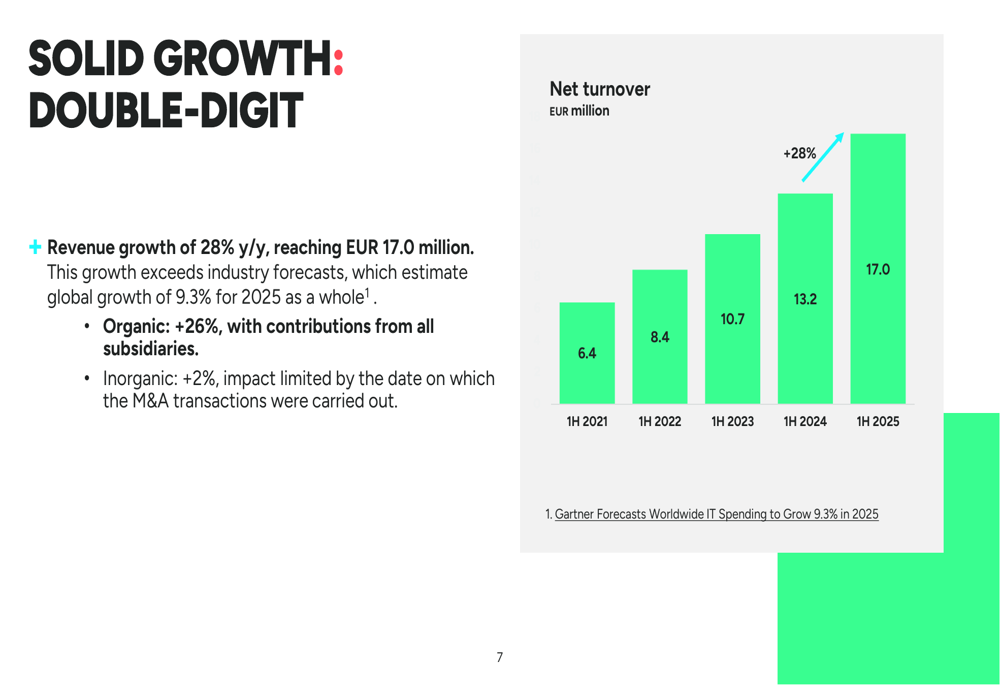

Cuatroochenta reported impressive revenue growth of 28% year-over-year, reaching €17.0 million for the first half of 2025. This performance substantially exceeded global industry growth forecasts of 9.3% for the year, with organic growth accounting for 26% of the increase and inorganic growth contributing an additional 2%.

As shown in the following chart of revenue progression, the company has maintained a strong growth trajectory over recent years:

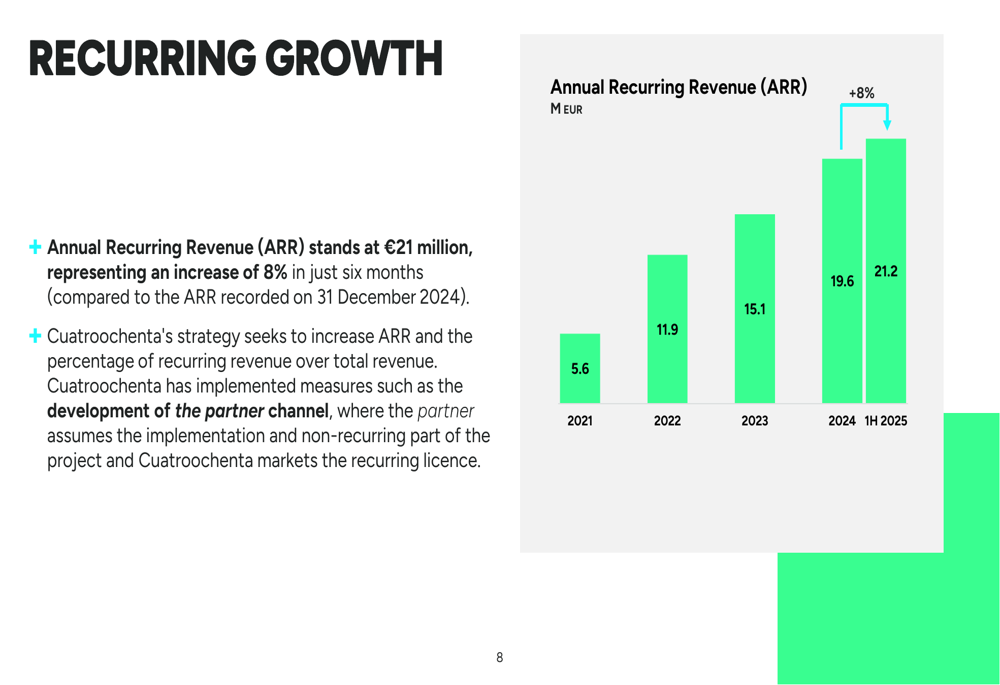

The company’s Annual Recurring Revenue (ARR) reached €21.2 million, representing an 8% increase in just six months. This metric is particularly significant as it reflects the company’s success in building a stable revenue base through subscription and recurring service models.

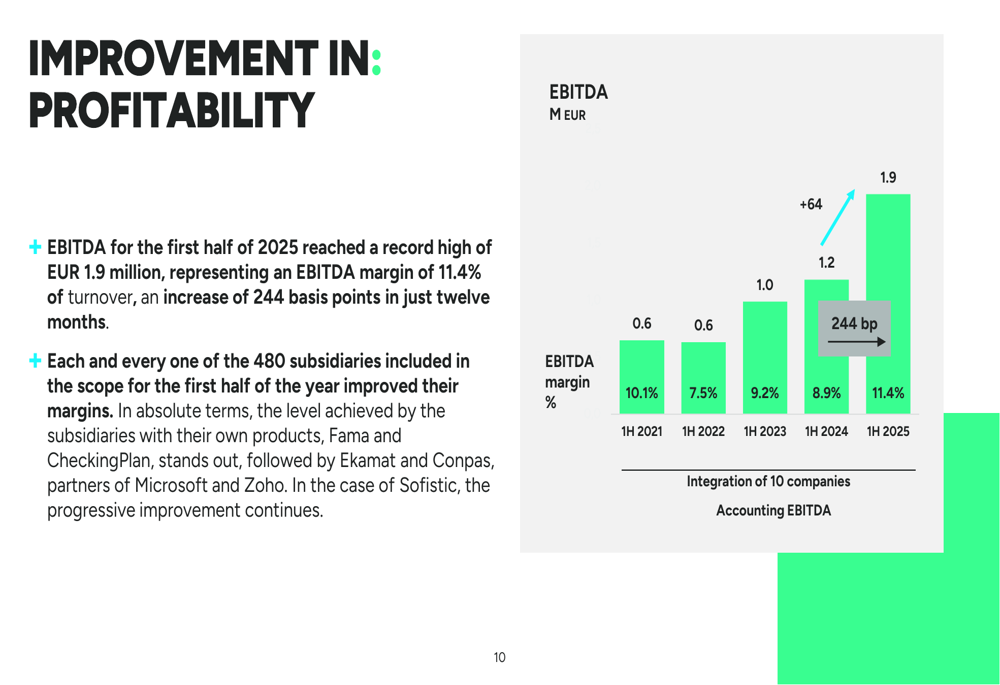

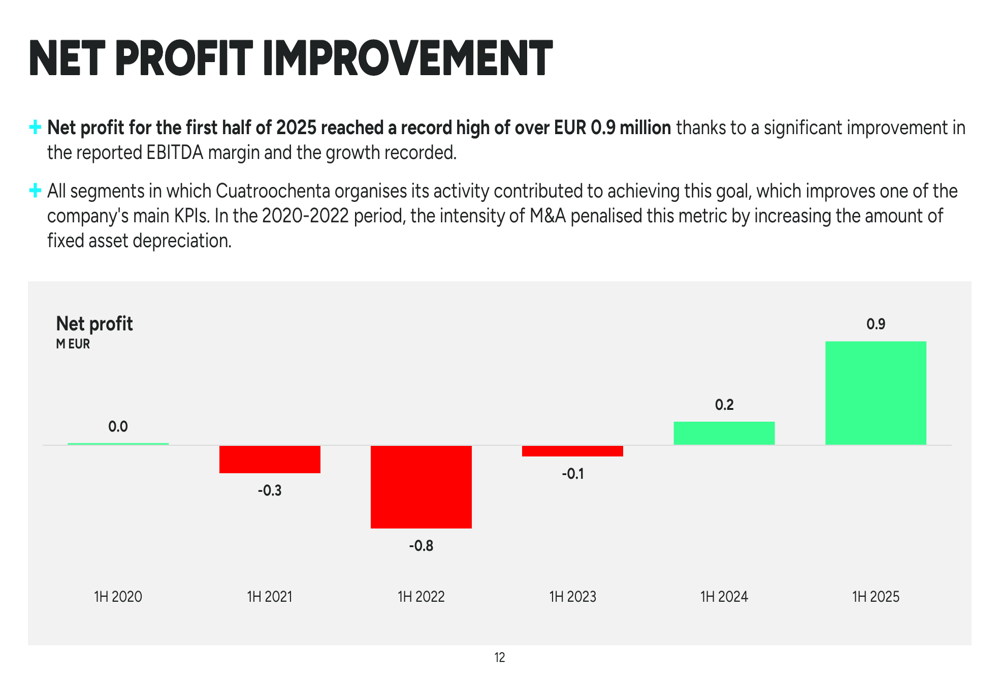

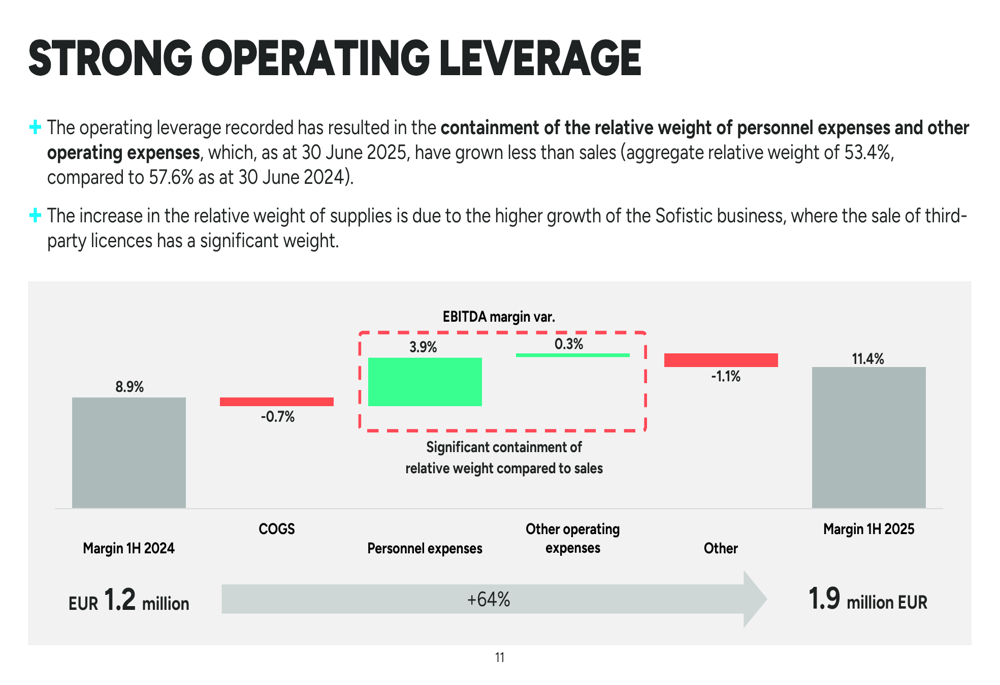

Profitability metrics showed even more dramatic improvements. EBITDA surged 64% year-over-year to €1.9 million, while net profit skyrocketed 339% to €0.9 million compared to the same period last year. The EBITDA margin expanded to 11.4%, up from 8.9% in the first half of 2024.

The following chart illustrates the company’s consistent improvement in profitability metrics:

Detailed Financial Analysis

Cuatroochenta’s revenue is geographically balanced, with Spain accounting for 52% of total revenue. By business segment, the company derives 47% of revenue from Cybersecurity, 27% from Value-Added Reseller (VAR) services, 16% from Independent Software Vendors (ISV), and 10% from Professional Technology Services (PTS).

The company’s net profit has shown remarkable improvement, turning from consistent losses in previous years to a record high of €0.9 million in the first half of 2025. This represents a dramatic turnaround in the company’s profitability trajectory.

The company’s strong operating leverage has been a key factor in its improved profitability. Personnel expenses contributed positively to margin expansion, while cost of goods sold had a slight negative impact. Overall, the operating margin improved from 8.9% in 1H 2024 to 11.4% in 1H 2025.

On the balance sheet side, Cuatroochenta reported net financial debt of €11.31 million, with a net financial debt to EBITDA ratio of 2.84x. The company maintains a cash position of €5.53 million. While debt levels have increased to support acquisitions, the improved profitability has helped maintain debt ratios at manageable levels.

Strategic Initiatives

During the first half of 2025, Cuatroochenta completed two strategic acquisitions that align with its growth strategy. On May 21, 2025, the company acquired Tresipunt, which specializes in E-learning solutions. This was followed by the acquisition of MP Services on June 30, 2025, a company providing anti-fraud services in e-commerce.

Additionally, the company secured a financing agreement in March 2025 for the issuance of €2 million in unsecured bonds convertible into shares. These bonds carry a 4% annual interest rate and a conversion price of €18 per share, providing the company with capital for its expansion initiatives while offering potential equity upside to investors.

The company also highlighted its 50% stake in Matrix Development System through Pavabits, which reported strong performance with revenue of €1.8 million (+21% y/y), EBITDA of €0.8 million (+25% y/y), and net profit of €0.5 million (+45% y/y).

Forward-Looking Statements

While the presentation did not provide explicit guidance for the remainder of 2025, the strong first-half performance positions Cuatroochenta well to continue its growth trajectory. The company’s focus on increasing Annual Recurring Revenue suggests a strategic emphasis on building stable, predictable revenue streams.

The recent acquisitions are expected to contribute to inorganic growth in the second half of the year, while the company’s improving profitability metrics indicate that it may continue to benefit from operating leverage as it scales.

With a diverse portfolio of business lines and a strong client base across multiple industries, Cuatroochenta appears well-positioned to capitalize on the growing demand for cybersecurity and digital transformation solutions. The company’s ability to outpace industry growth rates while simultaneously improving profitability metrics suggests effective execution of its business strategy.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.