Nvidia shares pop as analysts dismiss AI bubble concerns

Introduction & Market Context

Curtiss-Wright Corporation (NYSE:CW) presented its third-quarter 2025 results on November 6, highlighting strong performance across its defense and commercial segments. The aerospace and industrial technology provider reported significant growth in key financial metrics, leading management to raise full-year guidance despite challenging macroeconomic conditions.

The company's results reflect its strategic alignment with U.S. defense priorities and growing NATO funding, while also capitalizing on opportunities in commercial aerospace and nuclear power. Despite the positive earnings surprise, Curtiss-Wright's stock declined 1.56% following the announcement, closing at $585.12.

Quarterly Performance Highlights

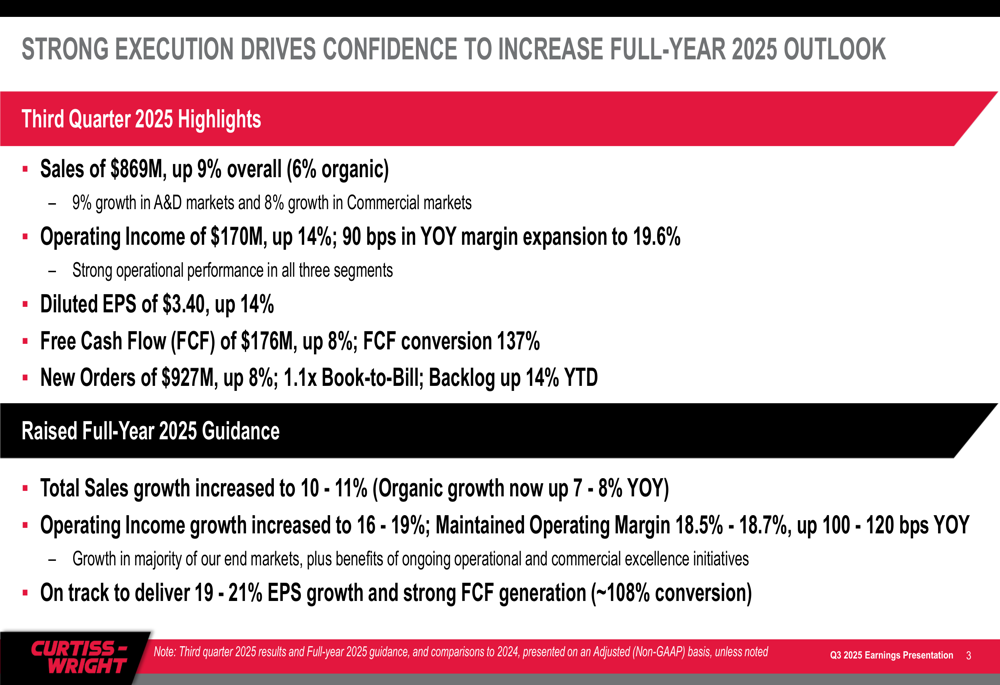

Curtiss-Wright delivered impressive third-quarter results, with sales reaching $869 million, representing a 9% increase (6% organic) compared to the same period last year. The company reported operating income of $170 million, up 14% year-over-year, with operating margin expanding by 90 basis points to 19.6%. Diluted earnings per share grew 14% to $3.40, exceeding analyst expectations of $3.30.

As shown in the following quarterly highlights chart:

Free cash flow generation remained strong at $176 million, an 8% increase year-over-year, with a conversion rate of 137%. New orders totaled $927 million, up 8% from Q3 2024, resulting in a book-to-bill ratio of 1.1x and a 14% year-to-date increase in backlog.

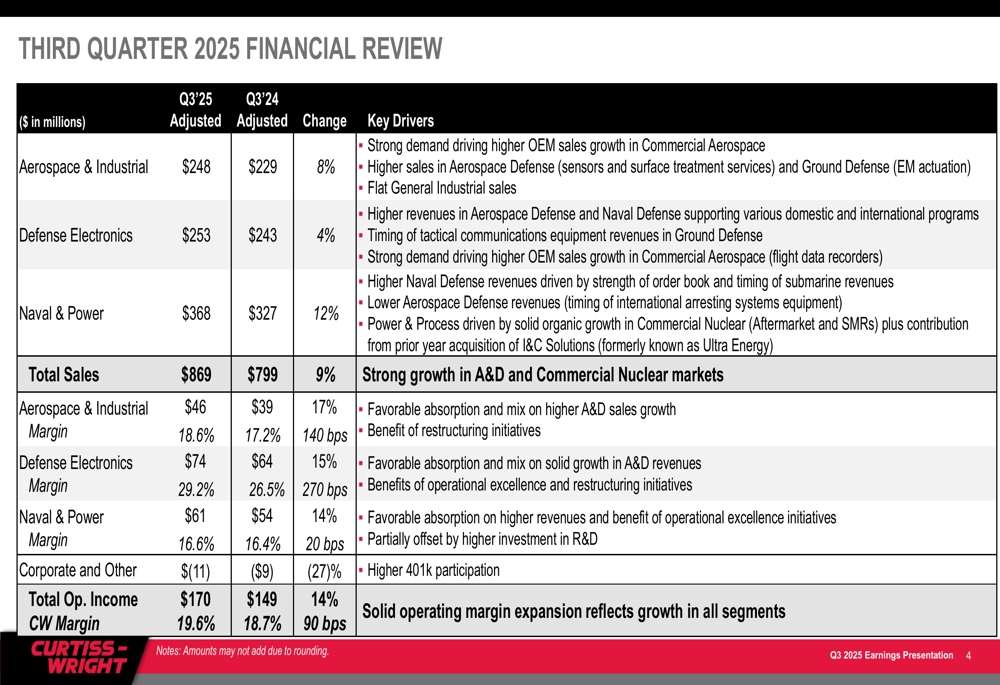

The detailed financial review by segment reveals the drivers behind this growth:

Detailed Financial Analysis

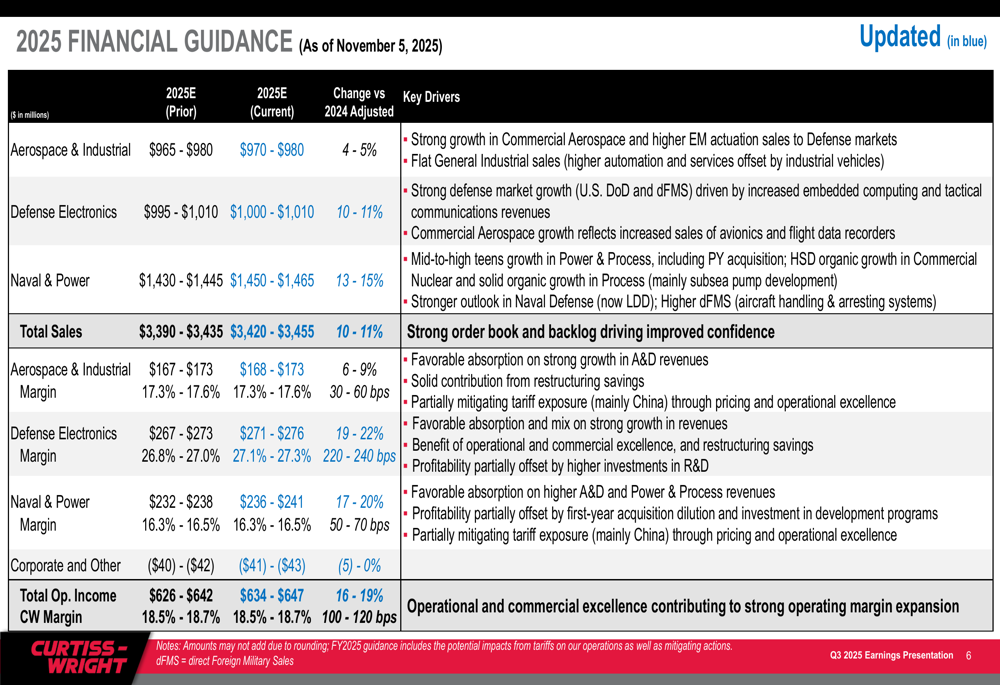

Curtiss-Wright's performance was bolstered by strong contributions across its business segments. The Defense Electronics segment saw a 10% increase in sales and a 13% rise in operating income, driven by higher sales of embedded computing and tactical communications equipment.

The Naval & Power segment reported a 9% sales increase and 14% growth in operating income, benefiting from higher naval defense revenues and solid organic growth in commercial nuclear power. Meanwhile, the Aerospace & Industrial segment achieved 8% sales growth and 14% operating income growth, primarily due to strong demand in commercial aerospace.

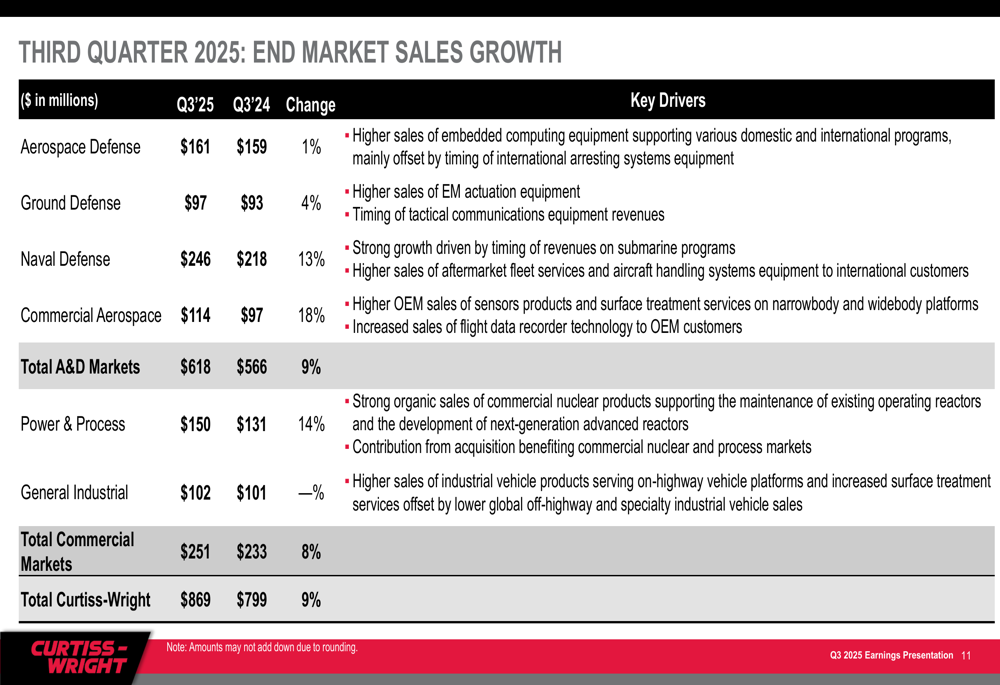

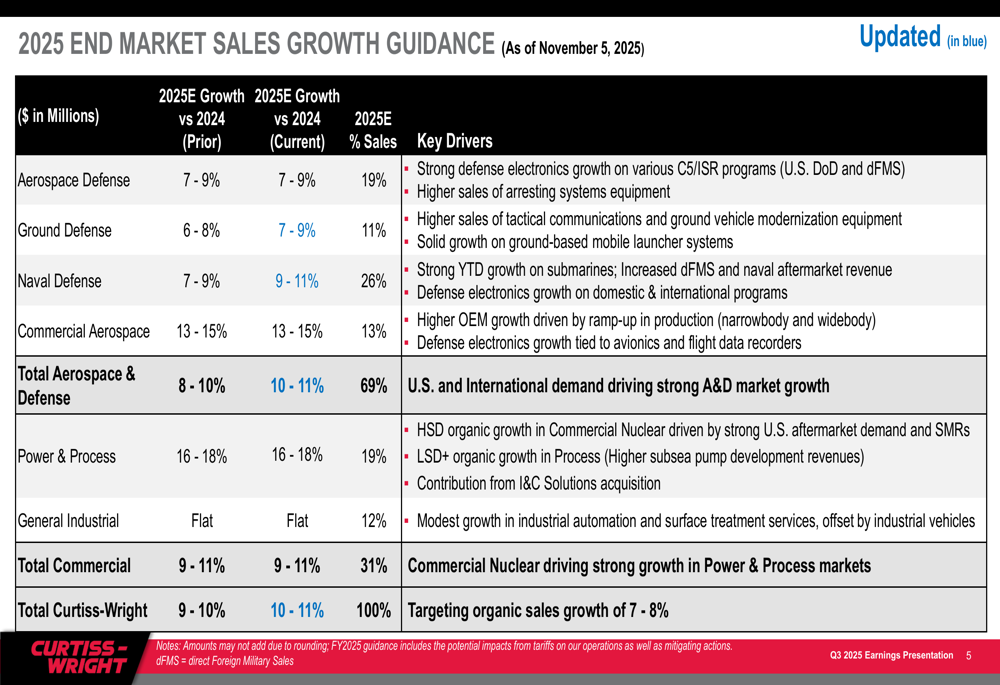

The company's end market sales growth for Q3 2025 shows strength across both defense and commercial sectors:

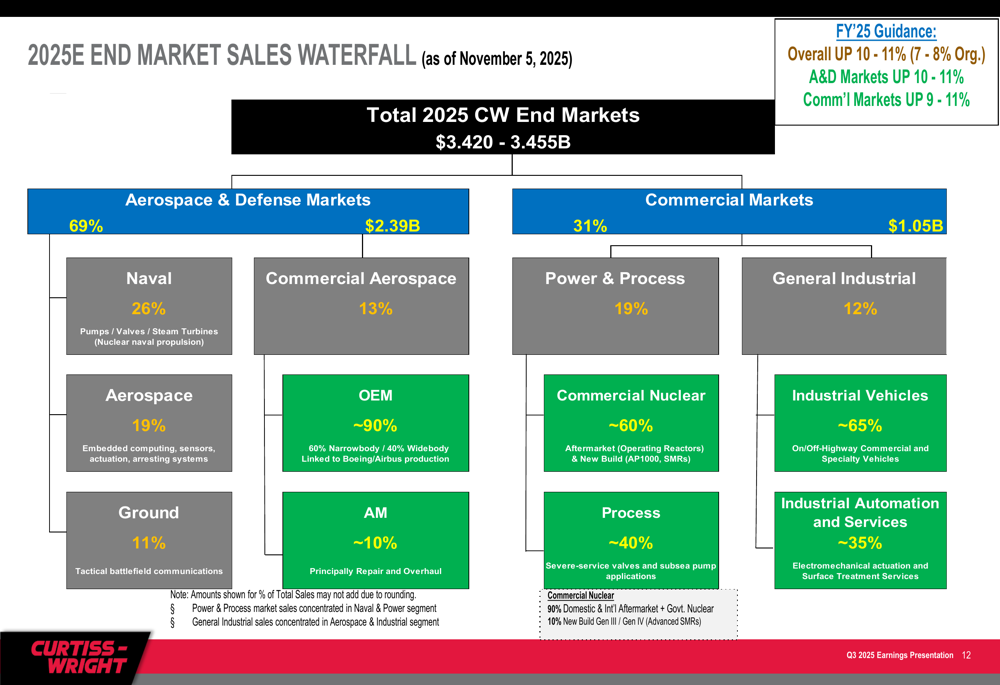

Looking at the projected full-year sales distribution across markets, Aerospace & Defense represents 69% of total sales at approximately $2.39 billion, while Commercial markets account for 31% at around $1.05 billion:

Forward-Looking Statements

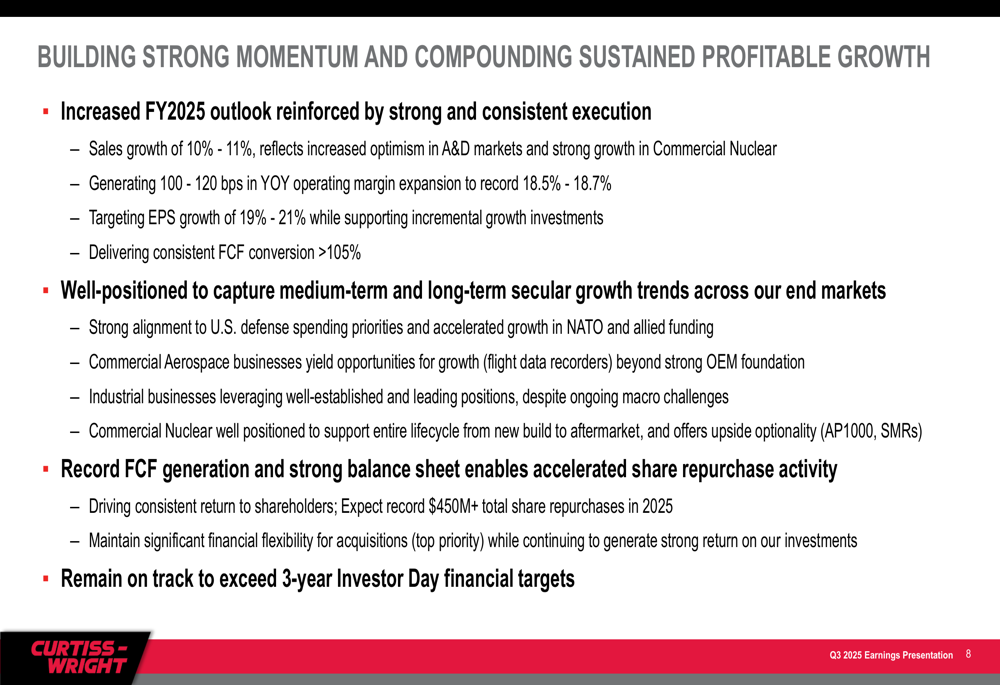

Based on the strong Q3 performance, Curtiss-Wright raised its full-year 2025 guidance across key metrics. The company now projects total sales growth of 10-11%, up from the previous guidance of 9-10%, with organic growth of 7-8%.

The updated financial guidance shows increased expectations for both sales and operating income:

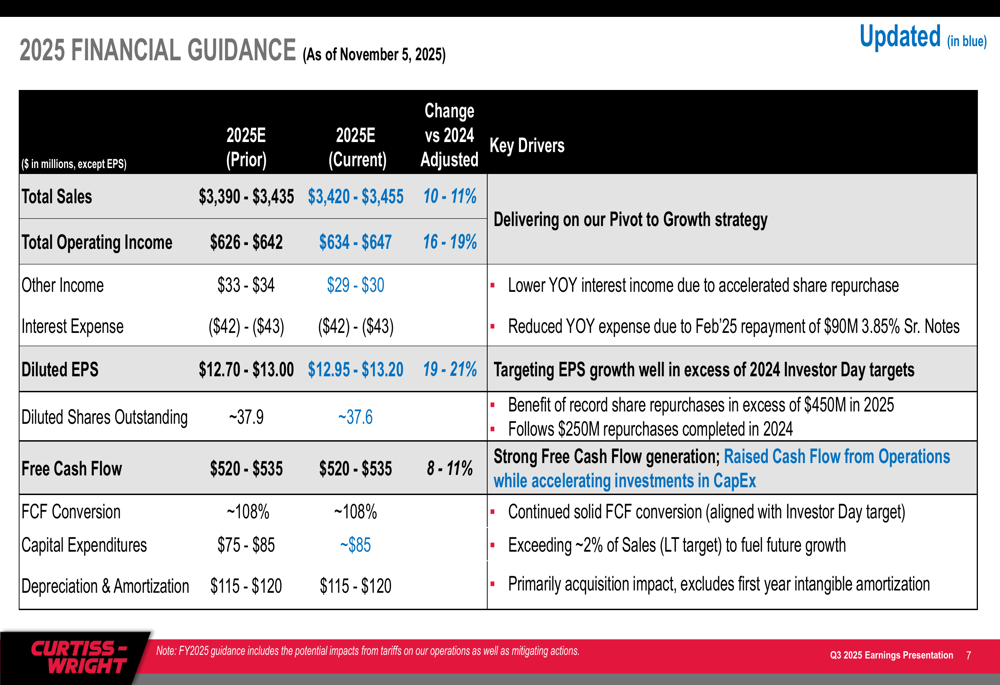

For EPS and cash flow, the company provided the following updated projections:

Curtiss-Wright expects diluted EPS to range from $12.95 to $13.20, representing 19-21% growth compared to 2024. Free cash flow is projected to be between $520 million and $535 million, with a conversion rate of approximately 108%.

The company's end market sales growth guidance has also been revised upward:

Market Reaction

Despite the strong quarterly results and raised guidance, Curtiss-Wright's stock declined by 1.56% following the earnings announcement, closing at $585.12. The stock saw a minor uptick of 0.18% in premarket trading, reaching $586.19.

This market reaction may reflect concerns about potential risks mentioned during the earnings call, including possible impacts from government shutdowns causing order delays in defense electronics, challenges in expanding content per nuclear plant, and ongoing macroeconomic pressures.

Nevertheless, Curtiss-Wright's management remains confident in the company's momentum and strategic positioning, as outlined in their forward-looking assessment:

The company's record free cash flow generation and strong balance sheet are enabling accelerated share repurchase activity, while its strategic focus on operational excellence and commercial growth opportunities positions it to exceed the three-year financial targets presented at its Investor Day. With strong alignment to defense spending priorities and established positions in industrial markets, Curtiss-Wright appears well-positioned to navigate potential challenges while continuing its growth trajectory.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.