Aspire Biopharma faces potential Nasdaq delisting after compliance shortfall

Introduction & Market Context

Customers Bancorp (NYSE:CUBI) presented its second quarter 2025 results in July, showcasing continued financial strength and strategic execution. The bank, which has positioned itself as both a traditional community bank and a digital banking innovator, reported solid performance across key metrics while continuing to transform its deposit base and expand its loan portfolio.

The Pennsylvania-based bank has maintained its momentum from previous quarters, with its stock currently trading at $64.69, representing a 3.54% increase. The company has been recognized in multiple rankings, including Forbes’ America’s Best Banks 2025, reflecting its strong market position.

Quarterly Performance Highlights

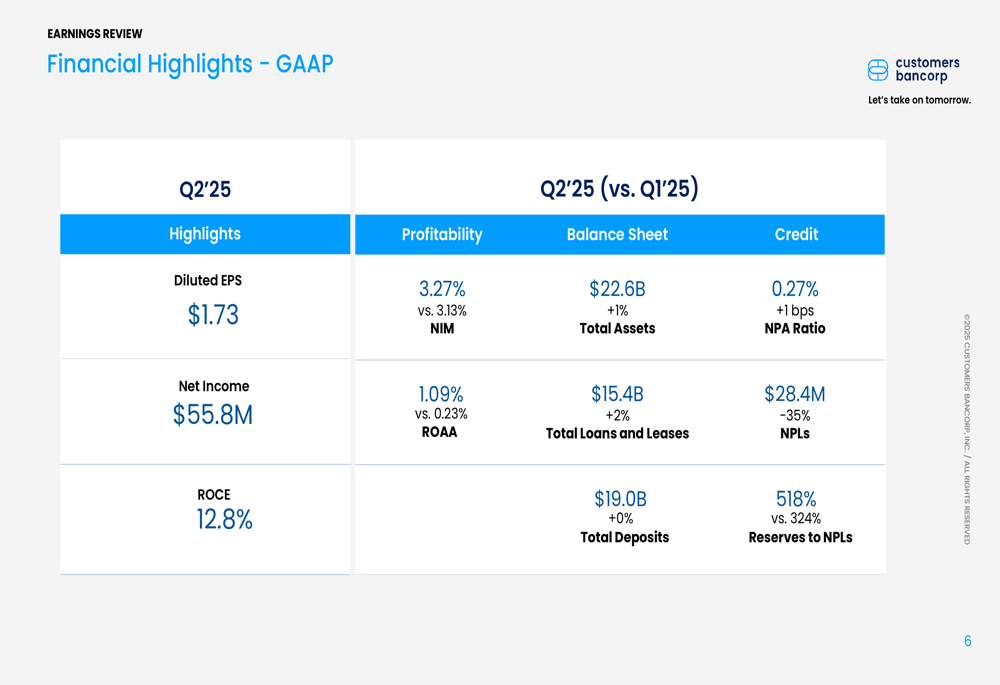

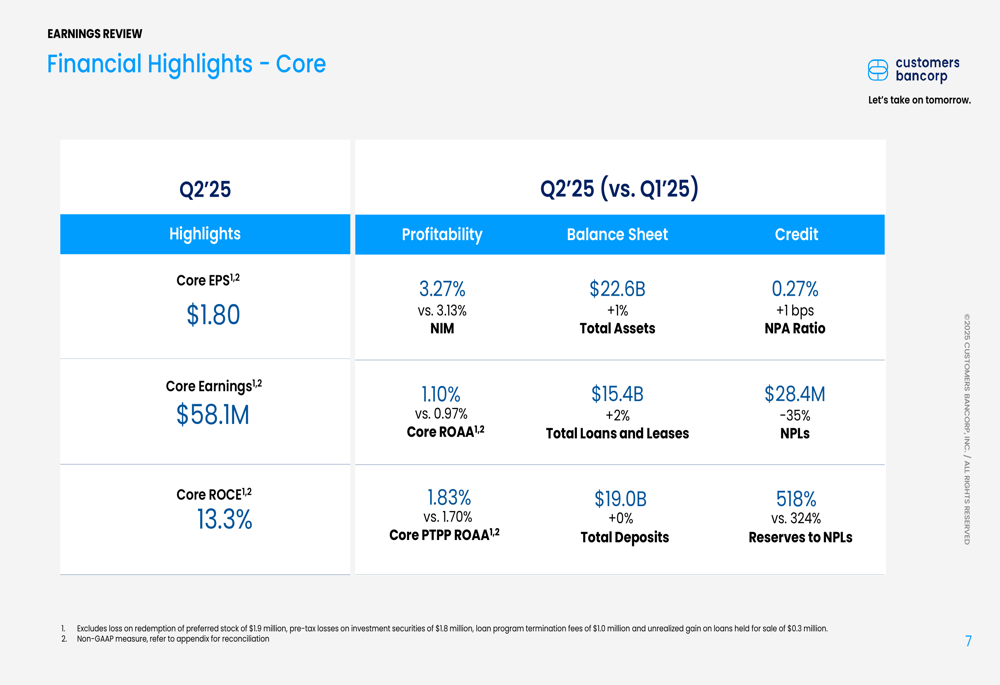

Customers Bancorp delivered robust financial results for Q2 2025, reporting core earnings per share of $1.80 and GAAP earnings per share of $1.73. The bank achieved a net interest margin (NIM) of 3.27%, representing a 14 basis point expansion quarter-over-quarter – marking the third consecutive quarter of margin improvement.

The bank’s core return on average assets (ROAA) reached 1.10%, while its efficiency ratio continued to improve, demonstrating positive operating leverage. Total assets grew to $22.6 billion, a 1% increase from the previous quarter.

As shown in the following financial highlights chart:

Core performance metrics showed consistent strength across all major categories:

Deposit Transformation Strategy

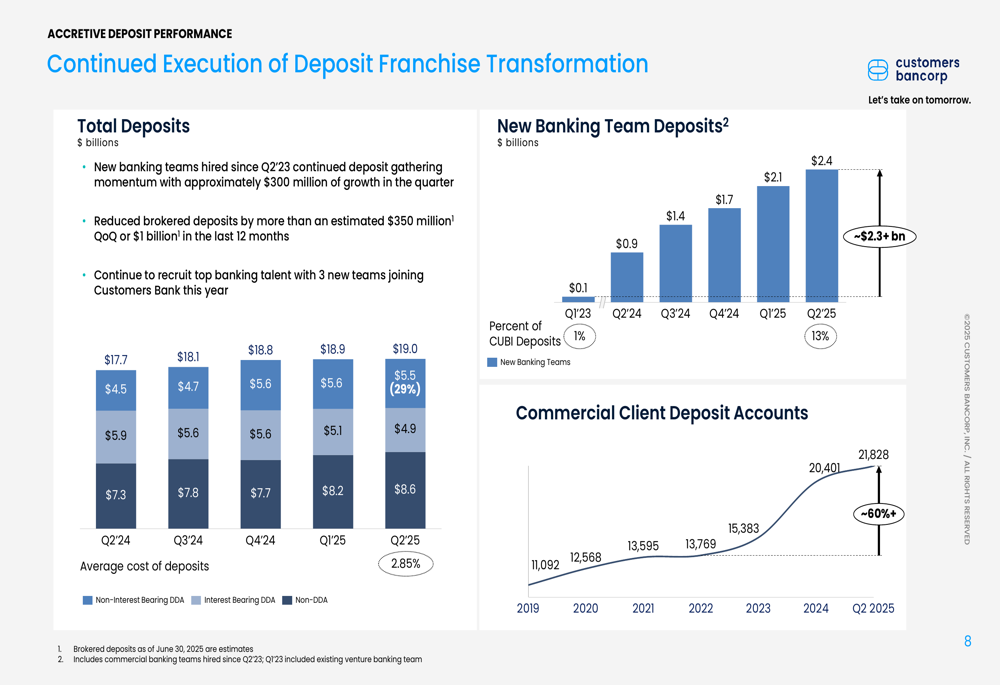

A key focus for Customers Bancorp has been transforming its deposit franchise to reduce reliance on brokered deposits while growing relationship-based funding. The bank reported approximately $300 million of deposit growth from new banking teams hired since Q2 2023, while simultaneously reducing brokered deposits by an estimated $350 million quarter-over-quarter.

This strategic shift has contributed to a favorable loan-to-deposit ratio of 81%, providing ample liquidity while improving the quality and stability of the bank’s funding base.

The following chart illustrates the bank’s deposit transformation progress:

Loan Growth and Credit Quality

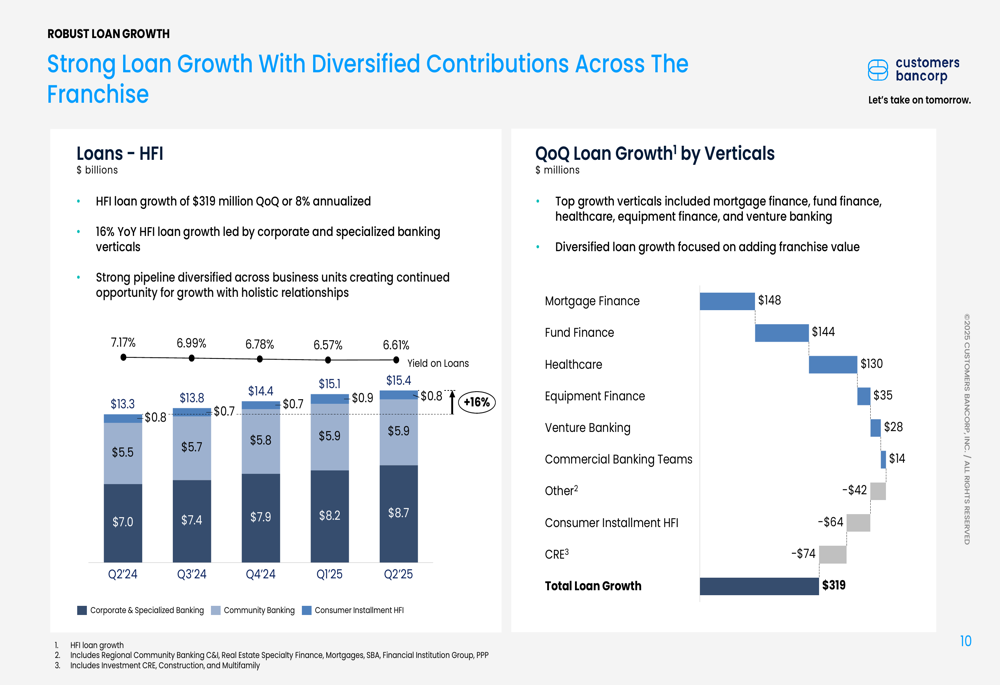

Customers Bancorp reported strong loan growth with its held-for-investment (HFI) portfolio increasing by $319 million quarter-over-quarter, representing an 8% annualized growth rate. Year-over-year, HFI loans grew by 16%, led by corporate and specialized banking verticals.

This growth was achieved while maintaining excellent credit quality. The non-performing asset (NPA) ratio remained low at 0.27%, with non-performing loans (NPLs) decreasing by 35%. The bank’s reserves to NPLs ratio stood at an impressive 518%, reflecting a conservative approach to credit risk management.

The following chart shows the diversified contributions to loan growth across different verticals:

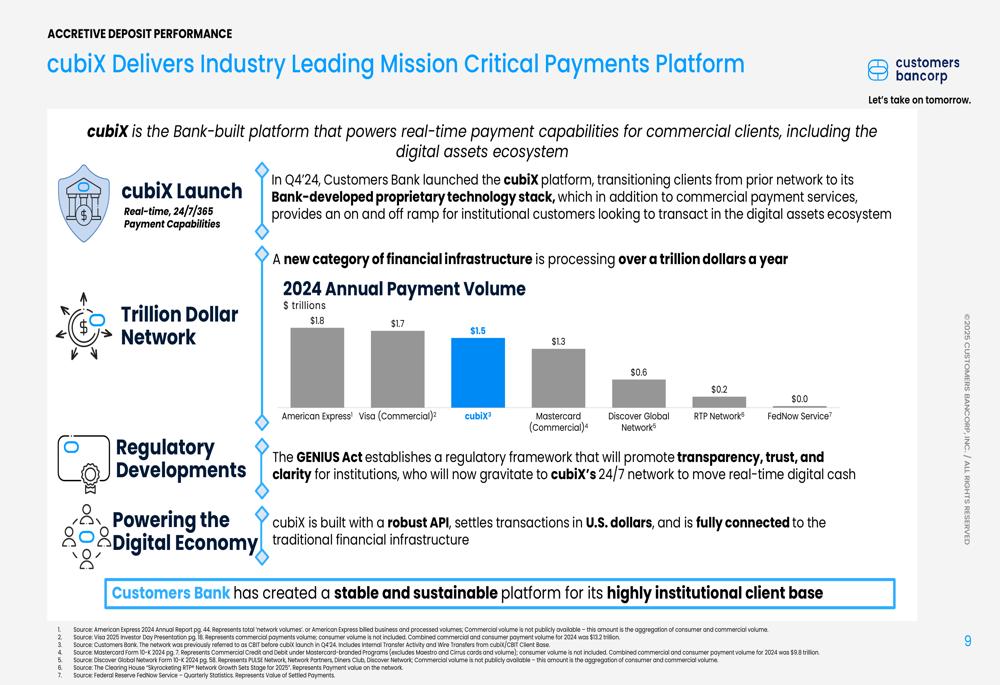

Digital Banking Innovation with cubiX

A significant differentiator for Customers Bancorp has been its cubiX payment platform, which enables payment capabilities for commercial clients, including those in the digital assets ecosystem. Launched in Q4 2024, cubiX has quickly established itself as a major player in financial infrastructure, processing over a trillion dollars annually.

The platform is fully connected to traditional financial infrastructure while serving the emerging digital economy, positioning Customers Bancorp at the intersection of conventional banking and financial innovation.

As illustrated in the following chart of annual payment volume:

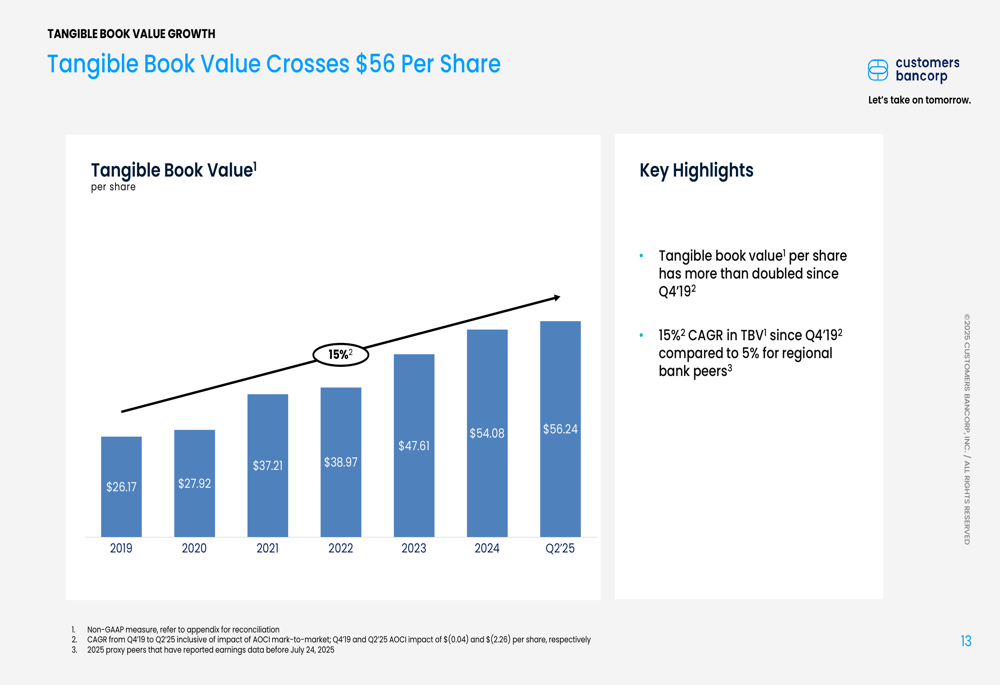

Capital Strength and Shareholder Value

Customers Bancorp has maintained strong capital levels while delivering significant shareholder value. The bank’s tangible book value per share crossed $56 in Q2 2025, representing a 15% compound annual growth rate (CAGR) since Q4 2019. This growth trajectory has effectively doubled the bank’s tangible book value over this period.

The bank’s capital position remains robust, with its Common Equity Tier 1 (CET1) ratio exceeding its target of approximately 11.5%. This strong capital position enabled the bank to fully redeem its Series E preferred shares during the quarter.

The following chart demonstrates the consistent growth in tangible book value per share:

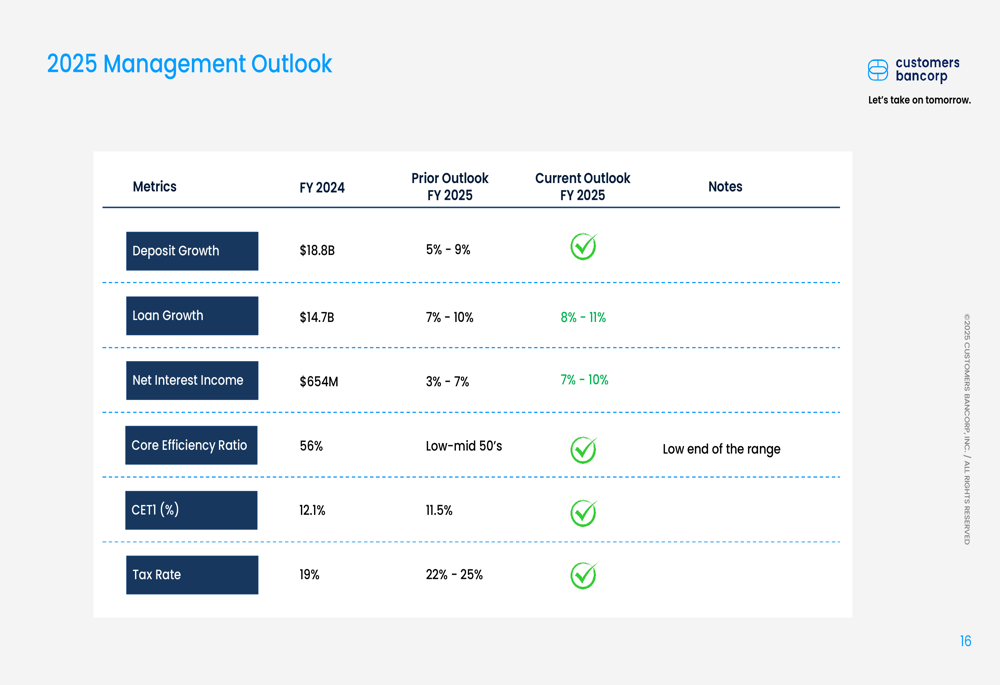

Management Outlook

Looking ahead, Customers Bancorp’s management team has maintained or improved its outlook across key performance metrics for 2025. The bank expects continued deposit growth, loan growth of 8-11% (raised from previous guidance), and net interest income growth of 7-10%.

Management also anticipates further improvement in the core efficiency ratio and maintaining a CET1 ratio above its target level of approximately 11.5%.

As shown in the management outlook summary:

Conclusion

Customers Bancorp’s Q2 2025 presentation highlights a bank that continues to execute effectively on multiple fronts – growing its traditional banking business while innovating in digital payments, improving its deposit mix while expanding its loan portfolio, and maintaining strong credit quality while delivering consistent profitability.

With its strategic focus on both community banking and specialized digital services, Customers Bancorp appears well-positioned to continue its growth trajectory through the remainder of 2025, balancing traditional banking strength with financial technology innovation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.