Lisa Cook sues Trump over firing attempt, emergency hearing set

Introduction & Market Context

Commercial Vehicle Group Inc (NASDAQ:CVGI) released its Q1 2025 earnings presentation on May 7, 2025, revealing sequential margin improvement despite ongoing revenue challenges across its key markets. The company’s stock, which has faced significant pressure over the past year, showed signs of recovery with a 16.67% jump in premarket trading to $1.05 following the results.

The presentation comes after a challenging Q4 2024, when the company reported an earnings miss with revenue of $163.3 million against expectations of $220.49 million. While Q1 2025 revenue continued to decline year-over-year, the sequential improvements in margins and cash flow suggest the company’s restructuring efforts are beginning to yield results.

Quarterly Performance Highlights

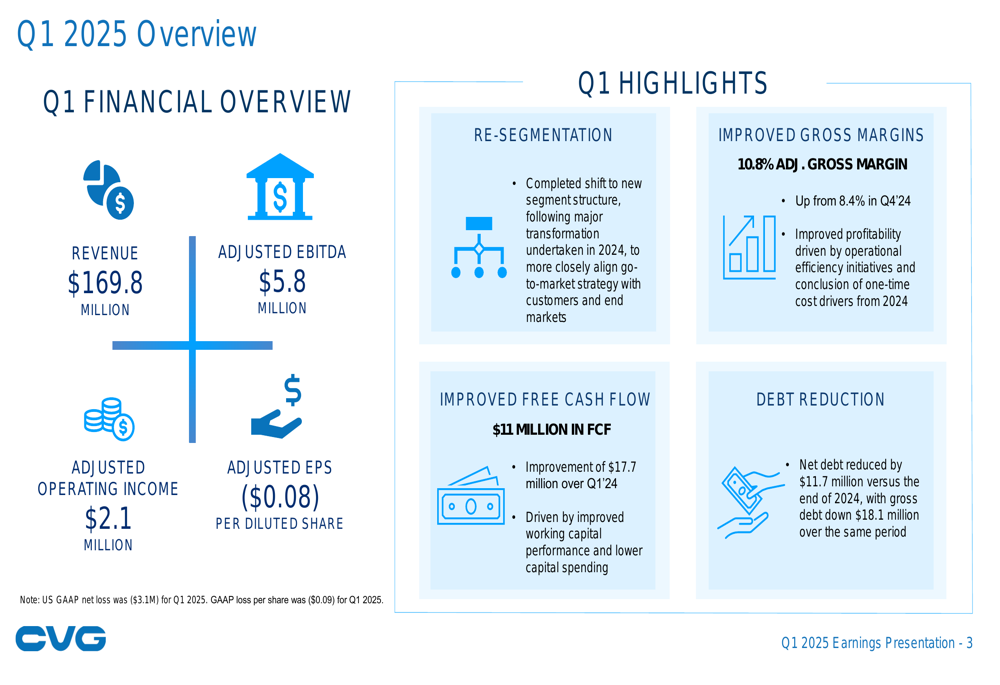

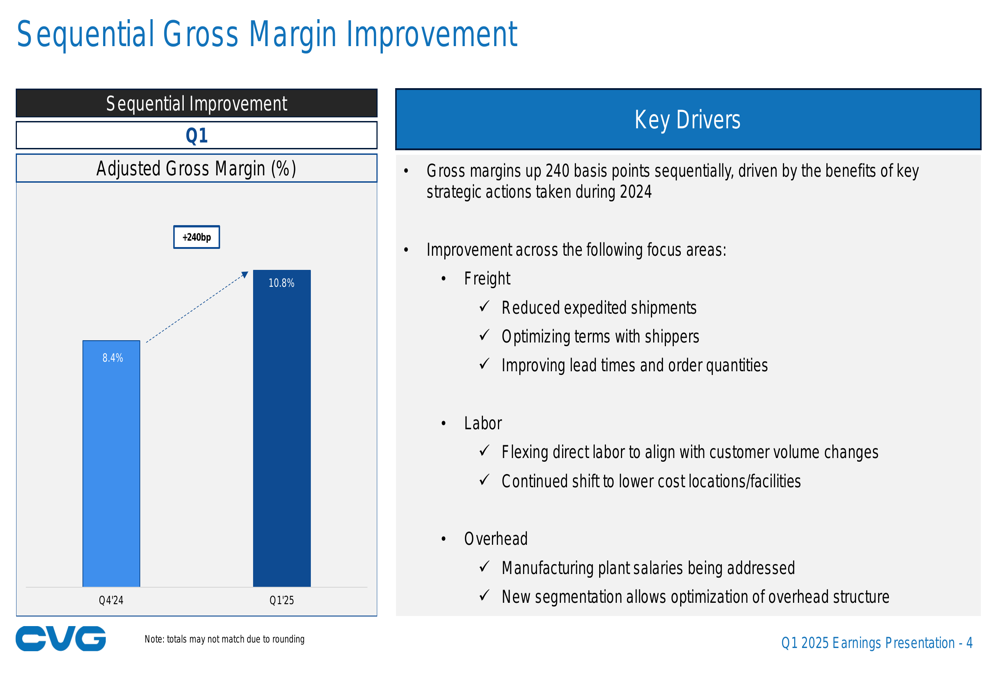

CVG reported Q1 2025 revenue of $169.8 million, down 12.7% from $194.6 million in Q1 2024, primarily due to softening demand in global Construction and Agriculture markets and North America Class 8 truck demand. Despite the revenue decline, the company achieved sequential improvement in adjusted gross margin, which increased to 10.8% from 8.4% in Q4 2024.

As shown in the following financial overview:

The company reported adjusted EBITDA of $5.8 million (3.4% margin) compared to $9.7 million (5.0% margin) in Q1 2024. Adjusted EPS was ($0.08), flat compared to Q1 2024, while GAAP EPS was ($0.09) versus $0.05 in the prior year. Notably, free cash flow improved significantly to $11.2 million, compared to ($6.5) million in Q1 2024, driven by improved working capital management and reduced capital expenditures.

The sequential gross margin improvement of 240 basis points from Q4 2024 to Q1 2025 was a key highlight, driven by strategic actions taken during 2024:

Segment Performance Analysis

CVG has completed its shift to a new segment structure to better align with customer and end-market strategy. All three segments experienced revenue declines year-over-year, reflecting broader market challenges.

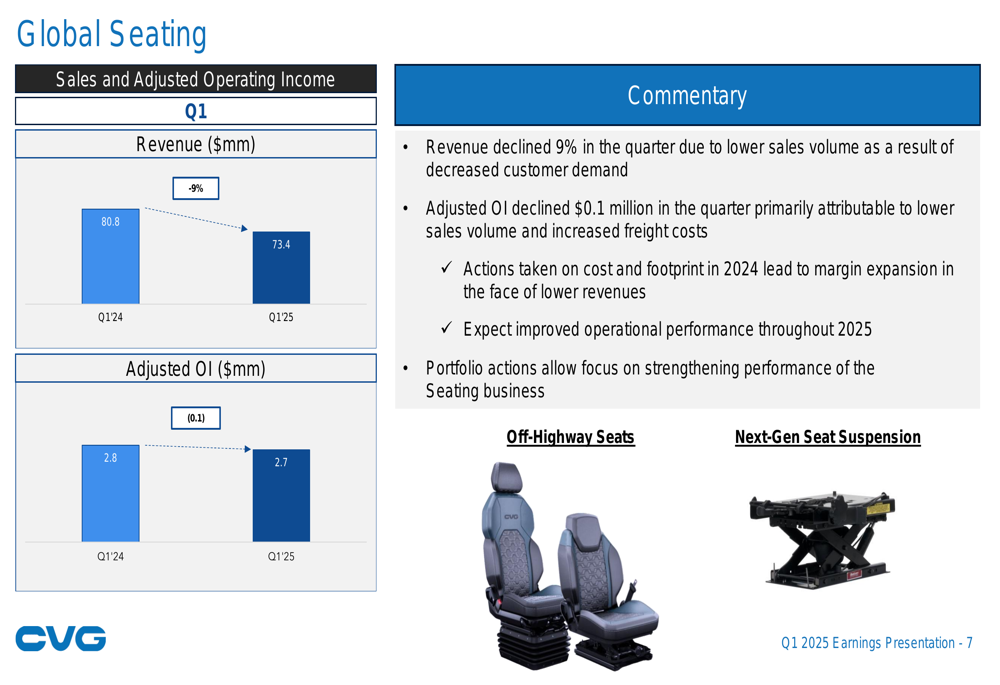

The Global Seating segment, which represents the largest portion of CVG’s business, saw revenue decline 9% to $73.4 million compared to Q1 2024. However, adjusted operating income remained relatively stable at $2.7 million, demonstrating the segment’s resilience:

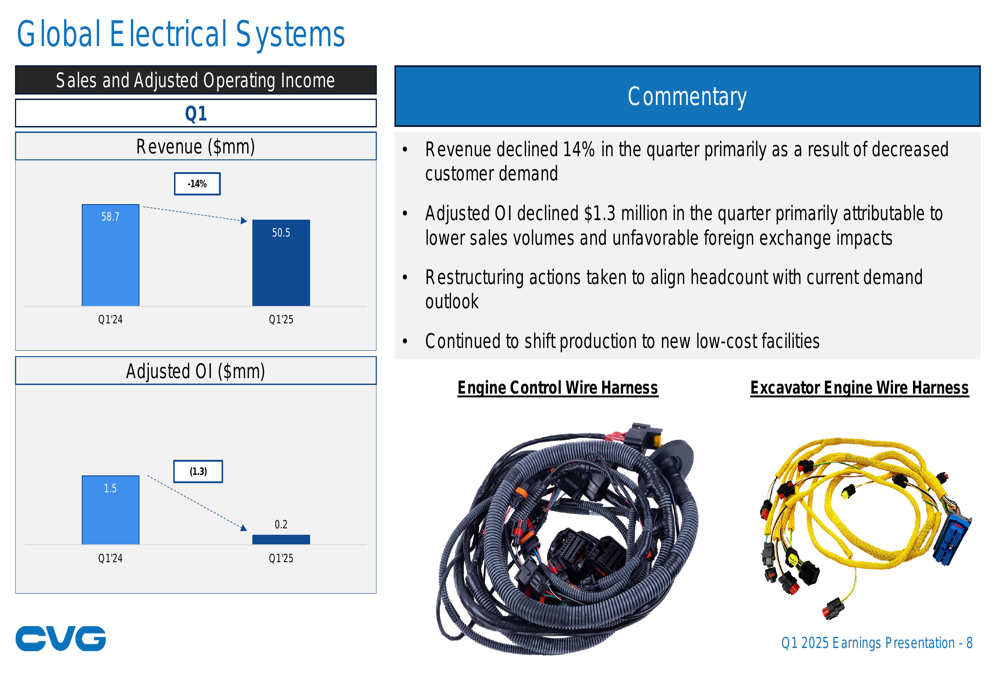

The Global Electrical Systems segment experienced a more significant revenue decline of 14% to $50.5 million, with adjusted operating income falling to $0.2 million from $1.5 million in Q1 2024:

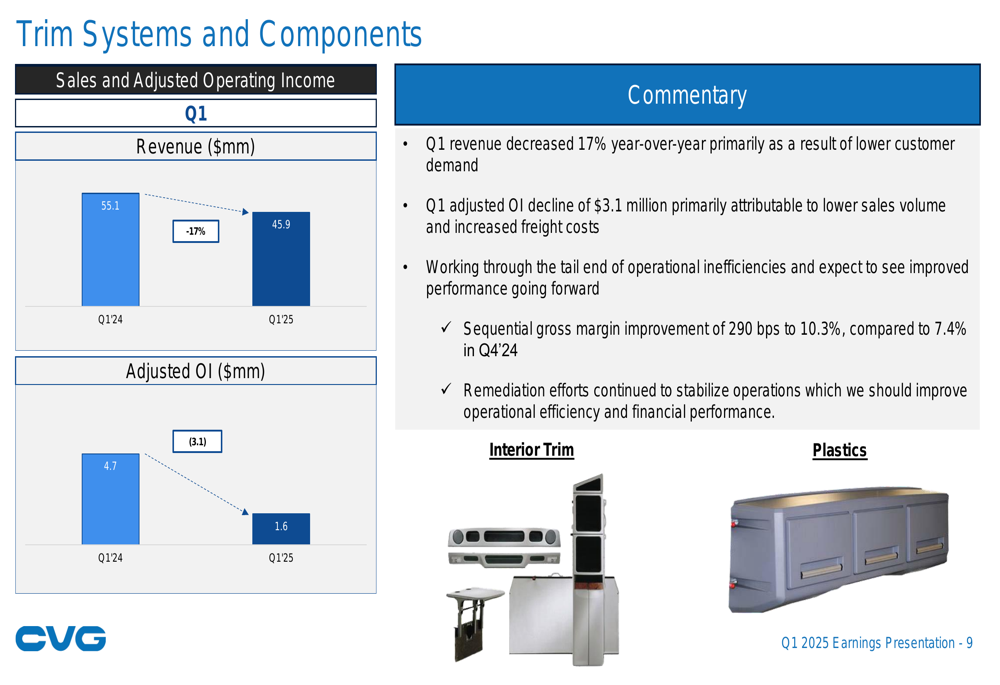

The Trim Systems and Components segment faced the steepest decline, with revenue down 17% to $45.9 million and adjusted operating income falling to $1.6 million from $4.7 million in Q1 2024:

Market Outlook and Revised Guidance

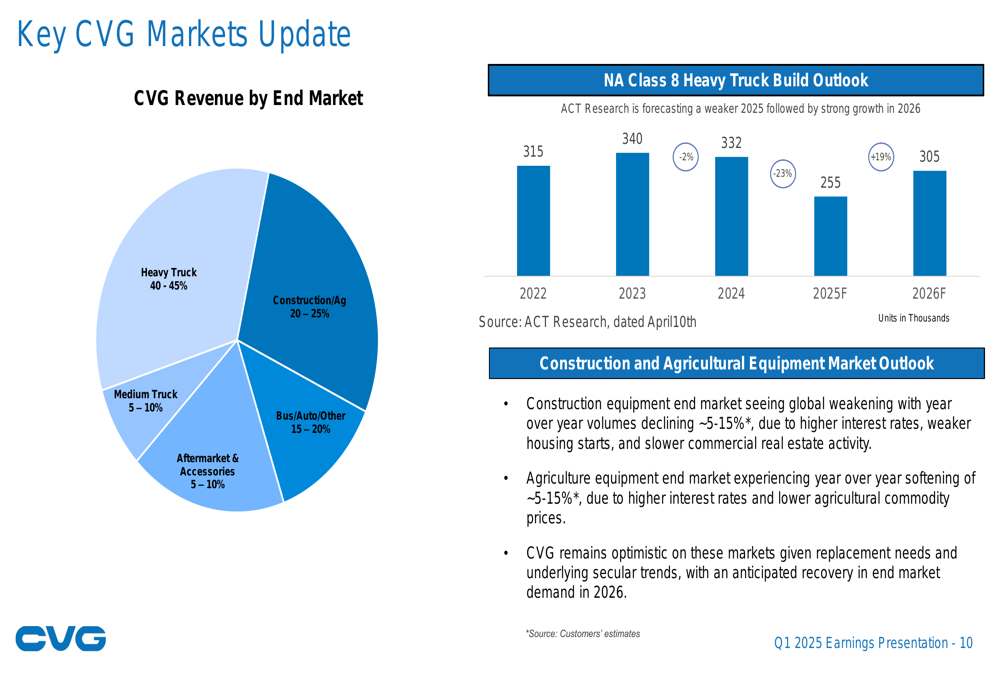

CVG’s revenue distribution across end markets shows its continued dependence on the Heavy Truck sector (40-45%), followed by Construction/Agriculture (20-25%) and Bus/Auto/Other markets (15-20%). The company faces challenging conditions across these segments, with North American Class 8 truck builds forecast to decline to 255,000 units in 2025 from 332,000 in 2024, before rebounding to 305,000 in 2026:

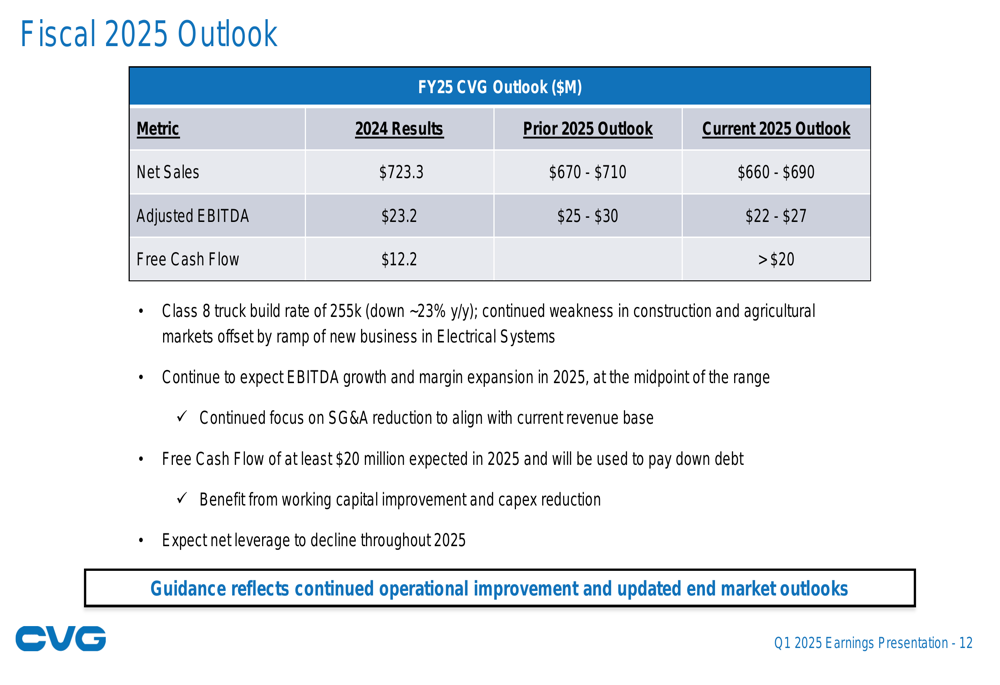

In light of these market conditions, CVG has revised its full-year 2025 guidance downward. The company now expects revenue of $660-$690 million (previously $670-$710 million) and adjusted EBITDA of $22-$27 million (previously $25-$30 million). Free cash flow is still expected to exceed $20 million:

Strategic Initiatives and Cash Flow Improvement

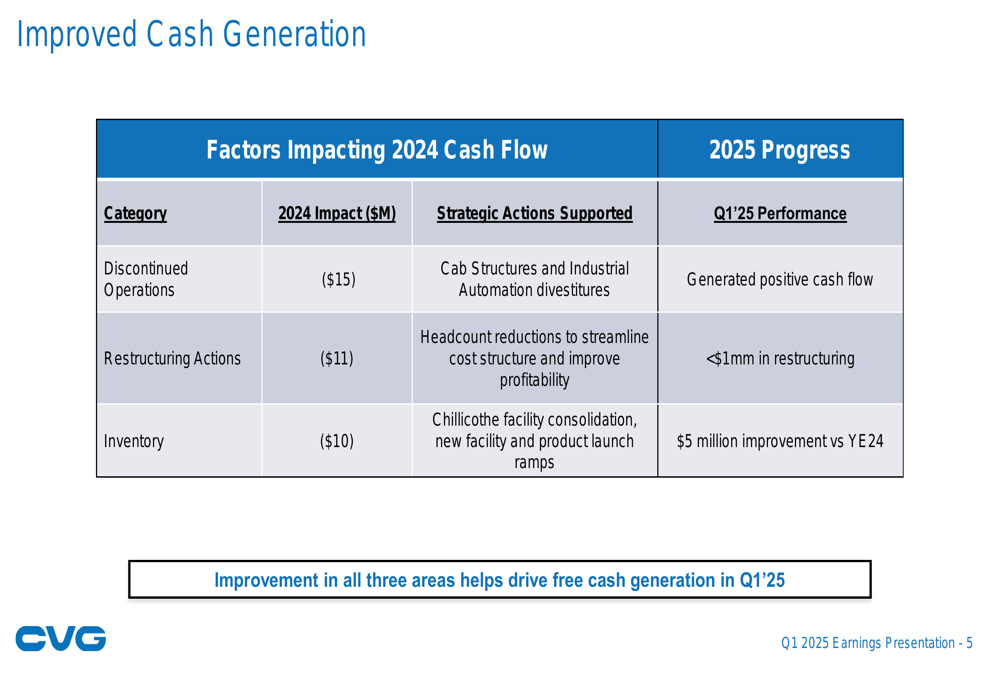

Despite market headwinds, CVG has made significant progress in improving its cash position. The company generated $11 million in free cash flow in Q1 2025, an improvement of $17.7 million over Q1 2024. This was achieved through better working capital performance and lower capital spending.

The company also reduced its net debt by $11.7 million compared to the end of 2024, with gross debt down $18.1 million over the same period. These improvements follow strategic actions taken to address factors that negatively impacted cash flow in 2024:

Looking ahead, CVG is focusing on several key initiatives to navigate the uncertain environment:

1. Capital expenditure reduction – 50% reduction in planned capex for 2025

2. Working capital reduction – targeting $20 million improvement in 2025, focused on inventory

3. SG&A reduction – continued focus to align SG&A with current revenue base

4. Evaluating reshoring and near-shoring opportunities to mitigate potential tariff impacts

Forward-Looking Statements

While CVG faces continued market challenges in 2025, management remains focused on operational improvements and cash generation. The company expects net leverage to decline throughout 2025, though it currently stands at 5.0x, indicating significant debt relative to earnings.

The improved free cash flow performance and sequential margin gains suggest that CVG’s restructuring efforts are beginning to yield results, despite the challenging revenue environment. The company’s focus on cost reduction and operational efficiency positions it to benefit from increased operating leverage when markets eventually recover.

Investors will be watching closely to see if CVG can maintain its margin improvements and cash generation while navigating the forecasted downturn in its key markets, particularly in the Heavy Truck and Construction/Agriculture sectors. The premarket stock movement suggests cautious optimism about the company’s direction, though significant challenges remain.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.