Street Calls of the Week

Introduction & Market Context

Cyber_Folks SA (WSE:CBF) presented strong Q1 2025 financial results on May 20, showcasing significant growth in revenue and adjusted EBITDA despite temporary pressure on net profit due to acquisition-related costs. The Polish technology group, which serves approximately 400,000 clients worldwide, has positioned itself as a leading tech ecosystem provider in Central and Eastern Europe.

The company’s stock closed at 162.8 PLN on the day of the presentation, down 2.33% despite the largely positive results, possibly reflecting investor concerns about the short-term impact of recent acquisitions on profitability and debt levels.

Cyber_Folks operates through three main business segments: cyber_Folks (hosting services), VERCOM (communication solutions), and Shoper (e-commerce platform), which was acquired in February 2025.

Quarterly Performance Highlights

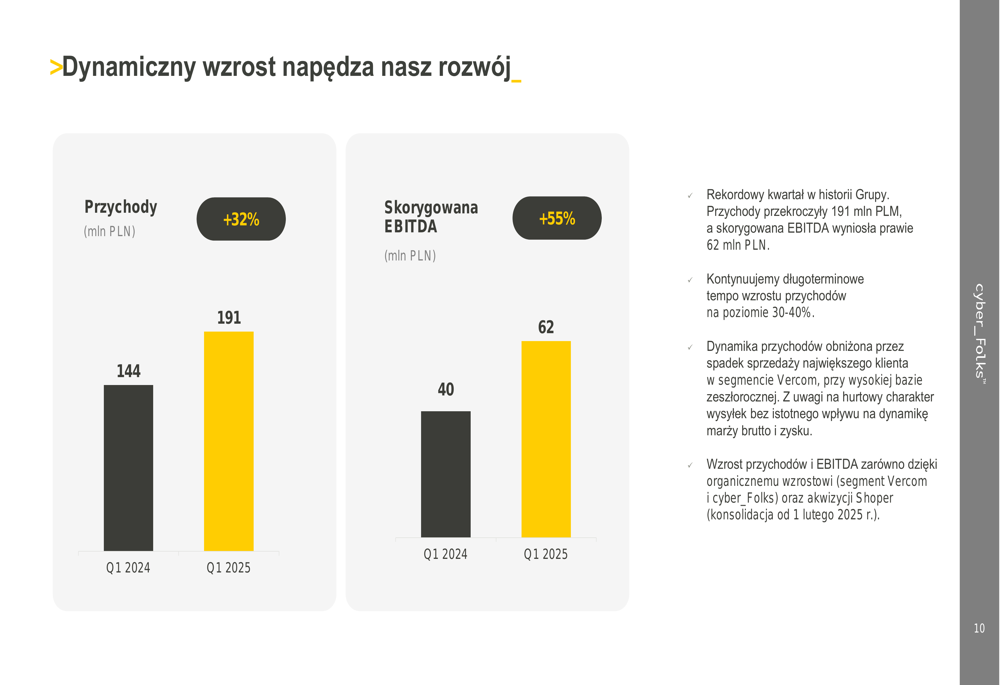

Cyber_Folks reported impressive top-line growth for Q1 2025, with revenue increasing 32% year-over-year to 190.5 million PLN, compared to 144.1 million PLN in Q1 2024. Adjusted EBITDA saw an even more substantial improvement, rising 55% to 61.8 million PLN from 39.7 million PLN in the prior-year period.

As shown in the following chart of quarterly revenue and EBITDA growth:

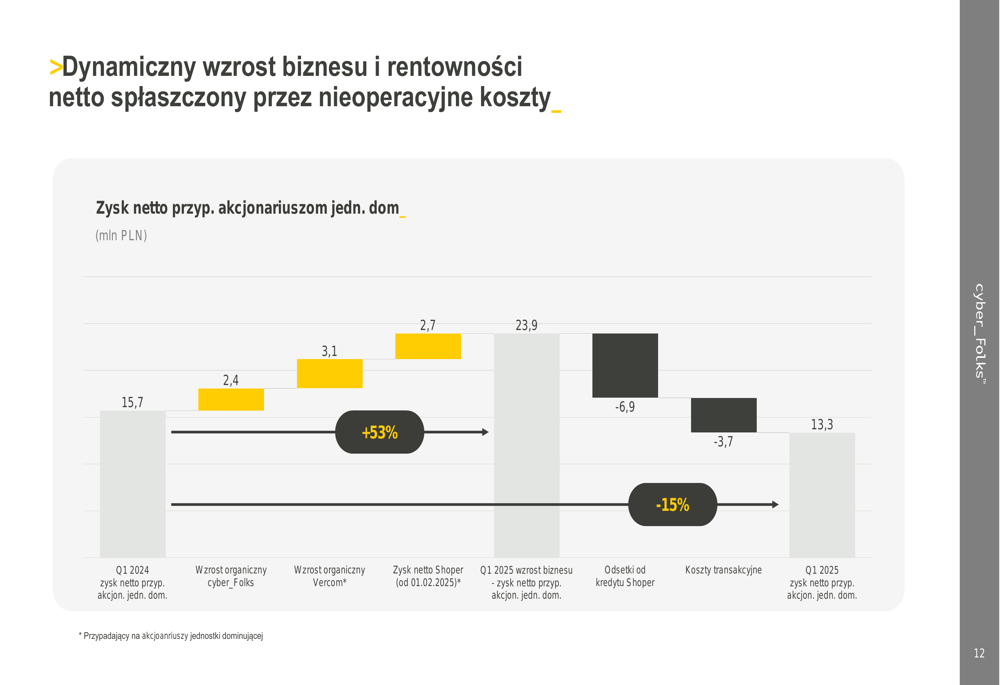

However, net profit attributable to shareholders declined 15% to 13.3 million PLN, down from 15.7 million PLN in Q1 2024. This decrease was primarily due to non-operational costs related to the Shoper acquisition, including interest fees on the acquisition loan (6.9 million PLN) and transaction fees (3.7 million PLN).

The following chart breaks down the components affecting net profit:

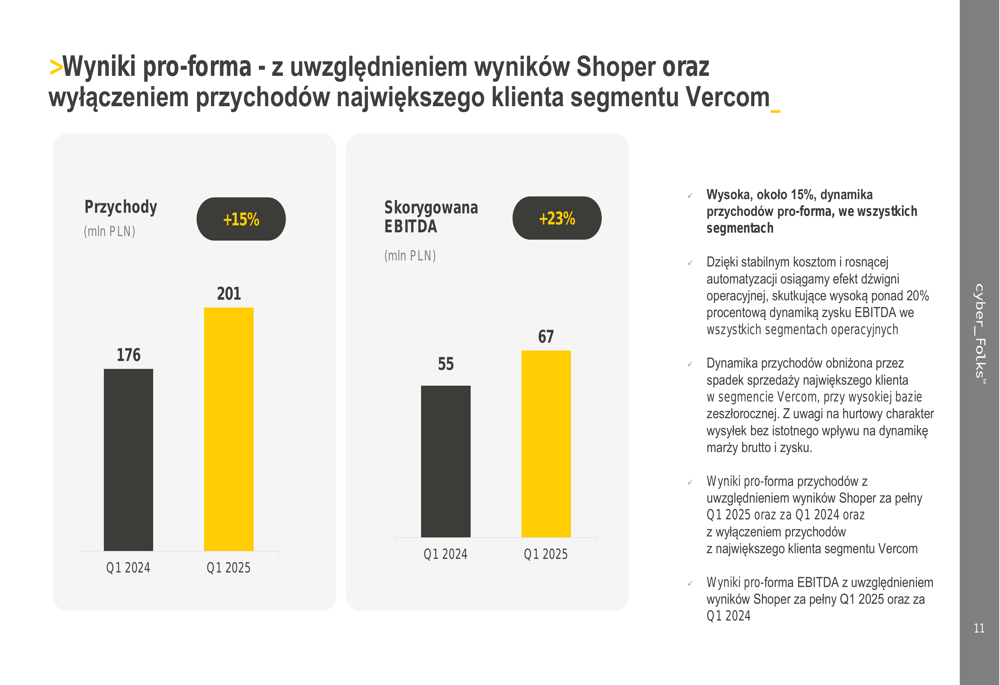

On a pro-forma basis, which provides a more comparable view by accounting for acquisitions as if they had occurred at the beginning of the reporting period, the company demonstrated solid growth with revenue up 15% to 201 million PLN and adjusted EBITDA increasing 23% to 67 million PLN.

Segment Performance Analysis

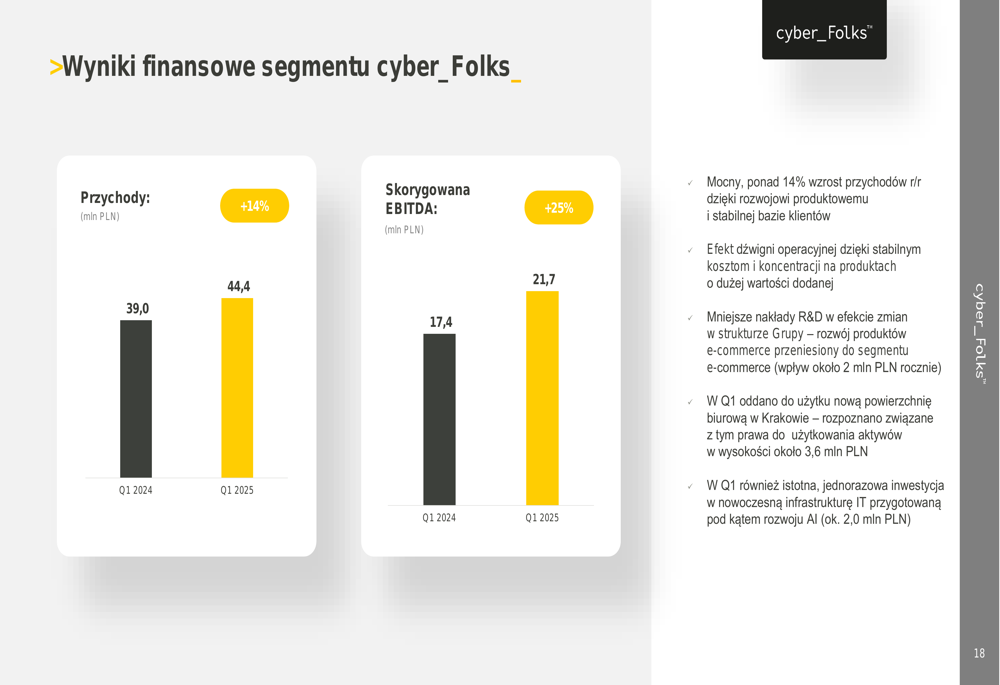

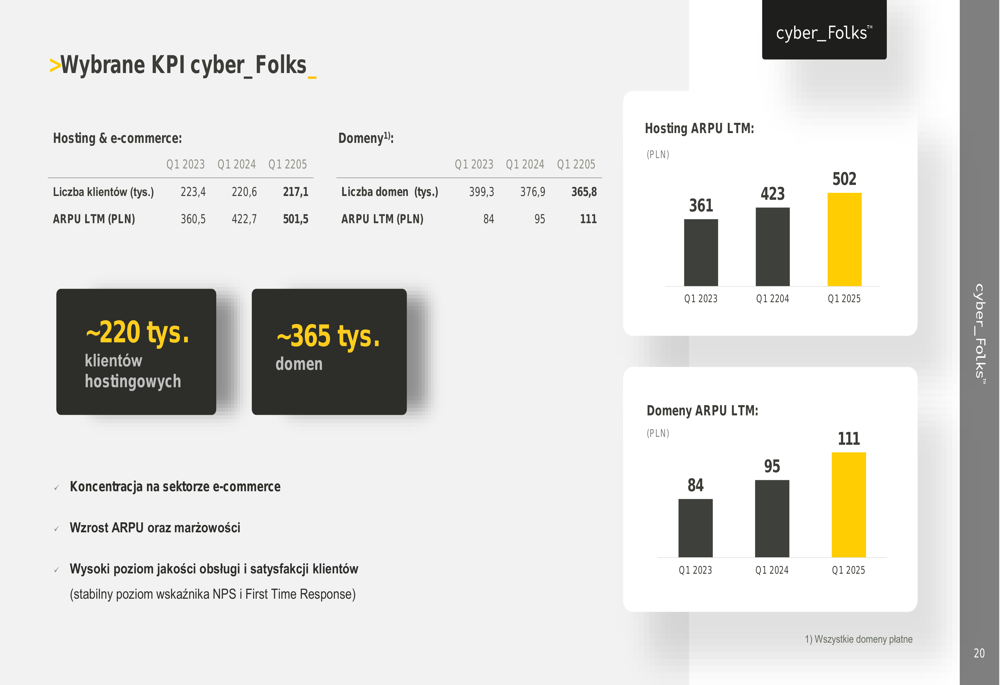

The core cyber_Folks hosting segment delivered strong results, with revenue growing 14% to 44.4 million PLN and EBITDA increasing 25% to 21.7 million PLN compared to Q1 2024. The segment’s revenue composition shows a strategic shift toward higher-margin additional services, which now account for 64.4% of segment revenue, while hosting represents 26.6% and domains 9%.

The company has successfully increased average revenue per user (ARPU) across its product lines. In the hosting and e-commerce segment, ARPU reached 501.5 PLN in Q1 2025, up from 422.7 PLN in Q1 2024 and 360.5 PLN in Q1 2023. Similarly, domain services ARPU increased to 111 PLN from 95 PLN a year earlier.

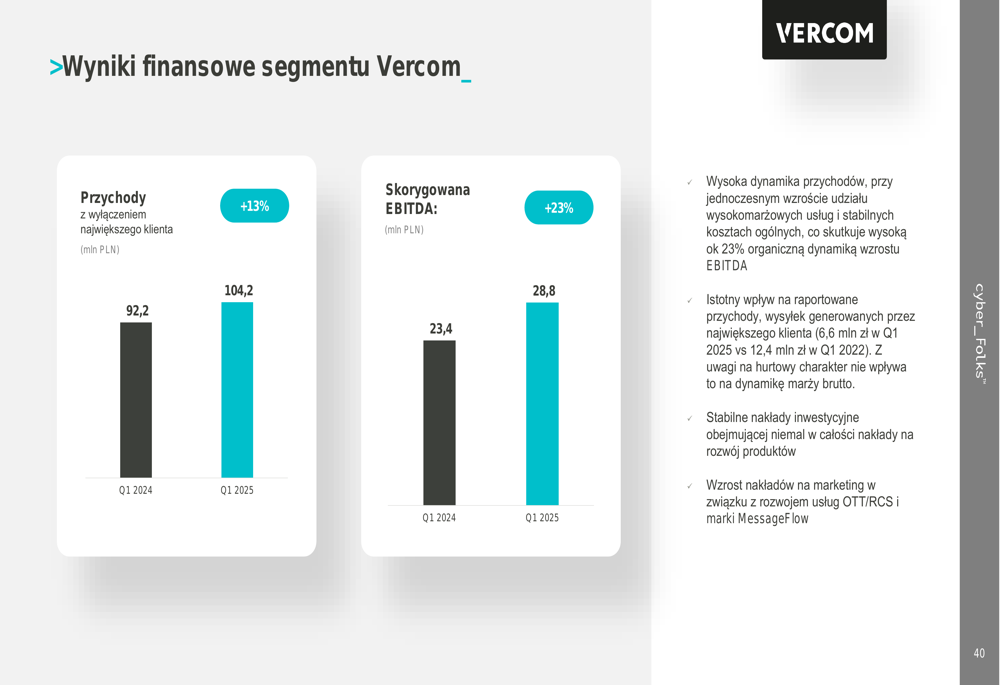

The Vercom segment, which provides communication solutions, reported 6% revenue growth to 110.8 million PLN and a more substantial 23% increase in adjusted EBITDA to 28.8 million PLN. Excluding the impact of its largest customer, Vercom’s revenue growth was more impressive at 13%.

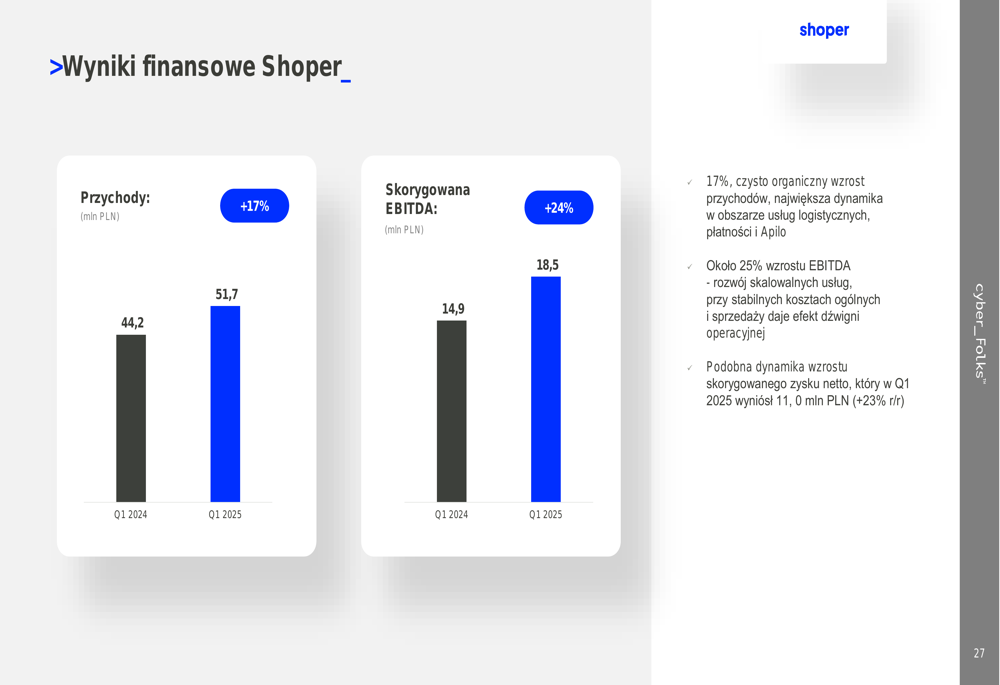

The newly acquired Shoper e-commerce platform contributed 51.7 million PLN in revenue and 18.5 million PLN in adjusted EBITDA for Q1 2025, representing year-over-year growth of 17% and 24%, respectively, when compared to its pre-acquisition performance.

Strategic Initiatives & Acquisitions

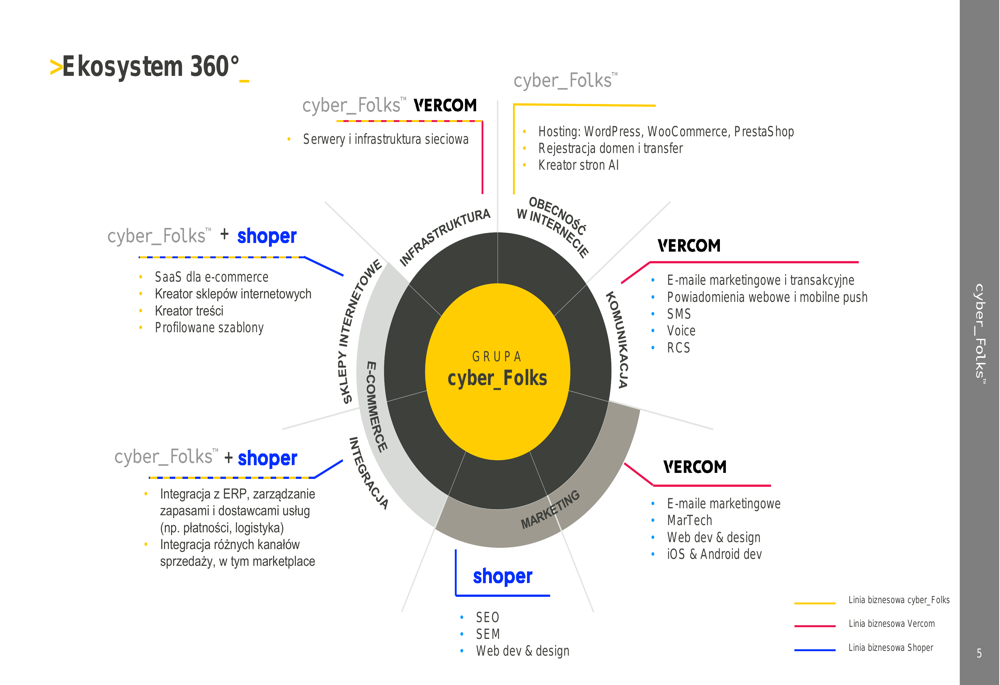

Cyber_Folks has outlined an ambitious 2025 agenda focused on balanced growth across all business segments, with the goal of becoming the technological e-commerce leader in Central and Eastern Europe. The company’s "Ecosystem 360" strategy integrates its various services to provide comprehensive solutions for businesses of all sizes.

The following illustration depicts the company’s integrated ecosystem approach:

The acquisition of Shoper in February 2025 represents a significant strategic move to strengthen the company’s e-commerce capabilities. While this acquisition has temporarily impacted net profit and increased debt levels, management views it as a crucial step in building a comprehensive technology ecosystem.

The company is also investing in modern infrastructure and AI implementation to enhance its competitive position. Its AI assistant, robo_Folks, is now in production, helping customers navigate the company’s services more effectively.

Financial Position & Shareholder Returns

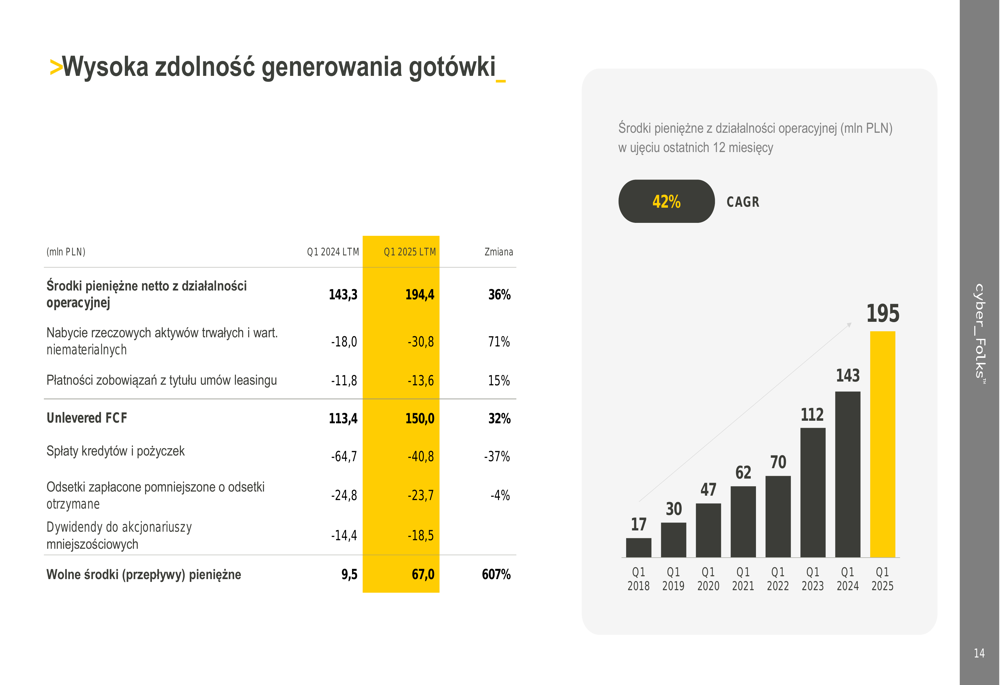

Cyber_Folks continues to demonstrate strong cash-generating capabilities, with net cash from operations for the last twelve months ending Q1 2025 reaching 194.4 million PLN, a 36% increase from 143.3 million PLN in the comparable prior period.

The following chart illustrates the company’s consistent cash generation trend:

The company’s net debt to adjusted EBITDA ratio increased to 2.1x in Q1 2025 from 0.5x in 2024, primarily due to the Shoper acquisition. Despite this increase, management considers the current debt level comfortable and well within manageable limits, especially given the company’s strong cash flow generation.

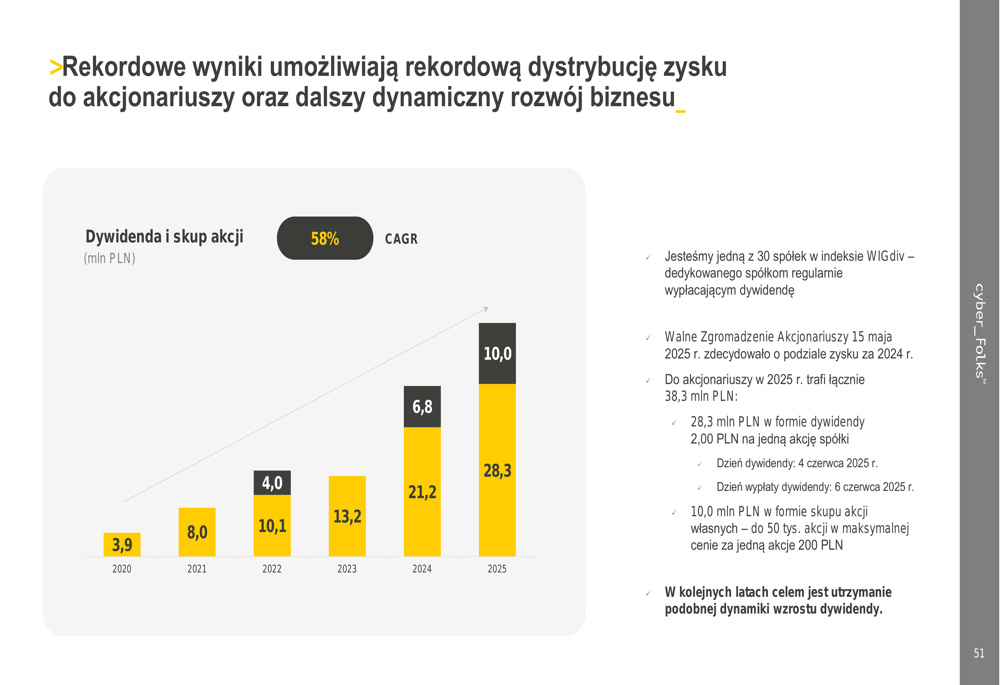

Cyber_Folks has maintained a consistent track record of increasing dividend payments, with projected dividends for 2025 reaching 28.3 million PLN, more than seven times the 3.9 million PLN paid in 2020. The company also plans to allocate 10 million PLN for stock buybacks in 2025.

In conclusion, Cyber_Folks’ Q1 2025 results demonstrate robust operational performance across all segments, with temporary pressure on net profit due to acquisition-related costs. The company’s strategic investments in expanding its ecosystem, particularly through the Shoper acquisition, position it for continued growth while maintaining its commitment to increasing shareholder returns through dividends and share repurchases.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.