Oklo stock tumbles as Financial Times scrutinizes valuation

Introduction & Market Context

Danaher Corporation (NYSE:DHR) released its third quarter 2025 earnings presentation on October 21, revealing stronger-than-expected performance that sent shares surging 9.42% to $228.03 by market close. The life sciences and diagnostics giant reported solid revenue growth and significant earnings per share improvement, comfortably exceeding analyst expectations in a challenging macroeconomic environment.

The company’s results demonstrated resilience across its diversified portfolio, with particularly strong performance in its Biotechnology and Diagnostics segments offsetting challenges in Life Sciences. Investors responded positively to both the current results and the company’s forward guidance.

Quarterly Performance Highlights

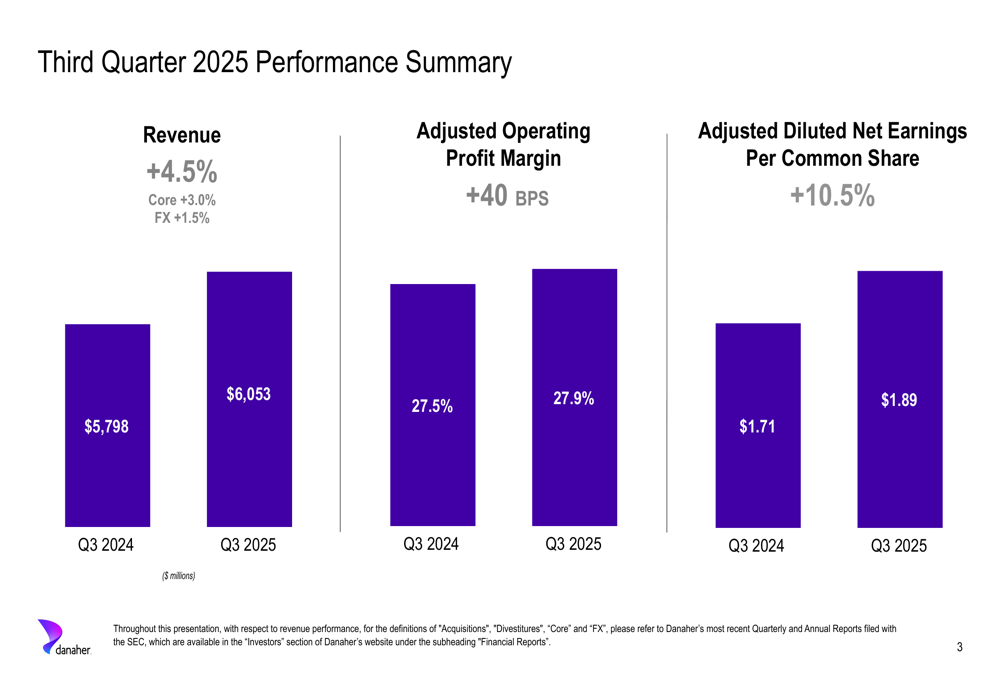

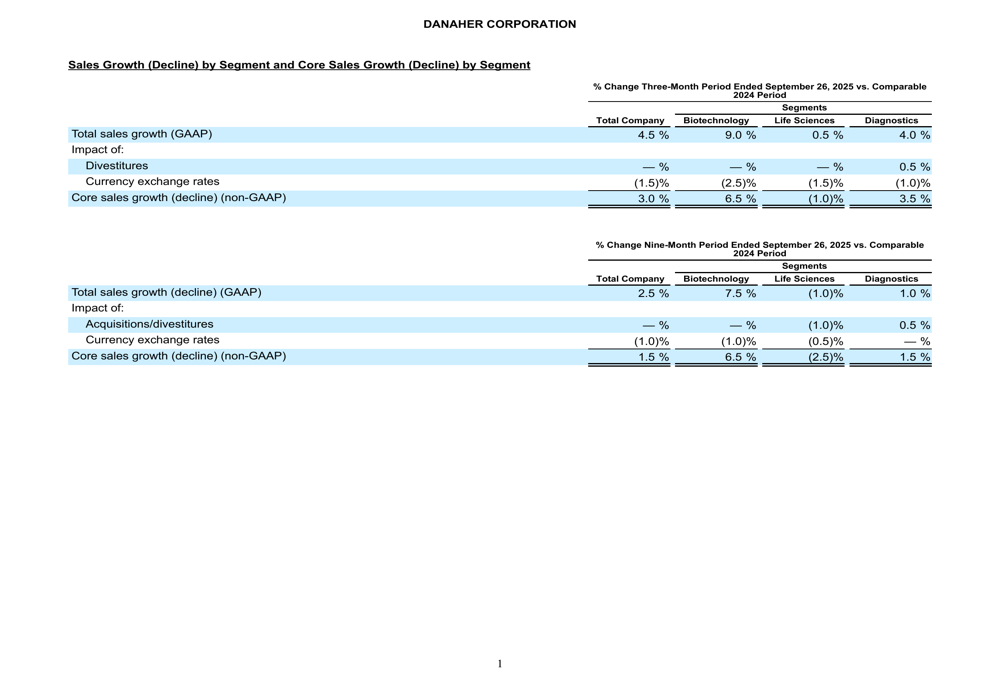

Danaher reported Q3 2025 revenue of $6.05 billion, representing a 4.5% increase compared to the same period in 2024. This growth comprised 3.0% core growth and a 1.5% positive impact from foreign exchange. Adjusted diluted earnings per share reached $1.89, a 10.5% increase from $1.71 in the prior year period, significantly exceeding analyst expectations of $1.72.

As shown in the following chart of quarterly performance:

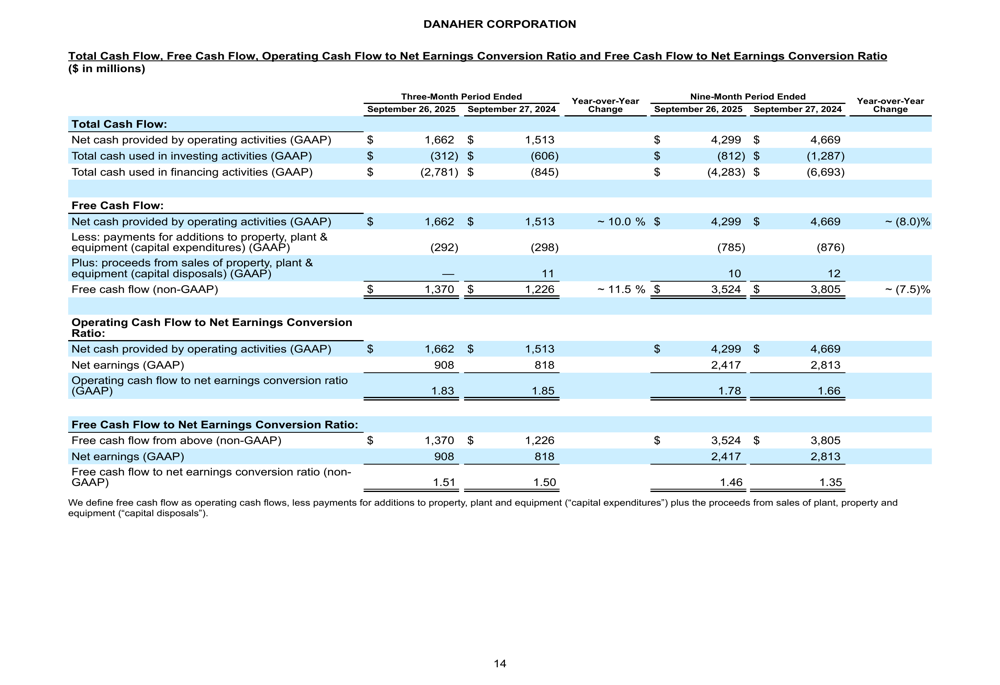

The company’s adjusted operating profit margin improved by 40 basis points year-over-year, reflecting Danaher’s continued focus on operational efficiency and cost management. Free cash flow generation was robust at $1.37 billion for the quarter, up from $1.23 billion in Q3 2024, demonstrating the company’s strong cash conversion capabilities.

Detailed Segment Analysis

Danaher’s performance varied across its three main business segments, with Biotechnology emerging as the clear standout performer.

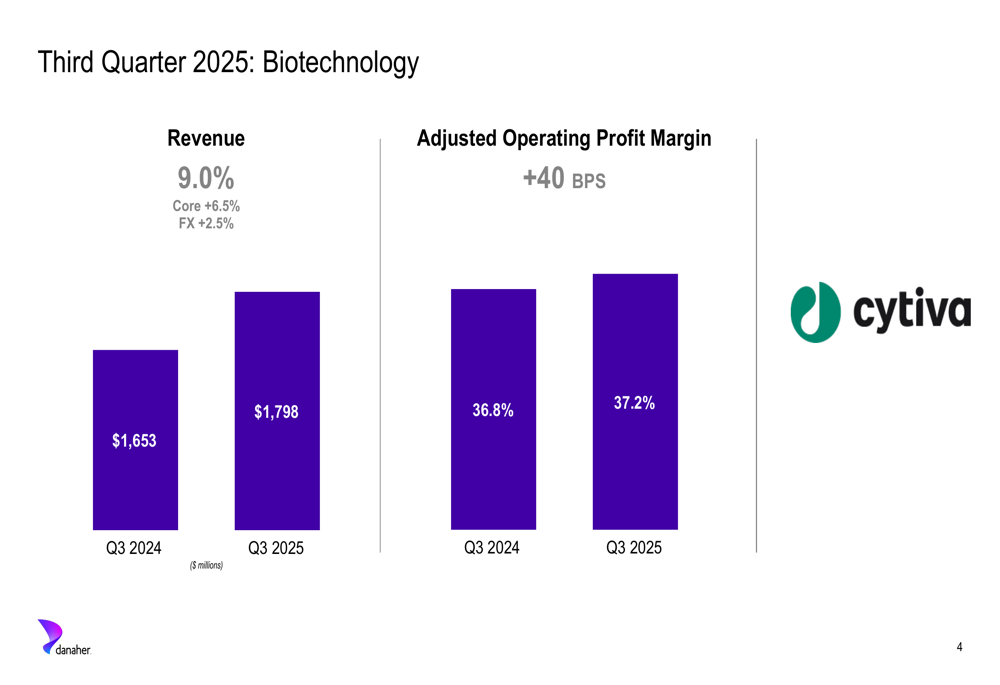

The Biotechnology segment, which includes the Cytiva brand, delivered impressive 9.0% revenue growth (6.5% core growth plus 2.5% from favorable foreign exchange), reaching $1.8 billion for the quarter. The segment’s adjusted operating profit margin increased by 40 basis points to 37.2%, maintaining its position as Danaher’s highest-margin business.

As illustrated in the Biotechnology segment performance:

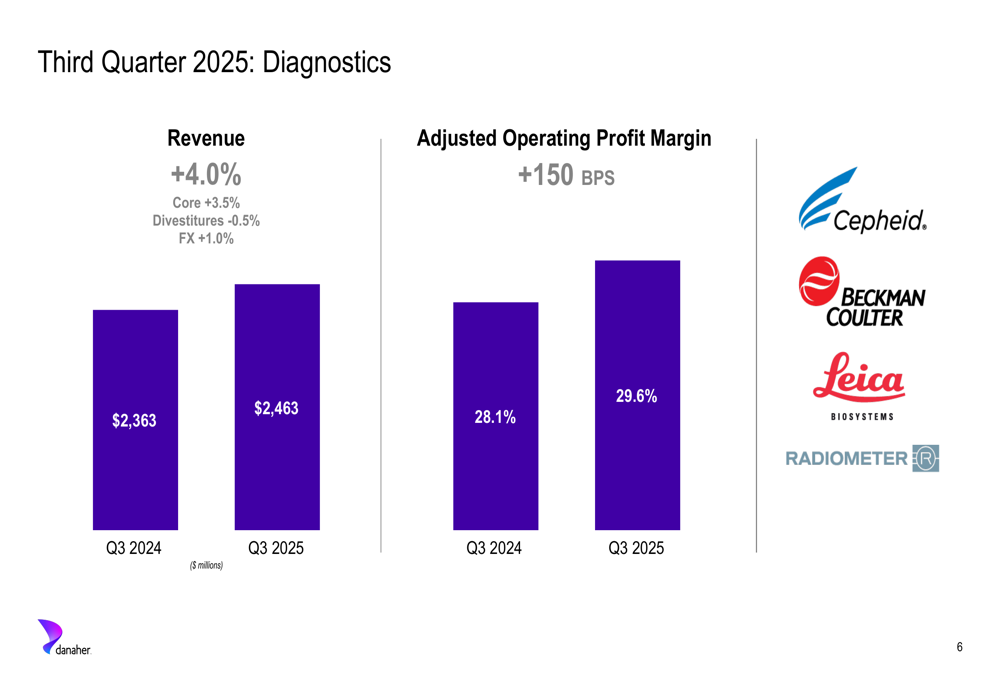

The Diagnostics segment also performed well, with revenue increasing 4.0% to $2.46 billion. This growth comprised 3.5% core growth and 1.0% from favorable foreign exchange, partially offset by a 0.5% negative impact from divestitures. The segment’s adjusted operating profit margin showed significant improvement, increasing 150 basis points to 29.6%.

The Diagnostics segment results demonstrate the continued strength of Danaher’s clinical diagnostic platforms:

In contrast, the Life Sciences segment faced challenges, with revenue increasing only 0.5% to $1.79 billion. This modest growth resulted from a 1.0% core revenue decline, offset by a 1.5% positive impact from foreign exchange. The segment’s adjusted operating profit margin declined by 170 basis points to 21.0%, reflecting ongoing competitive pressures and investment requirements.

The segment breakdown provides a comprehensive view of Danaher’s diversified business performance:

Financial Outlook & Guidance

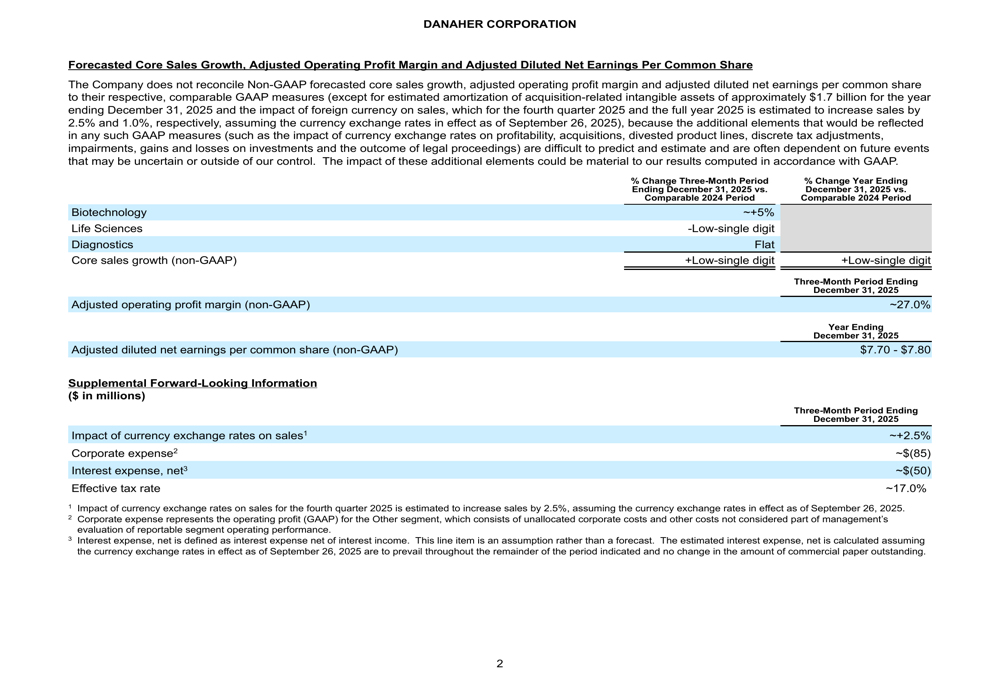

Looking ahead, Danaher provided a positive outlook for the remainder of 2025 and into 2026. The company forecasts continued strength in its Biotechnology segment with approximately 5% core sales growth expected. The Life Sciences segment is projected to deliver low-single-digit growth, while the Diagnostics segment is expected to remain flat.

Danaher anticipates an adjusted operating profit margin of approximately 27.0% and has narrowed its full-year 2025 adjusted diluted earnings per share guidance to $7.70-$7.80. The company also expects a positive currency exchange impact of approximately 2.5% on sales.

The detailed financial guidance illustrates Danaher’s expectations across segments:

Management highlighted ongoing cost-saving initiatives projected to yield $250 million by 2026, supporting margin expansion goals. The company also emphasized its strong cash position, which provides flexibility for strategic acquisitions and shareholder returns.

Market Reaction & Analyst Perspectives

Danaher’s stock performance reflected strong investor confidence in the quarterly results, with shares rising 9.42% on the day of the announcement. The stock had already gained 5.6% in premarket trading, indicating positive anticipation ahead of the official release.

The company’s free cash flow generation remains a key strength, providing financial flexibility for future growth initiatives:

Analysts maintain a strong buy consensus on the stock, with price targets ranging from $205 to $310, suggesting potential upside from current levels. Market observers particularly noted the strength in the Biotechnology segment and the overall margin improvement as positive indicators for Danaher’s long-term growth trajectory.

CEO Rainer Blair expressed satisfaction with the company’s performance, stating, "We’re encouraged to deliver third quarter results ahead of expectation in what remains a dynamic operating environment." Blair also highlighted the healthy outlook for the biologics market and the company’s active M&A strategy.

While Danaher faces some challenges, particularly in the Life Sciences segment and potential regulatory changes in key markets like China, the company’s diversified portfolio and strong financial position appear to provide resilience against market volatility. The continued focus on innovation, operational efficiency, and strategic acquisitions positions Danaher well for sustainable growth in the life sciences and diagnostics sectors.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.