NVIDIA launches Jetson Thor robotics computers for physical AI systems

Industrie De Nora SpA (BIT:DNR) presented its H1 2025 financial results on July 31, 2025, reporting revenue growth of 3.8% year-over-year and an upgraded profitability outlook. The electrochemical technology company’s stock closed down 4.49% at €6.91 following the presentation.

H1 2025 Financial Performance Highlights

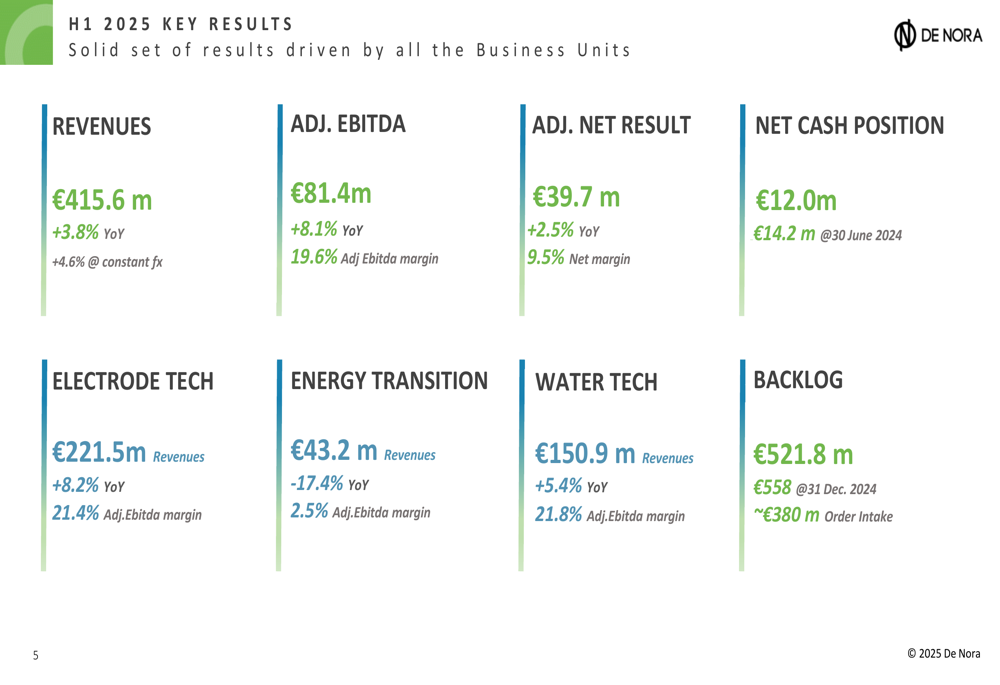

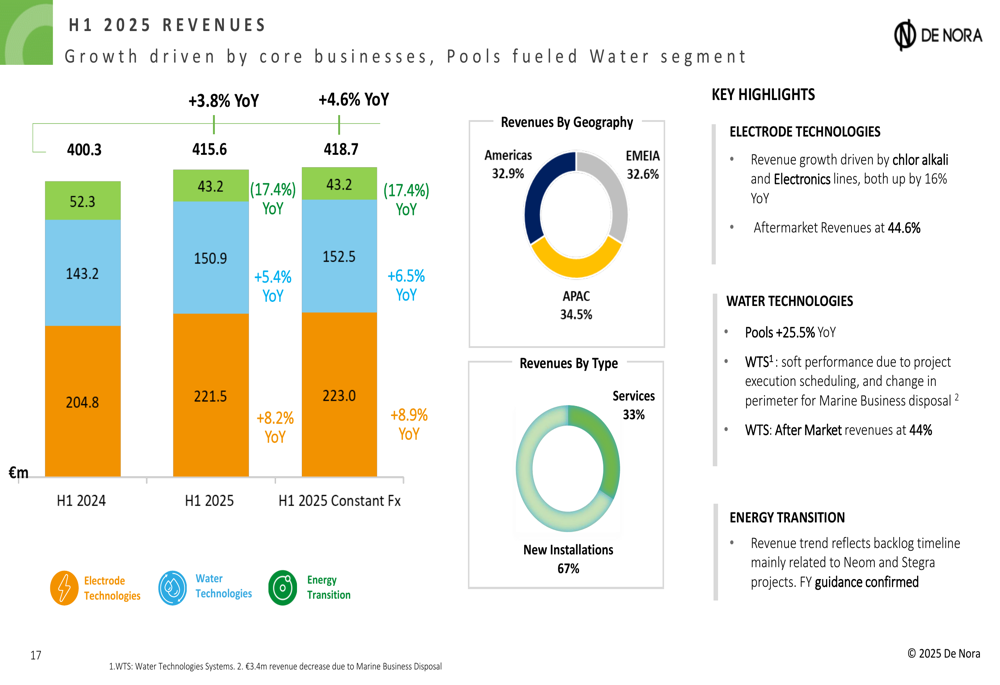

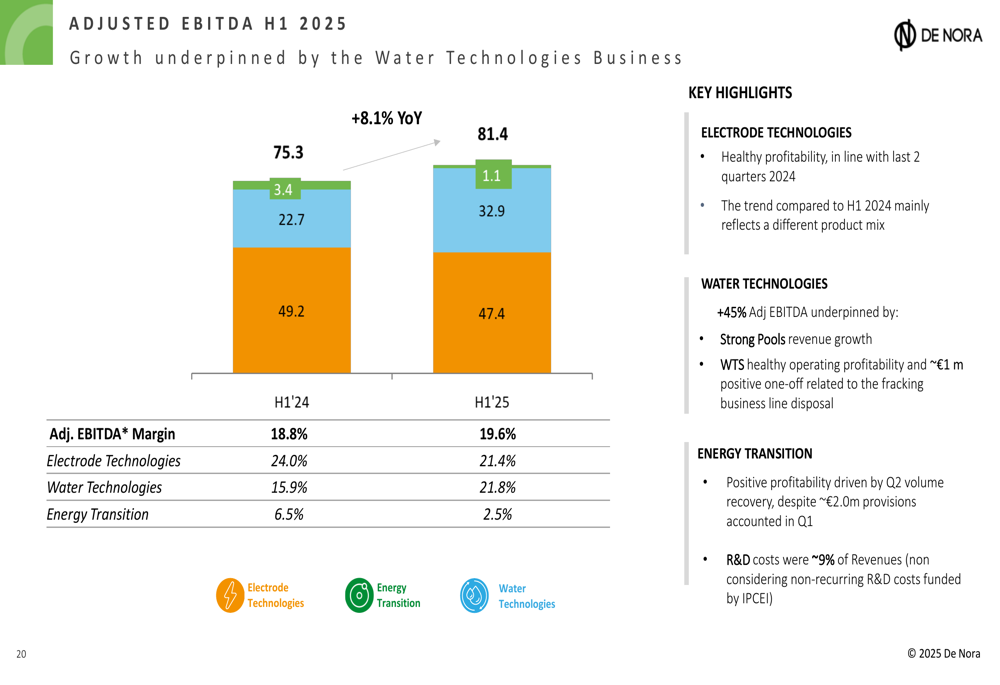

De Nora reported revenue of €415.6 million for the first half of 2025, representing a 3.8% increase compared to H1 2024 (4.6% at constant exchange rates). Adjusted EBITDA grew by 8.1% to €81.4 million, with the margin expanding to 19.6% from 18.8% in the same period last year.

As shown in the following key results summary:

The company maintained a positive net cash position of €12.0 million as of June 30, 2025, slightly down from €14.2 million a year earlier. Adjusted net profit increased by 2.5% year-over-year to €39.7 million, representing a 9.5% net margin.

CEO Paolo Dellachà commented during the presentation: "Solid results drive the upgrade in the 2025 profitability guidance, despite a challenging macroeconomic scenario. Core Business is growing and profitable, confirming the positive short and mid-term view."

Segment Performance Analysis

De Nora’s performance was driven primarily by its core businesses, with the Water Technologies segment showing particularly strong profitability improvement.

The revenue breakdown by segment shows:

The Electrode Technologies segment, which accounts for the largest portion of revenue, grew by 8.2% year-over-year to €221.5 million in H1 2025. This segment maintained a healthy profitability with an adjusted EBITDA margin of 21.4%, though this was lower than the 24.0% recorded in H1 2024, primarily due to a different product mix.

Water Technologies delivered the strongest performance with revenue increasing by 5.4% to €150.9 million and adjusted EBITDA surging by 45%, resulting in a margin expansion to 21.8% from 15.9% in H1 2024. This improvement was underpinned by strong pool-related revenue growth and included a positive one-off impact of approximately €1 million related to the fracking business line disposal.

The Energy Transition segment faced challenges with revenue declining by 17.4% to €43.2 million and adjusted EBITDA margin contracting to 2.5% from 6.5% a year earlier. Despite this, the company noted that Q2 showed volume recovery, although profitability was impacted by approximately €2 million in provisions accounted for in Q1.

The adjusted EBITDA breakdown by segment illustrates these trends:

Strategic Initiatives and New Markets

De Nora highlighted its expansion into new markets, leveraging its expertise in electrochemical technologies. The company has secured its first contracts in the PFAS (per- and polyfluoroalkyl substances) treatment market in the United States, with two municipal drinking water projects in Massachusetts and Pennsylvania to be delivered in 2026.

The company is also entering the sustainable lithium refining market, developing electrochemical technology to produce lithium from various feedstocks including rocks, brine, clay, and battery scrap. In H1 2025, De Nora secured its first contract to supply a plant to recover lithium from used batteries for a Japanese customer.

As part of its sustainability initiatives, De Nora is installing new photovoltaic plants at its facilities:

Green Hydrogen Projects Update

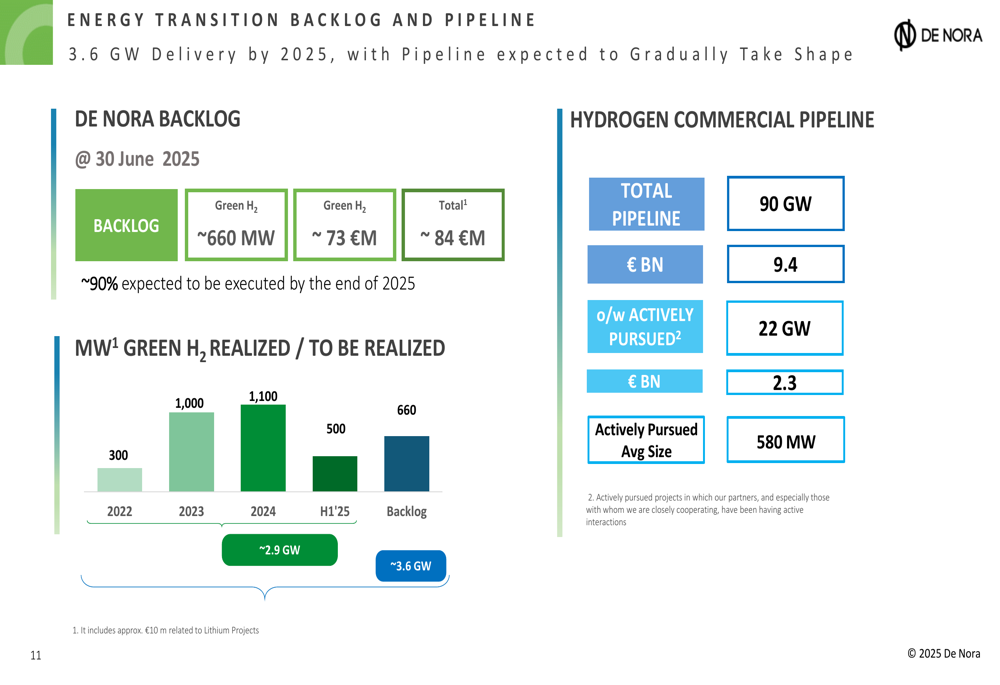

De Nora provided updates on its key green hydrogen projects, including the NEOM project in Saudi Arabia, which is the largest worldwide hydrogen project at 2.2 GW capacity. The project has reached 80% construction completion across all sites and is expected to be delivered by the end of August 2025.

The company’s green hydrogen commercial pipeline and backlog show significant potential for future growth:

The company is also making progress on the STEGRA project in Sweden, a 700+ MW initiative focused on green steel production, which is currently 25% complete and expected to be delivered by the end of 2025.

De Nora’s strategy in the energy transition sector includes:

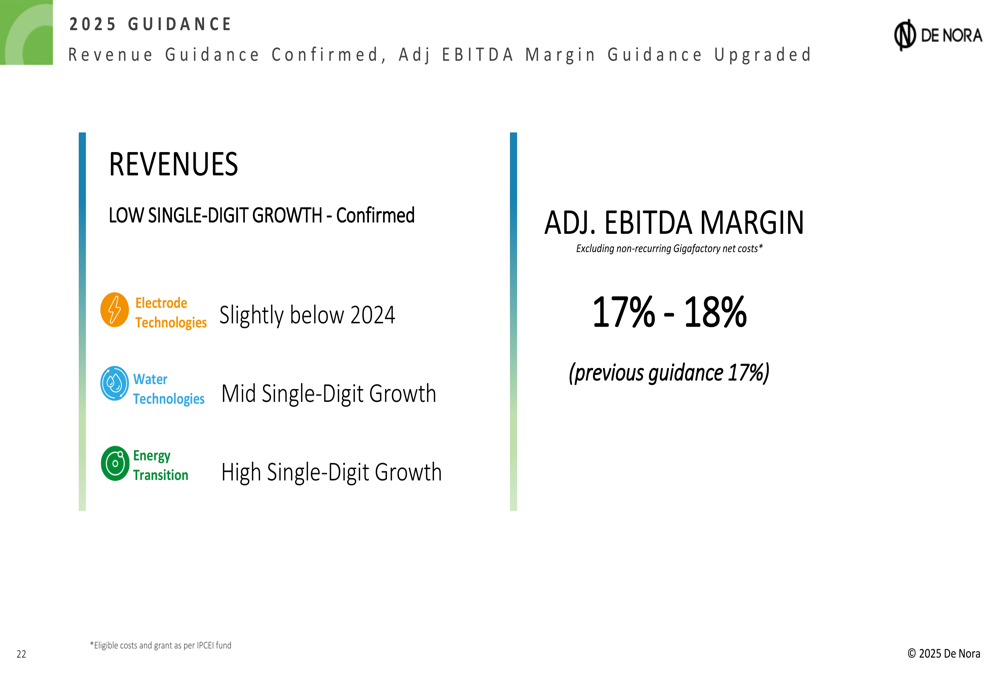

Outlook and 2025 Guidance

Based on the strong H1 2025 performance, De Nora upgraded its adjusted EBITDA margin guidance for the full year to 17-18%, from the previous target of 17%. The company confirmed its revenue growth guidance in the low single digits.

The segment outlook for 2025 is as follows:

The company’s backlog stood at €521.8 million as of June 30, 2025, compared to €558 million at the end of 2024. Approximately 61% of the backlog is expected to be deployed in 2025, with the remainder spread across 2026 (21%), 2027 (3%), and 2028+ (15%).

De Nora continues to pursue M&A opportunities in the Water Technologies segment to strengthen its position in the value chain and enter new segments, while also advancing strategic partnerships in the Energy Transition sector to accelerate market penetration across geographies and technologies.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.