NVIDIA launches Jetson Thor robotics computers for physical AI systems

Industrie De Nora SpA (BIT:DNR) presented its Q1 2025 financial results on May 14, 2025, highlighting solid performance in its core businesses despite ongoing challenges in its Energy Transition segment. The company reported a 6% year-over-year revenue increase to €200.4 million and an 8.2% rise in adjusted EBITDA to €39.4 million, with margins expanding to 19.7%.

Quarterly Performance Highlights

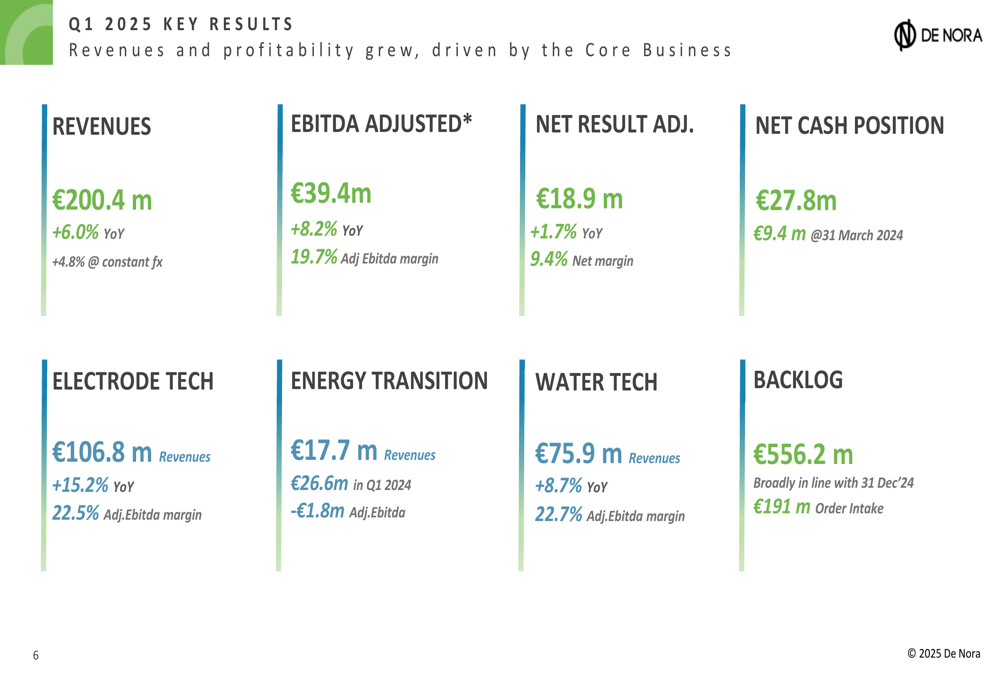

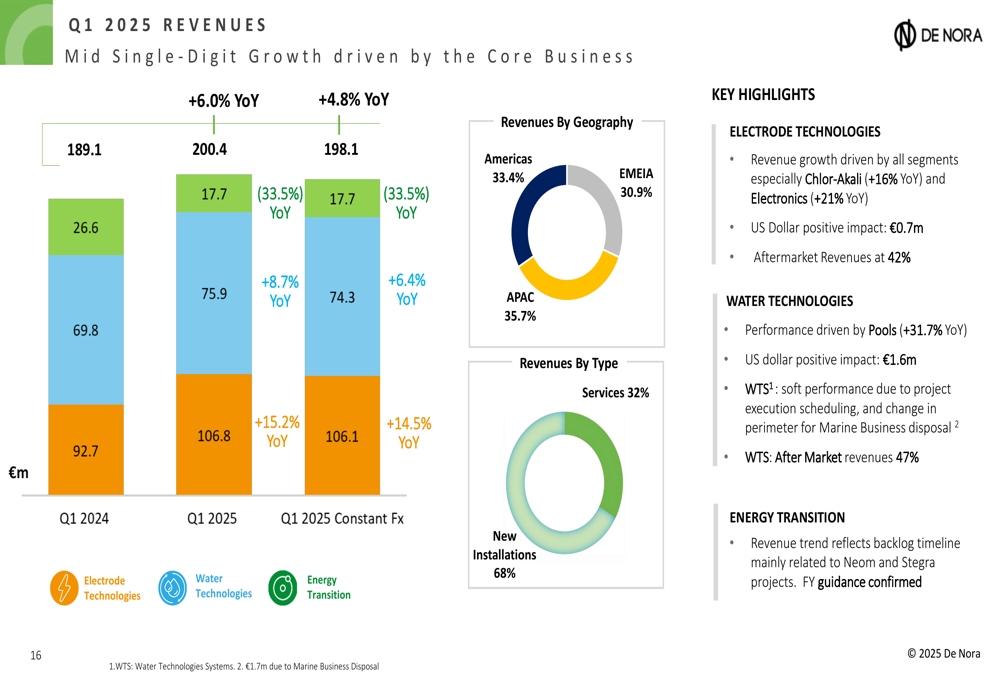

De Nora started 2025 on a positive note, with revenues reaching €200.4 million (+6.0% YoY, +4.8% at constant exchange rates). The company’s adjusted EBITDA grew by 8.2% year-over-year to €39.4 million, resulting in a margin improvement of 0.4 percentage points to 19.7%. Net adjusted profit increased by 1.7% to €18.9 million, representing a 9.4% net margin.

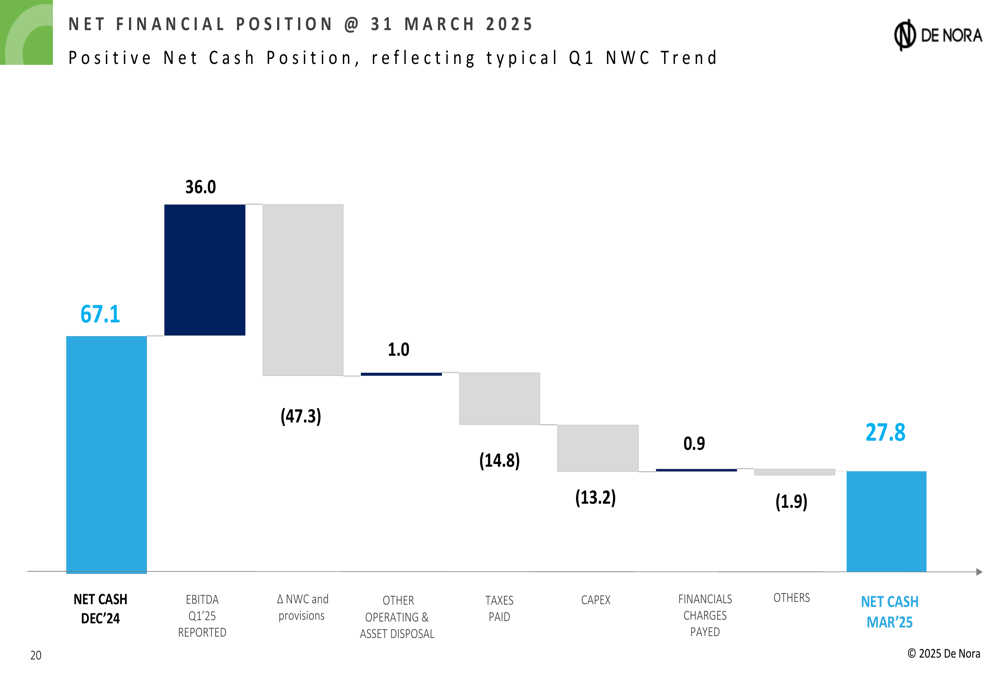

The company’s financial position strengthened considerably, with net cash reaching €27.8 million, a significant improvement from the €9.4 million reported on March 31, 2024.

As shown in the following comprehensive overview of key financial metrics:

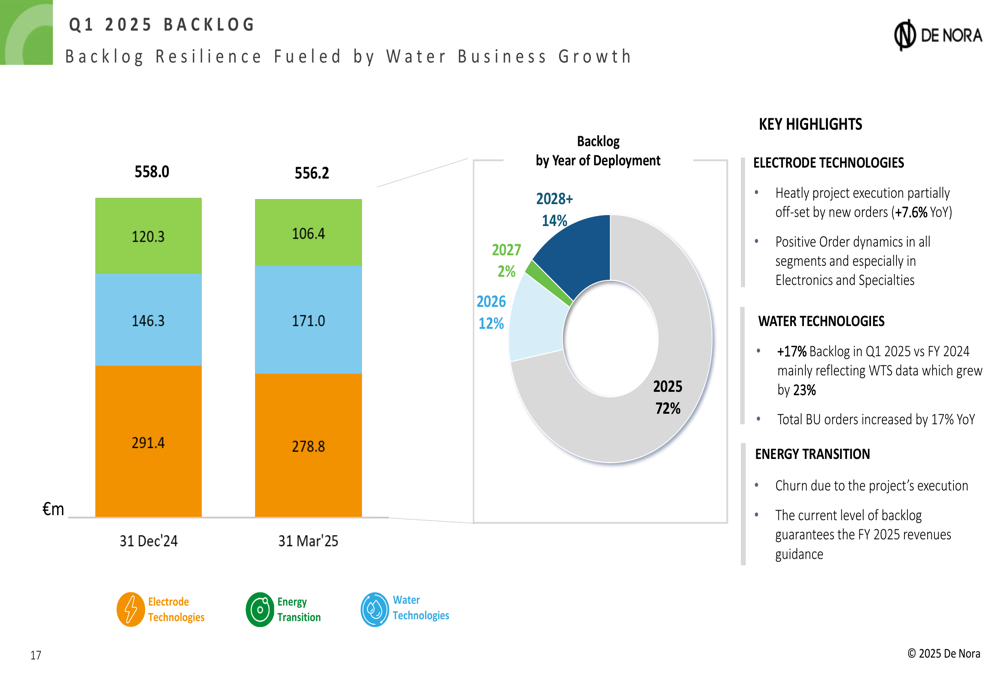

Order intake remained robust at €191 million, while the backlog stood at €556.2 million, broadly in line with year-end 2024 figures. The aftermarket segment continued to be a significant revenue driver, accounting for 42% of total sales.

Segment Analysis

The Electrode Technologies business delivered exceptional performance, with revenues increasing by 15.2% year-over-year to €106.8 million and an adjusted EBITDA margin of 22.5%. Order intake grew by 7.6% compared to Q1 2024, driven by a slight recovery in the Electronics segment and positive performance in Electrowinning.

The Water Technologies segment also showed strong momentum, with revenues rising by 8.7% to €75.9 million and an adjusted EBITDA margin of 22.7%. Order intake increased by 17% year-over-year, with particularly strong growth in the Pool (NASDAQ:POOL) business (+19%) and Water Treatment Systems (+16%).

The following slide illustrates the revenue breakdown by segment and geography:

In contrast, the Energy Transition business faced challenges, with revenues declining to €17.7 million from €26.6 million in Q1 2024, resulting in a negative adjusted EBITDA of €1.8 million. The company noted that revenue trends in this segment reflect backlog timeline execution, primarily related to the NEOM project in Saudi Arabia and STEGRA project in Sweden.

Despite these challenges, De Nora maintained that its Energy Transition pipeline remains steady at 94 GW (€8.9 billion), though new Final Investment Decisions (FIDs) are taking longer than expected.

The company’s backlog remains resilient, fueled by growth in the Water Technologies business:

Profitability Analysis

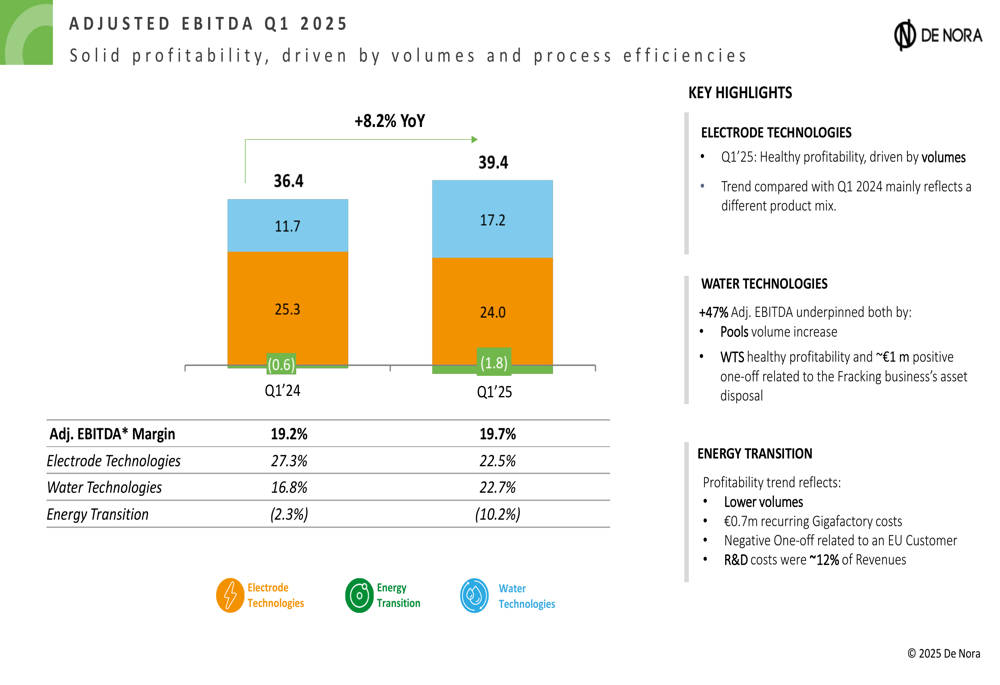

De Nora’s adjusted EBITDA growth of 8.2% outpaced revenue growth, indicating improved operational efficiency. The adjusted EBITDA margin expanded to 19.7%, with strong contributions from both Electrode Technologies (22.5% margin) and Water Technologies (22.7% margin).

As illustrated in the following EBITDA analysis:

Operating costs remained well-controlled, with COGS as a percentage of sales slightly improving to 64.7% from 64.8% in Q1 2024. SG&A expenses as a percentage of sales increased marginally to 14.4% from 14.3%, while R&D spending decreased to 1.8% of sales from 2.1% in the prior-year period.

The company’s net financial position improved significantly, as shown in this waterfall chart:

Strategic Initiatives

De Nora continues to invest in innovation and sustainability. The company inaugurated a new Innovation Center in Mentor, Ohio, focused on advancing product development and manufacturing capabilities for DSA electrodes and gas diffusion electrodes (GDEs).

The center, covering over 1,000 square meters and directly connected to the Mentor production plant, will develop technologies for fuel cells, alkaline water electrolysis, CO2 conversion, and specialty chemical production. This facility adds to De Nora’s existing five R&D labs across the US, Italy, and Japan.

On the sustainability front, De Nora is expanding its renewable energy capacity by adding 380 MWh of new photovoltaic plants and has joined the UN Global Business & Human Rights Accelerator program.

Forward-Looking Statements

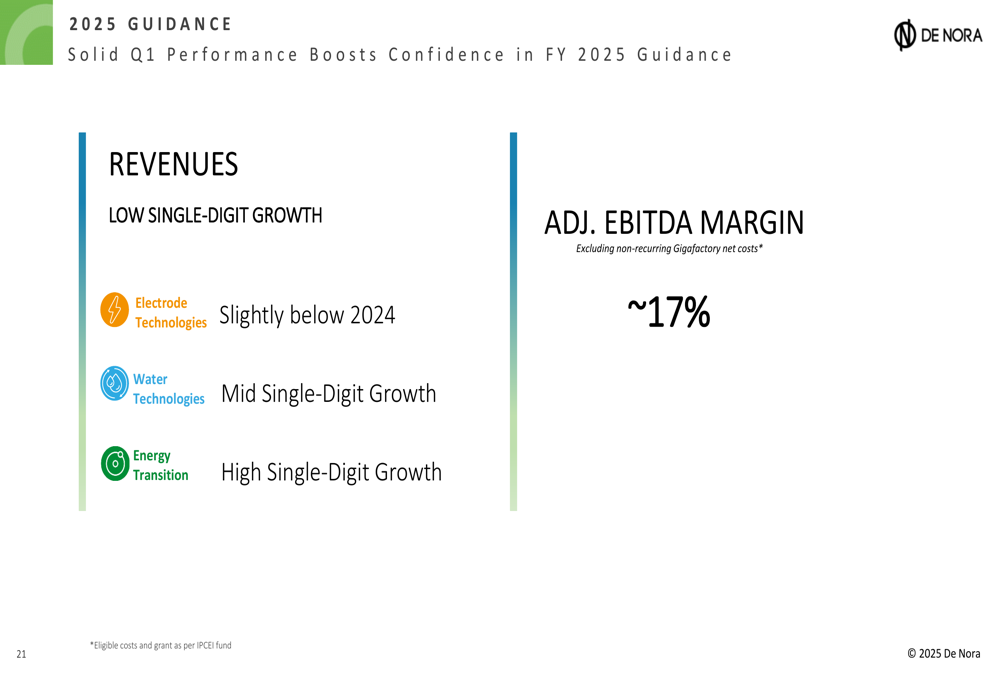

De Nora maintained its 2025 guidance, projecting low single-digit revenue growth and an adjusted EBITDA margin of approximately 17%. The company expects continued strength in its core Electrode Technologies and Water Technologies businesses, while visibility in the Energy Transition segment remains limited.

As shown in the guidance summary:

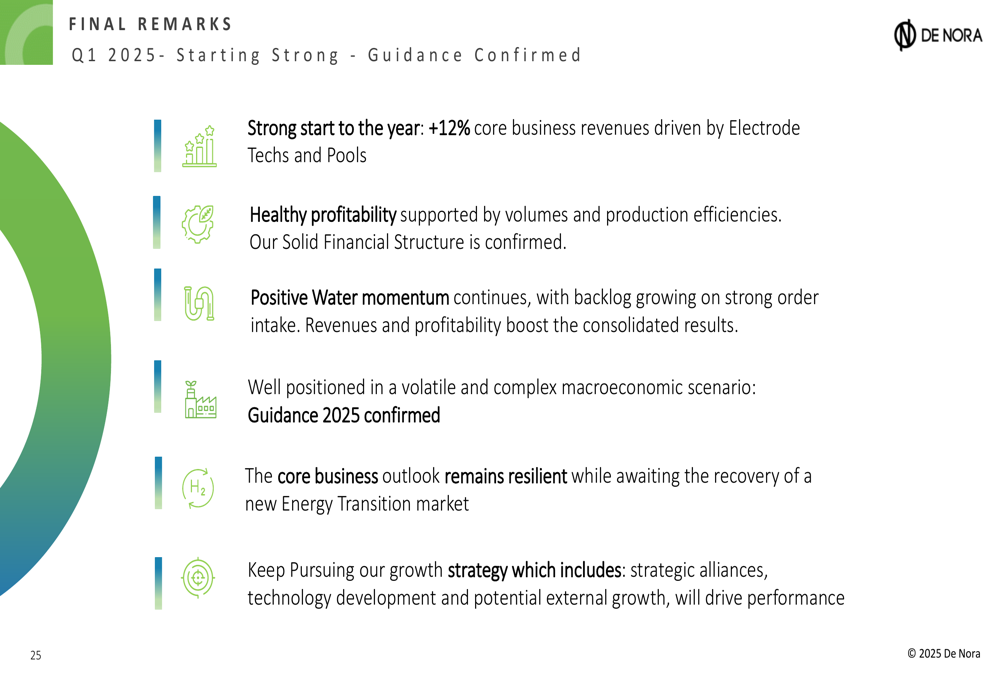

In its final remarks, management emphasized the company’s healthy profitability and solid financial structure, which positions it well to pursue growth opportunities through both organic initiatives and strategic alliances:

Market Context

Despite the positive Q1 results, De Nora’s stock has faced significant pressure in recent months. According to the latest data, the stock is trading at €6.89, close to its 52-week low of €5.52 and well below its 52-week high of €14.08. This follows a substantial decline after the Q4 2024 earnings release, when the stock dropped by 21.31%.

The market appears to be responding more to concerns about the Energy Transition segment’s performance and broader market conditions affecting the green hydrogen sector, rather than the solid results from the company’s core businesses. However, with its improved profitability, strong order intake in key segments, and solid balance sheet, De Nora maintains that it is well-positioned to navigate these challenges while continuing to invest in future growth opportunities.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.