EUR/USD likely to find a peak near 1.25: UBS

Introduction & Market Context

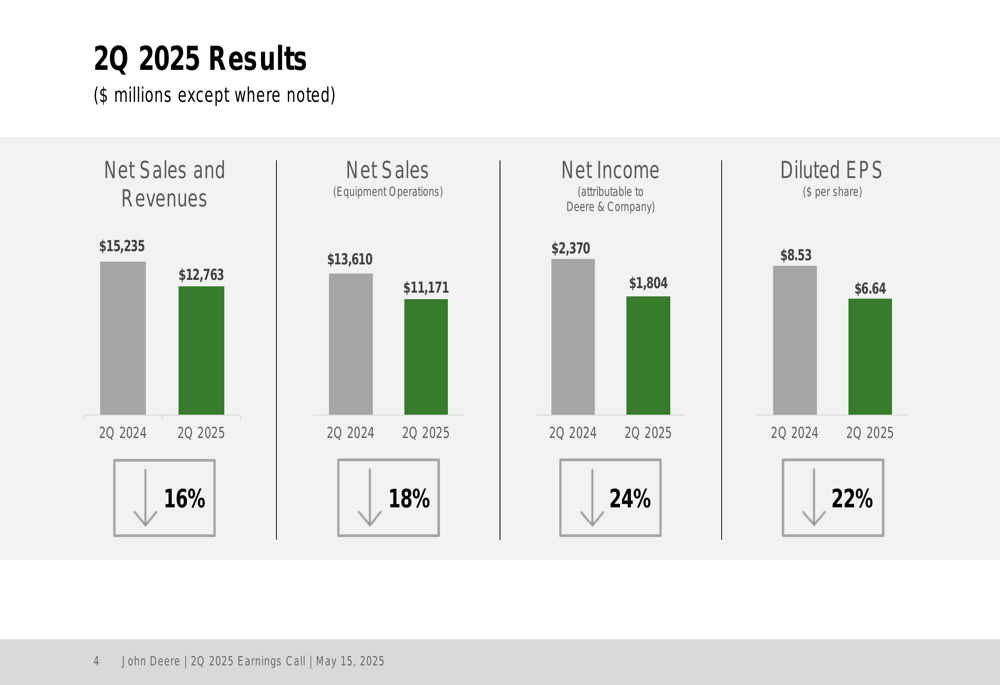

Deere & Company (NYSE:DE) reported a significant decline in its second-quarter 2025 financial results during its earnings call on May 15, 2025. The agricultural and construction equipment manufacturer faced considerable headwinds across most of its business segments, with total net sales and revenues falling 16% year-over-year to $12.76 billion.

In premarket trading following the announcement, Deere shares were up 1.01% at $502.50, suggesting investors may have anticipated worse results or were encouraged by the company’s optimistic full-year outlook despite current challenges.

Quarterly Performance Highlights

Deere’s net income attributable to the company fell 24% to $1.8 billion in Q2 2025, compared to $2.37 billion in the same period last year. Diluted earnings per share dropped 22% to $6.64 from $8.53 in Q2 2024.

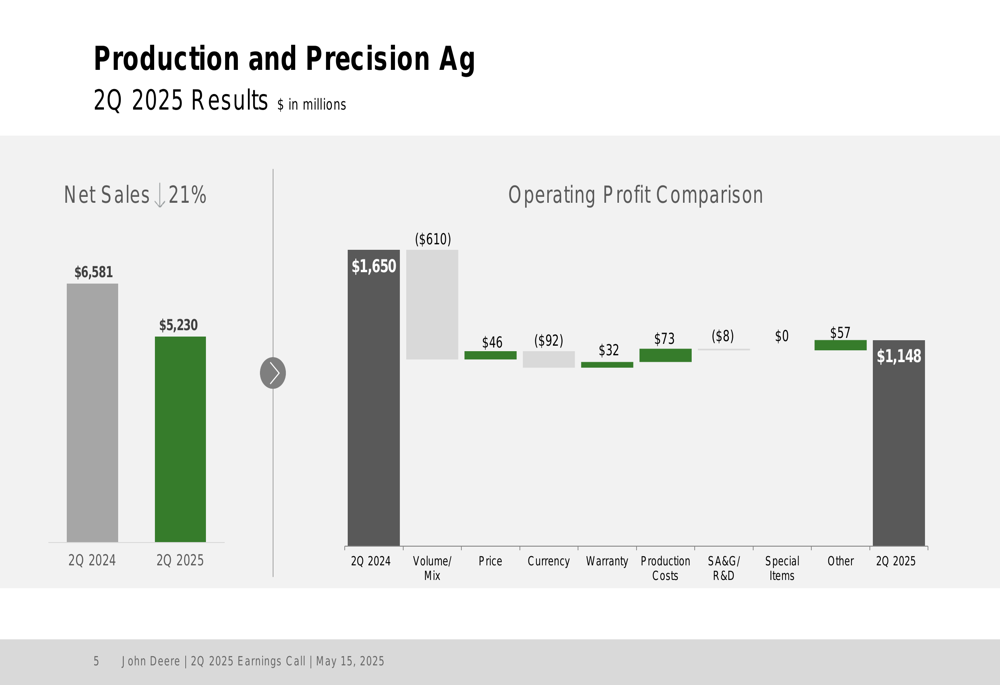

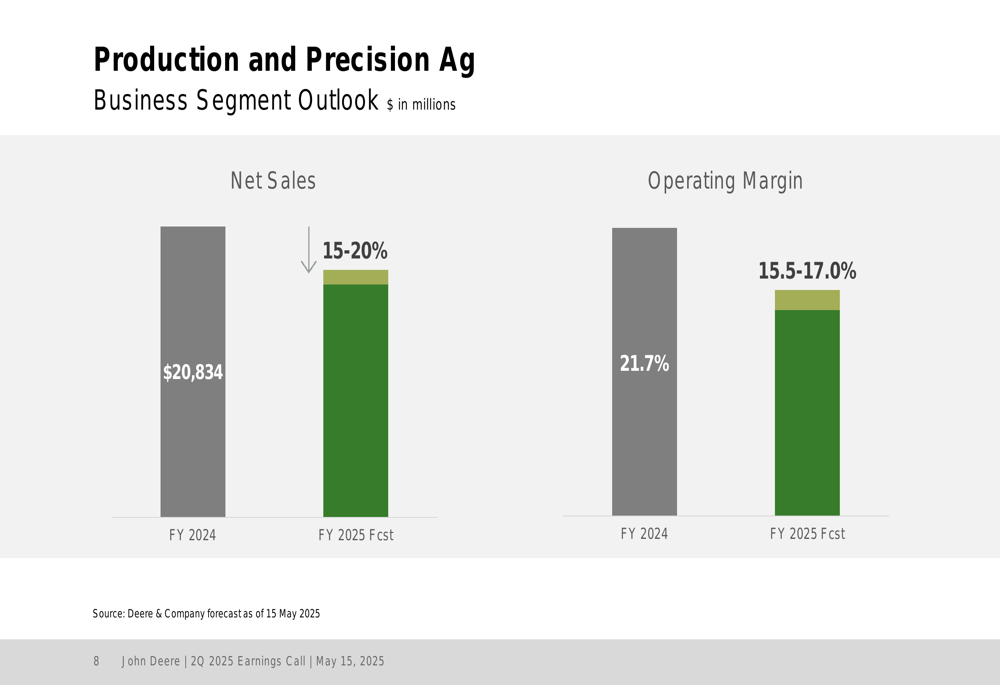

The Production and Precision Agriculture segment, Deere’s largest business unit, experienced a 21% decline in net sales to $5.23 billion. Operating profit for this segment decreased to $1.15 billion from $1.65 billion in Q2 2024, with negative impacts from volume/mix, pricing, and other factors outweighing positive contributions from currency and warranty improvements.

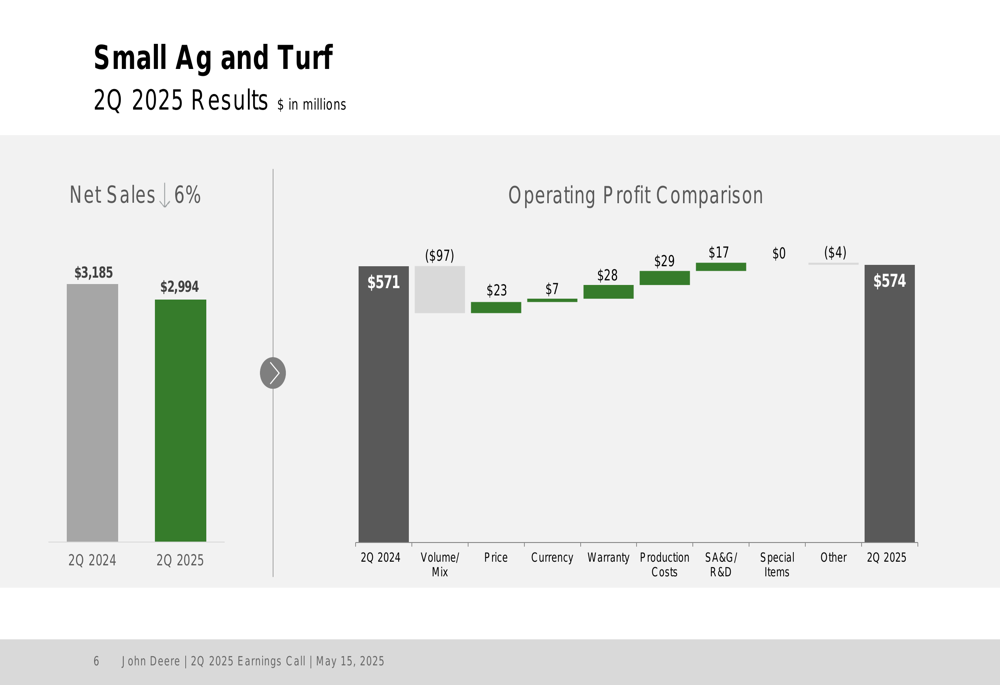

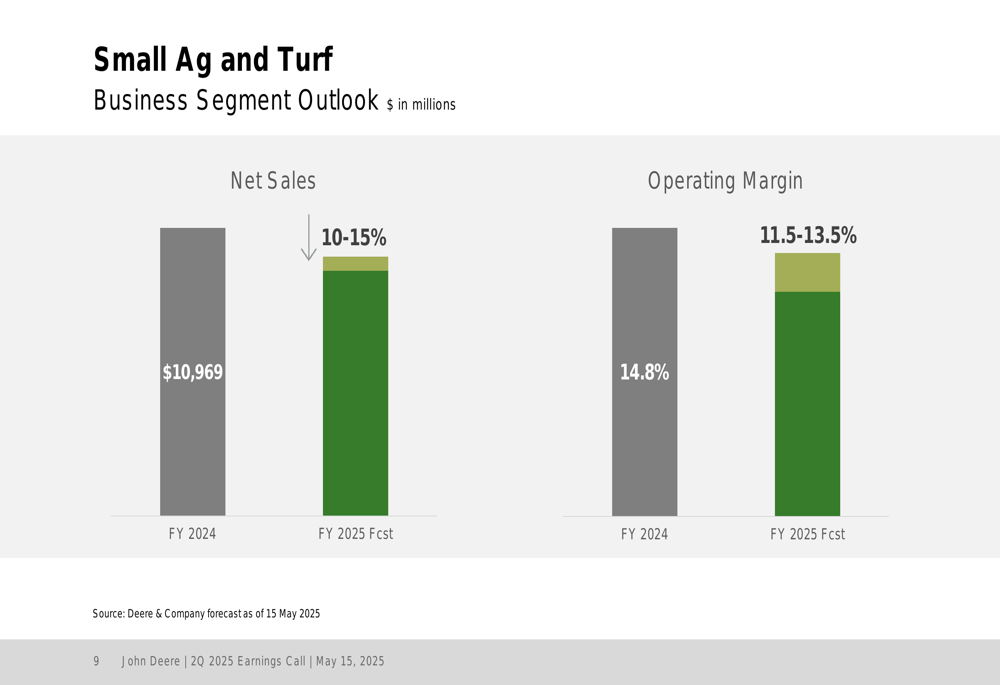

The Small Agriculture and Turf segment showed more resilience, with net sales declining only 6% to $2.99 billion. Despite the sales drop, operating profit for this segment remained relatively stable at $574 million compared to $571 million in Q2 2024, benefiting from positive contributions in volume/mix, pricing, currency, warranty, and production costs.

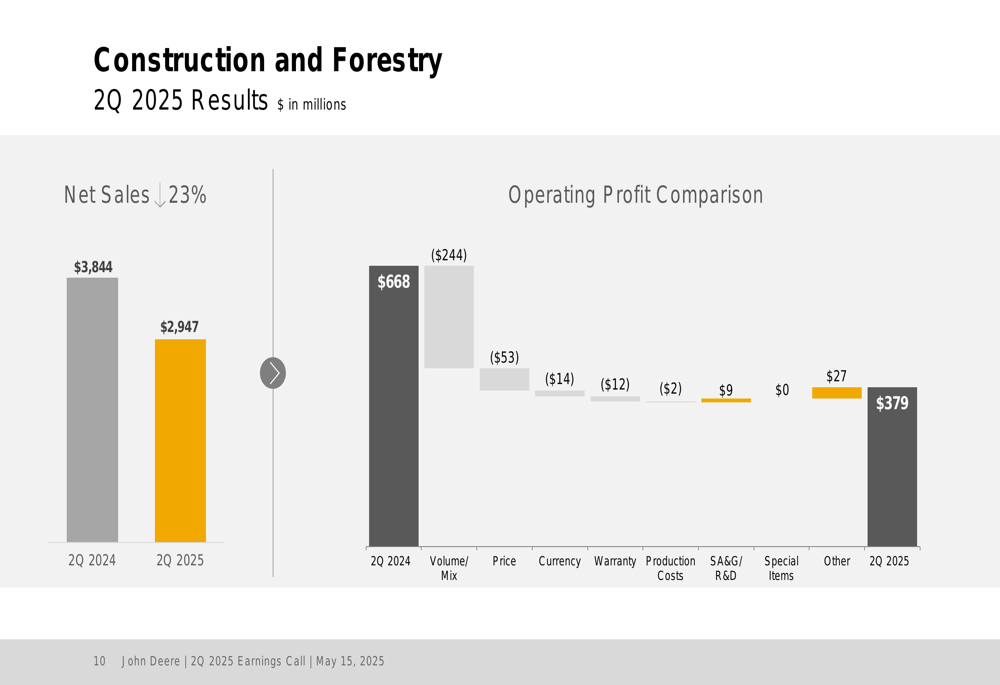

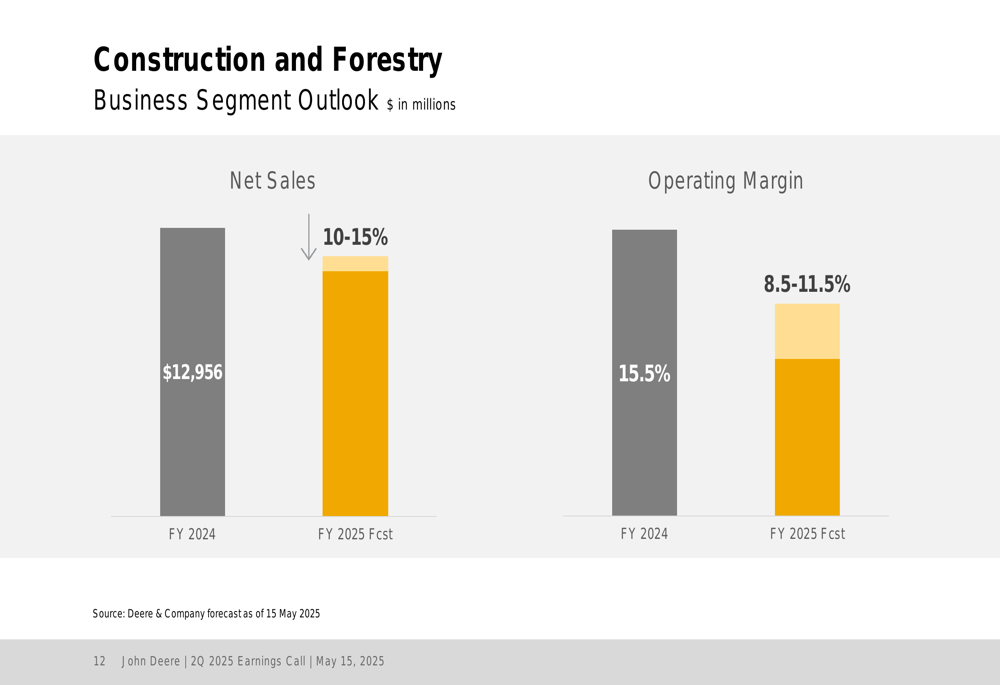

Deere’s Construction and Forestry segment reported the steepest decline among all business units, with net sales falling 23% to $2.95 billion. Operating profit in this segment dropped to $379 million from $668 million in Q2 2024, primarily due to negative impacts from volume/mix, pricing, and other factors.

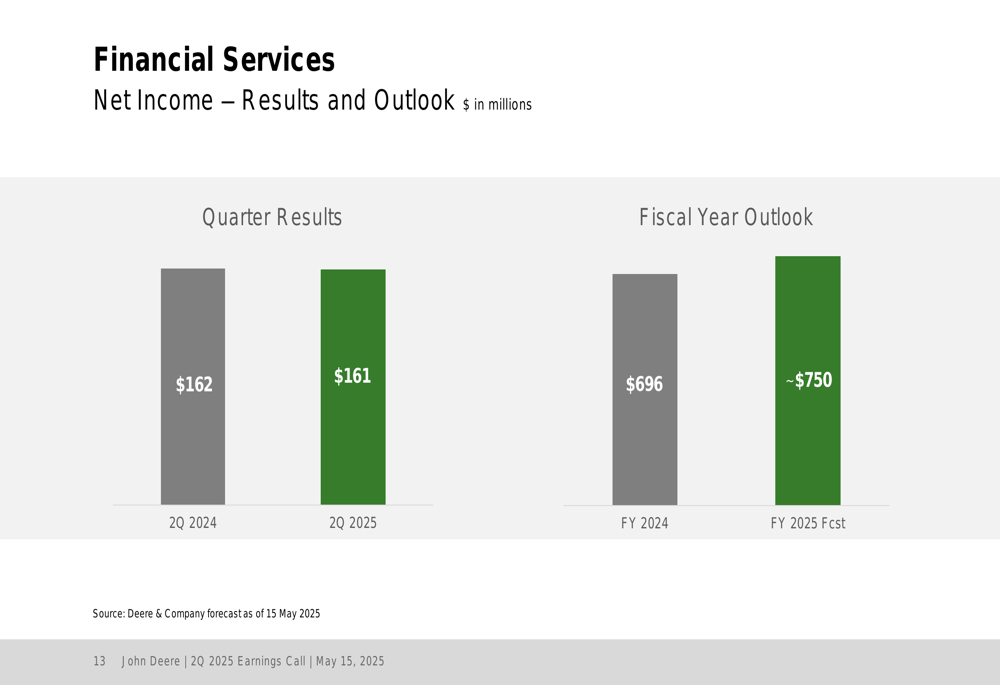

The Financial Services segment showed remarkable stability amid broader company challenges, with net income of $161 million in Q2 2025, virtually unchanged from $162 million in Q2 2024.

Industry Outlook

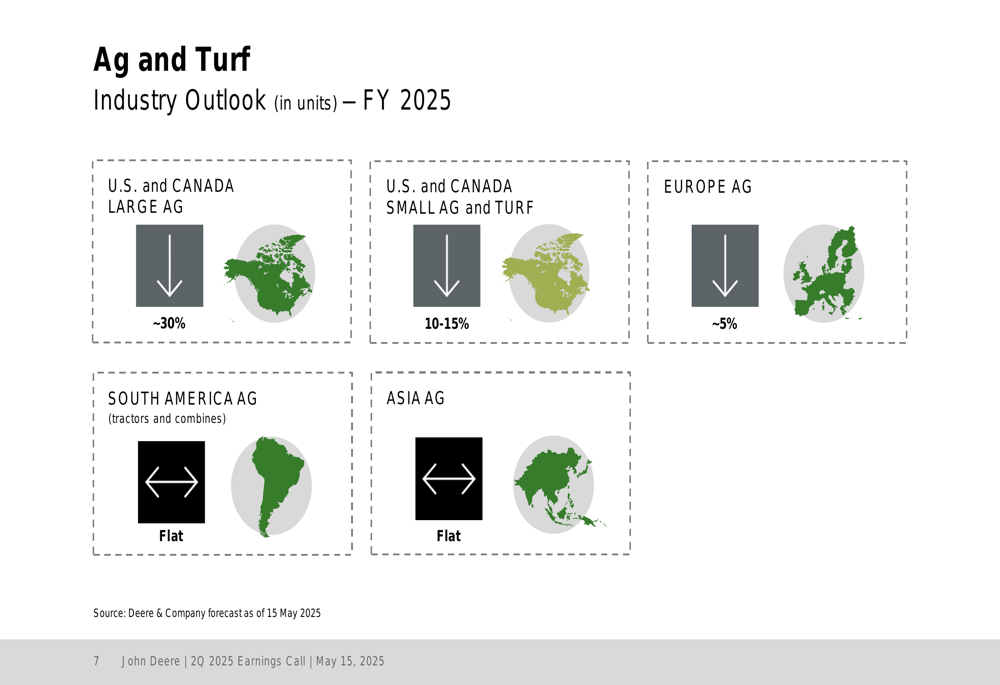

Deere’s presentation revealed a challenging industry outlook for fiscal year 2025, particularly in the large agriculture equipment market in North America, which is expected to decline approximately 30%. This significant contraction in Deere’s home market represents one of the most substantial headwinds facing the company.

In contrast, the small agriculture and turf equipment market in the U.S. and Canada is projected to grow 10-15%, providing some offset to the weakness in large equipment. European agricultural markets are expected to decline approximately 5%, while South American and Asian agricultural markets are forecast to remain flat.

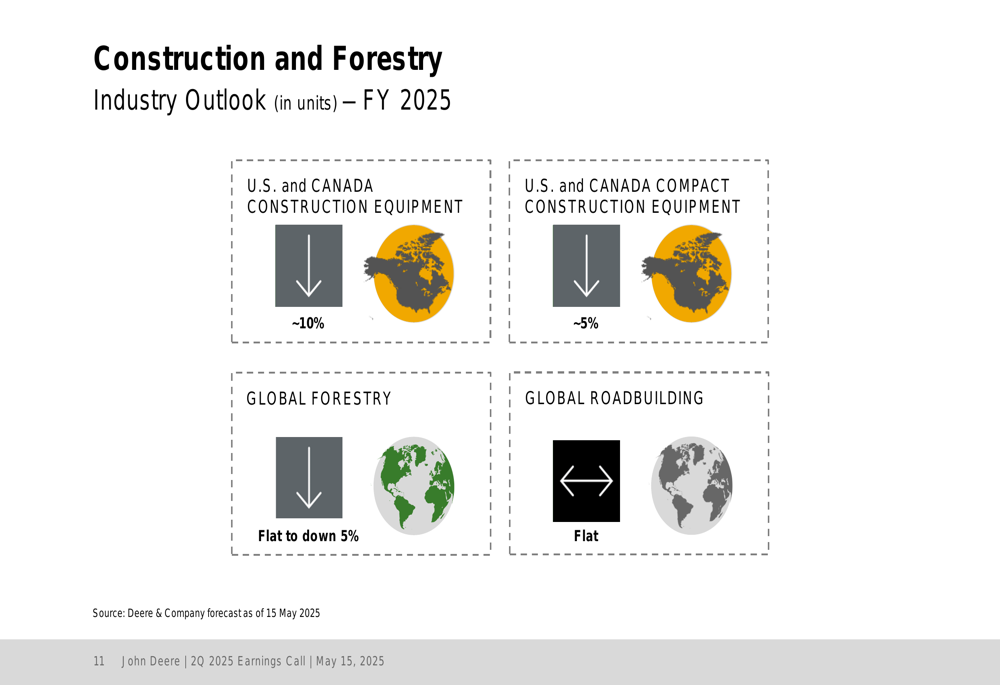

The construction equipment industry also faces challenges, with the U.S. and Canada construction equipment market projected to decline approximately 10%, and compact construction equipment expected to fall about 5%. Global forestry equipment is forecast to be flat to down 5%, while the global roadbuilding market is expected to remain flat.

Forward-Looking Statements

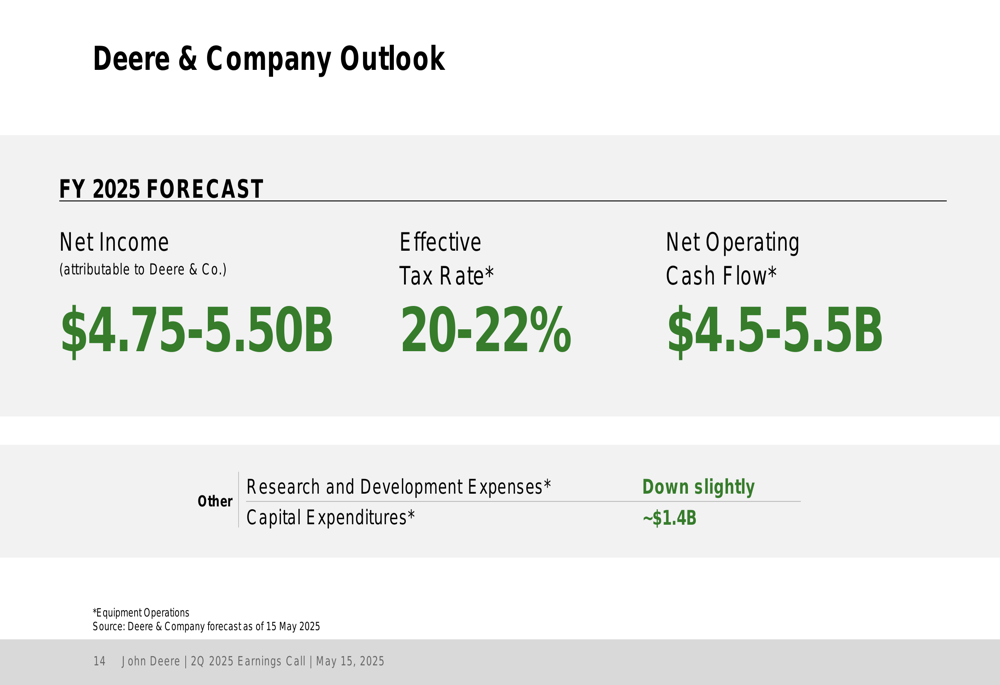

Despite the current quarter’s challenges, Deere provided an optimistic outlook for fiscal year 2025. The company projects net income attributable to Deere & Company between $4.75 billion and $5.5 billion, with net operating cash flow between $4.5 billion and $5.5 billion.

Deere forecasts significant sales growth across all segments for fiscal year 2025. The Production and Precision Agriculture segment is expected to see net sales growth of 15-20%, though operating margins are projected to decline to 15.5-17.0% from 21.7% in FY 2024.

The Small Agriculture and Turf segment is forecast to achieve net sales growth of 10-15%, with operating margins expected to decline to 11.5-13.5% from 14.8% in FY 2024.

Similarly, the Construction and Forestry segment is projected to deliver net sales growth of 10-15%, though operating margins are expected to decrease to 8.5-11.5% from 15.5% in FY 2024.

The Financial Services segment is forecast to generate net income of approximately $750 million in FY 2025, up from $696 million in FY 2024.

Strategic Initiatives

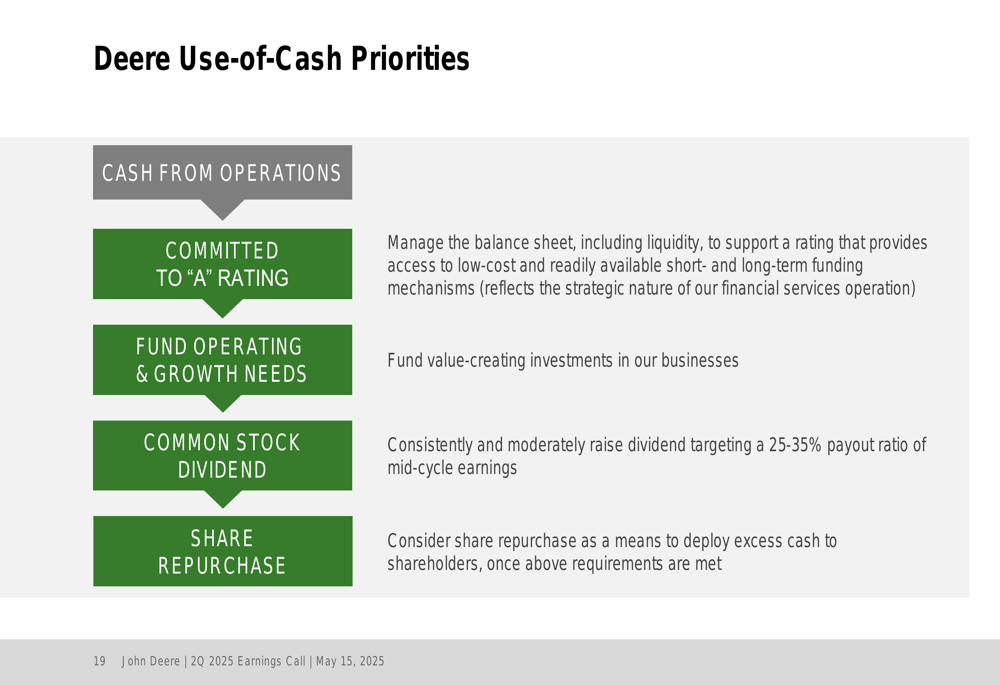

Deere’s presentation outlined the company’s use-of-cash priorities, emphasizing its commitment to maintaining an "A" credit rating to ensure access to low-cost funding. The company prioritizes funding operating and growth needs, followed by consistently raising its common stock dividend with a target payout ratio of 25-35%. Share repurchases are considered as a means to deploy excess cash to shareholders.

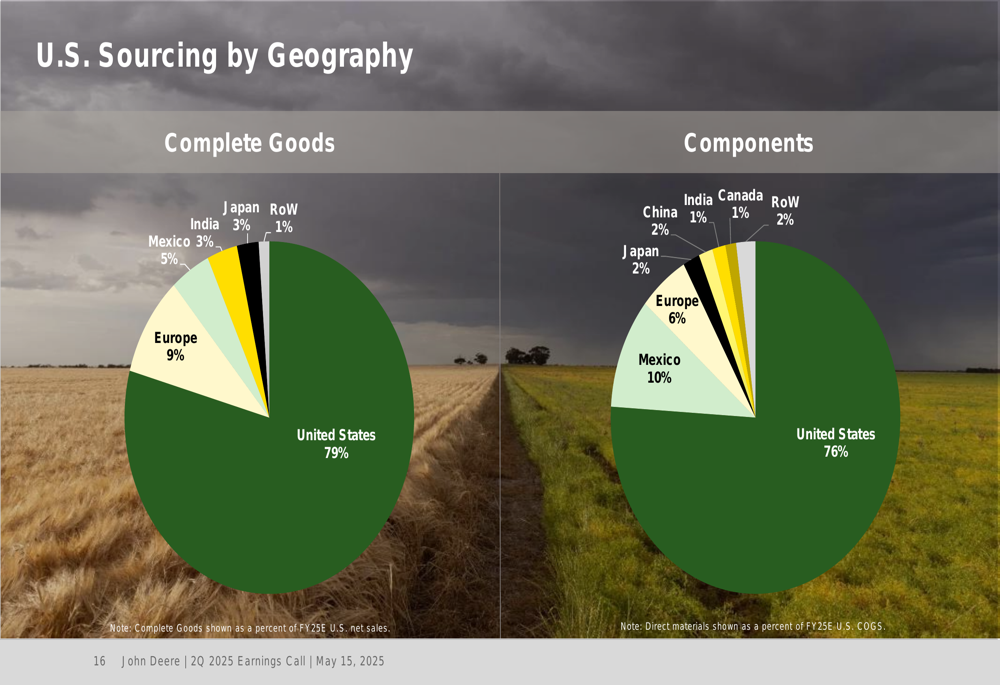

The presentation also highlighted Deere’s U.S. sourcing strategy, revealing that 79% of complete goods and 76% of components are sourced from the United States. This domestic sourcing focus may provide some insulation from international supply chain disruptions and potential tariff impacts.

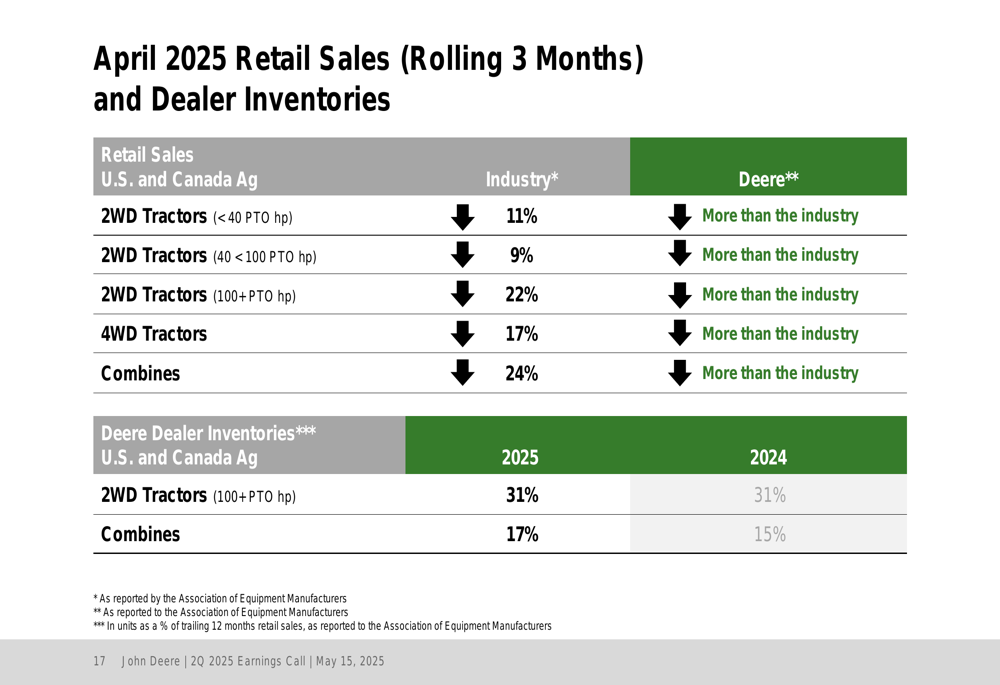

Recent retail sales data presented in the slides showed declines across most equipment categories in April 2025. In the U.S. and Canada, industry sales of large tractors, 4WD tractors, and combines were down significantly, with Deere performing worse than the industry average in these categories. This recent market weakness aligns with the challenging industry outlook presented for fiscal year 2025.

Deere announced it will hold a Brazil Investor Day on June 10, 2025, focusing on " Opportunity (SO:FTCE11B) | Foundation | Growth," suggesting the company sees significant potential in the South American market despite current challenges.

The company’s next earnings call is scheduled for August 14, 2025, when investors will be able to assess whether Deere’s optimistic full-year forecasts remain achievable given the current market headwinds.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.